By Joseph Darby*

JBWere's 2025 Bequest Report estimates $1.6 trillion is the total value of wealth expected to pass between generations in New Zealand by 2050. BERL puts the figure at $1.11 trillion over the next 20 years. Media coverage has been breathless. Financial services firms have built entire marketing campaigns around it.

Uncomfortable questions follow. How much of this will actually arrive for typical families? When will it show up? And how much will remain after aged care, retirement spending, tax changes, and the sheer unpredictability of the next quarter-century have taken their share?

Rather than take the headline at face value, let's stress-test it.

What the number doesn't tell you

New Zealand households hold roughly $2.4 trillion in assets, with residential property close to half. Those born before 1966 hold roughly 60 percent of total individual net worth. When transfers come, they will be dominated by houses, not liquid cash.

Distribution is uneven. The wealthiest 20 percent of households hold about two-thirds of total net worth. Statistics NZ's 2024 update found no statistically significant change in wealth for the bottom two quintiles. $1.6 trillion is an aggregate. It says nothing about how much lands in any particular lap.

Timing is also likely to be late. Australian Productivity Commission data shows most inheritances arrive when recipients are in their fifties and sixties. New Zealand demographics are similar. If you are forty-five today and factoring a future inheritance into your financial plans, the timing may disappoint. Most recipients are in their sixties or seventies by the time wealth transfers. By then, the mortgage pressure and school fees it was supposed to help with have long since passed.

Aged care: the wealth destroyer nobody wants to model

Residential care doesn’t come cheap. At Auckland and Wellington providers, published schedules show residential care running from about $73,000 per year for a standard room to over $110,000 with premiums and extras.

The government's residential care subsidy is heavily means-tested. The current asset threshold for a single person is $291,825. Where a partner remains in the family home, the property is generally excluded from the assessment, but if someone is single or widowed, the home's value typically counts. In practice, someone entering care with a house worth $900,000 and $200,000 in savings may be self-funding until assets are substantially depleted. Average funded stays may be around 18 months for many, but long dementia trajectories can last five or 10 years. Five years of care at $90,000 per annum consumes $450,000 before accounting for inflation or the cost of maintaining the property in the meantime.

For many families, the assumption a home will pass to the next generation collides with the reality of selling it to fund care. Care costs consume the wealth long before anyone inherits it. The bills are large, and the maths is unforgiving.

Boomers are spending their own money. Rationally

New Zealanders over 65 are spending more on travel, healthcare, and lifestyle than any previous generation of retirees. Fair enough, they earned it. But it reshapes the maths.

Retirement Commission research shows 40 percent of those over 65 rely entirely on NZ Super, and a further 20 percent have only a small supplement. KiwiSaver has an average balance at ages 61 to 65 of roughly $69,000. These are not people sitting on piles of untouched capital.

Many retirees are also paying attention to the evidence. A 20-year study of 3,200 families by the Williams Group found 70 percent of wealthy families lose their wealth by the second generation, and 90 percent by the third. While this was overseas research, the data would likely equally apply in New Zealand. The primary drivers: poor communication, unprepared heirs, and weak planning. If seven out of 10 inheritances will be substantially gone within a generation, the rational response is to consider whether gifting with intention during your lifetime, or simply enjoying the fruits of your own labour, might produce a better outcome than leaving a lump sum to be squandered.

And plenty of retirees are reaching this conclusion. Local research is lacking, but a 2024 Northwestern Mutual survey found only about 22 percent of baby boomers expect to leave an inheritance. A Charles Schwab survey found nearly 45 percent would rather enjoy their money while still alive. The "Die With Zero" philosophy, from Bill Perkins' book of the same name, has real traction among a generation deciding it would prefer to fund grandchildren's school trips now rather than leave a contested estate later.

The pool of wealth available for transfer is smaller every year. Retirees are simply doing what you would hope people would do with money they spent decades earning.

The trust and property trap

Inland Revenue's trust disclosure data confirms roughly $470 billion in assets held across trusts and estates, dominated by shares and real property. For beneficiaries, this creates a liquidity problem few anticipate. Wealth on paper is not usable wealth.

Receiving a third share of a jointly held house gives you a valuable asset you cannot easily spend, sell, or divide. The common scenario is familiar to any estate lawyer: one sibling wants to keep the family home, another needs cash, a third wants to renovate and sell for a better price. Legal costs, valuation disputes, and strained relationships can run for years, eating into the very asset everyone was supposed to benefit from.

Only 55 percent of New Zealand adults have a will. Most family trusts were established long before the Trusts Act 2019 introduced its disclosure and record-keeping requirements, and many trustees are still catching up with ongoing compliance obligations. The practical gap between "valuable estate" and "money in your account" is far wider than most people assume.

