By Jacob Shapiro*

For all the optimism surrounding low unemployment rates and record-high real median income, there are some signs that something is rotten in the US economy. This isn’t wholly surprising – economic health tends to be cyclical, and the US is due for a recession. But when the next recession comes, there’s reason to believe it won’t be business as usual. The structural problems that led to the 2008 financial crisis haven’t been fixed. If anything, they’ve gotten worse.

In January, we forecast that the signs of just such a recession would emerge by the end of the year. And emerge they have. The yield curve between short-term and long-term US Treasuries is the flattest it has been at any point in the past 10 years. One of my colleagues, Xander Snyder, wrote an excellent piece last week on this very subject, and I encourage you to familiarize yourselves with it if you have not already done so.

A flattening yield curve, as he points out, is a problem in its own right, as is a declining prime-age labour force unable to secure adequate wages. But there are other longer-term forces at work that threaten to make what should be a minor cyclical recession a much more painful and prolonged affair. The two most consequential of these forces are increases in total household debt and the continued growth of wealth inequality within the US economy.

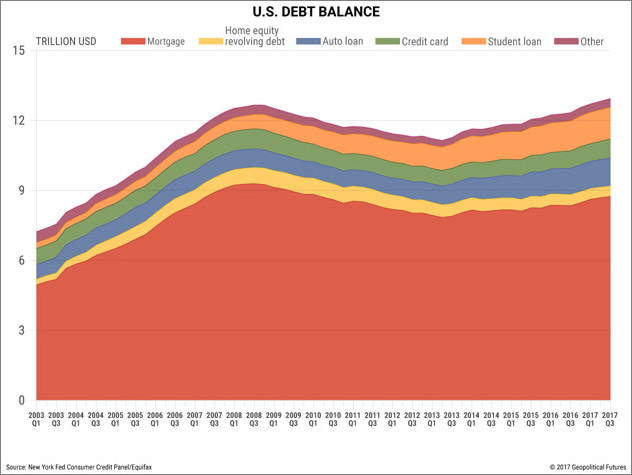

Household debt in the United States is now almost $13 trillion. That figure exceeds total household debt at any point during or in the recovery period after the 2008 financial crisis. Housing debt has crept back to pre-2008 levels. Credit card debt has reached pre-2008 levels too. Student loan debt has skyrocketed by 134 percent since the first quarter of 2008 (about 9 percent on average per year).

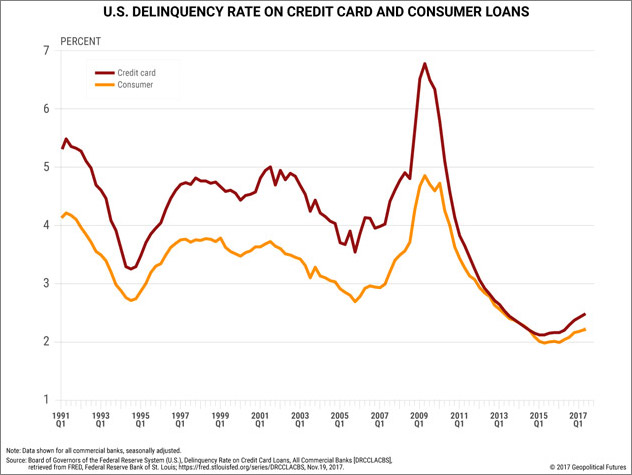

Increased household debt, though, doesn’t mean the end is nigh; it just means people are borrowing more money. Still, problems arise when people default on credit card and consumer loans. In the second quarter of 2017, the delinquency rate on credit card loans was 2.47 percent and on consumer loans was 2.21 percent. Low though these rates may be, they are trending upward.

Last month, shares of JPMorgan Chase and Citigroup fell on the news that both banks had increased their reserves for consumer loan losses – just under $300 million for JPMorgan Chase and just under $500 million for Citigroup. Put simply, American consumers are beginning to spend beyond their means.

