This is a repost of an article by Kernel, an index investing platform. It is here with permission.

Opinion

Property investment has been the darling of New Zealanders, enabling and driving personal wealth for at least the past 2 generations. Literally while sleeping, houses have been increasing in value faster than inflation. However, we say that houses are now a bad investment.

For the record, our products at Kernel are not the panacea, we are not paid or paying for our opinion, we don’t hate property, banks, or any type of asset (they all have their place) but we do want to help you understand wealth creation and some of the tricks previously reserved for the rich.

Why owning a home is good wealth creation

We all need to live somewhere and taking out a mortgage provides three key wealth creation benefits. First a mortgage is “forced savings” - normally a table loan schedule, which if you don’t comply with and make the payments, the bank will foreclose on you. This way, you build wealth by paying down the principal of the loan little by little, regardless of capital gains.

Second, it is inexpensive leverage, because through a mortgage you can own an asset worth multiples more than your deposit, paying a lender a changing rate of interest which you can fix for periods for the certainty.

Third, houses are illiquid and difficult to divide. You can’t easily sell a portion of your house and selling takes time and costs money. This is a good thing so that we don’t rashly sell or buy in the heat of the moment, although you do hear the occasional story of an impulse auction purchase, creating a variety of consequences.

Why owning multiple homes is not good wealth creation

Property is a valuable asset when, excluding the main home, it is part of a well-diversified investment portfolio. Historically, it has low correlations to bonds and shares. However, in our financial advisers’ experience, people generally don’t count the total cost of ownership. They make assumptions that the property will be tenanted 52 weeks of the year, forget about property management costs, repairs and maintenance and taxes. Mainly people forget about their time involved.

Have you ever wondered why there are no large property syndicates or listed property trusts (REITs) owning residential property? It’s just not viable, even at scale. As a result, we have a country of amateur landlords.

Recent NZ Herald research suggests that almost 40% of New Zealand’s 1.9 million properties are owned by amateur landlords. Some ‘lords loudly proclaim how well they have done, and others quietly worry about their tenants and their return on investment.

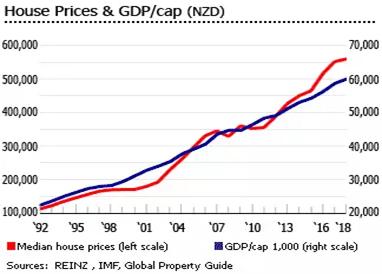

But now, four main factors have also played out. Interest rates at an all-time low, building costs remain high, landlord obligations and tenant rights are being challenged, and rents as a percentage of tenants’ income are in many areas at a maximum. New Zealand residential property prices are some of the highest in the world relative to affordability and now trending well above GDP per capita. Sure we could go further – with the likes of negative interest rates, legislation change or slum living conditions. But will this occur?

The truth about debt

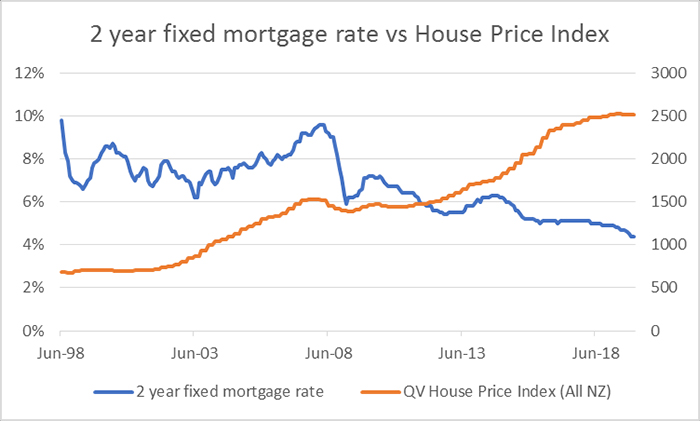

Leverage is a double benefit or double whammy. While interest rates are falling, it is a multiplier on increases in value and as the chart below shows, interest rates on mortgages have been falling for 20 years now. But what if interest rates rise?

Mortgage payments increase and property will often fall in value, leaving some leveraged investors “upside down” - owing more than the value of the asset.

This is where the concept of debt servicing is good to know. If your interest rate rose by 1%, 2%,3%, or even back to a long run average of 8%, would you be bankrupt? Or are you relying on the Reserve Bank or banks considering it too big to fail?

Now we are not suggesting interest rates are about to rise, evidence is to the contrary for the foreseeable future. However, we also don’t believe in crystal balls and suggest it is good risk management to consider the impact on you if they did.

There just are not enough houses

One argument pro-property is that because of strong immigration, arduous consent processes and costs of construction, New Zealand has a shortage of houses, meaning that the houses we have are more valuable and in demand.

Infometrics modelling suggests that New Zealand might have a housing shortage of around 40,000 but overall the nationwide undersupply of housing might be as low as 2,500 dwellings. The difference is that there is oversupply of housing in parts of New Zealand, notably Christchurch, and undersupply in other parts, for example, Auckland.

The reason for the “might” is a heavy dependence on a key assumption about the number of people per dwelling, which is rising in Auckland and falling elsewhere. Simplistically, whether driven culturally, socioeconomically, both or otherwise, there are less empty bedrooms in Auckland. There is plenty of misinformation, and suffice to say it is a complex issue when you consider global trends of urbanisation, freedom of movement, and government policies such as regional development and the defunct KiwiBuild.

Additionally, there are demographic effects such as longevity, dual incomes and starting families later, making correlation between house price changes in over supplied and under supplied areas hard to identify to prove the point. Meanwhile MBIE (2019) found no evidence that a higher share of new (international) immigrants in an area is associated with higher house prices.

Why there is unlikely to be a property crash in New Zealand

Both Ireland and the US experienced a significant house correction around 2008. These were due to serious structural issues: in Ireland around construction addiction creating a “bullwhip effect” of oversupply and in the US with subprime mortgages allowing huge leverage relative to wealth and income.

Both these bubbles burst. However, short of interest rate rises driven globally, our RBNZ macro-prudential policy looks to learn from the past, and due to the concepts of loss aversion and anchoring, few vendors are prepared to sell at a loss, instead holding on until growth returns. These factors smooth the property market falls, as seen in New Zealand twice in the last 20 years with the plateau of prices. If we look at the below graph as visual evidence, you could argue we are due for a plateau again, despite falling interest rates.

Healthier homes and tenant’s political power

It is an understatement to say landlords are historically lightly regulated and that legislation has favoured the owners over the occupiers in New Zealand. However, the Healthy Homes Guarantee Act passed in 2017 introduced standards to improve the quality of rental housing in New Zealand. These obligations on landlords stagger in until 2024 and increase maintenance costs. Furthermore, there are proposed changes to the Residential Tenancies Act 1986 which aim to increase tenant’s rights and stability. According to the 2018 census, 55% of Auckland adults and 48% nationally are not owning their own home, and this long term trend away from home ownership, surely will continue to increase the voting power of tenants and government’s promises for election, towards the international standards seen in other developed countries. Not a trend of increasing regulation and cost we would be betting against anyway.

So are Managed Funds or Property better?

