The latest auction results suggest real estate activity is recovering well from the COVID-19 lockdown, with more properties auctioned last week than the comparable period of last year.

Interest.co.nz monitored 216 auctions in the second week of June (8-14 June), compared to 166 in the previous week and 165 in the second week of June last year.

However while the number of properties coming to auction is continuing to rise sharply, the number of properties selling at auction is rising at a slower pace, which means the percentage of properties sold at auction each week is steadily declining.

In the week from 8-14 June interest.co.nz recorded 97 auction sales which gave an overall sales rate of 45%, down from 49% the previous week and 60% the week before that.

That means the sales rate has almost dropped back to where it was in the second week of June last year when the sales rate was 41%.

However while the sales rate has been declining, the prices achieved on the properties that sell appear to be holding their own.

Where interest.co.nz was able to match selling prices with rating valuations on the properties that sold last week, almost three quarters (73%) sold for more than their rating valuations.

That compares with just 48% that sold for more than their rating valuations in the same week of last year.

Of course it is not known how well prices will stack up on the properties that were passed in, when they are eventually sold, but anecdotal evidence suggests that tough negotiations around price are common between vendors and potential buyers post-auction.

Details of all of the properties offered at the auctions monitored by interest.co.nz and the results achieved, are available on the Residential Auction Results pages.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

84 Comments

"However, the prices achieved on the properties that sell appear to be holding their own."

To the disgust of many

Patience, Grasshopper...

"while the number of properties coming to auction is continuing to rise sharply, the number of properties selling at auction is rising at a slower pace, which means the percentage of properties sold at auction each week is steadily declining."

At some stage, 'motivated' unsold property owners, or their financiers, are likely to panic.

(NB: I'd be the first to applaud a median house price in New Zealand to be $5,000,000 IF the productive efforts of the workers of the country justified such. Today, they don't and are unlikely to in the foreseeable future. So in the absences of productivity inspired wage rises what will we get? More debt and that equates to more risk and eventually, that will come back to haunt us. The only question is - "When, and How Bad is it going to be?")

You may well be right, but you cannot argue with HW who is simply quoting what is, you on the other hand, are speculating on what could be in the future

"What is' is more properties coming to market this very day ( as written above) and less selling.

But you're right “It's tough to make predictions, especially about the future” and that works for all of us - especially so for those whose very financial survival rests on them 'being right' about the mists of future time.

Have you ever been wrong bw ...ever ???

bw is never wrong... He's just right before his time.

No I want to hear it from the horse's mouth so to speak

I was wondering the same about you HW :)

We know Yvill is...

I have called it correctly last year with the property price recovery and this year with the share price recovery. Both times I have taken stick for it. And then when correct I take stick ... lifes not fair

War's hell.

"War's hell."

General Hubhub

... and in your line of work, real lives are at risk, the collateral damage is real ...

Indeed CN.... but so is child poverty, homelessness and hard working folk forced to live in cold, damp overpriced garages, by unscrupulous landlords, who lord their wealth and power over them. So it annoys me when the people who have everything, complain life's not fair....

Its tongue in cheek wake up and get a life. You're an investor yourself right, you're pointing your finger at yourself then

If you want to figure out how the market goes, it's simply just not enough to find out what. You will need find out the why behind what. So simply stating what is happening is not valuable, everyone can read the article and find out that information. You don't need to make a statement second time.

Is it that they're stating the current state of the property price changes and extrapolating that recent "trend" that into the future to develop their property price expectations?

Hi Yvil and Houseworks,

Indeed, there are people here who would welcome a recession in the vain hope that they might be able to buy a house for a song.

Yet again, however, they're in for a disappointment. As economists note, house prices are "sticky-down" in NZ - and typically rise rapidly, post-recession.

Notably, the housing market had a very "soft landing" following the last housing boom, which ended around Oct/Nov 2016.

In the current circumstances - Covid-19 combined with winter - any recession in the housing market might well end up being short and shallow.

