By Benjamin Cohen*

Historically, the safe haven par excellence was the United States, in the form of Treasury bonds backed by the “full faith and credit” of the US government. As one investment strategist put it back in 2012, “When people are worried, all road lead to Treasuries.”

The bursting of the US real-estate bubble in 2007 offers a case in point. No one doubted that the US was the epicenter of the global financial crisis. But rather than flee the US, capital actually flooded into it. In the last three months of 2008, net purchases of US assets reached a half-trillion dollars – three times more than that of the preceding nine months combined.

To be sure, some of these dollar claims were due to the fact that foreign banks and institutional investors needed greenbacks to cover their funding needs after interbank and other wholesale short-term markets seized up. But that was hardly the only reason why portfolio managers piled into the US. Much of the increased demand was due to sheer fear. At a time when nobody knew how bad things might get, the US was widely seen as the safest bet.

But this was before the arrival US President Donald Trump, who has managed to undermine confidence in the dollar to an unprecedented degree. In addition to abandoning any notion of fiscal responsibility, Trump has spent his first two years in office attacking international institutions and picking fights with US allies.

To be sure, even before Trump, confidence in the dollar suffered a blow in 2011, when Standard & Poor’s downgraded Treasury securities by one notch in response to a near-shutdown of the US government. That episode was triggered by a standoff between then-President Barack Obama and congressional Republicans over a routine proposal to raise the federal debt ceiling.

Today, however, investors have even more reason to worry about the US government’s credit rating. In 2018 alone, the US government was shut down three times, and it remains in a partial shutdown to this day, owing to Trump’s demand for funds to build a “big, beautiful” wall on the border with Mexico.

Where can investors go if not the US? The eurozone might seem like a logical alternative. After the dollar, the euro is the world’s most widely used currency. And, taken together, the capital markets of the eurozone’s 19 member states are close in size to the US market. But Europe has troubles of its own. Economic growth is slowing, not least in Germany, and the risk of a banking crisis in Italy – the eurozone’s fourth-largest economy – looms on the horizon.

Worse still is the uncertainty over Brexit, which could prove highly disruptive if the United Kingdom crashes out of the European Union without a divorce agreement. Needless to say, Britain, too, can be ruled out as a safe haven, at least until the Brexit fiasco is resolved.

What about the Swiss franc? Though its attractions are obvious, Switzerland’s financial markets are simply too small to serve as an adequate substitute for the US.

That leaves Japan. With its abundant supply of government bonds, it is the biggest single market for public debt outside the US. The question for portfolio managers, though, is whether it is really safe to invest in a country where government debt exceeds 230% of GDP.

For comparison, the public debt-to-GDP ratio in the US is around 88%; and even in troubled Italy, it is no more than 130%. Admittedly, the market for Japanese government debt is more stable than most, owing to the fact that much of it is held by domestic savers (which is to say, it is safely tucked under the mattress). But Japan is an aging country with an economy that has remained almost stagnant for a quarter-century. Investors would be right to wonder where it will find the resources to continue servicing its massive debt overhang.

And then there is China, with the world’s third-largest national market for public debt. Certainly, the supply of assets in China is ample. But the Chinese market is so tightly controlled that it is essentially the opposite of a safe haven. It will be a long time before global investors even consider putting much faith in Chinese securities.

With secure ports becoming scarce, investors will become increasingly jittery. They will be inclined to move funds at the slightest sign of danger, which will add substantially to market volatility. Today’s rough patch is probably here to stay.

Benjamin J. Cohen is Professor of International Political Economy at the University of California, Santa Barbara, and is the author of Currency Power: Understanding Monetary Rivalry. Copyright: Project Syndicate, 2019, and published here with permission.

23 Comments

Without the USA as the number one power and economy, the world will become an unsafe place.

NZ and Australia will be particularly vulnerable.

Australia vulnerable to China slowdown already

High levels of Aus debt

NZ vulnerability tied to $AU tied to China slowdown

I think the USA is yet to relinquish itself as number 1 military & economic power

Don’t fret kiwis Trump will be over & normal transmission will be resumed as far as US is concerned

This was predicted by the Club of Rome. In a world with no growth, and a bunch of other measures unfavourable to our existing lifestyles.

It is my own thought that assets that command a yield behave like an interest bearing money supply. Interest rates, and yields, will drop over time. Eventually when interest rates hit zero you will have to sell your assets to live. Trouble is by then it will be a buyers market.

There will be nowhere to hide.