Both have their pros and cons and the ‘best investment’ is the one that is most right for the individual investor at the time, based on their risk profile, wider asset base, cash generating ability and longer term goals. Long term in NZ and elsewhere, the stock market performs best.

The table below summarises the often overlooked advantages and disadvantages. Aside from leverage, we would say managed funds are better long term wealth creation.

| Managed funds: | Residential rental property: |

| Historically shown the best growth over the long term in NZ | Historically shown good growth over the long term in NZ |

| Potential for huge diversification into sectors, economies and using different fund managers. | Harder to be adequately diversified. Even if you have multiple rental properties, they are usually in same city. |

| Ease and speed to sell - can receive cash without a discount to value usually within a week. | Slow to sell. From decision to settlement is usually months. |

| In New Zealand, it’s not easy to leverage, “margin” accounts are not common. | Banks are willing to lend against it so easy to leverage the investment i.e. mortgages. |

| Low transaction costs < 1% value | High transaction costs ~4% of value if including advertising and conveyancing. |

| Very little time commitment by you. A professional is managing the investment on your behalf and this cost is built into the managed fund. | Ownership burden, tenants, property management time and/or cost. Repairs, maintenance, upkeep, risk of damage. |

| Ability to use PIE or other tax structures, to reduce the tax payment. Normally no need for a tax return. | Rental income declared as personal income. Can offset expenses against income. Annual at minimum requirement for tax return and accounting. |

| No capital gains tax. | Capital gains tax if sold within 5 years. |

| A number of regulatory checks and balances including manager licensing, supervisor and a custodian. The manager must follow what is contained in the Product Disclosure Statement | Burden on the vendor and purchaser for legal risk, warranties and indemnities. |

| Excluding impact of leverage, shares have historically outperformed all other asset classes over the long term. | Historically it has been perceived to be less volatile than shares. |

| Because considered non-unique, accurate valuation available every minute. Move with sentiment causing emotional biases. | Because considered unique, valuation only on sale or inaccurate by a valuer. Self-valuation as sentiment. |

| Good regular income possibilities above term deposits. | Net (of costs) income usually low. It is more of a speculation purchase for capital gain rather than for regular income. |

| Can start with $100 | Difficult to start with less than $100,000 |

Not to mention further economic concepts or moral issues such as unproductive assets, lifetime of debt, deviation from inflation and real GDP, and improving quality of housing.

So to summarise, we suggest that property is now a bad investment, because 1) mortgages rates driving the past 20 year trend are unable to fall much further, 2) we are likely due for a plateau or underperformance in the next 3-5 years, 3) affordability is low inhibiting gross rental increases, and 4) landlord regulation and tenant rights are likely to increase.

But we would say that; what do you think?

This is a repost of an article by Kernel, an index investing platform. It is here as part of a range of views.

200 Comments

Known by many, but ignored in the main stream property mags, such as the Herald.

You could also include a column for 'self managed funds'.

Waiting for the property bulls...................

Ignore this chap.

It’s just Retired-Poppy operating under a new pseudonym.

TTP

Succinct and very well done! You are tothepoint

which part was he wrong in?

All of it. But for a start managed funds were not the best growth investment when you cant leverage. He said himself that the last two decades been good for property and also said that leverage helps. The returns from leveraged property have been truly enormous over the last 20 to 30 years. We started with less than zero in the nineties.

Rastus made no such comment.

Actually he made comments about self managed portfolios which CAN be leveraged. Such portfolios have outperformed property for the last couple of years.

I think TTP was referring to the author Dean Anderson from Kernel so I was responding to that. Yankiwi got the wrong end of the stick but what else do you expect from an american refugee. And furthermore the last couple of years is nothing.

No, TTP was clear in what they said. He replied to and was referring to Rastus. Not the author of the article.

PS, nothing says awesome character reference like your bigoted overtones. ("what more can you expect from an american refugee")

We have certainly seen which type of investor is correlated with a lack of decorum, a lack of substantive discussion, and with a large helping of ad hominem.

I am the poster child for the benefits of investing in the share market, as well as market timing on both the share market as well as the housing market. We paid off our house in 1993, and immediately took a mortgage and invested the money received from this mortgage in the share market. This went very well, then we went to cash for a while in 2000 while the dotcom crash happened. We sold our house in 2006 and rented for a year before moving to NZ, as the US housing market was clearly going to tip over, despite many predictions to the contrary. Interestingly, after arriving in NZ, we decided to rent for a while as it was far better to be a renter than an owner from a financial perspective (we were not in Awkland but the regions). Turned out that it was more prudent to rent than to own for a full decade. In effect the landlord subsidized our housing, which we greatly appreciated! When the tide was turning to benefit home ownership, we returned to home ownership four years ago. From our arrival to the time of our purchase, the capital gains for our region was single digits for nine years (in total, not annualized). From the time we bought, the capital gains has been almost 40%. There are clearly times to buy, and times to stay away from buying. This is true for housing, the share market, bitcon, and all other places that one may be wanting to put money for long term investment.

It has been a while since we have seen a post from BuyLowSellHigh. His moniker suggested that he should be selling his property portfolio a few years ago as the inflation was exceeding his capital gains. He was adamant that that wasn't the case... I suspect that he was another over-leveraged cash-flow negative specuvestor that got caught on the wrong side of the solvency equation.

Rational investors look at all forms of investing and choose their investment based on risk profile, investment diversity, and holding period. Irrational investors make silly claims and use ad hominem attacks instead of discussing the relative merits of the various investment approaches.

TTP,

The odds of rastus being a new pseudonym of R-P is less likely than the Ukrainian airliner crashing due to engine failure.

Rastus as been a member on interest.co.nz for nearly nine years, almost four times longer than you have been here. He also has a lot more credibility than you, especially with your usage of ad hominem rather than rational discussion of the topic.

Property has bottomed in nominal NZD terms. Prices won’t fall more than 5% at the maximum.

Property has bottomed literally forever.

It won’t pickup for a few years however.

Credit cycle is what you want to look at

Happy to be on the record for saying this

As long as we can maintain record low interest rates and continued credit growth then everything will be okay.

“Ok.......”

'We'? ;-) agreed our low interest rates is very independent from any world economic future shock. Credit/debt growth is the key to cure that productivity Cancer.

Thank you yawkiwi. Many pups on the site now. I recall the days of hickey and the legendary wolley- true character was he, truely missed.

Hickey now lives in hiding (suburb of Wellington)

Only rich boomers use NZ herald now that they charge you to read it

I am a 'rich boomer' and I wouldn't wipe my arse with the Auckland Herald (why? because what comes out of my arse is both more valuable and far more accurate than what you will find within the pages of that disgusting rag)

Uh-oh.... Blasphemy.

The elephant in the room to your opinion; which I largely agree with, is continued population growth through immigration.

While the present government campaigned on reduced immigration, the short term reason why this hasnt reduced is it increases the demand for accommodation; which is currently maintaining prices.

I can't see any government reducing immigration number any time soon in a country capable of supporting at least the equivalent of the UK's population, or at least until there is a global recession; likely to be driven by debt levels coming home to roost.

Surely at the end of the day house prices need to be supported by wages, ie production. That's our big weakness, how long will people accept getting poorer for, dividing the countries wealth between more and more people?