For sure, there are some investors who will be able to exploit such circumstances for their own $$$ gain.......

But, alas, the disaffected who come here daily are unlikely to be among them.

TTP

That is a fairly optimistic spin. In the GFC, the QV index fell by 10% nationwide and took 4 years to regain the 2008 highs. This is in nominal terms - prices would have fallen further if you accounted for inflation. We are already in a recession (although it won't be officially confirmed for another 3 months or so), and it is expected to be sharper than that seen in NZ after the GFC.

Always dangerous to make predictions about the future, but I would certainly make sure my portfolio could handle a 20% fall in property prices without breaking sweat.

https://www.interest.co.nz/charts/real-estate/qv-house-price-index

"in the vain hope that they might be able to buy a house"

Are you saying it's a vain hope that normal people (not property investors) might be able to buy their first home? How long do you think such a system would last? The medieval ages lasted for quite a long time, but even a serf had to pay less to his lord (as a portion of their 'income') than the average renter at the moment.

Where will investor demand come from when yields get below 3%? Or 0%?

Edit: Oh, I see, you just edited the sentence I was referring to. Now it means something very different.

Bravo CourtJester.

Great comment. I’d give you two thumbs up if I could.

Tim does sound particularly self-absorbed today. Must be too accustomed to the housing market being subsidised and propped up for his benefit.

No one’s worried. Housing has been eased by cheaper and cheaper money i.e ever decreasing interest rates. As we move to 0 and below money obviously becomes free, future generations will experience an even more extreme ponzi experience as the average house price will be maybe around 8 million but interest rates will be -25%. The system will essentially give houses away to citizens who dutifully take on theoretical debt for a small amount of time, because you can’t taper a Ponzi scheme. Jealous?, envious?, schadenfreude?.

TTP, we all make mistakes, but you should note that you've edited a post. Especially when your editing makes a response below look like they are misrepresenting you.

Yes he did that to me a few times yesterday as well. But not just once, on multiple occasions during the day. The content of the original post would be modified based upon the counter argument.

"The content of the original post would be modified based upon the counter argument."

One way of overcoming that is to copy that portion of their comment that you're responding to and pasting into your own response fully unedited (even if it contains spelling and grammatical errors).

Yes prefer if people would just reply below if they wanted to provide a counter argument. Wonder if TTP does that with his clients when they're not looking.

IO,

Did you see that a property investor in a property investor forum group was asking about Property Brokers in Manawatu?

Isn't it funny to see Karma working? ...

I missed that (unfortunately?)...

.

That's poor form. Not cricket, as they say. In fact, an underarm tactic.

"Not cricket, as they say. In fact, an underarm tactic."

More like, adding fictitious runs to their team's score? ...

Is this behaviour a reflection of the individual's character? In a business contract, would this person change the terms of a contract, after the contract was agreed and signed by both parties? ...

I choose to stay well away ... Every person is free to make their own choice.

"At some stage, 'motivated' unsold property owners, or their financiers, are likely to panic."

The panic has past, and why sell if you have a perfectly good but you feel like a change. Employment pressure is not coming on yet and may not, the IRD records show only 30 thousand from 2.2 million are off employer payrolls. It's a fraction of one percent

The worst GDP in 29 years...and worse to come. Let's call it that IMF 7% p.a. just for an indicator, and you reckon. the panic has passed'? Good luck with that!

As we all know, property prices - in fact, any prices - are set by a marginal number of transactions. It's 'who is transacting' that sets the price, and if only a small number of those 30,000 'have to sell' that's what lenders will use as their yardstick to finance future sales.

By the time most people realise what's happening, it will be too late for any of us who haven't 'got set' yet to do so.

That works in both directions, of course, but if I had the choice of 'being in the property market' now or 20 years ago? I'd chose then by a country mile!

20 years ago was year 2000. Bugs and bumps abounded then too

Btw bw how do you know that any of the 30000 HAVE to sell. The answer is you dont know. And mortgagee stats dont bear out what you've said. Enjoy

30,000 is 1.4%. Hardly a fraction, but it is only the beginning of what is to come, unfortunately.

