New homes continue to be completed in record numbers in Auckland, despite the recent COVID-19 lockdown restrictions.

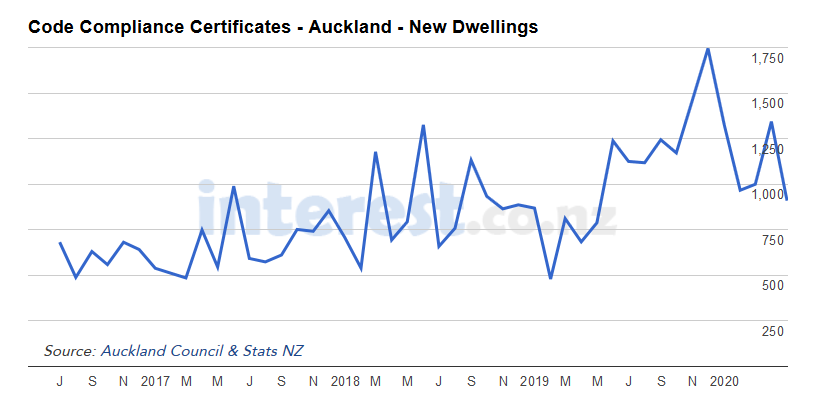

The latest figures from Auckland Council show that 1344 Code Compliance Certificates (CCCs) were issued for new dwellings in March.

That was a record for the month of March since the council's published CCC records began in 2013, and almost double the 678 CCCs issued in March 2019. That's even though the most severe COVID-19 lockdown restrictions took effect towards the end of that month.

However there was a dip down to 910 CCCs issued in April as the level 4 restrictions began to bite in earnest, but that was still up by 15% on April last year and was also a record for the month of April.

Code Compliance Certificates are issued when a building is completed and deemed fit for occupation.

The number of new homes being completed in Auckland each year has more than trebled in the last six years, rising from 4027 in the 12 months to March 2014 to 14,528 in the 12 months to March this year.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

41 Comments

Hmmmm, this ain’t gonna end well...

Council keeps approving crap little box townhouses. This will not end well for those buying. Meanwhile no upgrades to our infrastructure. More coverage, more catchments, flooding etc happening more often as a result. Council has no sustainable plans but keep approving to get more rates etc. Banks have to stop lending on these shoebox developments

I've come to the conclusion it doesn't matter at all... these tend to be sold to investors for rental rather than owner occupied, depending on the quality / price point. Provided interest rates don't go up (and let's face it, how can they without stuffing the economy?) they'll provide the owner with a nice wee yield compared to a TD.

the rush to gold... hem... sell

Good news; the market apparently works and can meet demand for housing. Govt should stick to it's knitting and stay out of it.

Great comedy.

A bit dated but probably as true today as when it was written ( as the World tried to recover from an unforeseen disaster - the GFC in that case, and today we have?....)

Neo-liberalism and the failure of housing markets to deliver adequate housing.

The driving forces of globalisation and neo-liberalism over the last 30 years saw a turnaround in housing policies, with the withdrawal of national governments from direct support of the housing sector and a move towards greater reliance on the market to address housing provision. Features of this era were the rapid growth of housing finance markets, deregulation of markets and the associated banking systems, privatisation of the existing social housing stock, reduced investment in new provision and removals of rent control. It is now widely recognised that this market-focused approach has failed to deliver affordable housing for all.

http://www.housingeurope.eu/event-178/where-is-housing-in-the-future-so…

That nails it. Trickle down my ass!

Only about 10 years too late...record consents at a time when house prices are heading for a correction? Yeah what could possibly go wrong? That’s what happens with boom and bust property cycles

Ireland - massive over build. We have a housing shortage...build, build, build! The young people leave while the market crashes...oh shit, we've got an over supply! Prices fall 60% in Dublin.

It was fun and games until someone decided to build more houses...

Residential buildings are built for coming migrants.

Which coming migrants?

The Red Army?

It would be NZ's fortune if that were the case.

Would the comentator care to elaborate as to exactly what he proposes that the benefits are,in having "red army " boots marching on this sovereign soil? Our patience wears thin.

if you think only a bit bigger and longer, in a scale of the Earth, the solar system, or the milky way or the universe, resources will always belong to the most advanced because they get used most efficiently and sustainablly and generates maximum values.

China, the most "sustainablly"? LOL, Friday night Comedy on a monday.

A bit of hacking does help the advancement

More CCC's issued in April this year when most of NZ was shut than in any month of April prior, that's incredible, there's a lag between applying for a CCC and obtaining it but still...

I am not sure I would read much into this Yvil.

If new dwellings were very close to completion just before lockdown, there's little poing in not getting COC.

The same will apply for data from May to August.

We are unlikely to see drops till August / September.

Spec builders can only hope that the hundreds of people emerging from Quarantine can afford to rent or buy one of these nice new houses. Travel stats for last 7 days 15-21 June.

https://www.stats.govt.nz/experimental/covid-19-data-portal

NZ Passport Holders Arriving 1459 Leaving 833. Net Gain 626

Other Passport Holders Arriving 1006 Leaving 3347 Net Loss 2341

Total Net Loss of 1715.

Interesting to see how these numbers play out over the next month. Will be an indication of which way the property market will be likely to go.

