By Terry Baucher*

Former Minister of Revenue Peter Dunne was right when he said last week that global co-operation was necessary to resolve the growing tax issues arising from the new wave of online tech companies such as Google, Facebook and ride sharing service company Uber.

It’s a huge problem, and also one where there are no easy answers.

Uber is just the latest example of the problems for tax jurisdictions when new companies exploiting the internet to achieve a global reach, collide with tax laws written decades ago around national boundaries. But even by the standards of other tech companies such as Google and Facebook, Uber’s model seems particularly ingenious.

Whenever someone in New Zealand uses an Uber driver, the fare is not immediately paid to the driver. Instead it’s remitted to a Dutch company, Uber B.V. which then pays 80% of the fare back to the Uber driver. Part of the balance is paid as a marketing fee ($1,061,018 for the year ended 31st December 2014) to Uber New Zealand Technologies Limited. The majority of Uber B.V.’s 20% cut is paid as a royalty to another Dutch company, Uber International C.V.

At this point, the so-called “Double Dutch” tax planning structure comes into play, under which any royalties Uber International C.V. receives from Uber B.V are tax free for Dutch purposes.

Furthermore, because Uber International C.V. has no employees and its headquarters is in the Bahamas, it technically derives no business income in the Netherlands. Uber is therefore able to accumulate tax free the vast majority of the royalties it receives from around the world.

It’s therefore unsurprising that Uber’s aggressive tax planning practices have come under fire here in New Zealand.

Another critic is the New Zealand Taxi Federation which in June last year warned the Ministry of Transport Small Passenger Services Review about the potential loss of GST revenue from unregistered Uber drivers.

The NZTF may be protecting its turf, but its point about the tax risk from Uber’s business model is valid. At present 20% of an Uber fare will escape the New Zealand tax net. Consequently, there is a fiscal risk if Uber was to capture a significant portion of the estimated $400 million a year taxi industry. (Interestingly, recent Victoria University of Wellington research indicates some Uber drivers may be taxi drivers looking to supplement their income).

What hasn’t been examined so much is why the likes of Uber adopt such complex structures. Arguably, they have little choice but to adopt aggressive tax planning if their American investors are to achieve any realistic returns.

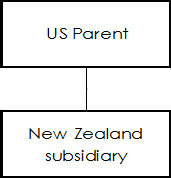

Consider the tax implications for an individual American shareholder in a “normal” structure such as the following:

How much would an individual shareholder in the United States finish up with after tax If the New Zealand subsidiary makes a pre-tax profit of $100,000 which it distributes as a dividend to its US Parent, which in turn paid it out as a dividend to the individual shareholder?

$6,487.

That’s an effective tax rate of over 93%. How?

The profits of the New Zealand subsidiary are taxed at 28%. The corporate tax rate in the United States is 35% and the top Federal tax rate in the United States for individuals is 39.6%. (We’ll ignore the effects of income taxes in States such as California for the purpose of this example). Applying these tax rates to a dividend of $100,000 results in the following:

| Pre tax profit in New Zealand subsidiary less income tax @ 28% |

$100,000 -28,000 |

| Net dividend distributed to U.S. parent company less U.S. corporation tax @ 35% |

72,000 -25,200 |

| Net income distributed as dividend to U.S. shareholder less U.S. income tax @ 39.6% |

46,800 -18,533 |

| Net after tax income of shareholder | $6,487 |

Such potentially high tax rates are the background to Uber’s tax planning and why multinationals devise elaborate strategies such as the Double Dutch structure to shift pre-tax income from overseas subsidiaries either directly to the parent company, or to a subsidiary in a tax haven jurisdiction. The numbers involved are eye-watering.

For example, In March this year American Fortune 500 companies, including the likes of Apple, Google and General Electric, were estimated to have US$2.4 trillion of “permanently reinvested” profits sitting in tax havens such as the British Virgin Islands.

The OECD’s Base Erosion and Profiting Shifting (“BEPS”) initiative is one answer to this aggressive tax planning. Once implemented, it is likely to increase the overall tax take from multinationals. However, the problem of the cascade effect of taxation resulting in very high effective marginal tax rates will remain.

Reducing corporate tax rates therefore seems a reasonable approach. And worldwide the trend is for lower corporate tax rates. But how low? An IRD/Treasury working paper prepared for the 2009 Tax Working Group noted:

“Under the stringent assumptions required for the Production Efficiency Proposition to hold, a small open economy should levy no tax on capital invested in the economy which would imply a zero company tax rate.” ( See here, Appendix A, page 35)

A zero company tax rate? Good luck with getting voters to accept that.

