By Amanda Morrall

Fixed-interest investments may have proven a saving grace during the global financial crisis but can they deliver better long-term returns than equities going forward?

According to a majority of New Zealanders surveyed on their understanding of risk diversification as part of an international financial literacy study the answer is yes.

Asked which of the following: (a) savings account b) range of shares c) range of fixed-interest investments, d) chequing accounts, would make the most money over 15 to 20 years, 47% answered c expressing a belief that fixed-interest would make them richer over a longer time horizon.

That compares with 27% who went with a mix of shares and 22% who thought a savings accounts would achieve optimal returns.

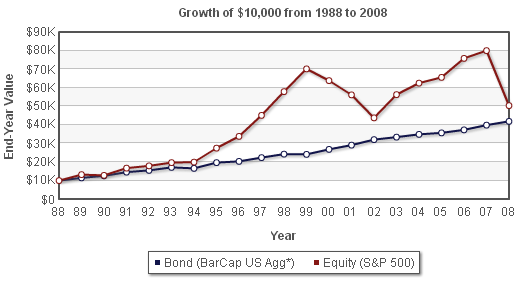

The "right" answer (debatable given recent experience) is b) a range of shares. On that question alone, 71% of Kiwi's got it "wrong.'' (See chart below measuring 20 year returns of bonds versus equities.)

As several of the eight countries that participated in the international survey tailored the question on risk diversification, New Zealand's relative performance on risk diversification is tricky to gauge, said Annamaria Lusardi, one of the academics heading the OECD study.

In general terms, Lusardi said most survey respondents, regardless of nationality, fared the poorest when it came to an understanding of risk, reward and the importance of diversification. The other main questions they were tested on related to interest rates and inflation. They were as follows:

"Suppose you had $100 in a savings account and the interest rate was 2% per year. After five years, how much do you think you would have in the account if you left the money to grow?"

i) more than $102

ii) exactly $10

iii) less than $102

iv) don't know

v) refuse to answer

And on inflation:

"Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After one year, with the money in this account, would you be able to buy..."

i) more than today

ii) exactly the same

iii) less than today

iv) Don't know

v) refused to answer

Finally, the standard question on risk diversification was this:

"Do you think the following statement is true or false? Buying a single company stock usually provides a safer return than a stock mutual fund?"

Lusardi joked that the latter could have been reworded: "Do you remember Enron and what have you learned from it.''

Savvy Germans

While the full survey results have not been released, Lusardi revealed some of the preliminary findings at a financial literacy summit earlier this week in Wellington.

Overall, Germans were among the most financially savvy, with 82% correctly answering a question testing their understanding of interest rates, 78% showing an understanding of inflation, and 62% scoring correctly on risk diversification.

Across all three, 53% of Germans answered correctly, with 72% correctly answering the interest rate and inflation question.

By comparison, less than half of New Zealanders answered all three questions correctly on interest rates, inflation and risk diversification.

Lusardi, an economics professor at the George Washington School of Business and Financial Literacy Centre, said the purpose of the international study was to assess the basic "a,b,c" financial knowledge level of the participating countries.

With governments and employers internationally shifting responsibility for retirement savings onto employees themselves, Lusardi said financial literacy would become increasingly important in the future.

Lusardi referred to a 2004 study, which found that those individuals who characterised themselves as "planners" in that they had done some preparation in this area, had a median net worth of US$308,000, compared to US$122,000 for those who hadn't done any planning.

Asked how a more recent snapshot measuring net wealth might look, given that some investors (who could be regarded as planners) saw their equities portfolios sheared in half, Lusardi said macro-economic shocks were in all likelihood beyond the scope of basic financial literacy.

For the full the interactive historical bond versus equity chart go to BondeskGroup.

The following charts show historical returns for the bond market vs. the equity market. During the past 20 years the trends are consistent - bonds have provided a steady stream of payments leading to much more stable returns. Compared to investment in equity, bonds have been more effective in preserving cash to meet predictable exp

46 Comments

1 = i

2= iii

3= true if you know what you are doing. false if you are 99% of people

Elliot, your answer to question 3 raises some other questions.

1. What makes you think you are in the 1%? Maybe only 1% of people can tell if someone is in the 1% of people who know what they are doing. Are you in that 1% also?

2. Reading balance sheets and income statements is entry level research. If everyone is reading them, why would the price not reflect that information?

