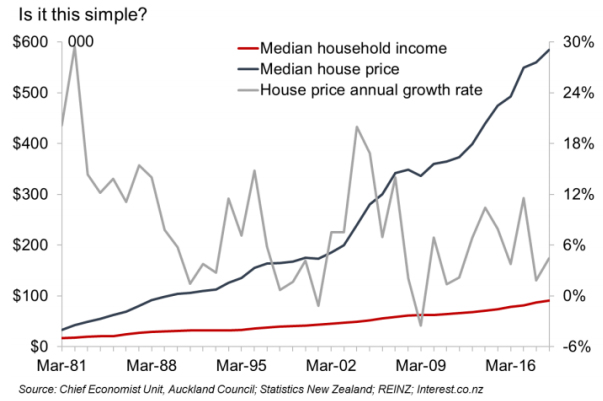

• New Zealand median house prices increased almost 18-fold between 1981 and 2019. In the same time, median household incomes increased only 5.4-fold.

• The 1970s appear to have been the glory days for house buying, with much lower interest rates and inflation than in even the early 1980s, although data is too limited for the evidence for this period to be unequivocal.

• Arguably the mid-1980s was the toughest in the last 38 years to buy a home in New Zealand.

• Today’s lower taxes and inflation mean mortgage serviceability has improved, and on paper, median income households have a far larger share of gross income available for spending on the mortgage.

• But median income households today often can’t secure loans because of small deposits and the share of gross income that would be required to service their loan, even though theoretically they could meet these payments.

Debate rages between generations. Each seems convinced the other “had it easier” in their day. If you were buying a house in the 1970s or 1980s, they were cheap relative to incomes, say today’s 20-somethings, allowing you onto the property ladder of untaxed capital gains. “We had no overseas holidays, avocado or regularly replaced cars, and had an apple crate for a dining table for the first three years,” says an older generation.

Is there validity to either view?

Headline income and house price growth

We compared median household incomes, house prices, floating mortgage rates, inflation rates, and tax regimes between 1981 and 2019 to understand the implications for servicing debt for a purchaser in each year. This was no simple task – data is hard to come by for several indicators even as recently as the 1980s. Data limitations prevented us from examining Auckland back past 1999.

Making a meaningful comparison requires some assumptions, but we can draw some headline conclusions. We know that New Zealand median house prices increased almost 18-fold between 1981 and 2019. In the same time, median household incomes increased 5.4-fold.

Percentagewise, recent annual national house price rises pale in comparison to the early 1980s and 2000s. National annual growth rates peaked at nearly 30% in 1982 and in the eight years including 1981 to 1988, annual growth rates were higher than in all but one year in the 2010s.

Let’s get (a little) technical

It’s important to understand what our model shows before jumping to conclusions, so we need to cover a few technical basics. We evaluate how long it would take a median income household buying the median priced house in New Zealand in March of each year to pay off the mortgage, based on a number of necessary assumptions.

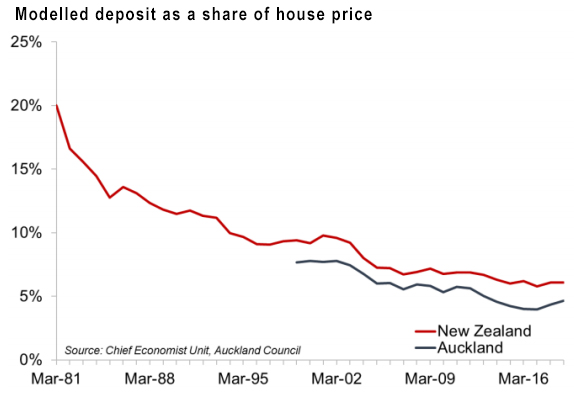

We use 1981 as our benchmark year, assuming a median income household could spend 30% of its income on servicing a mortgage for a median priced house that year, with a 20% deposit. The 20% deposit and 30% of spending on the mortgage simply set the benchmark against which subsequent years are measured.