The panic hasn't even started. Just wait for the end of subsidies...

When do they end CJ??

Yeah nah

We haven’t seen anything yet - when the wage subsidies end along with the mortgage holidays that’s when the rubber hits the road.

I am not surprised to see the prices to be holding their own. But don't be fooled by the prices, the more important indicator is the sales rate, as the sales rate continue to decline, auction number or stock continue to rise. The prices will fall eventually. When supply > demand, the price goes down. Let's see how it unfolds...

This is sheer madness buying like crazy in this uncertain times. Surely there will be a bit of sense coming into the prices

Yeah right ...about as safe as the Stock Market .

I would suggest that the increasing number of houses for sale could be the start of the stressed seller syndrome .

Redundancy does that !

I have a question: are the rating valuations usually updated before auctions, or are the rating valuations being referred to the last set that was done (i.e. the 2017 valuation).

Last set of valuations (2017 for Auckland)

Thanks Yvil

Just a remark that this was in many cases bubble peak prices.

I think they're due to be renewed this year in Auckland. It's a 3 year cycle. Will be interesting to watch when those come out ...

It's a Mexican stand-off on price!

One factor that strikes me: as time goes buy, an increasing number of sellers are those who purchased at 2016-2019 peaks. They paid a lot, many will hold a very large mortgage having purchased at peak, and it will be painful to sell for less than they paid. They'll also have less equity, and will on average be younger (probably more susceptible to unemployment). So they'll *need* to sell more, but also be more desperate on price than someone who bought in 2010 and can feel very comfortable about their profit even if they sell below CV. It all suggests a more 'adversarial' market.

8 Auctions CHCH right now, 7 passed in.

Auctioneer: Silence! Jesus!

1 sold, I wondered if it's TM2...

'Passed in' cannot go on forever. September is going to start a selloff frenzy. If you need to sell, do it now before its too late. Not 'by negotiation' or 'auction', put a price on it below 2017 CV and you may stand a small chance. If you don't you will be lucky to get 2008 CV in a year or two.

Looks like the effect of vendors fearing getting stuck with unprofitable properties with rents going down plus some auctions that could not happen earlier before of the lockdown. Either case more properties in the market than buyers willing to purchase them.

Meanwhile, in the main stream media, a story focusing on areas with the highest property price gains ...

https://i.stuff.co.nz/life-style/homed/real-estate/300037191/heres-wher…

Interesting (irony mode ON) I was not expecting the REINZ to be involved in propaganda like this.

"I was not expecting the REINZ to be involved in propaganda like this."

REINZ is an industry lobby and marketing group. Set up to look after and promote the interests of that industry ...

Meanwhile, a comment on the Queenstown property market on a property investor forum:

"Not looking good for Central Otago/Qtn lakes district property capital wise ...employment IMHO

latest numbers some 1200 properties on the market + record high rental properties for this time of year COVID has really kicked it in the guts ..

population est. 65k for the area

still have some of the Highest property prices in NZ ... Buyers market ....so many tradies in the area + Tourism bleak looking future.I just don't see property construction pulling the area out of a major depression for many years.... more than enough stock

I knew we should have sold long ago !!"

This is what a widely followed & high profile economist (previously employed by the BNZ), was saying in February 2020 (4 months ago) - no reservations or warnings whatsoever of any property price risks. Any owner occupier who acted on the economist's property price forecasts and purchased in January, February this year in Queenstown, on an 80% LVR mortgage could face the risk of being in negative equity (and a potential 100% or higher unrealised loss in their equity, which could become a realised loss if the purchaser is forced to sell due to closure of business, unemployment, etc).