3. How does doing that research protect you from things not contained in the records? Things that cannot be predicted? The question was about risk, not return.

4. If someone can pick the safest stock from publicly available, universally read, information, then why do even the best investors still choose to invest in a range of different companies?

5. Are you really claiming that it is possible to know the best investment ahead of time?

Yes, nice safe fixed interest like Bridgecorp, Hanover, "risk free" Greek debt.......perhaps some Gold like that nice man on the TV tells me....

Sorted

Now you tell me..

Had I listened to Interest.co.nz a few years ago as Hanover was one of the many highly recomended investment firms, my $100 would be worth about 3 - 4 cents now - yes a massive amount I know!

oh and Telecom shares!

Shows the importance of reading balance sheets and income statements...

Why would you willingly invest your life savings without checking out the ins and outs of an investment before hand?

Serves you right if you lost your money without doing your independent research before hand.

All Moa had to do was buy copper...sell it in 07...then buy it all back late 08...and sell it again two months back....

Twisted knickers?? A touch of sarcasm there, can you see it! I haven't lost a cent, my savings are spreaded amongst the (Australian) banks, small amount of shares ASX and a house.

Touchy lots... !

I blame two things , 1) The schooling system and 2) that our "cradle to grave" welfare state ensures we are quite clueless when it comes to saving and building a nest egg.

If like Oz we had to provide for our own retirement compulsorily , then we would be more savvy

Any arguements about my assertions/ observations?

Amanda is, I think, unfairly representing the results of the survey as far as NZ was concerned (yes I was at the seminar too and saw you Amanda - fab tights!).

New Zealanders did very nearly as well as Germans on the first two questions; it was only on the third that the results were much worse. But the Germans were asked a different third question, one in which the correct answer was rather clearer than for the New Zealand question which actually leaves considerable room for debate, as some of the comments here show.

No, Boatman, I do not agree that we'd be more financially savvy if we were forced by compulsion to save for our retirement.

Some of us might have more retirement savings, but that is not the same thing. Others might even have less, if the compulsion forced us to save money in a different way from what we'd have done otherwise.

Compulsion simply means you get told what to do. You are not required to think at all (brownie points to anybody who knows what song that line comes from). That doesn't make you savvy.

Ms DM. Glad my tights left a better impression than my story.:)

I did mention above that the risk diversification question was different for NZ but worth restating again.

As several of the eight countries that participated in the international survey tailored the question on risk diversification, New Zealand's relative performance on risk diversification is tricky to gauge, said Annamaria Lusardi, one of the academics heading the OECD study.

When the survey comes out in full, I'll revisit the story to see how we stack up.

Cheers,

Amanda

Blame nobody but the individuals, don't you realise 50% have below average intelligence, some obviously considerably below

Ask the individuals who have purchased and held Berkshire Hathaway that has delivered over 20 % compound over 35+ years if they should " diversify "

Maybe Berkshire have done that ... and yes there was always a difference between Enron and Berkshire

Run you eye down the Morningstar 5 year returns in the Saturday papers an see why equity returns are over stated.

They have delivered appalling returns over the years vs the 8% + you can get pre-tax from quality NZ bonds with far less risk than equity owners.

While it does suggest that NZ'ers think that fixed interest performs better over the long term, there are a couple of other factors here: (a) New Zealand retail investors have never recovered from the stock market crash (of 20 years ago!), so won't invest in shares unless at gunpoint; (b) NZ retail investors are fixated with property investment (which wasn't in the list of investment options).

The basic economic literacy bit suggests that NZ retail investors are even less savvy than their international peers, which comes as no surprise.

Tell me james_chch , what are the last three financial books , which you have read ?

........ we can blame the government , and the education department , til we're blue in the face ..... but how much of our financial illiteracy belongs to us , personally . The libraries are chocka-block with non-fiction material , and many have a good selection of Martin Hawes or Gareth Morgan books too boot , Peter Lynch , James Grant ....... sitting there , free for the use of , gathering dust !

Paperplus / Whitcoulls / Books'nMore ..... all sport a healthy sized business section , plus financial magizines ...... and I always have that aisle to my Gummy self ........ ( could be the Gummy B.O. effect ? )

I had to go and check. There's a few I've been browsing or half-read, but the last 3 I've actually read are: George Soros, The new paradigm for finanical markets; Niall Ferguson, the ascent of money; and JK Galbraith, the great crash 1929.