We assume that the household has a single income earner. This was almost certainly not true on average in 1981, and much less true in 2019, but it makes calculating the income tax burden of the household much easier. In reality, as the number of working adults per household has risen, average tax burdens will have fallen in percentage terms compared to what our model estimates, but childcare and transport costs will have risen, the net result being unclear.

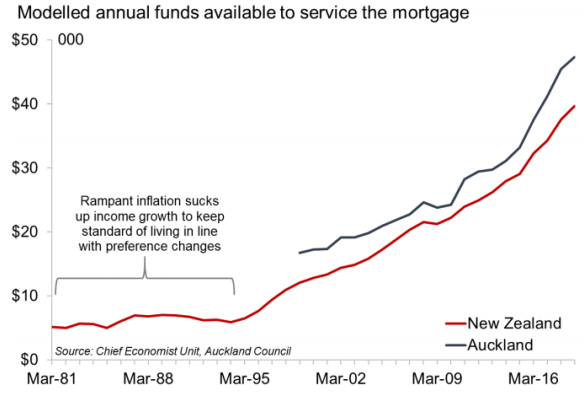

In 1981, every dollar not spent on tax or servicing the mortgage is assumed to be available for other household spending such as groceries, clothing, electricity, holidays or transport.

Gross income – Tax – Mortgage spending = Other household spending

From 1982 onwards, we assume other household spending adjusts based on the inflation. In years of strong inflation, the dollar value spent on other household spending rose fast. If incomes didn’t rise enough to cover the rise in living costs, the money available to spend on the mortgage fell. In other words, from 1982:

Gross income – Tax – Other household spending = Money available for mortgage spending

Further, we assume a household’s ability to assemble a deposit rises in line with their income. Over the 38 years in which incomes grew one-third as fast as house prices, this has major implications for the ability to assemble a deposit.

To estimate a payback period for households that have purchased homes in recent years, we assume that incomes and inflation will continue to grow at 10-year averages of 3.5% and 1.9% respectively. We assume floating interest rates average 6.0%, the 10-year average (data limitations also force us to use floating rather than fixed rates throughout).

We make further minor assumptions to compare Auckland data to national data.

It’s pay back time

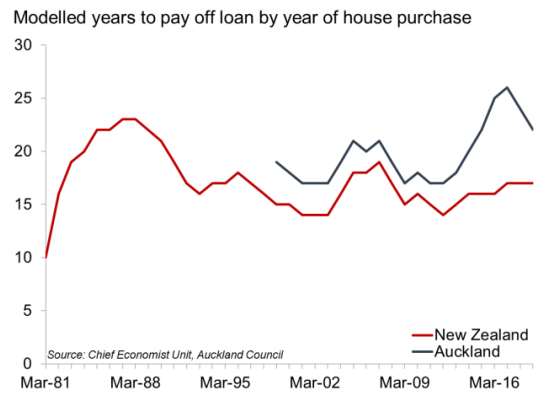

The number of years it would take to pay off the mortgage under these conditions rose from just under 10 for a household purchasing in 1981, to just under 23 years six years later. By the early 1990s, the time had fallen to just under 16 years. In the early 2000s, the time bottomed out at under 14 overall before rising through the house price boom years of 2003 to 2007.

It appears the mid-1980s were the worst time to buy, and payback periods have remained fairly constant between 1993 and 2019 in the case of New Zealand. The challenge has not been loan serviceability, but getting a loan approved with a suitable deposit in the first place.

For Auckland, payback periods have always been higher as the city’s income premium hasn’t bridged the house price gap. Here it’s been a mix of the ability to secure a loan as in the first place as well as serviceability challenges. At the peak of the boom in the year to March 2017, payback periods were particularly high in Auckland, but have since moderated to just under 22 years.