Meanwhile, the economist just changes his forecast on 6 April 2020 for property prices to fall and goes on to tell his audience how he was "right". What happened to the collateral damage / road kill that the economist just left behind? - the purchaser's entire financial future may now be ruined, lives changed forever, future financial security of the family now in entire doubt, potentially leading to mental health issues ..] - this is the reason that I have continued to highlight the property price risk warnings to potential owner occupier buyers, so that they can make a fully informed purchase decision. (contrary to the property price bulls claims that the property price bear's motivation for speaking up is due to envy, or personal desire to purchase a property at a knock down price, or being "anti-property").

Hard working potential owner occupier buyers in New Zealand have been denied an honest discussion of property price risks that put their entire financial futures at risk (due to the huge vested financial self interests). These are real people, real lives that are potentially forever affected.

20 February 2020:

A reader asked for my comments regarding a report released last week by a research foundation set up by ex-Prime Minister Helen Clark looking at housing affordability. So, I had a quick look just in case it offered something with a realistic chance of being introduced to the effect that prospects for future house price gains would be reduced. It did not.

Do I think price growth will continue? Yes. Interest rate rises lie a long way down the track. Our population continues to get a 0.9% boost per annum from net migration flows. Wages growth has accelerated. Construction growth is strong but will be retarded by shortages of labour and also shortages soon of some materials because of factory shutdowns and supply chain disruptions associated with China’s latest virus.

EDIT: name of person edited out (to avoid any potential claim of defamation).

Economists, never factor in the 'what if' factor - at least in their public communication. What if we have a 1930's style depression, starting in April that lasts for 2 years. 'Well everyone should be aware that NZ has some of the most expensive houses in the world based on any historic or current measurement of housing affordability, and we are very reliant on tourism and migration, if something were to remove those factors from our proejctions, well any outcome is on the cards'.

When I watched one of the presentations, of this particular economist, there were no reservations, caveats whatsoever ...

The more behaviour that can be observed by those with vested financial interests, with the current situation in the property market in NZ of elevated property price risks, if property prices drop substantially, some might ask the same question that was asked by the Queen about the GFC in 2008 ..

[During a briefing by academics at the London School of Economics on the turmoil on the international markets the Queen asked: "Why did nobody notice it?"]

https://www.telegraph.co.uk/news/uknews/theroyalfamily/3386353/The-Quee…

Not to bring up Shiller again but if you understand his insights into behavioural finance/economics (which you clearly do), you realise that people like to operate in herds - it would be dangerous for an economist to publicly say what they really think for many reasons. So they're all giving forecasts and generally agreeing with each other. I think its similar with fund managers and stock selection - they buy what the other funds are buying - it protects one another, until it doesn't any longer...

Also, a large contributory factor is the mainstream media not allowing a different perspective that property prices risks are elevated and that property prices could fall. The lack of public discussion of these possible risks in the mainstream media, and the marketing efforts of the huge vested interests drowned out the few warnings that were made. I recall stories of commenters who were posting property price warnings on the comments section on mainstream media websites having those comments removed by the editor of the website, and they were subsequently banned from making further comments. So people raising the potential possibility of property prices falling were effectively silenced and unable to have that discussion.

The huge vested interests used negative labels "doom and gloom" in the mainstream media to describe and dismiss those that gave warnings, and to ridicule those that had a different perspective, especially since the subsequent property price action proved otherwise. Property mentors at property investor conferences dismissed the opposing viewpoints as those motivated by envy or were labeled as "anti-property". There are no marketing dollars or vested financial interest in highlighting property price risks.

Also I'm reminded of the public dismissal and loss of credibility that a particular journalist received in 2009 during the GFC, as their forecasts of significant property price falls did not subsequently eventuate due to the subsequent mitigating actions of the RBNZ and the government stimulus packages. (The property price risks before the mitigating actions were elevated). Few people would want to do that publicly and be subject to subsequent constant public ridicule (which may be the reason that those gave warnings, didn't repeat their message frequently, despite their better informed industry viewpoints)

As a result, property prices increased significantly, and many property buyers have since believed that there was little or no risk to purchasing residential property and willing to take on large amounts of debt, and high debt service ratios.