And based on David Harvey's analysis of accumulation by dispossession, it seems to be an entirely planned outcome;

Thanks for the link. Some interesting ideas. Couldn't see how Thatcher giving state house tenants the chance to own their own home counted as 'dispossession' - just the opposite. Also wondered if a crisis is deliberately triggered by a neo-liberal govt or just happens. Could ask cubans and venezuelans. However the basic idea seems solid and decidedly worrying.

Cheers. This was the first article of his that I read (written in 2008);

Wouldn't it be a buyer's market?

Scarfi you neglected to mention the Freemasons

Worldwide conspiracy

Scarified,

I wonder just how many on this site know anything about the Club of Rome? You say that yields will fall to zero. Why? I assume that this includes dividends which would spell the death of the equity market. Can you elaborate on your views.

I'm going to invest in crystal balls.

"Investors" the central banks have created a world of "Speculators"

The US used the petro dollar to buy cheap energy. Cheap energy is over, net energy is on its exponential way to the scrap heap. And with it, the petro dollar. Energy becomes more unaffordable, and with it, the advantage of its worldwide intermediate of exchange, the $. The core will attract ‘money’ while the periphery chokes in their fountains of ever more worthless fiats. There’s not enough affordable energy for the worlds economies, so the world will abandon the energy fiat equivalent; the $. The US dollar becomes unaffordable too. Current US administration knows that and frontruns the hoard. They are not stupid

Pssst.. over here..

1) The oil price only recently recovered from a very low point because of collusion to artificially limit supply to get prices up.

2) the price of solar and wind keeps dropping

https://www.nrel.gov/news/press/2017/nrel-report-utility-scale-solar-pv…

https://about.bnef.com/blog/2h-2017-wind-turbine-price-index/

low prices ultimately break producers ...

May as well start your learning here

https://oilprice.com/Energy/Oil-Prices/Oil-Prices-Rise-As-Saudi-Oil-Exp…

https://oilprice.com/Energy/Crude-Oil/New-Data-Suggests-Shocking-Shale-…

https://ourfiniteworld.com/2018/12/20/electricity-wont-save-us-from-our…

I'm just saying we do still have cheap energy, contrary to you previous post. We are amazingly good at innovating to produce/extract what we need, the oil is about to run out thing has been a thing since about the time I was born.. and it hasn't come true yet. In fact we seem to currently have a glut, not a shortage.

As for your links. The first one is exactly what i mentioned.. they colluded to slow exports to get the price up and end the glut.. whats your point?

The second one.. again, prices dropped so low due to excess supply that they stopped drilling new wells. Not worth the effort, as stockpiles dwindle/prices come back up they'll start drilling again.

Third link.. yep, wind and solar alone aren't a good electrical system. Lucky we have a ton of Hydro. Other will use nukes, or have to get creative and develop solutions involving batteries, pumped hydro or something else.

well i dont know, how long do you think Saudi will just happily reduce export volume every time theres a price slump?

https://www.cfr.org/report/interactive-oil-exporters-external-breakeven…

https://www.bloomberg.com/news/articles/2018-12-09/saudi-arabia-said-to…

"..we do still have cheap energy.." ..

Affordability is ultimately measured in net energy available, not fiat.

We arent about to run out (a la the peak Oil story) .... sustained low prices for the producers (and a supply glut!) are exactly what lack of buyer affordability looks like ....

"as stockpiles dwindle/prices come back..."

This is the core assumption which doesnt hold (for long enough). Prices reached $140 a barrel and then broke the system in 08 .... the roof now appears to be below $80 ....

without a Goldilocks price which keeps producers afloat and the economy growing, bad things will happen.

Hydro? youre back onto electricity or some non developed infrastructure as a solution...

Yes, electricity.. One of the most controllable forms of energy. And yes, countries that have been solely reliant on exporting oil for their economy will have to adapt, develop new industries to keep their economies ticking over.

Cheer up, its not the end of the world.

take Japan - how do you imagine their industry will adapt without Oil/raw material imports across the board?

Are you saying they should fire up Fukushima again and they will all be rosy?

Are you saying the flow on effect will be negligible in NZ .. because we have some Hydro?

Im not sure you understand the nature of the problem.

And controllable electricity ... you need working maintained infrastructure ...

https://edition.cnn.com/2019/01/07/investing/pge-stock/index.html

"Shares of California utility PG&E tumbled Monday, because investors are worried it may go bankrupt.

PG&E (PCG) could be on the hook for tens of billions of dollars for its potential role in California's devastating Camp Fire last year -- the deadliest and most destructive wildfire in the state's history. The company has indicated it does not have the cash or assets to pay anything close to that amount.