Not rocket science

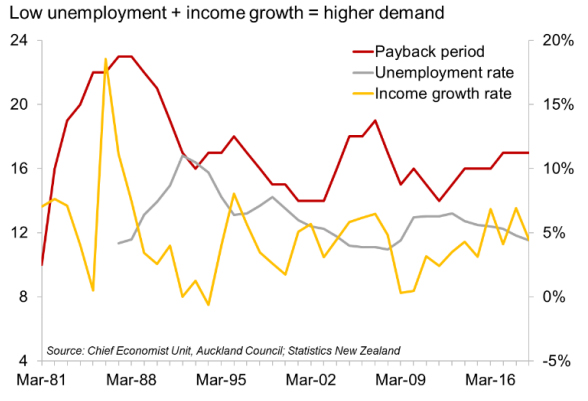

It’s worthwhile simply graphing payback periods against some of the key factors. As always, we’d point out that if houses are built at a rate that matches demand, prices don’t rise. But within the context of prices rising, it’s interesting to highlight their relationship to the key factors.

When unemployment rates were low, and incomes grew sharply, house prices rose sharply and payback periods surged, as in the mid-1980s and the years just preceding the Global Financial Crisis (see chart above). The unemployment rate and years to pay back in particular display a textbook inverse relationship. The economic slowdown in the late 1980s and the resultant rise in unemployment almost single-handedly led to payback periods for median income households moderating.

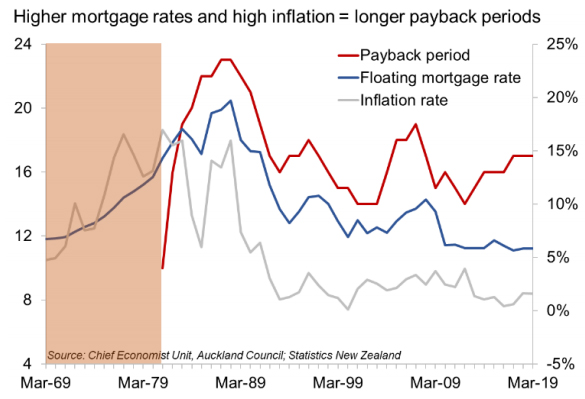

The other drivers of longer payback periods are high inflation, which is often coupled with income growth simply because wages rise to try and offset the surge in costs of living, or because wage rises stimulate inflation. Periods of high inflation meant the cost of meeting other household spending needs rose faster than incomes, leaving less money to service the mortgage unless dramatic changes in household spending patterns happened at the household level.

It goes without saying that higher mortgage rates meant longer payback periods as well. The extreme example was in 1981, when the payback period was only 10 years as mortgage rates were actually lower than inflation.

In interpreting the results, remember that the actual number of years given as the payback period is less important than the pattern the graph shows, as the line would move up or down based on deposit or mortgage spending assumptions.

But it’s the detail of the model and what we don’t see in the headline graphs that highlight some major differences between eras.

1980s horror or 1970s utopia?

In the mid-1980s, house prices grew fast, mortgage rates rose and inflation pushed up the cost of other household spending dramatically. These factors meant median income households would be unlikely to secure a loan at all without making massive sacrifices in terms of the 1981 benchmarked standard of living. The model is structured to allow debt to balloon in the early years as long as you can catch up later, which is obviously not an approach the banks actually take.

Instead, to buy at all, households would have needed to scrimp for a bigger deposit, and then scrimp some more to meet the repayments at the mortgage and inflation rates they had to deal with. Household spending needs increased in price by about 130% between 1981 and 1988 assuming Consumers Price Index (CPI) adjusted weightings and preferences were applied, while incomes rose “just” 71%. Floating mortgage rates averaged around 17% during this time.

A major frustration in this study was incomplete data for the 1970s. We do know that inflation and mortgage rates were lower through this period, and house price growth was weaker than in the 1980s. At first blush it seems likely the late 1970s were a much easier time to buy, without having to make the same sacrifices as home buyers even five years later. The 1970s was also the prime baby boomer buying era. But without median household income data, it is hard to determine conclusively that this was so.

The deposit hump

The model assumes that in 1981 the household has a 20% deposit, and that the available deposit rises in line with median household income in successive years. Because incomes rose slower than house prices, this means that by 2019, the median income household wanting to purchase would only have had a deposit of 6.1%, much less than most households would require to get a loan from their bank.

In Auckland, with much higher house prices, it’s even worse; the deposit is only about 4.6% of the median house price. Modelling shows that if the bank were to grant a loan, all other assumptions being held, the household could meet its repayment obligations. But loan-to-value restrictions and other risk management practices mean banks don’t typically lend this way.

