By Martien Lubberink*

“He is the problem,” the investment banker said on a sunny afternoon some weeks ago over a plate of Shed 5 fish & chips. I agreed, it’s the governance of the process, or the lack thereof, that puts the capital plans of the Reserve Bank at risk.

The investment banker had spent the entire Christmas break perusing the literature on bank capital, from Steven Ongena to René Stulz to Anat Admati. We met for lunch to discuss.

“But if he is the problem why don’t you study A Theory of Yes Men by Canice Prendergast, or What’s really wrong with bank supervision by Daniel Davis?”

“Just saying,” I continued. “If governance is the problem, then you are wasting your time on studies about optimal capital ratios, because few people at 2 The Terrace may listen, if any at all.”

Fear, greed and a pinch of vanity

I leave it to you to figure out who “he” is, or if it is only one “he” or perhaps two, or maybe a “she”. That’s besides the point. The issue is, as usual, a combination of incentives and governance. The incentives in this case are fear and greed, pictured below. These are all too powerful and can wreck organizations, if left ungoverned.

The capital proposals are the brainchild of one Reserve Bank official in particular. Someone who apparently is afraid of ever-growing regulation and the inability of the Reserve Bank to keep up. The end result is as simplistic as it is Trumpian: Let’s build that high wall of capital, let’s establish that high floor. Let’s get rid of concepts that we do not master: the internal ratings based (IRB) approach and CoCo’s. Let’s ignore Basel III, reinvent the wheel and make New Zealand banks great again.

Project fear is now well underway. Once the higher capital requirements have entered into force, the RBNZ official will be promoted. Having worked at a reserve bank myself, I expect no colleague to challenge that promotion. It’s how these things work in practice.

Whether it is a well-deserved promotion remains to be seen. Time will tell. But to give you an idea of the proper approach to addressing the complex task of rewriting bank capital rules, I invite you to a view on the governance of Basel III first.

Basel III: the result of teamwork

The great thing about Basel III is that it is not really a response to the Global Financial Crisis. If that were the case, then it would have taken the Basel Committee much more time to craft the post-crisis rules.

Just look at the timing of events: In April 2009 the G20 decided this:

In less than eight months, Basel produced a comprehensive document that includes a fresh recipe for capital: the resilience document emphasizes the role of common equity and it presents a simplified Tier 1 and Tier 2 structure. It also introduces a conservation buffer and plans for a leverage ratio – all internationally harmonized. Isn’t that exceptionally fast?

Speed is your friend

How did the Basel Committee write a comprehensive capital plan in such a short time? I mean, the European Basel Committee members are on holiday from July to the end of August. The document had to be ready by November for the top-level Basel Committee meetings. So, the group that wrote the document must have worked flat out during April, May, June, September, and October. Or, which is much more likely the case: there was already a group working on Basel III.

It was the latter, Basel III was the sequel to Basel II, which was done and dusted by 2006 and had entered into force. Work on Basel III had begun as early as 2007.

No prima donnas to be seen here

By April 2009 there was a fully functioning team, ready to respond to the call of the 2009 G20: write rules that improve the quality and quantity of capital. For some time, I was a member of that team. We worked diligently to overcome differences and find solutions for problems big and small. The team reached out. It invited stakeholders and experts to inform the process.

Moreover, the Basel Committee takes decisions by consensus, which means that each member can ‘veto’ decisions until consensus is achieved. In a relatively short time the team found solutions for capital of co-operative banks, for Italian deferred tax assets (DTAs), Australian “stapled instruments”, and the capital (in)eligibility of German Silent Partnerships.

Most of the time however, we spent on creating an instrument that would absorb losses in a going concern scenario. So, yes, it took years to reach consensus on a minor issue: the trigger that leads to conversion of Additional Tier 1 instruments. Should the trigger be high (7%) or low (5.125%)? In the end we chose the latter, see the FAQ of December 2011. Apart from that, many of the other items in the Basel III rules text were quickly decided.