What surprised me is the articles during the year which show we have almost 500,000 people here on temporary visas.

It seems to me we only need a bit of a recession and a few job losses and a lot of those people will leave, causing a large downward spiral in the economy (including housing).

I would also add that many of these workers that the horticulture industry is now dependent on, in the future will turn from a strength to a vulnerability they should have seen coming but got blinded by greed.

Greater regulatory policing of the sector locally as well;

https://www.stuff.co.nz/business/117493597/philippines-government-opens…

Agree with you GS

I am not aware that acceptance of such high levels of immigration was ever accepted by the New Zealand public. The only party I recall having a strong stance on the level of immigration was NZF who wanted to limit the level and now are complicit to the continuing high levels.

High levels of immigration are placing considerable pressure on all forms of infrastructure including housing.

Certainly the Treaty partners were never consulted;

https://e-tangata.co.nz/comment-and-analysis/its-time-for-maori-to-be-h…

How much more useful for its people would The Maori Party have been had it focused on this issue, as opposed to tobacco taxes?

Sorry but I certainly don't want to live with 65 million people in this country. 5 million is more than enough. A say in the matter would be nice rather than the government slowly boiling the frog.

The UK is grossly overpopulated

Pocket acres , less than 10% of the UK is built upon .

Do you believe this this the only metric for quantifying overpopulation? How large is their overall ecological footprint? Is the UK self-sufficient in food and energy production?

*Groan*

NZ with the population of the UK. Madness. Why? NZ would be better with 2 million max.

What about only 2 people? living in a cave, hunting and gathering for survival?

Adam and Steve.

Borrowing today's mantra? - One of them should be 'clever' enough to kill the other one, then claim the cave as sole RE owner, survive alone. But yea, alas one could decide to enslave the other one though, until... the first mantra take over.

So to summarise, we suggest that property is now a bad investment, because 1) mortgages rates driving the past 20 year trend are unable to fall much further, 2) we are likely due for a plateau or underperformance in the next 3-5 years, 3) affordability is low inhibiting gross rental increases, and 4) landlord regulation and tenant rights are likely to increase.

But we would say that; what do you think?

We think is the best place to park unoffical money in TAX FREE HEAVEN (Money Laundering).

Rememebr that Bright Line Test is a toothless Tiger, otherwsie why would so called investor be happy with no CGT if BLT as propogated is another form of CGT.

Is it ?

How many have paid tax under BLT - Many loopholes check with Chartered Accountant will show you ways and means to jump BLT. If government is serious can add another column when selling the house, Do you own a house in any form - Yes or No an if yes for how long and the same to passed to IRD for scrutiny or any other agency ......No CGT (bad as was one of the promise thatgot them votes) but does the current government has intent to impliment BLT to deter speculation.

Thanks for this article, interesting. I agree. Perhaps #5 to the summary should be, as stated in the article, the reported shortage may be rather exaggerated in most places. The situation on the ground certainly suggests this.

The most important advantage of property is it is a necessity for every human. People always need a roof over their head. Unfortunately at the moment, prices keep home ownership low among the majority and rents sky high

Not To forget Tax free and fast money - atleast for now.

That was one of the points of the article, in that when there are more renters than landlords, where exactly will political sentiment land...?

Peasant's revolt.

Nzdan,

That didn't end well for Wat Tyler.

What is required is a very strongly organised tenants rent revolt. If enough people refused to pay their rent, what could the government do? - allow landlords to evict thousands, tens of thousands, hundreds of thousands of families onto the street? where would the government house them under emergency provisions? are there enough motels?

What would the landlords do without the steady stream of rental income and more to the point what would the banks do to them?

This could blow up into an absolute and complete disaster for any government and it would be nothing less that they deserve given the cynical lack of meaningful action by all parties to address the housing shortage and affordability, combined with their continued pumping the country full of as many immigrants as they can get into our country.

There is precedence for this when in about 1886 a group of crofters on the isle of Skye went on a rent revolt, then stared down the troops that the government sent to deal with the situation. In the end the government had to back down and change the laws relating to crofting tenants.

There's a Renters United lobby group that's been kicking around for a couple of years now. Currently perceived as being a group of nobodies with nothing better to do than rattle some chains. If they get the right message out there, and it gels with enough people then who knows?

Ratepayers have tried that... didnt work

Rate payers have property that can be confiscated for unpaid rates. Tenants?

Tenants also have a due process. Can the Tenancy Tribunal handle a massive influx of rental arrears/eviction cases in a timely manner?

Give it a go, will be interesting to watch you squirm

With Internet? it could happen, the format that must be clever enough.. nothing is possible there. It's pretty much wild west, the structure must be perfect & appealing to many, popular? then yea.

Due to vested interests, I take this with a grain of salt. However, still a very valuable article as all investors need to consider a range of views and opinions.

To me, given the considerable increase in worldwide sharemarkets over the past decade and current uncertainity due to global headwinds, it would seem that there is increasing risk associated with equities whereas three years after Auckland's peak - and concerns over a bubble burst - the NZ housing market is stable and has seemingly possibly past it high risk post-peak period.

The equity market tends to be very volatile (and many older people of my generation still feel distrust of the sharemarket due to their experience in 1987) whereas property market tends to be more secure and less volatile.

Although there has been considerable seemingly anti-landlord legislation and poor yields, the outlook is a lot better especially with some continuing firmness of the market, possibility of capital gains and removal of the CGT factor, and improving rental yields.

While now out of owning rentals (for lifestyle reasons, although my wife has one) I still see rental properties as a great long term investment in addition to KiwiSaver for one looking 15 to 20 years to retirement by leveraging their home equity to buy the rental.

Something to ponder: What is one's bank's opinion regarding borrowing to investment property versus investing in the sharemarket? Try see what reaction you get - that should tell one a lot.

I agree with you about overvalued equity markets, however NZ real estate is also still really elevated even after the 3 year flatness in Auckland. You just need to compare it at a global level, like we do with sharemarkets. It’s still one of the most expensive in the world by usual measures. The market has way overshot the historical mean and will return to it one way or another.

ASB offer margin lending of up to 70% LVR on large company stocks on the NZX and up to 75% on the ASX, without shopping around or negotiating. By comparison, 95% of all bank loans to residential investors must be issued with an LVR of 70% or lower according to current RBNZ restrictions.

What was your point? I'll admit that due to lack of competition, the interest rate on a margin loan is likely to be higher than a mortgage, further encouraging the lazy into property investment rather than productive investment. I am also not recommending that anyone go out and buy any investment with a 70% LVR.

https://www.asb.co.nz/content/dam/asb/documents/asb-securities/2019/asb…

https://www.asb.co.nz/content/dam/asb/documents/asb-securities/2019/asb…

..Is that a mic drop I hear?

hi mfd

Not quite the full story there - in fact, as you put it, simply not correct (i.e. b*llocks).

Talking to a banker friend (in lending credit with five or six years experience) and his comment is that the document you quote would not relate to someone just walking in off the street without a well established banking relationship. He has never heard of a bank taking shares as security. In such lending, not only would they require one to bank with them, they would require that they hold other security - such as your home although that would not be a directly related security of your lending for shares. In the event of you reneging on your loan for the shares they have a caveat which allows them to chase you up against any security that they hold.