Let's take a look at the media narrative (spin) of the recent May 2020 median house price changes as calculated by REINZ - and the audience reach of that message to determine the main message that most of the public are receiving about property prices in New Zealand.

A) positive spin - focus on 6.9% yoy increase in property prices, no mention of property prices falling MoM

i) TVNZ - (mainstream media, widest audience reach) - https://www.tvnz.co.nz/one-news/new-zealand/property-sales-drop-covid-1…

"In terms of price, though, national median house prices increased by 6.9 per cent last month to $620,000.

In Auckland, median house prices increased by 7.1 per cent to $910,000 compared to the same time last year. It is the third highest price on record."

ii) NZ Herald - (mainstream media, broad reach) - https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

"Yet despite the dramatic slowdown in sales volumes, New Zealand's median sales price hit $620,000 in May, up 6.9 per cent on the $580,000 median sales price in May 2018.

Auckland's median sales price jumped 7.1 per cent to $910,000 from $850,000 in the same month last year."

iii) OneRoof (mainstream media, broad reach - property marketing website) - https://www.oneroof.co.nz/news/plenty-of-house-buyers-but-not-enough-se…

"Median house prices across New Zealand increased by 6.9 per cent in May to $620,000, up from $580,000 in May last year."

Add to the above :

a) the media interviews that Bindi Norwell from REINZ was giving the numerous media outlets.

b) that same message was being delivered by the thousands of real estate agents around the country

c) that same message being delivered by property tutors to their audiences

d) that same message being shares by property investors in property investor forums

B) balanced reporting - mentions both 6.9% yoy increase in property prices, and property prices falling 8.8% MoM

i) Stuff.co.nz - (mainstream media, broad reach) - https://www.stuff.co.nz/life-style/homed/300034780/days-to-sell-hits-lo…

"The national median house price lifted 6.9 per cent in May compared to the year before, to $620,000.

In Auckland, median house prices increased by 7.1 per cent to $910,000 up from $850,000 at the same time last year – the third-highest price on record. Outside Auckland, prices were up 9.4 per cent.

However, median prices compared to April were quite mixed. The country as a whole reported an 8.8 per cent drop month-on-month."

ii) interest.co.nz - (niche readership) - https://www.interest.co.nz/property/105499/reinz-national-median-sellin…

"Prices were also weaker, with the national median selling price dropping from $680,000 in April to $620,000 in May (-8.8%), although that was still up by 6.9% compared to May last year."

C) negative reporting - mentions only property prices falling 8.8% MoM

None noted

So in conclusion, this is an anecdotal example of how the message of property prices rising 6.6% yoy was received by the public and drowned out the message of property prices falling 8.8% month on month.

Here is a property purchased in December 2019 for $1,730,000 located in Queenstown. The July 2017 CV was $970,000, and estimated market value of $1,050,000 before the purchase in December 2019.

Will be interesting to see what happens to the property price of this address in the next few years if the property remains substantially unchanged. (i.e no property development or significant improvements to the property). Will the property owner be able to hold on in the current downturn?

https://homes.co.nz/address/queenstown/queenstown/107-frankton-road/XL7…

Don't you understand the meaning of "irony"?

My apologies to you, for my mis-interpretation - I interpreted the irony to be applied only to the word "Interesting". And not to the second sentence.

I frequently find anything that is intended to be irony, or sarcasm tends to get lost in translation in written form. It may in the writers intent and mind, however it may not get communicated on paper and can be prone to misinterpretation by readers who may be in an entirely different headspace when they read the comment.

From Australia - who we don't resemble at all. Their GDP fell 0.3% for the first quarter after all; ours was 5 times worse....

In May, Australia's largest bank warned house prices could fall 32 per cent in a "prolonged downturn."

The Commonwealth Bank, which holds more Australian mortgages than any other, warned that under a "worst-case" scenario, house prices would fall by almost a third from their March 2020 peak over the next three years.Reserve Bank economists considered urging the Federal Government to shut down the real estate industry, "pausing" sales of established homes to avoid perceptions of a coronavirus-inspired housing market crash.