Not sure if you mean specifically investment books, rather than finance/economics. I can go back to the bookshelf if so...

Well done ! .... You are amongst the elite . Few people read a single book of any sort , after leaving school . But I wasn't picking on you per se , just making a general point , that we need to take more personal responsibility for our education .

....... excellent books , by-the-by , james_chch .

Daddy Gummy got to 95 y.o. , without ever reading a non-fiction book . The closest was an occassional dip into Yates Garden Guide ! ... DG retired on a pension .

Gummy Jr. has recently finished " The Origin of Financial Crises " : George Cooper .

...... Royal Little : " How to lose $ 100 000 000 , and other valuable advice "

..... Mohamed el Erian : " When Markets Collide "

and of course , Michael Hill's : " Toughen Up " .

The Black swan should be required reading IMHO....however in terms of books there is so much out there on the Internet that is newer and free its unbelieveable....phd's pdf's....peer reviews....mind boggling....google is your friend...

regards

Ive read a few pieces that say point to point...over a typical investors life bonds actually do as well as shares or better.....which is surprising....another interesting point I read was those who make real money know when to move from one investment to another catching one as it shoots jumping off the one about to wane.....today though is exceptional, everything is a bubble.....

Yes on the NZ shares and the crazy thing was it could have been fixed easily.....if it had been today the NZx would have been far richer, larger and dynamic I suspect....

regards

Amanda : In the chart at the bottom of your article , is the S&P 500 shown as a gross index , or an accumulation index ?

...... my point being , are dividends factored into the S&P line , i.e. compounded , or are they ignored ?

Good point. Particularly as the data is from an organisation called BondeskGroup, which at a guess makes money by flogging bonds to people.

BondeskGroup !!! ...... well spotted james_chch ...... sometimes Gummy is as dim as a glow-worm's arm-pit .

Cheers !

LOL. You missed a career in comedy Gummy. Give me your top 3 picks for financial books, it'll throw into my Five-fold Friday books section. And if you have aless b(ond)iased comparative reference chart send me the link and i'll put that into the story above. Cheers, Amanda

Gummie's Starter Pack of Essential Investment Books :

Peter Lynch : One up on Wall Street

Philip Fisher : Common stocks and Uncommon Profits

James O'Shaughnessy : What works on Wall Street

....... and for those suffering from ADD , an easy peasy junior's booklet :

Robert Cole : The Unwritten Laws of Finance & Investment ... ( GBH : They're written now ! )

Roger Ibbotson presents the comparative returns of stocks vs. bonds in an easy to follow format , here : ( link not working , bugger ! )

www.corporate.morningstar.com/ib/documents/MediaMentions/AreBondsGoingToOutPerformStocks.pdf

Thankyou , Count ! ..... and that is why you are the chosen one , the leader of the revolution , and the Gummster is a mere prawn in your game .

Good read GBH.............for lobbing that in ...you are duly promoted to Rank of Lobster...with accompanying celery...on expense accounted gruel.

I might give my self a little promotion ...I'm feeling a little shellfish.

Thanks for that Gummy. Can I entice you in a pristine copy of Allan Hubbard's biography sitting on my desk?:) "A man out of time.'' Hmmm, expect this one will be widely available at the sidewalk sales, not stocking the shelves of local libraries in NZ any time soon. I'll have to get BH to make us some t-shirts or something. For now, you have my thanks.

Thanks for the offer , Amanda ...... gotta finish Alan Greenspan's book " It wasn't all my bloody fault .... not all . " ........ then I'll peruse the other Allan's excuses ..... ooops , I mean " memoirs " !

@GBH -"Amanda : In the chart at the bottom of your article , is the S&P 500 shown as a gross index , or an accumulation index ?" '"

Gummy your query is somewhat immaterial as the S&P 500 index is a biased relection of winners over time.

Bankrupt companies are expelled and new stars are added along the way.

Hence actual returns to participating index investors are not recorded.

Flat fugle & nonsense ! ...........The S&P 500 is re-weighted every 6 months , and the stocks at the bottom , with the lowest market capitalisations , are replaced by stocks outside of the index , which have grown bigger than them .

...... there is no " survivorship bias . "

Actual returns must include dividends .