His comment was that it would be a guideline to lending provided the bank held other security.

Bottom line - they are not going to carry the risk that you won't lose more than 25% on your investment. I'd borrow heaps if I knew the most that I could lose on my share investment was 25%.

Do you really seriously think ASB or any bank loan up to 75% of the value of shares - shares are too volatile for a bank to take that risk.

"Do you really seriously think ASB or any bank loan up to 75% of the value of shares - shares are too volatile for a bank to take that risk."

Yes, they do lend on value of shares. It's a call account though, so limits fluctuate.

I presume your banker friend was not from ASB.

https://www.asb.co.nz/content/dam/asb/documents/asb-securities/2016/asb…

Perhaps if your friend has never heard of a bank lending money on shares, he's not a good person to rely on for information about lending money on shares? The documents I posted are not hypothetical - ASB do perform this lending, as do other companies. Certainly not all banks, so if your friend is with a bank that doesn't perform margin lending he may not know much about it.

Of course, a far more common (and cheaper) way to leverage into shares is to use your own house as security. I essentially do this as I have a mortgage on my house and a share portfolio.

mfd,

I wish you luck. I am a long-term stockmarket investor and would never dream of borrowing to invest.

I only mean theoretical - I bought a house and didn't sell all my shares to do so, taking out a larger mortgage instead, therefore I am now leveraged. Over my entire net worth, I'm about 45% LVR, all secured against property.

printer8,

You make some good points. banks will certainly look much more favourably on property than equities for lending purposes, but I would argue that nobody should use leverage in the stockmarket. For property on the other hand, it is almost impossible to access the market without leverage.

Stockmarket volatility does put some off and yes, many still vividly recall the '87 crash. In the UK, it was a 5 minute wonder and then forgotten. However, for those investing on a regular basis-say through Kiwisaver-volatility is their long-term friend through $ cost averaging. For investors like me, volatility is just part of the market and not a source of anxiety. I have both shares and a rental property and have certainly had a better return net of all costs from my stockmarket holdings over the past 15 years.

The NZ property bulls are not going to like this article. Real estate is generally a good investment, as proved over centuries, but for reasons stated in the article, now is not a good time to buy in NZ. There will be better times and bargains ahead, when the market reverts to historical mean.

Hi VOR

What is the "historic mean" of property and when is the return to these "historic mean" going to happen?

Historically, the big influence on property prices is the cost of mortgages - not wages - and for the past 40 years bar the last 10, interest rates were 8 to 10+% whereas the long term view is for continuing historically low rates of 4%. Look at long term mortgage and term deposit rates and the expectation of those with knowledge and influence (i.e. the banks) is that interest rates look to be at these levels for 7 or more years.

So do we wait seven plus years - and even then very uncertain - for this return to "historic mean" to happen?

Historical mean of both interest rates and price-to-income ratio. These are both way out of whack. Very unusual times. Predicting when it will change is impossible, but it will over time. What is clear is that when it does, I don’t want to have not accounted for the change adequately in a buy decision, which I don’t think many people have in the past few years.

Hi VOR

"Historical mean of both interest rates and price-to-income ratio."

So historic interest rates and price-to income ratio.

The start of the housing boom in 2012 was related solely to cheap money (low interest rates) becoming available. Wages remained stable and nothing to do with the boom; it was solely interest rates which chiefly drove the boom.

Interest rates will again continue to be the main determinate and as said, banks - and even Orr - think that low interest rates are going to continue for some time - i.e. "the new norm".

Yes price-to income ratio will be a factor but will be nullified by buyer demand due to high levels of immigration and housing shortages and supply - neither of which seems to be being currently addressed.

“price-to income ratio will be a factor but will be nullified by buyer demand due to high levels of immigration and housing shortages and supply”.

That is only one scenario and amounts to a prediction. Things could happen quite differently, so I wouldn’t bet substantial money in things playing out like that. Also, history shows it would be unwise to put any money on “a new normal”.

"Historical mean" Do you do stand up comedy too?

Odd, remind me to one of our cancer patient similar reply. Until we can only nod to the stadium status then understand why..reality sometimes difficult to acknowledge.

"when the market reverts to historical mean"

FYI, there are two potential interpretations of this comment with respect to house prices which may give diverging conclusions (and expectations of future house prices):

1) historical average house price to income ratio

2) historical average annual house price increase - 7.2% (aka "house prices double every 10 years")

CN, sure, after a boom of high percentages (above the norm) rises are likely to be lower for a string of years, even negative. They can overshoot on the downside by a lot too.

Interest rates were very high in the 1980s and very low now. Neither is the historical norm. In terms of prices doubling every 10 years, even if that happens, it can really matter when you buy. If you buy at the peak of a boom, it can take a lot longer than 10 years to double from there.

"If you buy at the peak of a boom, in can take a lot longer than 10 years to double from there."

Yes, and the owner may no longer benefit from the subsequent rise in house prices, if the original purchase was financed with high levels of debt, and the owner was forced to sell as the owner lost their job in the recession (and unable to find an equivalent replacement job) and was unable to keep up with the mortgage payments. Saw that in 2009/2010 in many countries around the world.

Property owners must be able to hold on under ALL economic conditions.

"House prices double every 10 years"

Ok, let's work this through.

- Assume a $500k mortgage now at the best 3.39% rate. This is a monthly payment of $2215 over 30 years.

- House prices double in 10 years. The mortgage payment on $1m becomes $4429 (assuming you can raise double the amount for the deposit).

- But interest rates are going to drop? If the OCR goes to 0% then mortgage rates would be 2.39% so the mortage would be $3894. (Note: where is the mortgage rate drop for the next doubling once we hit 0% OCR?)

- But wages will increase? Factor in wage rises at a generous 3% and that makes the cost of that mortgage in today's dollars = $2897

So to support this doubling in ten years, you would need to increase mortgage payments by 31%. Where is this money coming from?

In 10 years time, who actually owns these houses to sell?

"We suggest that property is now a bad investment"

OK

It says NZ property, at this time.

Is “OK” your full reasoned argument?

Full and final, ..... pretty concise huh? ….. Sure beats "return to historical mean" (hysterical mean joke though)

... there is a kernel of truth in your cynicism ...

" Mr Anderson ... pray tell , where would you suggest we invest our money... if not in houses ? "

.... " ... good question ... I'm pleased you asked ... have youse guys heard of Index Funds , perchance ? "

NASDAQ went up 33% in 2019. Up 110% since 2015. Me, the idiot, has been keeping my future house deposit money in term deposits instead. But you know, it could go down 50% next year. Or up another 30%. Nobody knows.

Excellent article, and great to get one free of the usual property BS machine.

I think multiple property investment has been a great investment in the past, but I think it's fraught moving forward from here as discussed in the article.

I also don't think capital gains will be anywhere near as great in the next 10 years as the bulls suggest. It will go up, but I think it will be 30-40% higher than now - not 100% higher (double)

If I had spare money to invest, I'd definitely do shares rather than property at this point.

Fritz I am glad to see that you see the light.... In a few years (or sooner depending on how well you do) you can capitalize the gains, borrow and buy an investment.

I am happy to own a home, but am not convinced property is a great investment moving forward.