Key points:

RBA documents obtained under FOI warn of a sharp fall in housing prices.

In April, an RBA economist wrote to colleagues, calling for a housing market halt as happens in stock market trading during emergencies

Documents from inside Australia's central bank, including many marked "highly restricted", also suggest house prices could slump up to 15 per cent.The internal reports contradict a much rosier public view the Reserve Bank of Australia has been displaying about the billions of dollars and millions of jobs tied up in housing, construction and real estate.

https://www.abc.net.au/news/2020-06-18/reserve-bank-considered-asking-f…

We are diffrunt!!!

I hear this mantra often repeated. NZ is not "Unique" or immune to the fundamentals of economics. High unemployment will occur. The government cannot bail everyone out indefinitely. When greed turns to fear in the property market, owners of property under stress will sell, and they will take a lower price compared to their inflated expectations of always asking high percentages over the CV. Lower incomes will translate to mortgage stress. The big Hi Def TV's, the SUV's, the dining out will all but disappear. Smug middle class property owners will have to take a haircut and experience how the lower income wage earners live. About time. Multiples of 7 or 8 of average income for what I would describe as a shed in Oz. Get real. Strap yourselves in for the ride.

When the aussie market goes tits up (see https://www.abc.net.au/news/2020-06-18/reserve-bank-considered-asking-f…) NZ FHB will leave NZ to pick up a reasonable priced home over the ditch, which will in turn trigger more of a down turn here.

Most likely if the Australian market tanks, we go with them. Same parent banks, probably same fear around lending. Most of the market is psychological frenzy. The fear will spread to our market as well.

My concern is that the banks will become very tight on lending when this happens.

My wife and I (nurse/teacher) have been pre-approved currently. Our job security is high. But your deposit is low (13%). What if we leave it too long and the banks don't want to lend to us anymore? It was already quite a long process for us.

Do we wait until the end of the year to buy? Or buy around September/Oct before our pre-approval ends?

So, a nurse and a teacher find themselves in a casino one day, with an accountant and a truck driver and everybody else in NZ...

If the housing market gets bad, its going to be bad for years...not months. So if your can't delay you desire to purchase a home by years then perhaps you should purchase and just enjoy the benefits that come from home ownership. But if you know that you will beat yourself up badly if the market falls and you resent being stuck in negative equity (and can't move until prices recover) then think carefully. Have you ever purchased stocks and lost money on them? Being stuck in negative equity will be that type of pain but much higher. Especially if you see other younger people buying on the same street a few years after you for hundreds of thousands of dollars less.