One other alternative to deal with the cascade effect of tax would be to fully credit the tax paid in an overseas jurisdiction in a similar way to the current imputation or franking credit regime.

Unfortunately, even between such closely connected economies as Australia and New Zealand or the European Union, mutual recognition of tax credits has proved impossible to implement. After several European Court of Justice decisions required countries to provide imputation credits to non-residents where imputation credits were provided to residents, European countries began abandoning imputation regimes, concerned about the potential cost to their tax base.

Similarly, the stumbling block for recognition of imputation credits between Australia and New Zealand is the potential fiscal cost for Australia. The Australian Productivity Commission estimated this to be US$353 million per annum in April 2015.

If two such integrated economies as Australia and New Zealand cannot agree on mutual recognition of imputation credits, there is little chance of a similar initiative working worldwide.

Although the general mood of the public and tax authorities is against aggressive tax planning by Uber and other multinationals, BEPS is not likely to change drastically the economic imperatives for multinationals.

Zero company tax rates are politically unacceptable, so we can therefore expect to see ingenious tax planning by multinationals to continue for a long time yet.

*Terry Baucher is an Auckland-based tax specialist and head of Baucher Consulting. You can contact him here »

26 Comments

I don't have a problem with it. They remain within the existing laws of the land. They are simply running their business in the most efficient manner possible, legally. Whether it is a grey area or not, until governments worldwide decide to come to an agreement or even a single government can create new tax law that tackles this kind of thing we only have our politicians to blame.

These companies hire very smart people to design these company frameworks, I'm sure those same people could probably design tax laws that would help to solve many of those issues but government pay vs. private sector doesn't compare.

Well I do have a problem with it. The unfortunate side effect is to severely disadvantage your own domestic companies. We have foreign companies competing with a "tax optional" advantage over our own "tax compulsory" companies. Good luck expecting our businesses to grow with that sort of a handicap.

We should either completely do away with company tax or institute some sort of "license to operate" for foreign outfits with a contribution to the running of this country at a similar rate to the company tax. If Heinz Wattie or Keirin Breweries or Vodafone don't like it then that's just too bad; we are quite capable of brewing beer, making tomato sauce or running a phone company without them as we do now and have done in the past.

Your problem is with our existing tax laws.

Totally agree JK should stop disadvantaging NZ owned tax paying businesses. AND stop delivering the sound bite that he's waiting for OPEC, which is like that Samuel Becket play "Waiting for Godot"!

Hi Terry,

Hope all is well with you.

Your Uber example is curious (as was the initial reporting around it at the time).

"Whenever someone in New Zealand uses an Uber driver, the fare is not immediately paid to the driver. Instead it’s remitted to a Dutch company, Uber B.V. which then pays 80% of the fare back to the Uber driver. Part of the balance is paid as a marketing fee ($1,061,018 for the year ended 31st December 2014) to Uber New Zealand Technologies Limited. The majority of Uber B.V.’s 20% cut is paid as a royalty to another Dutch company, Uber International C.V."

Not to say you don't have a point. But the actual figures that one needs are missing, or at least have been replaced with percentages. Without knowing what there real revenue is, one cannot conclude, or at least support the conclusion that there is any significant tax shift happening at all.

What was Ubers total revenue in NZ for the 2012? year?

Thanks and regards

Edgie

Hi Edgie, thanks for your comment. What's Uber's total revenue in New Zealand? Good question and the short answer is we don't know.

The fee Uber NZ received of $1,061,018 for the year ended 31st December 2014 is a marketing fee and has no connection to the Uber fares earned in New Zealand. This is another of the problems with the tax planning of Uber and other tech companies, it's very difficult for tax authorities to get a handle on the potential loss of revenue because the structures are so opaque. But if Uber fares represent 1% of the estimated $400million taxi industry then that would equate to $4 million, 20% of which would be $800,000. Not a large number but over time it could be significant. Then there's the potential non-compliance effect in relation to the 80% remitted back to the Uber drivers in New Zealand.

Thanks again, Terry

1% you are joking right..... Uber is half the price of a normal cab i would be surprised if the figure wasn't 10-20% at least

From another angle. Uber operates a non cash system. I imagine it would be fialry simple for Uber to identify drivers who keep 'cancelling' fares and take and pocket cash. The rest of the traditonal tax industry I suspect not so good at this...seems to be rife with cash fares and gst non payment issues. So might we get a higher tax take from Uber?