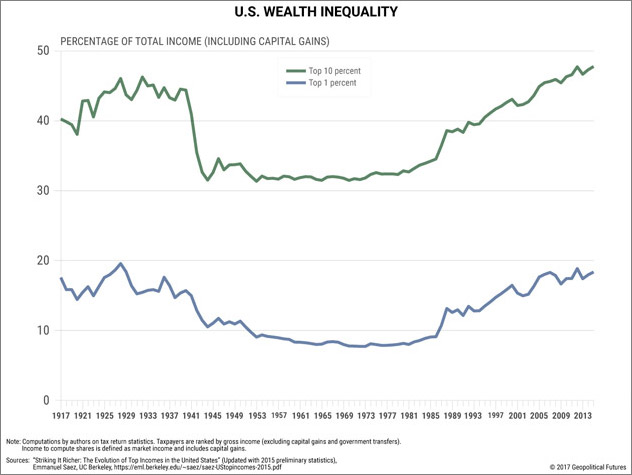

More serious than higher household debt, though, is increased income and wealth inequality in the United States since the 1970s. In 2015, the top 10 percent of all US earners accounted for just under 49 percent of total income – a share greater than at any time during the Great Depression. The top 1 percent accounted for 20 percent of total income.

This kind of disparity is a refrain in US economic history. It characterized the Gilded Age of the late 19th century as well as the decade or so before the Great Depression. Both were eras of immense wealth generation that benefited only the top, and both were rampant with speculation – the railroads and oil in the Gilded Age, the stock market in the Roaring Twenties. Today’s inequality is statistically more pronounced than during both of those times in history.

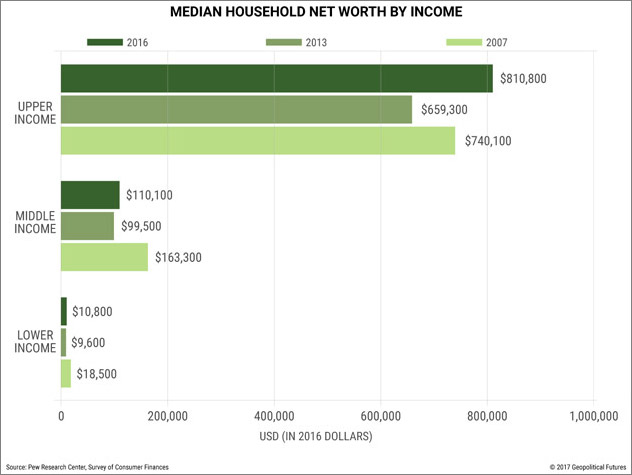

Wealth inequality was already increasing before the 2008 financial crisis, but what happened in 2008 has exacerbated the problem. According to the Pew Research Center, only upper income families have recouped the wealth they lost during the financial crisis. Median wealth was roughly 40 percent lower for lower-income families in 2016 than it was in 2007. It was roughly 33 percent lower for middle-income families. The median wealth for upper-income families, however, grew by 10 percent.

The US economy may have recovered in terms of top-line figures, but middle- and lower-income families have not. For those hardest hit, the tales of recovery ring hollow.

If that is the case, then how is it that real median income – one of the most important economic indicators we use to assess the health of the US economy – is so high? When we first forecast the coming crisis of the American middle class in 2011, median household income, adjusted for inflation, was lower than it was in 1989 or in 2000. The subsequent rise in real median income is a sign that the middle class has stabilized, right? Well, not really. Real median income can rise even as the gap between those above and below the median widens.

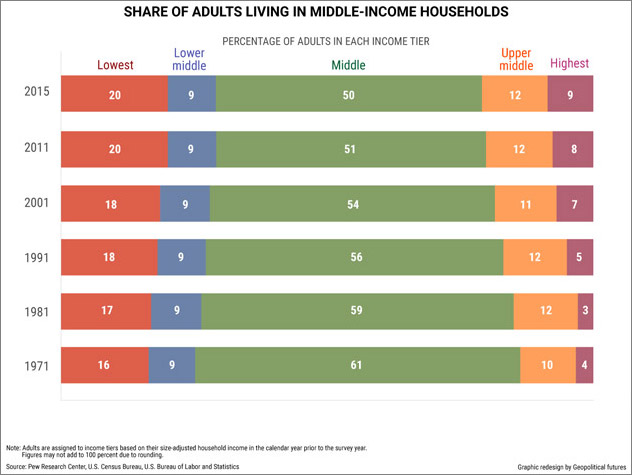

For example, the share of adults living in middle-income households has fallen since 1970. That year, 61 percent of adults lived in a middle-income household. In 2015, that number had fallen to 50 percent. The share of those living in a low-income household increased by 4 percent, and the share of those living in an upper-income household increased by 7 percent. The underlying problem is wealth inequality, and real median income does not necessarily capture wealth inequality.