https://mblogthumb-phinf.pstatic.net/20160114_206/man1120_1452767390401…

{kind=link}

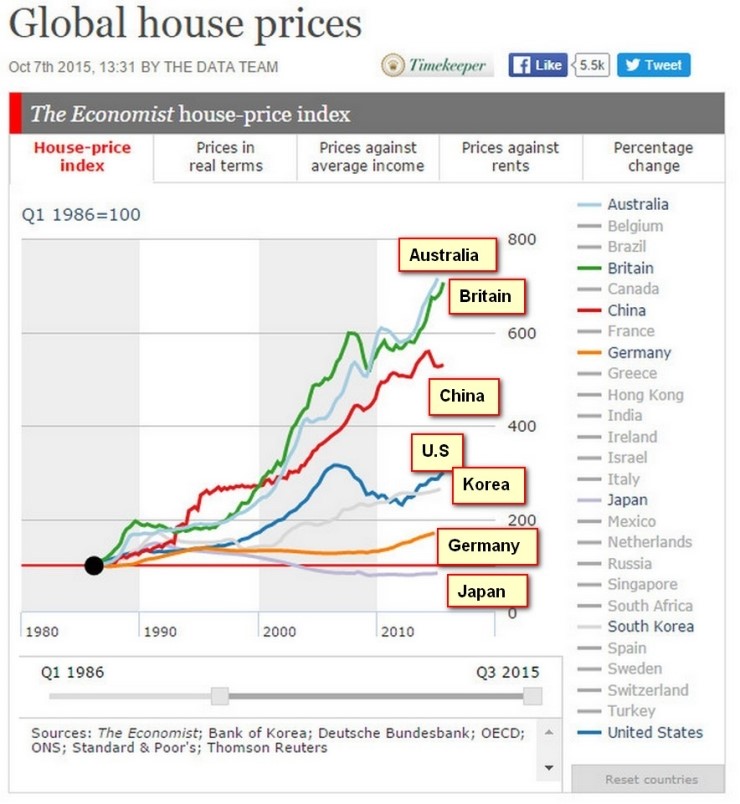

We're up there with Australia in these charts. Note that prices fell for decades in Japan. Ireland and the US bubbles took a number of years to bottom out, Spain took a lot longer again (like 5-6 years).

https://gpg-production-cdn.s3.eu-west-2.amazonaws.com/assets/Spain-1/sp…

https://upload.wikimedia.org/wikipedia/commons/e/ed/Vivienda_n_jun2009…

{kind=link}

{kind=link}

To be honest its totally shit that younger people have to make these types of decisions and in some respects could be stuffed if they do and stuffed if they don't - hence my resentment to central bank policies and governments supporting policies that have made this property bubble so big and the situation/decision making so difficult for FHB's.

Here are some numbers for you to think about. Given the lower deposit, then the larger impact of price changes on your equity value. (The numbers below are based on a 13% deposit)

Choose your scenario and act accordingly.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential loss of their savings invested as the initial deposit for purchase of the house or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of financial impact of leverage on equity, assuming an 87% LVR for owner occupier (13% equity deposit), for a recent $1,000,000 property purchase, $130,000 initial deposit, mortgage $870,000. (simple round numbers used for illustration purposes)

A) Scenario - property price rise:

1) property price rises 5% to $1,050,000, mortgage $870,000, equity $180,000, so 38% gain in equity value from $130,000.

2) property price rises 10% to $1,100,000, mortgage $870,000, equity $230,000, so 77% gain in equity value from $130,000.

3) property price rises 15% to $1,150,000, mortgage $870,000, equity $280,000, so 115% gain in equity value from $130,000.

4) property price rises 20% to $1,200,000, mortgage $870,000, equity $330,000, so 154% gain in equity value from $130,000.

5) property price rises 25% to $1,250,000, mortgage $870,000, equity $380,000, so 192% gain in equity value from $130,000.

6) property price rises 30% to $1,300,000, mortgage $870,000, equity $430,000, so 231% gain in equity value from $130,000.

7) property price rises 35% to $1,350,000, mortgage $870,000, equity $480,000, so 269% gain in equity value from $130,000.

8) property price rises 40% to $1,400,000, mortgage $870,000, equity $530,000, so 308% gain in equity value from $130,000.

9) property price rises 50% to $1,500,000, mortgage $870,000, equity $630,000, so 385% gain in equity value from $130,000.

10) property price rises 100% to $2,000,000, mortgage $870,000, equity $1,130,000, so 769% gain in equity value from $130,000. (i.e if they believe that the property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any potential significant reduction in household income).

B) Scenario - property price falls:

1) property price falls 5% to $950,000, mortgage $870,000, equity $80,000, so 38% loss in equity value from $130,000.

2) property price falls 10% to $900,000, mortgage $870,000, equity $30,000, so 77% loss in equity value from $130,000.

3) property price falls 15% to $850,000, mortgage $870,000, equity NEGATIVE $20,000, so 115% loss in equity value from $130,000.

4) property price falls 20% to $800,000, mortgage $870,000, equity is NEGATIVE $70,000, so 154% loss in equity value from $130,000.

5) property price falls 25% to $750,000, mortgage $870,000, equity is NEGATIVE $120,000, so 192% loss in equity value from $130,000.

6) property price falls 30% to $700,000, mortgage $870,000, equity is NEGATIVE $170,000, so 231% loss in equity value from $130,000.