Now that is where a FTT comes into play. Instead of income tax if a transaction tax was put on both deposits and money sent overseas then this rort could be minimised. That is the only way these international companies can be made to pay taxes.

Nah. Income tax works just fine.

Just don't allow deductions. Just like individuals. Time for a level playing field!

If you want a level playing field then you wouldn't make employers do all the associated book work and compliance required with the income tax model.......income tax model like GST is outdated and doesn't serve either the Government or the people well!!!

Are you sure your tax calculations are correct?

Most countries allow a tax credit for taxes paid on income derived in a foreign country. Similarly, it is normal to allow some form of credit to a shareholder on dividends where those dividends relate to income that the company has been taxed on (e.g. in NZ we have an imputation credit account); Both these regimes (i.e. foreign tax credits and imputation credits) help avoid double taxation. Your example has triple taxation which is why I question its accuracy.

I understand from a NZ stand point we don't tax dividend income from a foreign subsidiary. Rather any income of the parent is determined under the Controlled Foreign Company regime which allows a tax credit for foreign tax paid by the CFC as well as imputation credits for tax paid on any excess income by the NZ parent. This avoids double taxation (let alone triple taxation).

Never mind the tax calcs, they need to work on basic math;

$46,800

-$18,533

=$6,487

Might want to try that again...

Maths, as in short for mathematics, i.e. more than one solitary equation.

Here’s what Apple CEO Tim Cook had to say about it in a long interview published this weekend in the Washington Post:

We’ve said at 40 percent, we’re not going to bring it back until there’s a fair rate. There’s no debate about it. Is that legal to do or not legal to do? It is legal to do. It is the current tax law. It’s not a matter of being patriotic or not patriotic. It doesn’t go that the more you pay, the more patriotic you are. Read more

The government's of the world really are cr*p at designing, implementing, and enforcing tax law, aren't they.

There are any number of tax rorts being managed by foreign companies in NZ.

We sell a productive industry eg a pine forest and plywood mill. The product is sold at close to a loss to their sister Co back in the homeland who then make the profit off shore.

Then there's the telephone technicians recruited from 3rd world country, employed at low pay that kiwi technicians won't work for, subsidized by NZ taxpayers with WFF benefit and again the profits go offshore.

Not to mention that we rob the 3rd world country of their skilled labor.

And then we call it foreign investment and say its a wonderful thing.

i have a problem with it....

old laws trying to deal with new industries.... common sense tells me the way to rectify it is to update the laws....and new scheme should need IRD approval....

The way government departments work under national that approval could take years and by that time the tax law can be amended to counter the new scheme.

If you have an APT tax then none of the problems can exist so in effect politicians and bureaucrats don't want this issue to change........or it would have been done!!

Ireland seem to thrive (ie run a solid current account surplus), on 12.5% company tax, so that is worth a try. We, on the other hand, have failed miserably and have run a current account deficit since 1973. In order to put petrol in our tanks we have been selling the country to overseas buyers ever since.

On a wider note, we are completely stupid in our attitude to business. Businesses are our customers, whether as individuals selling our labour, or as government selling our location in return for the tax revenue. Most of the return from hosting a business here is in the income it pays to our residents, from this point of view corporation tax is counterproductive as it basically says:

"Sod off, we don't want your type here".

Hard to imagine a dafter system, really.

NZ is incapable of collecting taxes efficiently all the costs of collection are lumbered onto business and all the IRD does is tick a box, banks the tax or supplies the refund. The costs to business for this inefficient organisation are enormous..........once the Government has its hands on the loot they then disperse it to another inefficient organisation like a school, hospital, WINZ etc to deliver more inefficient so-called services...........

NZ seems to have a business bashing media who constantly drop feed the populace poor quality information.........

The closest thing we have to investigative journalism is a staunch National supporter, Mr Paul Henry who is blind in one eye and can't see out the other.

Yes - National seem to have 'Groomed' quite a few high profile media types. Is this them front running spin for their ""at the end of the day" lets do nothing as the populace are all dumbos" positions?

Whoever controls the media, controls the mind.

Jim Morrison

The should do payment solely in bitcoins, which will further confuse the tax systems. The thing is that tax systems around the world are so slow to adapt.

For Uber shareholders its great. For the country they operate in its tax avoidance, and for the non Uber cab drivers locked into the country's of operations tax model, it is clearly anti-competitive.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.