And in 2017, real median income doesn’t go nearly as far as it used to. In the 1950s, the median cost of a home was a little more than double a family’s average annual income. A car was just under half of a family’s average annual income, according to data from the US Census Bureau and the US Department of Commerce. Today, it costs an average family about four times its average income to buy a house, and almost two-thirds its annual income to buy a car. A majority of households in the 1950s, moreover, were single-income households. By the end of that decade, the husband was the sole income generator for 70 percent of American households.

Analysis performed by Pew in 2015, based on the last US census, estimated that in 2012, 60 percent of American households were dual-income households. The purchasing power of the real median income has decreased even as US households have added a second breadwinner to the home.

For the past 40 years in the US, the rich have been getting richer, the poor have been getting poorer, and the middle class has been disappearing. The crisis of 2008 was a global phenomenon, but in the US, it was also an episode in an era of increasing inequality that began in the 1970s. The American dream was never about just making ends meet – it was about social mobility and giving your children a better life than you had growing up. That is beyond the means of an increasing number of US households. When the next recession comes, it will come as inequality reaches new heights, and if US history is any indication, that will translate into massive political change.

-------------------------------------

*Jacob Shapiro is director of analysis at Geopolitical Futures. This article was first published by Mauldin Economics, and is used with permission.

31 Comments

The bubble economy is set to burst, and US elections may well be the trigger

http://www.scmp.com/comment/insight-opinion/article/2114248/bubble-econ…

unfortunately this story wont have a fairy tale ending

A headline and article worthy of Zerohedge :-P

The tax cuts about to benefit the 1% ers will add fuel to the political fire and social unrest. The US is run by the Koch brothers and friends, they need a revolution.

2018 - The year of the crash. If this article comes as something new to whoever may read it , then i suggest stop watching the mainstream media .

Here are a couple of links that show just how bad things are.

I have posted the NY times 2011 item a number of times, but it is worth repeating because it is just so brilliant. It shows you just about everything you need to know from an historical perspective and confirms that the level of inequality in 2011 was at about the level before the great depression. It would be interesting to see how much it has worsened since 2011.

The second shows just how much the opportunity to grab more wealth has moved to favour the extremely wealthy. Again it shows how the lower and middle classes are being ground down. This cannot and will not continue. If the governments are unable to address these issues, these matters will be taken out of their hands and the political instability that we starting to now see is only just a small beginning. Trumps moves to substantially lower death duties and the top tax rate are only going to make matters worse in the short term.

Heaven help us

http://www.nytimes.com/imagepages/2011/09/04/opinion/04reich-graphic.ht…

https://www.nytimes.com/interactive/2017/08/07/opinion/leonhardt-income…

Ray Dalio has written something that adds to this discussion...

https://www.linkedin.com/pulse/our-biggest-economic-social-political-is…

The death rates are very revealing. They point out just how much out of kilter the USA is compared to the rest of the world. (however it would be interesting to see similar research for NZ) The improvement in many causes of death contrasted to the strong increase in drug and alcohol related deaths also shows that we need to put a lot of work into this area. It is hard not to group low/no wages, drug and alcohol, and premature death. Pretty obvious I suppose and it seems sensible to suggest that improving equality would go a long way to improve things.

Mauldin: It's A Bonfire Of The Absurdities

http://www.zerohedge.com/news/2017-11-20/mauldin-its-bonfire-absurdities

Mauldins article really does highlight the dilemma,. The best example is what the Swiss Central Bank has been up to. They have all painted themselves into corners and the dilemma is that unwinding things is very problematic.. ( ie... highly destructive to mkts ).

My view is that there will be No Big Crash until we actually see a paradigm shift in the policy responses of both central Banks and Govts.

Apart from scary moments, asset prices will continues upwards... ( any recession will be met with the same policy response that has been used since the GFC ).

I've learnt that the economic forces of Central Banks and Govts. are like the titanic... They can take the economic path of madness much, much further than anyone thinks, before it all turns to custard.

In my lifetime , people have been calling for the "big end-times crash of all crashes" since 1980.

I would not be surprised if this mess carries on for a few more yrs.

In regards to that crash of all crashes, I think the biggest clue to timing is interest rates. Ask what happens when they are all zero, or negative, across the board. I hear talk all the time of normalising interest rates, but never any support for this other than the belief of what interest rates should be. To me it is the downward trend that is normal, and so we will see zero.

Regarding the SNB, and more so the BOJ, Richard Duncan calls this activity cancelling debt. Duncan seems to think this is a good thing. Trouble is by buying up all the debt it inflates the asset price, but at the same time devalues it. That probably doesn't make sense on the face of it, but think of it as by cancelling debt you are making other debt based instruments worthless. I am thinking out loud here, so would appreciate thoughts on this matter.