The future is not cooperating with anyone's forecast

Before anyone builds a financial plan around wealth they do not yet own, it is worth recalling how often confident forecasts, including those made by very smart people with very good models and all the best intentions, turn out to be spectacularly wrong.

There are too many examples to count.

HSBC dubbed New Zealand the "rock star economy" in January 2014, predicting growth would outpace the developed world. Within 18 months, New Zealand was on an HSBC vulnerability watchlist as dairy prices slumped and growth cooled. A decade later, per capita GDP had fallen 4.6 percent in the largest per capita recession since the Global Financial Crisis. The same pattern of overconfident prediction appears globally: in the 1980s, the consensus was Japan's economy would overtake the US, right before its asset bubble burst and produced a lost decade. Japan’s economy has never caught the US. And billions were spent preparing for the Y2K millennium bug, which turned out to be one of history's most expensive non-events.

Forecasting complex systems is genuinely hard. The $1.6 trillion figure rests on demographic projections, which are more reliable than economic ones, but the amount and real value of transfers depend on variables no model can fully capture.

Surprises cut in unexpected directions, too.

One variable worth watching: medical breakthroughs are accelerating, particularly in AI-assisted diagnostics and cancer immunotherapy. Every year of additional healthy life is wonderful for human welfare. It also means another year of retirement spending, another year of potential aged-care costs, and less wealth left to transfer.

Which leads to an even larger wild card.

The tax collector has noticed

Politicians of all persuasions have spotted the scale of wealth concentrated in boomer balance sheets, and the fiscal pressure to act on it is growing. New Zealand currently has no inheritance tax, no gift duty, and no comprehensive capital gains tax. Relative to most of the OECD, this is unusual. Whether it remains the case over the next two decades is an open question.

Treasury's Long-term Fiscal Statement projects net core Crown debt reaching 200 percent of GDP by 2065 without significant policy changes. You read that correctly, 200 percent. Net debt has already risen from below 20 percent of GDP in 2018/19 to over 40 percent today. Those numbers create pressure for broadening the tax base, and the obvious targets are headline-grabbing forms of wealth which are currently lightly taxed. Labour has already proposed a capital gains tax on investment property. The Green Party's 2025 alternative budget proposed a wealth tax and a 33 percent inheritance tax. The IMF's 2025 Article IV mission explicitly recommended New Zealand consider a comprehensive capital gains tax and a land value tax.

Regardless of which party is in power, the fiscal gap suggests the direction of travel matters more than the specific form any new tax might take. And here is where the $1.6 trillion headline starts to look particularly fragile: if a CGT, inheritance tax, or wealth tax is introduced before peak transfer years in the 2040s, the after-tax value of transfers materially shrinks. Or more specifically, the great wealth transfer may just be a transfer to the tax collector. Combine taxation with inflation and rising care costs, and the pool available for the next generation is considerably smaller than the headline suggests.

The political difficulty of taxing wealth in a country with high home-ownership should not be underestimated. But Inland Revenue research suggesting New Zealand's wealthiest 311 families pay an effective tax rate of 9.4 percent, compared with 20.2 percent for wage earners, creates political momentum. As boomers age and their electoral weight diminishes, it is feasible voter sentiment may shift toward taxing inherited wealth.

Even without formal tax changes, adjacent policy pressure is building. NZ Super is not means-tested today, but debate about means-testing or raising the eligibility age has intensified as costs rise. Residential care asset thresholds are indexed annually. While not technically taxes, tighter settings would have the same practical effect: retirees using more of their own wealth to live, leaving less behind.

So what should you actually do?

If you are in your forties or fifties, build as if no inheritance is coming. Make your own savings do the heavy lifting. The best financial gift you can give yourself is never needing someone else's wealth. And the best gift you can give your parents is meaning it when you tell them to enjoy every dollar.

If you are the older generation, have the conversation. Not about how much anyone will receive, but about the realities: what care might cost, how assets are structured, what the trust says, and what your own retirement needs require. Consider whether gifting during your lifetime, for a grandchild's education or a first home deposit, might deliver more value than a contested or late bequest in two decades. And if policy changes are coming, whether a capital gains tax, tighter means-testing, or something nobody has proposed yet, make sure your plan can absorb them.

The question worth asking

The Great Wealth Transfer makes for a compelling headline, and sure, some families will pass on meaningful inheritances. But as a financial plan, it is a weak foundation. Distribution will be uneven, timing may be late, aged-care costs are real, retirees are spending more of their own savings, and the politicians are salivating.

Build your own house first. The safest plan for most New Zealand families is to own their financial future outright. Nobody wants to be in a position where they catch themselves calculating how much better off they would be when a parent dies. Financial independence removes the calculation entirely. And for the older generation: you spent decades earning it. Spend it without guilt.