I am genuinely pleased for you. I know when we went back to owning a ppor it was such a good feeling and sense of freedom. Even if the house was a dive. The good thing is that after a bit of tlc its worth a shitload more and good to live in.

thanks.

It is a good feeling, I must say.

Thanks for your commentaries, while I disagree with a lot of it, it has changed my perspective a bit, especially regarding the question of whether to buy my own place (rather than a property investment).

My biggest change of mind is that while I don't think property will 'boom' in the next 10 years, neither do I think it will fall (other than maybe one or two dips along the way).

I do think now is a good time to buy for FHBs (was even better 6-9 months ago), provided it is achievable. Unfortunately for many people it's still not achievable. I've only just been able to make it work.

All of those highly negative views you had last year really got up my nose. Did you ACTUALLY believe that the Auckland market would fall 15 percent?

Well, firstly I said it could drop by that sort of amount in 2021-2022. I still think it could if there's an economic shock. There's obviously not much room to cut interest rates from here.

But as I said yesterday, I think prices will be higher in 10 years than they are now. That's all I needed to be satisfied of in order to buy a house as an owner occupier.

I still don't think for people thinking of buying investment property today that it's necessarily a great investment.

I can answer you that, Did you ACTUALLY believe to fly with Boeing 737max before the two jet crashes & subsequent release of fact findings, grounding directives, internal Boeing memo etc. - In all probabilities.. everything have the chance of it, it's back to risk mitigation. Personally we all want to hear what we want. In the end? Take it or not, believe it or not...di da du..

I keep asking myself, how long can the property price growth last for NZ without real business investment and wages increase? We've even out stripped London in overinflated property markets where at least their wages are much higher and better able to support property prices. Currently the London average property price is £458,363 ($902,970) and Auckland's city average based on the recent QV data is: $1,244,959 (£632,265). And we have much smaller wages, crazy isn't it.

Here's a link to the UK's average house prices for Q4 2019: https://www.thisismoney.co.uk/money/mortgageshome/article-7864225/House…

The funny thing about modern investing is that asset prices are now based mostly on growth assumptions. The expected growth is already built into the price.

Fundamentals don't matter anymore, psychology and mania do. Just look at rental yields in the fancier Auckland suburbs - my gut feeling is that most new landlords are losing money there at the moment and their "business" relies solely on expected capital gains.

The other day I was talking about property with my boss, and I asked him if he thinks it makes sense that Auckland is one of the most expensive (by house price to income ratio) cities in the world... He said he doesn't understand why it's not number 1! This, coming from a person who has travelled all over the world, flies to London 5 times a year, just shows to me how blind some kiwis choose to be when it comes to property.

Auckland is nowhere near the productivity of cities like London, Hongkong, LA, New York etc.

Just because someone has travelled around the world multiple times, it doesn't mean that they have developed an appropriate framework to value financial and physical assets (or even an understanding of how to value financial and physical assets).

Those two are mutually exclusive.

I know many people who are similar to your boss.

Many people use the following frameworks to value residential real estate:

1) house price compared to recent transactions of comparable properties in the area

2) house price vs current replacement cost

3) reversion to historical mean - average historical house price increase for the last 50 years (aka house price double every 10 years)

4) shortage between underlying demand and underlying supply (not effective demand vs effective supply)

My answer would be: "as long as NZ can get immigrants from other emerging economies."

Averages can be deceptive .

"Why owning multiple homes is not good wealth creation" Ahem... Dean Anderson is bosom buddie with Shamubeel and we know what happened to Shamubeel "owning a house makes no sense" Eaqub.... of course he bought a home ... and property investment I wonder??

The larger, better funded investors will always stick with property, because of strongly rising rents (thank you labour) and capital gains. Direct property investment is regarded as the best around.

I have some very clever, very well off and financially savvy friends / acquaintances who don't own any investment properties.

I think if people are expecting big rent increases moving forward they might be bitterly disappointed.

Firstly, I dont need rising rents or capital gains to run my business... for the sake of the next group of house buyers I would rather house prices stay static, they did in auckland in 2019. As far as rents go the trend has developed and this will continue due to govt botch ups. Just have to look in wellington this month, it used to be only students finding it hard but now it is also others cant find a property to rent. Wish I had bought in Wellington

I wish I'd bought Amazon in 2009 and hadn't sold Apple at the same time, but there you go.... you'd rather be a position to hold people ransom, I'd rather invest in companies shaping the world.

Oh cmat, you're so much better than us… buying and selling apples

Youre right. Youve invested in one of the great sweatshop exploiting companies to ever exist, helping 3rd world labourers get flogged for 4/5ths of sweet F all and paving the way for other MNCs to follow in their lucrative footsteps

My experience from rental hunting in AKL last year:

Under $600 / week -> 30-50 people viewing each property, in multiple batches.

Over $600 / week -> Crickets. Only one other person showed up to the open home (Nicely renovated 2br house in Campbells Bay). We could even negotiate from $630 down to $600 + lawn mowing included.

Oh and they didn't put up our rent this year.

600 per week would be pretty low in my opinion.. easily pay that in sth auckl. Of those who missed the >600 they had to go somewhere as did you.

They most likely got a rental for below 600. The point I'm trying to make is that rental prices can't go up forever. Since it's paid by average people who are already struggling to save, there is an upper limit on it.

If there is no upper limit, then why isn't the average rental yield in Auckland the same as in Rotorua or Invercargill?

If there's an upper limit why do rents keep rising every year for…. ever, and what's your magic "upper limit"in $ rent/week ?

My rent hasnt gone up in 3 years, 700, 3 brms, central auckland (western springs) - awesome backyard. Thankyou

Good on you, it must have hit the magical "upper limit", rest assured it will never go up again

You're really good at pretending to not understand what the rental upper limit means... You know damn well what it means, that's why you don't ask for $50000 per week on your rentals (if you have any). If there is no such limit, why are rental yields 4% in Auckland and 7% in Rotorua? When the housing shortage (haha) is supposedly worse in AKL, why aren't people paying 7% here as well? Why aren't landlords asking for much more?

Residential property investment is a charity, landlords ask for their costs plus a small nominal fee. Nothing more.

Because the limit is tied to incomes, and incomes increase every year on average. Duh...

You know exactly what he means by upper limit.

Rents cannot keep pace with housing increases. That's a simple fact controlled by supply (of money). This is a fact over the recent boom years. It is a certainty there is an effective ceiling on rent, with minor inflation related (not house price related) increases all that's possible. That's the point.

I had 5 years recently before moving when rent went up an aggregate of 5% over 5 years.

Landlords who do well are those who limit increases do way better - what's the point of trying to squeeze another $50 out and have empty property. As the commentator correctly pointed out, at the high(er) end of the market, there's much less demand. That's the end of the market where the properties are worth more, and yields are anemic. My landlord had a gross yield of just 2.8%.

It's pointless to try to explain it to someone who most likely already knows these things, but is only here to try to make me look like an idiot.

Make you look like an idiot? Well, thats not going so well for him, its not you that looks like an idiot.

Good points.

I commented here last year that rental properties in the eastern suburbs were struggling to be tenanted, presumably the high rents were part of the reason.