If a household were able to assemble a 20% deposit in 2019, it would reduce the payback period by about 2.5 years in New Zealand, or by almost four years in Auckland. But in Auckland, that would be a big ask, needing a lump sum of $170,000.

What inflation measures do and don’t tell us

The model increases spending on other household needs by the rate of inflation each year as measured by the CPI. Every few years the CPI revises the “basket” of goods and services it includes and the weightings it assigns to each of those goods and services to determine the weighted average increase in consumer prices. To do this, it has to examine what people spend their money on and how that changes over time.

Since 1981, some items have been removed from the CPI because they no longer play a big role in consumption patterns: offal, canned meat, delivered milk, sewing machines, VCRs, buzzy bee toys, and waterbeds (added in 1988 and removed in 1993 – the definition of a fad). Added since 1980: avocados, exotic cheese, muesli bars, free-range eggs, packaged leaf salad, craft beer, massages, cellphones and internet services.

The CPI’s job is to measure price changes, but changes in the basket mix point to bigger changes in society not captured in overall price changes: quality of life improvements evidenced by the goods and services people choose to consume today. The CPI doesn’t explicitly demonstrate the change in quantity of these higher quality goods and services consumed (other than for the purposes of weighting for inflation calculations).

The model demonstrates this by showing that if people increased spending on other household needs in line with inflation, making the preference and quantity changes described by changes to the CPI over time, today they would spend only 33% of their gross income on these needs (down from 37% in 1981). This is because over 38 years, the CPI has risen slower than incomes. Accounting for tax, aspirant home owners would have 44% of their gross household income to spend on the mortgage.

Yet this is not reality, as banks do not see a demonstrated consumer willingness to spend 44% of gross income on mortgage repayments and don’t approve lending to people on that expectation. In other words, not only have preferences changed leading to a different mix of items, but as incomes have risen, people have chosen to spend more of their income on other household spending and not primarily the mortgage. At the same time, banks have managed their risk by assuming a much lower share of income will be used on the mortgage.

That depends on what a house “is”

It is well-established that since the 1970s, the size of the average new house size has surged, even after accounting for garages being internalized into house designs, but the number of people per dwelling has fallen. This change means the median house price is buying more house than it did in the 1970s, although data gaps don’t allow us to say how much more.

A little less taxing

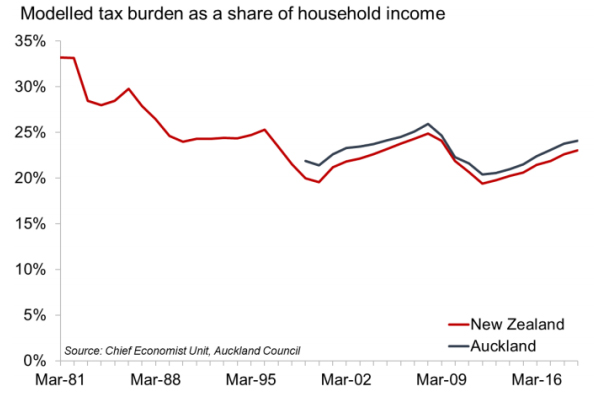

The income tax regime has also changed markedly since 1981. The average income tax rate for the median household has fallen by 10 percentage points, from 33% to 23% of gross household income. Because tax rates are set nationally and Aucklanders tend to earn more than the New Zealand median, the share of income going to taxes here is likely higher. As an aside, modelling the household tax burden also shows the impact of bracket creep on median income households between New Zealand’s irregular tax rate and bracket reviews.

New Zealand underwent a fundamental shift in tax policy in the mid-1980s when income tax rates were sharply reduced from a maximum rate of around 66% to 33% in four years, and GST was introduced. GST is captured in price changes via the CPI, so is dealt with in the other household spending category in our model.

The summary is that all else held equal, the median income household today has at least 10% more of its gross income available than in 1981, assuming they kept their spending patterns in line with inflation and changes in preferences over time captured by the CPI. With a greater number of people per household now working, the tax burden reduction is probably a bit bigger than this.