Basel also succeeded in developing a term sheet for CoCos. Spanish banks Popular and just this week Santander demonstrate that these instruments perform largely to specs.

The importance of proper governance

By now you should understand the importance of governance. Basel III is not the brainchild of one person, it was the result of a well-governed multidisciplinary team which worked out how to complete the task set out by the G20 countries. Most of the team members were selected before the onset of the GFC on the basis of expertise. We worked as supervisors and represented the Basel member states, which introduces a form of accountability. Decisions were made on the basis of consensus, not on the basis of simplistic mantras, fear, or greed.

On top of that there is a comprehensive system of checks and balances. A consultation process to start with. Then, twice a year the Basel Committee publishes a monitoring report to check if member states are on track with improving the quality and quantity of capital. There is also some naming and shaming: the Regulatory Consistency Assessment Programme RCAP. Lastly, countries implemented Basel III by way of laws, which introduces additional accountability.

I do not remember the Basel Committee posting a trove of internal documents on a Friday afternoon web-page. Or updates because the original document contains typos. Neither did the Committee go public impromptu to announce capital plans in picture format to “clarify” the speech of a deputy.

Is that all there is?

Unlikely. Bank supervision is not only about floors, CoCos, or capital ratios. It is also about Pillar 2: capital requirements that are bank-specific and at the discretion of the supervisor.

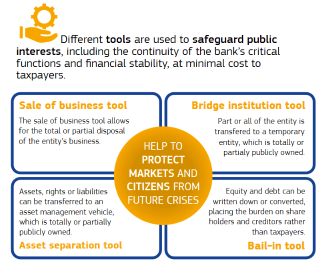

Bank supervision is also about resolution: one cannot discuss the (in)adequacy of CoCos and at the same time rely on only Open Bank Resolution. The Reserve Bank should take a leaf from the European bank recovery and resolution directive, BRRD. It is a comprehensive toolbox that includes bail-out (!) as well as the tools shown below.

But more on this later.

*Martien Lubberink is an Associate Professor at the School of Accounting and Commercial Law at Victoria University. He previously worked for the central bank of the Netherlands where he contributed to the development of new regulatory capital standards and regulatory capital disclosure standards for banks worldwide including Europe (Basel III and CRD IV respectively). This article first appeared in Capital Issues and is reproduced with permission.

18 Comments

I think I got the gist of this article and my smattering of banking knowledge has now tipped closer to zero. My eyes nearly glazed over but I managed to finish the article.

"Bank supervision is also about resolution: one cannot discuss the (in)adequacy of CoCos and at the same time rely on only Open Bank Resolution. The Reserve Bank should take a leaf from the European bank recovery and resolution directive, BRRD. It is a comprehensive toolbox that includes bail-out (!) as well as the tools shown below."

I must have missed something here as I'm not unhappy with OBR provided that capital ratios are adequate and until RBNZ ups them to a much high figure than they are now I feel they are currently inadequate.

"Moreover, the Basel Committee takes decisions by consensus"

Perhaps consensus ends up as the lowest common denominator?

Basel III may also suffer from the racehorse/camel design and that the one person at RBNZ could be the better option for NZ.

"European bank recovery and resolution directive, BRRD"

Is this valid for NZ?

"investment banker said on a sunny afternoon some weeks ago over a plate of Shed 5 fish & chips"

Didn't think an investment banker would stoop so low. More like quaffing a single malt and sampling caviar at the Wellington Gentlemans Club, wherever that may be.

"improving the quality and quantity of capital"

Interesting. Last I checked, it was issued as debt, issued at a key-stroke, backed by someone making a bet. Are we looking at issuing more of it with CAPS LOCKS on? Don't think that will solve the coming crisis.

http://www.debtdeflation.com/blogs/2012/07/22/the-crisis-in-1000-words-…

Herein lies the problem; 'Someone who apparently is afraid of ever-growing regulation" This is about private organisations which have the resources, power and ability to bully, intimidate and simply run rough shod over any Government's effort at sensible balanced economic management. They seek to prevent being regulated so that they can continue to reap literally billions in profits, and avoid as much as possible paying taxes.