Because rentals have gone up a bit in the last 3-4 years, prices have been flat, and interest rates are much lower, I think many more people would be looking to buy rather than pay a high rent.

We had been paying $790 pw in rent, we pay about the same now for our mortgage so it was a no brainer really to buy.

I think this will be a factor in areas with higher rents.

3 years ago there was a much bigger differential between renting and paying a mortgage.

Rubbish! I've been told by many experts that The Great Property Clock is the only thing that dictates house prices.

Auckland median will be $2 million in 2024! Surely the average person will be earning $150k per year by then, so that they'll only have to save for 20 years for a deposit.

You are exaggerating to make a point I know but just wait and see

At this point I'm willing to admit that I'm not capable of predicting anything in modern economics. I also doubt that anyone can predict anything about it - apart from the obvious (eg. interest rates won't go up to 10% next month). It's all based on psychology and whatever the major banks decide to do.

We all make choices. You seem to keep telling yourself to expect the worst which affects your view.

Interesting, I think my "predictions" for 2020 (which are really just my wishes) are very optimistic and would be very good for more than half of the country. They might seem to be "the worst" from your point of view, because you would lose your expected capital gains. People have different circumstances, and what might seem doom and gloom to you, might be a glint of hope for wannabe FHB's like me.

A prediction is not a wishlist, this is a business site, the logo is "helping you make better financial decisions". It matters little what you or I "want" to happen in NZ in 2020, it matters what WILL happen, and if you or I can predict this mostly correctly, then we can "make better financial decisions"

From the article, a tipping point may be more than 50% of adults in rentals. Seems obscene for a country that once prided itself on home ownership.

What is overvalued more? shares or property?

In the current investment world, finding something that is undervalued is like looking for a needle in a haystack. The stock market is full of pumped up prices, from company share buybacks, do some tyre kicking , look at fundamentals, if you own share in a power company, go and have a look at the dam, is it always full of water?

CGT is irrelevant, I never sell, new properties are brought with the rental income, you could call that organic growth, probably why I've only got six properties, but I'm happy, mowing a few extra lawns , and grabbing a paintbrush, that's more important than money. Beats sitting on a plane to the other side of the world every year ,and back, that some people think is fun.

… Financial advisor's opinions

And one with very little skin in the game compared to a typical property investor

"new properties are b(r)ought [sic] with the rental income"

So you dont take out loans using the equity? That would be a first.

Never have, never will.

DIYman,

So, you buy new properties with the rental income from the existing properties-no loans. Thus, when you had only 3 properties with say an average rent of $550 pa giving you a gross rental income of $85,800pa, you simply saved that amount until you had enough to buy another property. Is that right? Perhaps you took off the costs of rates and insurance which might have reduced the net amount by 25% to around $64,000pa. I am assuming no maintenance costs, though that is a little hard to believe. Assuming a purchase price of around $550,000, that would have taken you over 8 years. You must forgive me if I find that more than a little hard to believe.

Your comment about checking to see if a power company dam is always full is simply bizarre and shows that you don't understand how they work.

When you see a Studio Apartment in a retirement village priced at over 300k you just know that house prices aren't gunna fall.

So ho in investors,still plenty to be made esp if you can put in a decent deposit.

I don't quite understand your logic. Why do you think the current price of an asset sets a lower boundary on it's future price? Is there any reason why the price of that retirement village apartment can't change to, say, $250k a year from now?

the best advice i recd a long time ago is go against the advice of self proclaimed gurus. property investment is fine, just like any other investment, as long as you have your eyes open. Investing with closed eyes would lead to disaster in any investment class. Remember, the self appointed property gurus around 2009 where they advised, get out of res properties "right now". The savvy ones wished investors took these gurus advice and a lot did. guess who were the buyers.

Exactly the point, if you are going to make anything out of anything, be it property, bonds or shares, you need to be a counter-cyclic investor, not a follower,

I remember the end of the 80s, when I got out of property, just keeping my own home, and 2000, when we went back in, and in that ten years, my money was in zero rated bonds. Sure it gets taxed at the end, but nothing beats compound growth, ie reinvestment of earnings, at those interest rates.

The only reason its a bad investment is the same reason stocks are - cheap money. There are a very small number of property deals that add up now...where vendors are being realistic.

ohhh, a smart comment !

It has been quoted many times over the last 40 odd years that property is a bad investment. History tells us different it has been very good. Technology has killed of inflation hence current interest rates. This is the new norm as I see it. I will continue to have the greater share of my wealth in property a 3.8% return on a big number is just fine. Having liquid investment's in managed funds is part of my strategy too, great returns of late and access to cash when required. I say never take to much notice of the soo called experts, the only people I listen to are those who have a proven visiable track record of investing. Talk as they say is cheap !

the only people I listen to are those who have a proven visiable track record of investing. Talk as they say is cheap !

You mean like Ray Dalio? Do you think he would see NZ residential housing as the right place to park money?

You say "talk is cheap". I would suggest that you want to look for "cheap assets". NZ houses are not cheap by any stretch of the imagination. Furthermore, we know that without the banks' ability to lend into existence, this could never have happened. That ability to keep doubling down on mortgage lending is looking more suspect by the day.

Houses are currently very cheap in Christchurch, but not forever.

J c - I have no idea who Ray Dalio is ?? Just for you Jc the people I have listened to and learnt from have been people I have meet and got to know on a personal level. People who have backed themselves and made good decisions. Auckland has woken up from its usual 3 year hibernation growth year's ahead. Happy investing !

And you didn't google him to find out eh. Much better just to learn from people you know on a personal level. That's not an echo chamber at all, is it.

"the only people I listen to are those who have a proven visiable track record of investing. Talk as they say is cheap !"

LOL.

Rental investment is in my view, for people who have little or no financial education, much the same as growing kiwifruit which is also known as dial a crop because it has been so well refined by husbandry service providers that literally anyone can get involved. Owning your own house is logical but the costs involved and risks of losses from tenant damages are high and coping with multiple rental properties is only getting worse as the healthy homes requirements (long over due) take effect. Investing in mixed class assets has proved highly beneficial for me and when I need to I can liquidate holdings over night...no openhomes or upset tenants in site. You won't catch me diddling around owning a few boxes and puffing my chest out at the golf course and daring to call myself an investor because I owe the bank on my rentals...I'm far smarter than that and I suggest more of you educate yourselves, get out of housing and into real investing, you won't look back.

Oh man, awesome comment.

much the same as growing kiwifruit which is also known as dial a crop because it has been so well refined by husbandry service providers that literally anyone can get involved

BTW, Zespri Among Most Counterfeited Brands In China.

http://www.perishablepundit.com/index.php?date=6/26/07&pundit=3

Hey mate you always have acid reflux that's getting and bringing you down! It takes a range of skills to do well in property investment and not just fundamental financial education. If you saw the program last night about the guy who started Just Water it would show you that being successful is about a lot more than being an analyst. Anyway having read many of your posts interesting as they are, you cannot claim the intellectual high ground.

Thanks for your well thought out contribution. A documentary on the Just Water franchise...gosh that'd be on par with watching Suzanna Paul infomercials, what did you take away from it? Apart from a watercooler you don't actually need....