7) property price falls 35% to $650,000, mortgage $870,000, equity is NEGATIVE $220,000, so 269% loss in equity value from $200,000.

8) property price falls 40% to $600,000, mortgage $870,000, equity is NEGATIVE $270,000, so 308% loss in equity value from $130,000.

9) property price falls 45% to $550,000, mortgage $870,000, equity is NEGATIVE $320,000, so 346% loss in equity value from $130,000.

10) property price falls 50% to $500,000, mortgage $870,000, equity is NEGATIVE $370,000, so 385% loss in equity value from $130,000.

Something additional for you to consider.

FYI, the REINZ house median price dropped 8.8% last month - https://www.interest.co.nz/property/105499/reinz-national-median-sellin…

How would that have impacted that $1,000,000 purchase above using an 87% LVR mortgage (13% deposit)?

Using that same purchase price of $1,000,000, 13% deposit of $130,000, and 87% mortgage of $870,000

1) property price falls 8.8% to $911,765, mortgage $870,000, equity $41,765, so 68% LOSS in equity value from $130,000. - IN ONE MONTH.

If that purchase was made at the lower purchase price of $911,765, and same $130,000 deposit, then the mortgage would be $781,765 (10% less than above). Also

a) you could have lower mortgage payments for 30 years (due to the lower size of the mortgage) OR

b) you could make the same mortgage payments as above, and could result in paying your mortgage off in a shorter time period.

Overall, it would result in lower total interest payments over the period of the mortgage.

'The number of residential auctions is rising at a faster pace than auction sales, which means the auction sales rate is declining'

It indicates: Number of House for sell going up and number of sale reducing.

Reason number of people selling now are as expecting to get situation worse in future so earlier the better. Also good houses are still going at decent/premium so selling now is better than waiting.

Selling by Auction, as it helps RE Agent from the hassle of convincing vendor of the price fall if is not successful in Auction also more chances of RE Agents getting more commission if sold through auction.

Sales has already started declining and should follow by fall in house price in future.

Agree that good houses are still selling at decent / premium and 72% houses that sold went above RV is an indication of the same and it is this houses/prices though few are still holding the price but for how long so best advise for anyone who has to sell should sell now.

Whatever anyone or so called experts may say but repercussion of Coronavirus cannot be avoided though has been diluted/delayed for now through easy and free distribution of money but just like lockdown that ended or has been loosened in many countries though Panedemic is still spreading in those countries - similarly printing of money will have to be controlled/stopped despite .........My understanding is, it should be by September/October being election time.

It is 73% of houses selling above RV for those that cleared.

But overall if sale rate is only 41% then 0.73*0.41 = 30% of houses available on auction sold for above RV. One of these days I will check to see if there is any trend there.

I am dedicating this song to all property investors (or speculators).. You know who you are..

https://www.youtube.com/watch?v=PGNiXGX2nLU

When a product lacks, there's price rise.

When a product is in surplus, buyers have more options and sellers more competitors,

hence they have to drop price to sell.

I wouldn't be surprised to see an average price drop of 10% (compared to March 2020) in the next 2 months.

But.. that's only my idea, without reading any marketing-related articles sponsored by REINZ

"When a product lacks, there's price rise."

The property market promoters like to remind the general public that there is currently an underlying housing shortage ...

That underlying housing shortage argument is being repeated by many property investors in their comments on property investor group forums ...

Yes while tens of thousands of houses (in Auckland alone) sit empty - as a tax free store of wealth.

Is access to the bank of mum and dad is increasing wealth inequality in New Zealand?

What happens to those who don't have access to the bank of mum and dad?

"Mortgage brokers report around 70 per cent of first home applicants have some sort of help from what is colloquially known as the Bank of Mum and Dad (or BoMaD). Banks report a slightly lower percentage; anecdotally around 60 per cent."

https://www.oneroof.co.nz/news/pros-and-cons-of-borrowing-from-the-bank…

Interesting stat! The Ponzi scheme extending through the generations.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.