While our model assigns this extra 10% of income to servicing the mortgage after increases in other household spending are accounted for, in reality it does not appear to be the case that people are generally using this extra money in their pockets to pay the mortgage. On its own, this would imply around 40% of the median income household’s gross income being assigned to the mortgage payments.

In conclusion

While the data doesn’t allow a complete analysis, evidence suggests the 1970s was likely an easier time to buy than the 1980s. On paper, household incomes today seem adequate to cover the cost of servicing a mortgage at the New Zealand level at least, even with small deposits.

But in reality, the combination of a small deposit and a high share of gross income going to servicing a loan appear too risky to lenders and the Reserve Bank. Further, it is evident that as technology and competition have lowered the price of various goods and services, consumers have acted in line with economic theory and consumed more of these goods and services. These choices have left less money for spending on the mortgage. Banks respond to this observed behaviour by being more cautious about how willing they are to lend.

* David Norman is chief economist at the Auckland Council. This article was first published here. It is here with permission.

58 Comments

We need to get rid of equity requirements altogether. The reserve bank still doesn't understand that house prices only go up.

The ruling elite and general public of NZ think that house prices are like the Titanic: "unsinkable." They will provide all kinds of "evidence" to explain why that is. Now, there is no "evidence" to suggest that house prices are sinkable (only cases from eleswhere), but you will see plenty of denial as to why prices can't go down. But in a country where Mike Hosking is a household name and where Robert Shiller would be largely unknown, this is to be expected.

Prices will only fall if the era of an ever expanding credit market comes to an end. As long as we can keep pumping it up with money to generate a competitive return, why would you invest anywhere else? We can just make it more affordable by lowering interest rates and deposits forever. 2008 is when economics was solved, now we just ride the gravy train.

Where did you learn this and why do you believe it? You're saying that you can produce more of something (money) and "generate a competitive return" from it (which doesn't actually make any sense). The assumption is that this can continue forever and a day. Now that might appear to you to be happening now, but this supports the"unsinkable Titanic" mindset.

I personally read their comment as sarcastic. They can correct me if I'm wrong with this assumption.

Yes, it could be 1.) sarcasm [I guess]; 2.) trolling; or 3. a belief.

You don't need to produce anything to get a return. If the value of your investment is rising at a faster rate than other things as a result of continuous easing, there has to be something to incentivise the money to move elsewhere. Similar to a Ponzi scheme, but without the need for additional investors.

Unsure if OP is troll or just economically and financially illiterate

Rude. Just singing from the central bank hymn sheet. Also was sarcasm. Will add sarcasm warning to future comments. Also politically houses get the too big to fail privilege. Just read a monetary policy statement.

Also politically houses get the too big to fail privilege.

Right. This fits nicely into the "Titanic is unsinkable" mindset.

And (Ctrl-F for " land ") text search reveals zero instances of Land Prices. Selective investigation, much? Because the percentage of 'house' price attributable to 'land price' has surely increased over the surveyed period. As the Productivity Commission has concluded, TLA's and their dopey policies uninformed by urban economic reality, have pushed unimproved land prices to a multiple of 8-10 times underlying rural land prices, because of squiggles on planning maps.

And also why make the assumption that all household income is for a single earner. The fact that increasingly two incomes plus is needed to pay the rent, or mortgage has a huge effect socially on how families operate, including how and why they consume goods and services.

Depends on where you view point is; Take Auckland for example where older generations have had the most opportunity to benefit for the onslaught of foreign buyers who were particularly prevalent over the last few years, so much so we had to bring a Foreign Buyers Ban. Older Kiwi generations didn't have to compete with that many overseas speculative investors and mass immigration in competition for a home.

Not to mention the wage stagnation that our younger generations have faced due to mass migration/globalization, so have less buying power.

IN the 80s sizes of sections were still 6 to 800 sq m, now they are barely big enough to swing a cat. The complete demise of the home garden is imminent.

...and with it things like pet ownership and living space for kids, along with our ability to influence our immediate surroundings.