Living with The Boss

The business owner moved to Otara and stayed with his employee and did everything with him for a week. Tony is a thoroughly nice person but had to work all his life now 72

You sound far too clever and wealthy to be talking to us peasants on here. Please refrain from spending your precious energy, go and enjoy your many millions at your carribean mansion oh great one since you are obviously so successful

I think his post shows quite clearly that he is not wealthy, the adjective you're looking for is more along the line of envious, bitter,

My thoughts exactly

I suspect you all belong to cult of somesort, you say the samethings without thinking...brainless.

How did you become an intellectual giant 4thE

Brainless would be comparing investing in kiwifruit with property

is that the best you can come up with, clearly you are suffering from some kind of impairment, frontal lobe damage perhaps from falling off your skateboard...or even fetal alcohol syndrome courtesy of your inbred parents? ? Had any tenants take you to the tribunal lately or kick your house full of holes at your expense? I'll give you to Monday to process that and get back to me..sharp... not!

Maybe you should find better tenants than my inbred parents then lol. I'll hand it to you though, you've got that Steve Jobs attitude about you haha

The biggest drawback for managed funds & Kiwisaver are the fees.

Kernel has an annual 0.39% management fee for holdings of $24,999 or less. The fee is slightly less for holdings over $25,000. This will have a huge effect later on when balances are larger. There is also a monthly membership fee, albeit a small one.

https://www.moneyhub.co.nz/kernel-review.html

I won't be charged any fee for holding self managed stocks, only for buying.

The second drawback is relying fund managers to use your money wisely.

Perhaps people don't have the time to spend hours and hours researching stock data or reading company annual reports about stocks and companies, but they may indirectly interact with stocks on a daily basis (through brands, industries, services etc)

- What brands do I come into contact on a regular basis?

- What industry do I work in?

- What services do I use?

An example: I tend to fill up my car at Z petrol stations - why is that? Convenience? Price? Location? Attentive staff? Rewards / Bonuses? If upon further research I decided they had a competitive advantage, moats etc, I might consider them a good pick. But I don't think if I could pay a fee to someone who may not fully understand the holdings they have, or ones I don't understand myself.

I think picking stocks that you understand will give you success.

Yes, but an individual investor cannot bundle stocks as Kernel has done. Furthermore, there are cost benefits for regular contributions for these baskets that individual investor's cannot compete with. Nothing to do with individual stock picking.

Who on earth is this Dean Anderson, never heard of him!

If Mr Anderson is such a knowledgeable person with investing he wouldn’t be needing to advise others.

If there is an investment that can provide you with income of 6 figures and make you millions with very little initial deposit let me know Mr Anderson

"If Mr Anderson is such a knowledgeable person with investing he wouldn’t be needing to advise others."

Remarkable understanding of business models there buddy.

Hey, Mr Jobs, if your computer was so great, why did you try to sell it to others?

MisterB, what a weird thing to say!

If a financial adviser knew what to invest in then why does he need to continue to be advising others what to invest in for payment?

A professional property investor does his own buying and investing and gets his own reward!!

So, following your logic here THE MAN 2, you can't be a good property investor as you are advising others to do it?

What about the property bulls idols.. Ashley Church and Tony Alexander.. didn't they have day jobs. Obviously they must be not too bright.

Each to their own as to what anyone invests in!

What I do know is that there are various levels of property investors, just like various levels of business owners!

Personally never buy negatively geared property and the property needs to purchased at under true market value and have upside.

If you follow these rules you have a recipe for financial independence without doubt!

No, I am not being paid for an income by saying on Interest.co that property investing can be very profitable.

I have plenty of time available so if people are looking for experienced advice for free, I can offer that!

https://www.fma.govt.nz/investors/getting-financial-advice/types-of-adv…

"Generally, if someone is providing a recommendation or opinion on buying or selling a financial product, or providing financial planning services, they have to be an authorised or legally registered financial adviser. If you’re not sure, or if you think someone is providing a financial advice service when they shouldn’t be, you can contact us for more information."

You mean other than the fact that a financial adviser who does not provide financial advice is not really doing his job??

So much about you makes sense now.

MisterB, advising someone and selling something to someone is totally different

Why would I want to bundle stocks that I don't fully understand? Or risk having a fund manager not fully understand them either? Does the fund manager know why Auckland Airport is a good investment? Or are they just hitching a ride like everyone else? If they have to explain why a stock is good to all their clients, it is less time they spend researching or analysing other stocks. Fund managers have a lot of capital to work with, therefore they aren't going to put it into companies, that are perhaps smaller, or less well-known. Also, while it has its tax advantages, Kernel has no overseas exposure.

I think one should treat these index fund investments as part of their diverse portfolio, which would include rental property. One cannot replace the other, the amount required to invest being vastly different. The money that might go to these index funds won't reduce the money available in the country for property purchase/investment, so it is not one vs the other. It is one supplementing the other.

The advantage of index fund investment, etc is you can decide the amount and the market does not as in house investment.

I don't think the author is trying to draw investment away from property to funds. He has presented the pros and cons. It is for the individual investor to gauge and act upon.

I hope people understand NZ runs an immigration economy. And it is not something new; we have been doing it for a while. While NZ wants wealthy immigrants to ingest cash into the economy directly, NZ also needs not-so-rich immigrants to be the working bees. The problem is, just like many different aspects of the 21st century NZ, the lack of vision and planning or even the acknowledgement of it. National's 9 years was a perfect example.

Why plan for and invest to align with high immigration, when that costs money?

Just artificially bolster GDP and let the plebs experience more congestion, more overstressed health care and education systems and unaffordable housing without doing anything about it.

(Sarc mode on full)

As long as we continue to flood in overseas arrivals, which no one voted for, its status quo. It is either protect the bank debt ponzi, or protect the average tax payer which last time I checked is actually the job of the govt. Interesting election this time around.

Isn't the whole Millennial vs Boomer cold war based on the inequality of those that were able to buy property when it was "affordable" then leveraging the capital gains to purchase more, and those that cannot buy even their first property due to both rent and house prices rising out of proportion to income?

If all these "amateur landlords" divested themselves of their rental properties, and instead invested in New Zealand companies, wouldn't that be better for the economy? Of course, MP's could lead by example but I don't see that happening.

The "Millennial vs Boomer cold war" is just about having someone to blame for ones own shortcomings.

Yeah, I guess millennials should blame their shortcomings. Shortcomings such as not being born 30 years earlier, or not having rich parents. Sometimes it feels like we are playing Monopoly on a board where everything is already owned by others.

That said, I actually blame politicians, not boomers. Boomers are doing what gives them more power and money, perhaps I would do the same. Politicians should be the ones working on preventing such a huge generational wealth gap, but they only care about being elected and filling their own pockets.

How about you stop blaming others altogether and spend that time focusing on things you do have control of, to improve your own life?

To put it down to ones "shortcomings" is a bit of a low blow.

Why? we all have shortcomings, what matters if what we do with them;

a) blame others, whinge and moan

or

b) face them and do our best to improve our shortcomings

I don't blame boomers or millennial's or anyone else for my situation. That was all of my own doing. 15 years in Japan ruined me financially.

However, it seems to me that New Zealanders in the past have made it a lot harder for New Zealanders in the present to become owner-occupiers.