Let me get this straight - you’re saying that there’s more people leaving NZ than coming here, that means less people in NZ needing homes (own or rent). Underdemand.

The article says consents are still higher than last year, so there’s more houses available. Oversupply.

Then we also have to factor in the mass layoffs and business closures come September / October when the wage subisidies and mortgage “holidays” end, which is conveniently around election time.

I think house prices are pointing one way - down.

(ToThePoint will say up)

There are a number of repatriation flights happening at the moment. The airforce started flying 1000 seasonal workers back to Vanuatu last week, and we are about half way though a series of 8 repatriation flights between India and NZ (about 2000 people going back to India and about the same number leaving India for NZ). The Vanuatua people don't rent or buy houses in NZ and suspect the Indians going back were visitors or temp migrants who don't buy houses either and probably were staying in shared accommodation. It might be quite a while before we have any idea of the NZ population going forward.

I was surprised at the number of non NZ passport holders coming across the border in the last week, Jacinda has been assuring us that we are paying quarantine costs for "Kiwis coming home" but that seems to be a bit of a lie.

The next quarterly employment stats are due for release 5 August - unemployment is likely to swamp these up/down immigration numbers.

Would be good if all the worldly, educated kiwi folk wind up coming back to live in NZ. Can't hurt to have more processing power in this country, by golly we need it at the moment.

But in all seriousness who will be buying all these new homes?

I will if the price realigns with, say, 6 * median income instead of 9 *. Along with good build quality of course. And yes, first home buyer, in Auckland.

OK - lets see where a house price of 6 x median household income sits in the context of this global house affordability survey thing:

http://www.demographia.com/dhi.pdf

Right...oh here it is right on page 1:

Affordable = 3.0 & Under

Moderately = Unaffordable 3.1 to 4.0

Seriously Unaffordable = 4.1 to 5.0

Severely Unaffordable = 5.1 & Over

OK, so a drop from 9 to 6 takes us from "Severely Unaffordable" to, oh dear, "Severely Unaffordable" (!?).

Sigh.

Yeah I know....it's all the hope I can cling onto. Moderately unaffordable would be bliss!

That would make you feel like a boomer in the tough old days of doing it all on one's own two feet thanks to affordable housing from massive state and private efforts following the war.

To be fair, those historical affordability ratios are all based off much higher interest rates. We are not going to see 7% mortgage rates again in our lifetimes. The world is turning Japanese and we are heading for decades of low or zero interest rates.

I'm not saying houses are a buy. Far from it, I think we heading for 20% to 30% declines over the coming 2 years. But we are never getting back to 3.0 ratio for household income vs house price.

Yes, fair point. What do you think of a possible scenario where creditors (eg Super Funds) get spooked by a global wave of defaults and either want their money back or a rate that reflects the risk. Would sovereign money printing to "support the market" be able to carry on to cover that without triggering hyper inflation that would pressure rates up anyway?

Good build quality? Probably. Usable as a house? Depends. Is a house in West Auckland, with no access to rapid transit, really that usable if it has one car park or less?

Kiwis, for shedloads of Aussie money....

It's about now that Jacinda will start telling us that she & the CoL govt has solved the housing crisis.

The point of your comment is subtle sarcasm pointing to the fact that the COL govt has done nothing to help the housing crisis. This is true. Given however the other mob encouraged and accelerated said crisis over 9 years while swearing black and blue that there was no housing crisis and that the market would provide means that there is a worse alternative and we are well and truly up the creek.

Its going to be very interesting to see where the construction sector heads over the next 12 months. Am currently reaching the end of a very interupted redevelopment and watching all the subcontractors we deal with, I feel sorry for them, knowing what I saw post gfc. Conversely, if it helps them to actually answer the phone when I call them, perhaps its not such a bad thing to have a little recessionary fear nipping at your heels? We will see...

Please have a look at what Wolf column is saying re USA.

I feel NZ will follow this pattern, but of course not as severe.

As we have much better situation re Covid and unemployment, main effect in NZ will be unlikely to show til August and be moderate price drops and BIG sales drophttps://outlook.live.com/mail/0/inbox/id/AQQkADAwATM0MDAAMS1kNWRmLTIzMD…

Really, we all need to look at more detail: especially of WHAT is being consented and where.

A lot of it is units for retirees, not family houses.

Another crucial variable is demand v supply and for what type of place.

Most commentators continue to hold that there is a shortage of housing/homes in NZ and esp in Auckland.

I disagree and the amount of stock being issued not the market whilst demand (real, buyers) is dropping, is to me a classic sign that prices will fall. Wait til the wage subsidy starts dropping and people want to sell but buyers are insufficient. Then the "conversation" with RE will take place and asking prices and selling prices will drop.

With an aging population, units for retirees are good across the board, because those retirees will most likely be vacating 3, 4 or even 5 bedroom houses oftentimes. And putting them on the market. That's exactly what I was looking at on the weekend. A 3 bedroom in Auckland South/Central with one owner who'd lived in the house from when it was new 50 years ago and moving into retirement facilities.

Well, that owner may have paid 20k? for the house 50 years ago. Now the agent is telling them it's worth 800k and they have made their plans accordingly. But after a while on the market with no bites. Will they be conditioned to drop the price so they can move on with their lives. Heaven forbid they wait too long and it is left to their heirs and successors. They are often less keen to put off their windfall spending until the market recovers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.