Good work David. As thorough research as could be expected given the multitudes of different ingredients one could add into it. We first bought in 1982 & we had to shine our shoes wear our best suit & shirt to see the bank manager in those days. In fact, getting a time at all was thought of as a blessing. And many were turned away or told sorry, your record with us needs more input. And then we were paying 19.5% at one point in the late 80's which seemed a lot at the time, & still does in hindsight. My advice to you youngies is to buy land. They're not making any more of it.

Yes buy land because they are not making it any more. Of course humans invented this thing called a building with these other inventions called stairs and elevators that allows floor space to be built on floor space to cope with the shortage of land...

How many food crops are grown on elevators?

There's actually a lot of innovation going on in the area of vertical gardening:

https://www.cropsreview.com/vertical-gardens.html

Much of the funding is coming from impact investing arms of big-ticket investors like Goldman Sachs and Prudential Financial.

https://www.theguardian.com/environment/2016/aug/14/world-largest-verti…

The world’s population will bloat to 9.7 billion by 2050 and 70% of people will reside in urban areas, according to the World Health Organisation. Using large swathes of land for growing food will not be an option, supporters of vertical farming argue.

Declining household formation, lower birthrates, aging first home buyers, yet a significant increase of female participation in paid employment since the 1970's, additionally a significant shift in females transitioning from part time to full time paid work . With low unemployment, high participation rates , historically low mortgage rates , yet surprisingly home ownership rates continue to fall, and in Auckland particular (where we need an economist to tell porkies to justify unsustainable real estate prices ) the lowest rate of home ownership nationwide other than Gisborne.

What everyone overlooks is the rise of feminism which has its advantages and disadvantages. Back in the 1960's and 70's a man (usually) could earn enough to feed, clothe and provide for his wife and kids, still pay the mortgage and have some left over. His wife stayed home and did the highly honourable job of minding the house, doing the cooking, washing and looking after the the kids.

This seems laughable now but encouraging women into the workforce by demeaning the minding the home and the family has led to vastly increased financial pressure on families, the doubling of income, the quadrupling of house prices, a lowering of standards, more crime and immorality, greater divorce rates, more homelessness, and a lots of other evils. One wonders if our predecessors had it right and womens emanicpation is a double edged sword for which we are now paying the price.

I agreed with every word except increase in immorality. As an elderly person told me in 1970 referring to Woodstock and Free Love - we were doing everything back before the WW2 but we just didn't talk about it all the time. More recently we have entered one of those embarassing ages where prudery rules.

It is not the emancipation of women that is at fault, it is the outsourcing of production and the importation of too many fully formed adults to give an illusion of growth because we cannot seem to function without it, and at the end of the day, that means more people, in a world that does not need that.

To think that women need chaining to the kitchen sink in order for society to function is pretty damned ugly thinking. Clearly you never had to slave day after day over never ending chores (and chores they are) while your partner grew their life and status, yours relying on theirs, till one day, sick of that one, time for a trade in, find yourself alone, not able earn decent money and unlikely to find another partner.

At the same time governments were pushing hard to create affordable housing supply.

It's a great argument for a UBI, as it appropriately values the contribution of the stay at home/child-rearing partner.

Did David Publish his model? How does "Modelled years to pay of the loan by year of house purchase" decrease from 26 to 22 for Auckland between 2015 and 2018 (second plot), when he fixes the future rates and inflation. This makes no sense.

Agree, that doesn't make any sense at all!

It would only make sense if prices had dropped significantly between 2016 and 2019, which they haven't...

I thought prices began to stagnate in auckland around 2016, incomes have risen by some measly amounts, and interest rates have dropped. The modelled years to pay off the loan would definitely have dropped. 26->22 seems quite significant but perhaps reflects just how powerful the lower interest rate is (with the assumption it doesnt uptick in the next 20 years)

He is using a floating rate. Mortgages taken out in 2015 are paying the same rates now as those taken out later in 2018. The plot shows someone who bought in 2018 would pay their mortgage off 1 year before someone who got their house in 2015, its like those 3 years of payment counted for less than nothing.

yes,he says he assumes a 6% interest rate. So, according to his stated assumption, the big differences in interest rates over the last few years shouldn't be reflected.

but it looks like they are....despite his stated assumption.