Maybe that's too broad a brush? More accurately, successive New Zealand Governments have made it a lot harder for present-day New Zealanders, but since the majority of cabinet members of our current Government are boomers, it's no wonder that measures like CGT get quashed and "OK Boomer" remarks create such a furor.

Of course, in another 30 years, the future New Zealanders from Gen Alpha will be blaming the Millennial's for not doing enough.

Come on man! Really unfair.

Young kiwis today face much bigger barriers to home ownership than 20 or 30 years ago.

It's just not credible to argue otherwise.

Oh it's so unfair, boomers didn't have Email had to write letters mail them and get a reply in the mailbox 1-2 weeks later, couldnt see photos taken instantly had mail the film and wait 1-2 weeks get the prints, no Google, Uber, Airbnb, online banking FB, Google maps, mobile phones, computers, etc… etc… boohoohoo. We're all born when we are, we can't change it, accept what you cannot change and focus what you can change to improve your life. Sorry not feeling sorry for the complainers and whingers.

Game theory experiments that introduce only a handful of "wolves"among hundreds of "sheep" rarely end well. As long as there is a non-zero number of investors who don't show empathy (ie. are happy to snap up assets from the people who actually need them) and suffer no penalties for doing so, things won't get much better for the average wage earner.

Making money gets easier the more you have. The solution would be to disincentivise owning multiple properties either via taxes, or by making other (productive) investments more attractive. Instead we get stimulus from the bottom (sorry for the mental image...), extra cash handouts to the poor that go straight into the landlords' pockets. We are living in a trickle-up economy, and policy makers should act accordingly if they really care about inequality.

"Making money gets easier the more you have." And does that fact encourage you to make money ... because all I read is moaning and sniping. There are people a lot worse off than yourself, people who haven't got two cents and exist on a benefit

It is as if stating my opinion on interest.co.nz is not the only thing I do...

I know it's hard to imagine, but commenting here is not my main activity. I'm making money. Sometimes I'm making money while commenting here, gasp!

Also, expressing an opinion or stating facts that aren't positive isn't moaning. But I guess if you actually wanted to argue one of my points you would have done so.

Housework’s, you are correct that the first million is the hardest and after that things do get progressively easier!

Banks just love property investors that are cashflow positive and asset rich, and will generally bend over backwards to accommodate you.

What I can guarantee is that people who are financially secure and do t need to have a 9 to 5 job will be happier than their lot than people who are not earning enough to live on and are t looking to improve their circumstances.

There are people who do things for themselves and their families financially and then others who just hope that things change so they become financial!

Reality is that you need to take action for your situation to improve!

Not rocket science!!

You seem to have forgotten about the people who do things for themselves and their families financially and also hope that things change so they become financial (sic)...

The two aren't mutually exclusive, I don't know why well-off people think nobody else works as hard as they do (or did).

Jester, of course people do things for their families and hope that things change for the better financially!

Reality is that if a family has too many children for their financial circumstances, then nothing will change if they are working on wages or on welfare.

This has always been the situation, and my point is that you need to do more than just working for wages if you want to improve the financial situation.

The average family in NZ aren’t that satisfied with their financial situation but do not do much about it.

Yes you will get by financially generally working for wages but it will not get you financial independence.

What over generalized drivel.

Man, you've had the coolade believing it's impossible to be financially independent on wages. How independent will you be if you had empty houses and no buyers?

Fortunately we would be just fine!

Each generation uses or tries to use the advantages they have to improve their well being. After the war, it is true that the governments spent large sums to make it easy for the populace. Politics thereafter started screwing up things for successive generations. Large scale greed, avarice and corruption (called lobbying in the west) made it difficult for fresh youngsters with ideals to adapt and grow in the big bad world. Climate change has also spoiled it for all, but Boomers escaped it during their formative/growing years.

One thing though, the Millennials of today seem to be easily distracted by Social Media, Smartphones, Internet etc and are losing the focus on financial improvements for themselves. They are getting trapped in by some of Gen X's/their own inventions..

Two Headline on the same website at the same time :

"Residential property is now a bad investment"

"Why you should not believe the "experts"

To be fair, experts in economy tend to disagree with each other over many things. It's very far from an exact science, economists aren't engineers. So whatever an expert predicts must be taken with a grain of salt.

Trust me expert engineers often have different opinions too!

Balance in reporting the views ?

"due to the concepts of loss aversion and anchoring, few vendors are prepared to sell at a loss, instead holding on until growth returns"

The key assumption is that the property vendor is able to hold on until growth returns. There are scenarios where the property vendor is unable to hold on and is under pressure to sell. Some scenarios include:

1) a highly leveraged owner who has a high debt service ratio - then an unexpected recession occurs, and the owner is made redundant. The owner is no longer able to continue debt payments. If the unemployment rate rises significantly, then this puts pressure on more property owners.

2) business owners - many small business owners have put up their homes as collateral for business loans. If the business goes into financial difficulty, then the house owner may be unable to hold on - refer example here - https://www.stuff.co.nz/business/property/116378021/ecohouse-businesses… (Remember this happened when the economy was still growing. What do you think happens if the economy goes into a recession?)

For more examples, look at

1) Ron Hoy Fong's 7 D's.

2) examples during the GFC in 2009-2010 where property vendors were unable to hold on ...

I have read and heard of this all before in the eighties and 90s, wait until a financial crash happens, these people run and hide, property wins in the end, sure it will take a hit, but will win in the end.

I remember these finance people saying say away from the Government super schemes and go private. THEY WERE WRONG and fooled many people, luckily I was not one of them.

Check yours out before listening to these people.

some of the "negatives" listed are actually positives or at worst neutral.

"construction costs have risen" makes owning existing property a good thing.

"interest rates have been falling for 20 years and are unlikely to go lower" - struggling to see how interest rates being at historic low is somehow a bad thing for property investment, when it is in fact it is one of the most positive things imaginable.

"there are just not enough houses" again - this an uber-bullish reason to own residential property rather than a negative.

Also conveniently leaves out the much more favourable tax treatment of property vs managed funds etc (no taxes on long term capital gains vs high tax rate on managed fund earnings).

What is more, compare the two scenarios of a cashflow neutral (or even slightly negative cashflow) property vs a non leveraged managed fund. after 25 years al you have put into the property is the initial deposit (if any) and you are left with a mortgage free property that likely has at least doubled in value. Whereas, a managed fund after 25 years would leave that same amount you spent as a deposit collecting at best average share market returns, less a management fee, less income tax.

@KBKIWI I think you might need to read the article again, especially about housing supply. It's also the change in interest rates that the article is saying affects house values, and if they go up, the value could/should fall.

Finally the tax treatment is better / more favourable for managed funds over property, so not sure of your logic. Capital gains on funds (i.e. unit price and share price increases) are untaxed in NZ, and in a managed fund the top tax rate on income is 28% (i.e. dividends), lower than the 33% on property income.

Well , it was never a really good investment if one considers all the risks of tenant default , interest rate risk , damage and costs of insurance rates and repairs .

From a yield point of view , it was always a shocker .

The only thing that took care of the investment value was immigration bouying demand and thereby raising prices , and that has NOT changed

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.