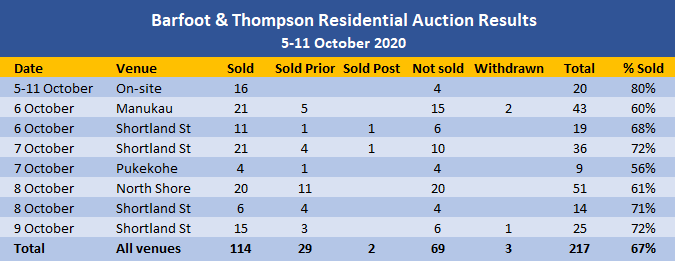

It was another cracker week in Barfoot & Thompson's auction rooms with the real estate agency auctioning a double century of homes and achieving sales on two thirds of them.

A total of 217 residential properties passed through Barfoot & Thompson's auction rooms last week (5-11 October), slightly up on the 207 properties auctioned the previous week.

Sales were achieved on 145 of those, giving an overall sales rate of 67%, also slightly up on the 62% sales rate the previous week.

At the individual auctions the sales rates ranged from 56% at the Pukekohe auction to 80% at the on-site auctions (see the table below for the full breakdown).

A high number of sales being agreed between vendors and buyers prior to the properties going under the hammer continues to be a significant feature of the market, indicating strong buyer demand.

The latest results suggest auction activity is maintaining the full head of steam that has been apparent for the last few weeks and is showing no sign of slowing down.

Details of the individual properties offered and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

21 Comments

Continuing saga of buying a rental unit/townhouse in central Auckland.

2 bed duplex Onehunga - CV $620k, agent indications high $600s, sold $825k

Only benefit? of trip to Auckland was Wendys for lunch.

Something I learnt recently - never listen to an agent's indications. They are only concerned with getting another bidder so understate. Property one - agent extremely reluctant to give any price indication. Advised budget of 1 million and they said it would be worth a look. Sold for 1.35 million after pre auction offer of 1.25. Property two 'feedback is in the 900s'. Spent $900 on builder report and lawyer. Bids up to 1.07 million, didn't meet reserve then got negotiated up a bit more to sell.

This is madness. As a FHB it would seem you’re damned if you do and damned if you don’t. Don’t know what to do other than jump in and be out of our misery.

That and also vote for parties who will not shy away from a wealth tax.

I'm in the same boat, it's been going this way since at least this time last year, gradually getting worse. We went to our first auction in Sept 2019, 3 bed villa in Otahuhu. CV 740, agent says high 700s, we were set to go to 839. Sold for 935.... Needed a new roof too! I think your right get in and hope it doesn't tank.

Same. We can't be doing with yet another year of renting. Unfortunately moaning about unfair it all is has gotten us no where, so we're going hard on a tender and thinking long term.

Great informed feedback from someone on the short end of the stick.

Tough call.

Indications while Covid an issue is downside for interest rates upside for prices.

Whatever happens the critical thing is ability to service the mortgage and as one is in long term short term fluctuations irrelevant.

Post Covid I’m picking relatively flat market with some possibility of some minor correction but long term that is irrelevant.

FHB need to keep in mind that it is firstly about a home.

You're correct, but when in less than 12 months. We all can surely seen the massive distortions caused by Govt & RBNZ decisions. With that in minds, for any rational professionals.. then it's no longer about a home BUT also about a simple equations of 'serviceability of the debt'. Across the ditch that factors clearly differ, remember world is not just about NZ matey.

I decided not to buy, what you experience now is normally called "real estate/ monetary policy terror" , "FOMO" , I am not dealing in any shape of or form with terrorists, even that will probably mean I'll have to leave this city/country

Likewise; Attended auctions before lock-down and wore the associated costs (building reports, LIM, valuations etc). Had both my buying agent and the vendors agent very actively encouraging me turn up and bid as I was in "an extremely good position".

In two auctions my stated top dollar turned out to be miles off the reserve and well short of the final (over RV) price. Again, this was for family homes that needed a lot of work (re-roofing, bathrooms, kitchens, EQC repairs etc). Buying Agent shrugged her shoulders: it was all about "getting bodies in the room"

My gut feeling is that I should go all-in and buy whatever I can, using all my KS and what's left of the marital equity. It will be going into a trust for the kids anyway, so when I die (still working full-time) they can pay off the balance of the mortgage...... As long as Mortgage interest rates don't climb much in the next 30yrs...