The utility, which provides electricity to about 16 million Californians, is contemplating filing for bankruptcy protection, "

So we started with the statement "cheap energy is over" now we are morphing to the world has run out of feedstocks.. again, back to the fact that the only reason the oil price is going up is because of the collusion of some of the oil exporting nations to artificially restrict the supply. Feedstocks can be substituted, the plastics we use today can largely be substituted for bio-plastics.

Again, we are constantly innovating, and we will continue to do so, if something becomes to expensive (monetarily or energy) to make, we will either improve the process or find/make an alternative.. we always have in the past. And yes, there will be times when we don't innovate fast enough and the is some sort of temporary shortage and price bubble, but thats not the end of the world, its a hiccup and a temporary crisis that will spur development and innovation.

Throwing in distractions like PG&E doesn't help your case. One case of mismanagement doesn't an intrinsic failure make.

Pragmatist and ham n eggs,

As someone with no expertise in this area, I find your exchange fascinating. Which view is right? I suspect that the answer lies somewhere between the two. We will eventually exhaust our oil and gas reserves and must move to renewables before that point. I doubt if the transition can be managed smoothly,which means that we can expect severe price spikes from time to time.

As climate change becomes ever more obvious,so efforts will intensify to speed the transition. People and economies will be hurt in the process.

I agree entirely, there will be shocks as demand temporarly outstrips supply and we have failed to innovate fast enough, but the difference is H&E refuses to acknowledge that we can and will innovate.

H&E's entire premise is the "end of energy".. but the sun isn't going anywhere for a few million(billion?) more years, so wind, and solar are going to be available, we just need to find ways to harness and utilise them to replace the current use of fossil fuels. Basically we need to short circuit the (sunlight -> dead trees -> ~80k+ years underground -> fossil fuel) bit.

There are all sorts of ideas out there to achieve this, and some of them will end up working, most will probably fail. But it only takes one Algae to fuel type idea to work at scale and we have won that battle. The real problem is keeping population growth under control until sometime we figure out how to expand beyond this planet and then eventually the solar system. (not that I expect either to happen in my lifetime, but who knows)

"H&E refuses to acknowledge that we can and will innovate"

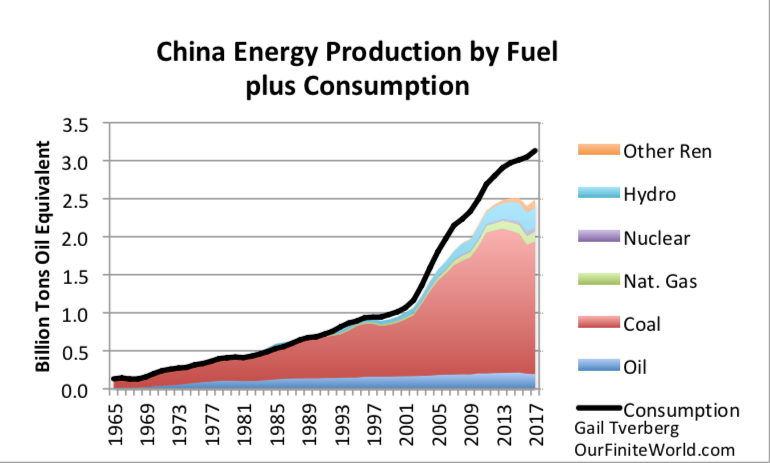

Doesnt look like much innovation to me...

https://www.iea.org/weo/

https://gailtheactuary.files.wordpress.com/2018/06/china-energy-product…

https://gailtheactuary.files.wordpress.com/2019/01/oil-as-pct-of-total-…

{kind=link}

{kind=link}

Add in the need for a DEBT mountain and ever lower interest rates then for 30+ years to stoke growth shows we arent innovating fast enough to counter diminishing returns.

(Aside: it turns out the boomers werent canny investors afterall - they just bankrupted the future)

And Debt (which promises that there will be more surplus net energy consumed down the track) is now looking like a very thin promise...

You are spot on in two areas

- the new solutions just cant be scaled up

- population is now a BIG problem ... yet every country uses population growth as its (personal) growth strategy - making the world energy/capita equation ever worse

So given China is now looking at expanding coal production ... ask yourself why Solid energy failed. You are telling me they ran out of coal.

Or was it low prices?

Trump happenings - tomorrow if you want to find a live feed;

https://edition.cnn.com/2019/01/07/media/networks-trump-border-security…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.