Maybe one of the editors can seek clarity from him.

Reading his model again the whole thing is bullshit. He seems uses the CPI to calculate the change in household expenses indexed all the way from 1981. The accumulative error between the recorded CPI number and actual changes in standard household expenses for home owners in Auckland (paying of their mortgage) over 40 years would be massive.

Yeah having looked at it again I think there are some fundamental flaws.

Assume... For simplicity we assume... Because it's too difficult we assume.

I assumed the chief economist of our largest city could have been better spent his time elsewhere than adding to a debate the generations narrative.

Who cares how it was, it's obviously a problem now. Do we as a whole not want society to be easier for future generations. Do we actively resent progeny benefiting from prior hardship?

Have you heard about the chemist, the physicist and the economist stranded on a deserted island with a can of food and no can opener... The chemist and physicist proposed clever schemes to open the can... The economist proposed that they should just assume they had a can opener...

So longer payback periods on higher amounts, and only for those who can actually scrag a deposit together in the first place? Jeez it doesn't take a rocket surgeon to guess what's going to happen to whom when rates start to lift a bit.

Best case scenario is people's mortgage repayments increase with inflation at each refinance. In other words, people lose the ability to reduce their debt burden through inflation.

Yup, people also lose their ability to increase their earnings as inflation/living costs rise. There's also a big difference in the way things like paid overtime and redundancy work in the modern era too. These things add up; especially when Kiwis are prone to working stupid hours and now generally have to leave a job and start somewhere else to get a decent boost in income.

A few other flaws with this model is it assumes home buyers are medium income earners. Which seems unlikely as many of them will be younger and not yet on higher incomes. Also it doesn't take into account that most FHBs will be renters and that rents, like house prices have also risen faster than income. So not only do FHBs need to save more for a deposit their disposable income after rent payments is less.

I've done similar calculations in the past for my own interest. The results for the payback periods in the 80's are way off, salary inflation led to rapidly diminishing relative size of mortgages. It was easy to pay off a mortgage within 10 years because after first couple of hard years at the end of that 10 year period the mortgage was in real terms only about 1/2 to 1/3rd of what it was at start, and was only 3-4x average salary to start with rather than 15-20x common now. Net result Boomer had freehold house in 10 years and was then able to move forward with other investments or hobbies, and they had much higher disposible income in last few years. Millenial has freehold house in 25-30 years, with mortgage payments still eating up most of average income even at end due to low inflation. No chance for other investments.

In some ways I agree Foyle. Today your income increases as you gain experience and might have to change jobs for that to be recognized. The worker charge out rates for service industry are stupidly high but customer has little choice

Are you trying to say that is somehow different from the past? that people didn't also get wage/salary rises for experience and higher level skills in the past?

General wage rises are less significant today but not non-existent for instance nurses wage round. I myself found

by changing employer and I could get a big pay jump with other perks (and more responsibility). Hence it improved the income to mortgage calculation, so millenials should not have to suffer paying a mortgage for 25 to 30 years as Foyle states

So what was your point in the previous post exactly?

And what may I ask is your point of being on this website for over Nine friggin years since 2010 .... and you haven't learned a thing.

Lol, somebody got kicked out of the wrong side of bed this morning.

How did you get to be so smart and intelligent, rich and famous. You know everything you are a true genius hahaha

Keep going, you're really making a strong case for your shallow pettiness here.

Coming down to your level then... how about you 'find someone' to play your games with.

Keep digging...

Like night vs day to compare the two eras. The challenges then were ugly, today has different challenges nonetheless. Shopping has changed immensely, Think of doing all of your shopping for everything you need between Monday to Friday 8am and 5pm with ONE evening open late. (Maybe you could race out during work lunch hour to buy something you need or for banking ... dont want to be late back to work). Everything closed after Friday and not open until Monday. No online shopping either and you could not pop down to paknsave /countdown with its low prices and easy shopping whenever you felt like during the weekend. Imagine also that the checkout operator had to learn all of the prices for items and specials and the receipt only printing out a price list with no description to try and check you were not overcharged. Late night supermarket queues were horrendous. Challenging times in 1970s New Zealand.