*Joseph Darby is a financial adviser and CEO of Become Wealth. The firm is a licenced provider of financial advice and Discretionary Investment Management Services (DIMS), trusted to advise on over $1 billion. Become Wealth has offices in Auckland and Christchurch, and clients nationwide. Disclosure: This article is the author's opinion and does not reflect the opinions of Become Wealth. Nothing in this publication is, or should be taken as, an offer, invitation or recommendation to buy, sell or retain a regulated financial product. Become Wealth provides financial advisory and investment management services to clients, some of whom may be planning for intergenerational wealth transfer.

21 Comments

Good write up, esp the bit on how uncertain timing and the values actually are

Bit like the property chat on here really, plenty of confident takes, but it usually plays out slower and messier

Recent governments quite rightly have sharply increased scrutiny of family assets before approving any funding for hospital care services at rest homes etc. This is overlooked by a good number of commenters on here decrying that such folk have such wealth stored in the family home in the first place. In most of the circumstances it is largely no more than that, people have retired in their home and lived on the pension and their life savings. It should be acknowledged then that these people will fund themselves in care as opposed to someone who has spent all they have earned and thus are of an immediate full on cost to the tax payer.

Yes, and in many instances looking through family trusts that were set up in an attempt to protect assets from hospital care costs.

it is worth recalling how often confident forecasts, including those made by very smart people with very good models and all the best intentions, turn out to be spectacularly wrong.

https://www.latimes.com/opinion/story/2026-03-17/paul-ehrlich-wrong-eve…

“...The battle to feed all of humanity is over. In the 1970s and 1980s hundreds of millions of people will starve to death in spite of any crash programs embarked upon now.”

“If I were a gambler, I would take even money that England will not exist in the year 2000,” Ehrlich prophesized during a speech in 1971. He also said that the U.S. would be rationing water by 1974, and food by 1980. That smog in L.A. and New York would cause some 200,000 deaths per year. That Americans born after World War II wouldn’t live past 50.

...England still exists. Life expectancy in the U.S. just set a record high of 79 (in Europe it’s 81.5). There is no country in the world with a life expectancy under 50. Air and water quality are much better today than they were in 1968. Global food production has exploded. Famine is rare, and almost always a product of war or the backward command-and-control economic thinking Ehrlich supported. And fertility rates are worrisomely declining throughout the developed world, and far beyond. Slightly more than half the world’s nations have sub-replacement birthrates. We have not run out of any resources and America has more forests than it did a century ago.

...Perhaps the most remarkable thing is not that Ehrlich turned out to be so wildly wrong, but that he was so obviously wrong from the beginning. My old boss Ben Wattenberg battled Ehrlich throughout the 1970s and 1980s. His feud began with a 1970 article for the New Republic titled, “The Nonsense Explosion,” in which Wattenberg explained that even as Ehrlich was writing about soaring birthrates, birthrates were already declining.

...Simply put, his pessimism was simply too big to fail."

Sounds like the typical interest.co.nz commenter. And whenever something bad happens (eg war) it makes their doom and gloom correct, even if it’s been wrong for 50 years. Probably doesn’t believe in official statistics I imagine.

Yes. Fama has said of Shiller, who is the idol and often quoted by one prolific DGM poster on this site, that he is "consistently pessimistic about prices, so given a long enough horizon, Shiller is bound to be able to claim that he has foreseen any given crisis.” Shiller has been saying this since 2005.

Like crossing the road, there is always a risk but we take care to look and consider the risk and minimise it. Those who live in fear with Shiller will be life-long renters contributing to the wealth of their landlord.

As soon as it's the system's fault

You've greatly diminished your own capacity to exert control over your own life.

If there is such a thing as free will, it's in knowing the world is a brutal place, and singing along with it regardless.

You want wealth transferred to you now, not once Labour get in and place an inheritance tax on it.

The children of boomer property owners win again, the rest, not so much. Even after 25% falls from peak.

Main point I took away from the article was about Boomers deciding to spend it on themselves rather than the next generation "squandering it"

Many have the means to do both, and still have plenty of change afterward

I don't understand your comment Bobbyknuckles.

As a boomer, I am still alive, and rightfully expect to access health care and support in my fading years when I am more frail. I don't expect taxpayers to meet my living costs as I age just as i didn't expect taxpayers to meet my living costs in earlier years. As I age, some costs of living will become disproportionately higher compared with earlier periods. I expect my healthcare costs will increase and other costs, relatively, to decrease.

I may have $x in assets and savings. Spending that as needed in my later years is not squandering wealth. It is acting in a self responsible manner rather than expecting taxpayers to meet my costs so that I can pass wealth onto my children that they have not earnt.