From 1926 until 2010 , fully 44 % of the S & P 500's returns came from dividends ........

...... so the chart at the bottom of the story is grossly mis-leading , understating the returns from equities by 44 % ...... a chart that was drawn by a bond trading firm .....

And naturally , they wouldn't be biased , would they ! ......... ahem !!!

I dont think that chart is wrong.....also Ive read this elsewhere....bonds dont pay much per year but they dont lose money and over the long term do close to as well or better...looking at the S&P you can see investing in it at the wrong time could lose heaps (like today IMHO). So to make money on shares you have to get in at the right time and out more or less at the right time....I made a tidy sum over the last 10 years but now Im out.....The p/e etc is just insane....

Also in terms of dividends v share price has that ratio changed? By this I mean in the period 1926 to say 1946 was the return a bigger % per year than share price gain than today (1991 to 2011?)?

regards

Err hello...

Intelligent Investor by Ben Graham?

I have a copy of " Intelligent Investor " , but am yet to read it . ..... I just selected 3 easily approachable tomes , which I have read . .

..[... at 640 pages , Graham's work is rather large , and sorely lacking in pictures of the Natal Sharks Super 15 cheer-leading squad ...]

Wot? No recommendations for Olly Newland books? Snobs.

Kiwis seem clued up on property as it is , without encouraging them more !

....... but if I was compiling a list of 100 top investment books , I'd find a spot for one of Uncle Ollie's .

I'd find a spot for one too. My table is a bit wobbly at one end. Could be just the thing for under one of the legs.

I wonder how many of the people in New Zealand who have actually bought investment property actually have read up on the principles of it.

I have spoken to a number of people who own second houses who don't seem to andeither leave it to their accountant or muddle along not getting the best out of their investments.

Same principle as buying a share without really understanding value vs growth stocks, dividend imputation credits etc.

Yup ! ..... And that is why I have little patience for those who stuff up their finances , but then get a government bail-out . The library has enough free investment books to read , to keep one informed , and out of trouble .

...... if Gummy , who isn't the crispest cracker in the Weatbix packet can understand that , anyone can .......

And the govt. wonders why our capital markets aren't performing and the excuses - investors are still hurting from the 87 crash, the failed finance companies, and can expect to hurt if the property market ever corrects.

I bet investors got into the sharemarket because of the hype and because everyone else was doing it without any research/knowledge of what they were doing. Same goes for investing in finance companies. Same goes for property. I don't know how many times I've asked this but how many "property investors" did their homework and bought an "investment" property because of the long term yields and not because of the tax advantages and capital gains?

RE: Olly Newland. Reading the above, one wonders how many of cadre of the failed property developers and associated finance company conduits were either products of the Olly Newland School, Seminar Circuit, or influenced by him, his methods or books?

Just curious, as I've only been living here a few years. Have any of these guys ever been seriously scrutinised by the media? Anything like investigative journalism? Because they don't even have the basic requirements applied to financial advisors and fund managers applied to them. Has there been any real regulation or scrutiny?

Getting late ....better put something up...friday..ya.....h.....this seems like a nice place...lots of warmth n connection......hey ho happy day..

Mike was going to be married to Karen so his Father sat him down for a little chat. He said, 'Mike, let me tell you something. On my wedding night in our honeymoon suite, I took off my pants, handed them to your Mother, and said, 'Here, try these on.'' She did and said, 'These are too big. I can't wear them.' I replied, 'Exactly.. I wear the pants in this family and I always will.' Ever since that night, we have never had any problems. 'Hmmm,' said Mike. He thought that might be a good thing to try. On his honeymoon, Mike took off his pants and said to Karen, 'Here, try these on..! She tried them on and said, 'These are too large. They don't fit me.' Mike said, 'Exactly. I wear the pants in this family and I always will. I don't want you to ever forget that.' Then Karen took off her panties and handed them to Mike. She said, 'Here, you try on mine ! Mike did and said, 'I can't get into your panties.' Karen said, 'Exactly. And if you don't change your smart-ass attitude, you never will.'

And it's a true story , folks ....... just the names are changed to prevent a certain Dis-Count from being knocked out by the Miss-Count

Just no sliding one past you is there.?......... still every Junta needs it's Contessa...or there would just be bullets n camouflage.....me ...an old tea chest...an a real pretty camel.

If you go down to the woods today......................... You're sure of a big surprise

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.