Bank capital requirments are about putting a mattress on the ground in case they fall off the walkway. What about putting a railing on the walk way? Or even stopping them being on it at all? Regulation is about protecting the general public, bank capital requirements is lip service that does little to rein them in, if at all. The statement from the G20 is ignorant of or simply ignores banking reality. "Buffers of resources built up in good times" just doesn't happen. Banks pay out their profits yearly to shareholders, indeed neither they nor Insurance companies build their buffers in the good years to carry them through the bad ones.

They're trying to ward off a financial crisis.

It is so obvious.

Yup.. the bankers are trying to ward off a financial crisis brought about by ill-considered capital rules.

prior yes, but would have happened anyway. The market going from 100% of gdp, to 450% now, 1990-present, is a function of offshore flows & low savings rates, plus a healthy dose of an expanding working age demography. Financial crises are commonly associated with large real loan buildups, high house price to gdp ratios, and a shrinking in the working age labour force relative to the dependent brackets, New Zealand fits all those requirements so it will be interesting to see how things play out.

FYI thats the real reason the real estate market has slumped so far in terms of volumes. A financial crisis can only be avoided through an early adoption of quantitative easing, not through regulatory rules. I suspect they will do just that, and that larger capital requirements actually enable them to enter a quantitative easing program safely, i.e it expands the size that they can ease.

Hi Lalaland,

Think you missed also Sovereign Debt crisis. Interest rates for the past 10 years have been too low to keep up with return required to meet pensions ( government ). Thus some of that $ also gone in to foreign emerging market debt to catch higher returns ( thus higher risk)

Quantative easing ok yes only that $ is used properly and not give it banks to NOT lend out after selling government debt.( create liquidity ) on a private and corporate level. ( Should not be allowed to be used to park it in government debt. It must be used in the local private sector.)

You can't direct lending, banks are free to hold whichever securities they choose. Banks are very risk adverse in practice.

The problem you are missing is post-gfc, its not that banks don't want to lend, its that they can't really find the aggregate demand to lend to again. i.e its demographic and a demand side issue

Quote : "You can't direct lending,......"

Fund XYZ to be able to have a license to operate MUST HAVE 30% of its $ in Government Bonds/Debt ..... ( ie. lending $ to the goverment )

Oh but you cant direct lending ....

What you cant direct is government on how to spend....

Jesus you really don’t know a thing. Sad to see yet another financially illiterate person in NZ

Jesus lived some 2000 years ago. Or so the book says.

Do tell us your real world experience in the financial world then. Would love to hear ....

I remember when I first got into finance too. Good luck

Thanks.

You must have had some real experience since ...

I know enough about banks to know that banks look after banks, & that includes central banks. The theory is fine but the practices always seem to lack.

I'm not sure Wellington has a Gentlemens Club, has it? Or is it a lack of gentlemen?

Just banks using lobbyists as per usual

Anything to curb rules & regulation

Depositors come last in New Zealand

Persons at 2 The Terrace need not listen. They have the Bail "IN" legislation.

I see Martin North is a strong advocate of Adrian Orr's proposals . North also commented that resistance to increased capital buffers is effectively privitising profits and socialising losses! So the author implies the RBNZ needs a committee of veto enabled market participants. Sounds to me like a recipe for regulatory capture, because you'd only need one single banking insider to resist any meaningful change. As for the Trumpian wall slur, that's a pretty desperate and laughable insult

Do I detect sour grapes here. More capital means less losses for the public purse. Simple yes.... Trumpian no. In fact the exact opposite. That’s makes the risk takers pay for their losses, not other persons in the trumpian way.

A central bankers views would be more relevant, not a failed central banker that now teaches. Remember, those that can; those that can’t teach.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.