I am fortunate in that my children stress to me, to live my life fully. They do not count on an inheritance. But I am not profligate, I live a full and satisfying life. And I expect there will be something meaningful left over for them at the end.

If seven out of 10 inheritances will be substantially gone within a generation, the rational response is to consider whether gifting with intention during your lifetime, or simply enjoying the fruits of your own labour, might produce a better outcome than leaving a lump sum to be squandered.

And plenty of retirees are reaching this conclusion........

No need to defend your generation. I'm not attacking boomers LouB. I felt the main theme of the article is that boomers should spend it on themselves, leaving nothing to pass on. If anything is left, that it's likely to be eaten up by healthcare/agedcare/taxes.

Apologies, I misinterpreted which generation you suggested was squandering.

An adage I've heard is the first generation creates wealth, the second consolidates it and the third squanders it

Plus the -20% inflation loss in purchasing power......

Those born before 1966 hold roughly 60 percent of total individual net worth.

The wealthiest 20 percent of households hold about two-thirds of total net worth.

So the inference being that the top 20% of households are predominantly boomers given 60% is practically two thirds.

Politicians of all persuasions have spotted the scale of wealth concentrated in boomer balance sheets, and the fiscal pressure to act on it is growing.

Precisely. We can't afford top class healthcare and universal pensions, so eventually the govt will have to act to target those with wealth e.g means testing, additional tax on those working when claiming super etc.

Born in 1955, I agree with you.

Also agree, so long as when I can't stand working any more (also born in 55) I can actually get access to world class healthcare to keep standing... well past that methinks. As long as this Government continues to push for privatisation of what we have been paying for for (in my case at least) 55 years, we will never address the core issue of what Governments can do to promote a fair society.

I'm more than happy to pay tax, CGT, Inheritance tax and any other tax that reduces the burdens on future generations (as opposed to individual beneficiaries of unearned wealth) so long as a stable political system can provide assurances that my contributions will be part of an equitable health system, and an economy that rewards both excellence and participation.

Not sure this bunch of prats even understand what they are taking away...

Agree with that too. Well put.

I'm more than happy to pay tax, CGT, Inheritance tax and any other tax that reduces the burdens on future generations (as opposed to individual beneficiaries of unearned wealth) so long as a stable political system can provide assurances that my contributions will be part of an equitable health system, and an economy that rewards both excellence and participation.

Eloquently put. As far as an economy that rewards both excellence and participation, we have gone backwards with this for a decade perhaps e.g DEI hiring, renteirism (a few decades for this perhaps), and financialisation of more and more which doesn't seem to be slowing down.

Perhaps we will see another great stock market crash which, while causing great loss for many, would provide a more egalitarian populace to push for the greater good of all instead of the self, and be reflected in the caliber of political candidates and proposed policies, as well as engagement in politics and communities.

I searched up on ChatGPT the best year to be born in order to maximise net worth and it came up with 1951, so if aged 74 today. The reasons it espoused that year being:

Cheap entry into property

Inflation eroding debt

Multi-decade asset inflation

Favourable retirement timing

I wonder if thats true?

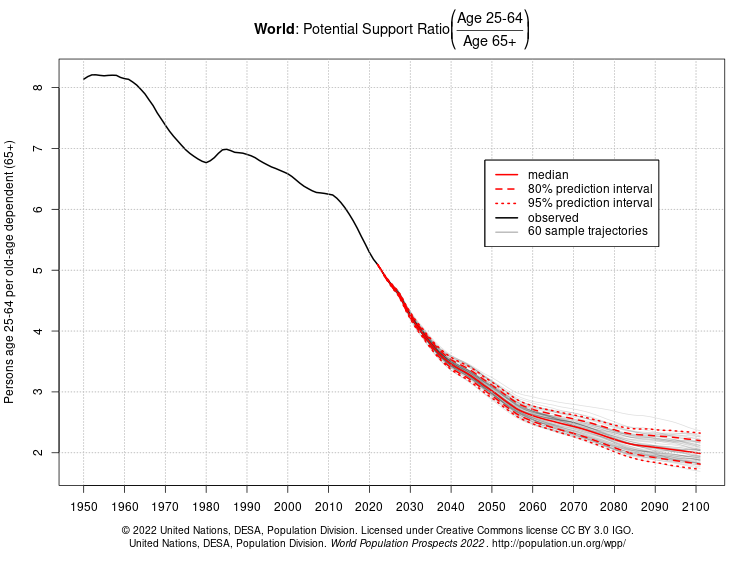

Good times - dependency ration was 8:1 vs 4:1 now, dropped int o 3:1 in 20250 and 2:1 at the end of the century. No wonder they got their pot holes filled in.

https://insightplus.mja.com.au/wp-content/uploads/2024/02/Picture4-1.png

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.