Is this what they mean by having "initiative and commitment"?

Really sad to hear comment from Jacin, that the only way is to 'increase supply' she & Lab clearly shy away to mention about their wages subsidy decisions, subsidy to beef up corporate profits, shy away for Banks deferral facts, shy away from RBNZ independent madness of OCR, QE/LSAP, removing LVR, FLP - The multiple input from Mr. Bloomfield that can cause certain 'healthcare conditions' clearly is NOT a lesson for her.. the only way is to 'increase supply' tells a lot about her bias view on this NZ housing... 'everything else' Off the table.

I bet they are all some kinda Kiwis.

No foreign buyers, house price still soar?

Can't deny these though: LVR, OCR, Subsidy, QE/LSAP & FLP - be honest, because Mr. Orr does and mentioned the correlations buddy.

The comments in this thread will fuel the house buying mania. The property prices must fall crowd have cried wolf for too long now. Things feel weird though.

I disagree. On a bigger picture, much of the world economy is moving to the insolvency stage. NZ is not immune. No point paying silly amounts of money for houses just for the sake of it when the there is no business case to support it.

Pricing assets over the past few decades have become impossible for the average person who is using financial or economic theories thought in business schools. The strange role central banks play in money supply and the strange role governments play in uplifting "aggregated demand" create complex sources of demand that are so very hard to predict.

So coming up with a business case for anything is very hard. People have been saying since 2000s that there is no business case for house prices to further inflate, yet here we are.

People on this website had business cases for falling house prices by way before now. I was one of these people. Things turned up quite differently, as it is only in hindsight that you can know for sure how factors may end up affecting prices.

All this off course does not mean that I know what is going to happen tomorrow and all the house price increases over the past 30 years may suddenly be replaced by falling or even collapsing house prices.

The level of uncertainty associated with prices makes any meaningful prediction nigh impossible. There is an element of gamble. It may go up further, it may go down and burn you.

I would personally recommend people to focus more on their own financial situation and what price they can reasonably able to pay for something that they find reasonably and realistically acceptable. Their future income prospect, their job security, their expected cost and quality of housing if renting, the positives and negatives of buying a house on their lives and happiness, their opportunity cost if they would use their saving now and future saving (i.e. principle not repaid on a mortgage) on something other than housing, etc than be solely focused on something so very difficult to predict as house prices in 1 year, 5 years and 25 years,.

Pricing assets over the past few decades have become impossible for the average person who is using financial or economic theories thought in business school

You'd never hear that from a spruiker, the govt, or Granny Herald. But you raise a good point: intuition and prudent risk management are key. Buy low, sell high. If you buy high and hope that money printing can make it work for you, then you also have to accept the consequences. I for one don't believe that central banks are the masters of the universe.

Haven't posted a comment for a long time... but have moved back to Auckland after four years in another part of NZ... going to auction next week... Agent has given one indication (which seems very reasonable) - wondering how bad it might get at auction on Tuesday!

Agents lie about expectations. Take whatever they say and add $200k. They want another warm body at the auction bidding even if at the lower end

We'll see. I'll post an update next week. I really have no idea what this one will go for. I know what I'd like it to go for... but that's probably wishful thinking!

It's a bit of a unique property - only had one owner, never really been on the market. Probably too small for people with a family, yields won't be there for investors, retirees might not like the stairs, couples might not like some of the body corporate rules... there's a lot of people who aren't interested in this one. I could see it going 3 ways... around the agent's expectations... $100k-$200k above the expectations... or ballistic because it is a unique property... if it goes ballistic - I won't be winning it. I don't see the point in bidding significantly over what I think a property is worth.

I give up...Property wins. Backed by the powers above. It's the only thing that matters in life.

I saw a banner ad asking for donations to World Vision. Made me giggle.

I walked into a Shoe store, tried on a pair of Nike trainers. Shop assistant said you'll take them, I said yip, I'll buy them and I walked out and I bought them...online of course, half the price.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.