Rubbish. My in Laws got their deposit for a house by cashing in their child allowance (yes. people got PAID to have children back then) from the government then upskilled by getting paid to do a degree, again from the government. Imagine that happening today.....

It was inconvenient but such a big issue?

We have certainly gained some convenience, but at quite a lot of cost in terms of life balance

A little info to put some things into perspective...

"...buying a house in the 1970s or 1980s, they were cheap relative to incomes, say today’s 20-somethings, allowing you onto the property ladder of untaxed capital gains. “We had no overseas holidays, avocado or regularly replaced cars, and had an apple crate for a dining table for the first three years,” says an older generation...."

"...It is well-established that since the 1970s, the size of the average new house size has surged, even after accounting for garages being internalized into house designs..."

In the 1970s and pre 1970s and into early 80s, one brought a house with no landscaping, no fence, no paths or drive, no carpets, no curtains , no carpet, no dishwasher no insulation, no heat pumps, no 2x glazing, and no garage.

Now add all of these "added value" items up...and put onto the price of a std 1972 98 sq m Universal/ Neil/ home and 610 sq m section and you will be not far off A todays std internal garage brick home.

Interest rates around the 7 to 8% with a 20% deposit

The advantage back then, was being able to get into a home, without all the added value, and still have the time and budget if worked over time @ 1.5 x 1st 3 hrs and 2x wages to put in paths , drives, garages over the next 5 to 7 yrs...Labour only... Then to a little larger home to accommodate the 2.5 children.

It was not harder or easier back then, just different market, different skills, different objectives... and 55 to 70 hr working weeks double income.

All fences (min a wire chain) where required to be added in a time frame of approx 18 months/2yrs

Pssst. Most FHBs now are buying those same 1970s homes, and then installing insulation, replacing 20yo wallpaper and carpets. Not a lot of FHBs are buying new builds. And much of what you are calling "added value" items are now the minimum requirements for a new build, double glazing and insulation, driveway..

Yes, I have posted about this before. It is a generational thing that has gone on since the dawn of time. It's called progress/modern life.

Some things probably are luxuries - do we really need 400sqm houses, multiple cars, and electric/automatic kitchen cupboards. But as you say, much of the stuff is now regulated inclusions.

- Parents say Insulation, computers, phones, etc... were luxuries in their day so we shouldn't need them. (Yet their houses all have them now)

- Grandparents said Fridges, TV's and Cars were luxuries in their day so parents shouldn't have needed them. (Yet their houses all have them now)

- Great-Grandparents said Running water, power, and internal toilets were luxuries, so grandparents shouldn't have needed them. (Yet their houses all have them now)

I can see first man shaking his head. "Back in our day we had no house, no clothes, and no food..."

Also add to that, if your house does not include most of these things, it is not sellable. Try building a house with no garaging, no dishwasher, no place for the TV/connections etc.

It's the same issue as relative poverty. If a child does not have internet and a computer at home, it is very difficult if not almost impossible to complete their school homework requirements to the same standard as their peers and they are seriously disadvantaged in our society, but still better off than the kid in India making bricks.

If I could have plonked down a 5% deposit 9 years ago when I moved to Christchurch, I would have had the mortgage paid by now. Instead, for the last 9 years I've been paying for other peoples investments while struggling to put together a 20% deposit, and because it's taking so long, I no longer qualify for Government help as my income is over the $85000 cap.

Of course, none of this is news. It's been there for everyone to see for at least the last decade, probably longer, but neither National nor Labour are willing to bite the bullet and end the residential property investment gravy train. Just look at that $8 billion infrastructure spending. Very little of it was on building what is needed to support increased housing. Sure, a lot of it is on transport, but that's only to increase the value of the cheap investment properties that are currently too far away for commuting. We've already seen this in the rapid house price growth in the regions surrounding Auckland.

The 20% deposit should never have applied to first home buyers. It achieved the complete opposite of what should have happened. First home buyers should have always been allowed to buy with 10% ( or less?)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.