Scarfie, I agree... All savers are and will be, the sacrificial lambs.. The next recession we have in NZ will probably result in a 0% OCR...

I thought Duncan was alluding to the extreme level of Japans Govt debt and the BOJ, kinda, monetizing new issuance of that debt. Might seem good for Japan, but if everyone did I can't see it being a good thing.

Japan seems to have a very insular economy, and has a high level of net external assets.

If NZ ever tried to Monetize debt... .... I think things would not be good ...

We're pretty close to a zero percent rate for savings in real terms already aren't we?

Yes - and as the underlying cost of energy always rises it means buying power can only decrease. A deflationary spiral.

Never mind the OCR - it's the OBR that will make NZ savers the actual sacrificial lambs. In the end, it will be the savers who stump up with bail-out capital by taking a haircut on their savings (or should that be investment?). https://www.rbnz.govt.nz/regulation-and-supervision/banks/open-bank-res…

I think it will be jobs that will go first.

Is it not a bit crazy that instead of (for example) land tax to encourage money out of housing and into productive use, the next target for politicians is penalising those who have saved their money, in order to protect those who have speculated on assets?

to quote Tim Morgan ..

""Remember that we’re supposedly living in a “capitalist” system – but how can we have capitalism without positive returns on capital?""

"no system can function without affordable energy. The market prices of oil, gas, etc., fluctuate for all sorts of reasons, but the underlying cost of energy – the trend cost to the economy – is the critical issue. This cost is rising exponentially, and has now reached and passed levels which kill growth. No amount of tinkering with money quantities, interest rates and so on can change that. What this tinkering can affect, however, is who owns what."

Zero/negative interest rates effectively evaporates any trust in money.

If there's concern about US structural problems then where does that place NZ - especially households.

I'd say that in the event of another GFC, policy response will require even deeper negative interest rates, possibly even in NZ. If this happens then people have the choice to store money in other ways where it might be cheaper and to them possibly safer - like in a private safe. I am suggesting old tools may no longer be effective and could be counterproductive in ways unimaginable to speculators next time.

I'd just be chucking every spare penny i have on the mortgage, and use my credit card (55 days interest free) as a revolving credit i.e. groceries/petrol etc then pay it off bang on payday.

That said, I wonder if you put your credit card....in credit.....will it be subject to the negative interest rates?

Wouldn't that be the opposite of what you'd do if they did resort of negative interest rates? To benefit the most from it, you'd want to keep your mortgage as large as possible and keep your credit card unpaid.

This is purely speculation though, plus I'm guessing the reserve bank would put in controls to avoid asset accumulation in housing again (that didn't go too great last time). It'd be a lot better to funnel it into more productive sectors e.g. tech and innovation.

It'd be a lot better to funnel it into more productive sectors e.g. tech and innovation.

The sort of thing some of us were hoping for from a "capitalist" government such as the last. Turned out they were more happy to just keep blowing up housing, to the point of using taxpayer money to subsidise it. Pretendy capitalist.

I wasn’t aware that mortgages would follow the same path, just thought that savings would be taxed. But I imagine your savings would be gouged at a higher rate than the returns on a mortgage.

But further to that, I think I’d prefer to accept the extra help from the bank to pay off my first home as quickly as possible.

A CRYPTO could be the worlds next reserve currency....

I have had $1.2M for over 10 years i.e started in 2006. . Its now really worth about 40-50% of what it used to be worth. Haven't paid a penny back. Dont pay your loan back as quickly as you can. Extend it out as long as you can.

PKchew, where do you get these loans where you pay nothing back ?

I'm curious as well is he talking interest only loans, banking on inflation to reduce the loan burden?

$1.2 million @ 5% over 30 years interest only is $1.8 mill in interest and you still owe $1.2 mill

$1.2 million @ 5% over 30 years P&I = $1.2 million in interest, $1.2 million in Principal Payments and you owe nothing.

You sell the house for $3 million, on your Interest Only arrangement you bank $0. On P&I you bank $600k

$1.2M loan that is...

Cap it all ism ?

No rate increase if economies crash, as predicted. The Banks get bailed out again by massive QEs. Value of money comes tumbling down. The wealthy get more chances to hoard wealth. Job losses or wage declines pinching the middle and lower class, affecting mortgage repayments.

Politicians and Central Banks scrambling cluelessly.

In NZ, reduction in migration and job opportunities and export revenues will kill off whatever prosperity was gained in the last few years.

Interesting times ahead,,,Again ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.