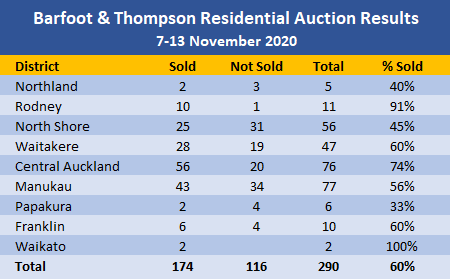

Activity is going from strength to strength in Barfoot & Thompson's auction rooms with the agency handling 290 auction properties last week (7-13 November).

That compares with 258 auction properties the previous week, 243 the week before that and 214 the week before that.

This suggests the market is showing no sign of slowing down as it heads towards its last big rush before the Christmas/New Year break.

The overall sales rate was also up slightly for the week at 60%, compared to 59% the previous week and 54% the week before that.

The central Auckland suburbs were the busiest with 77 properties going under the hammer and sales achieved on three quarters (74%) of them, while the Manukau auctions were just as busy, handling 77 properties and an overall sales rate of 56% (see table below for the full breakdown).

Details of the individual properties offered and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

81 Comments

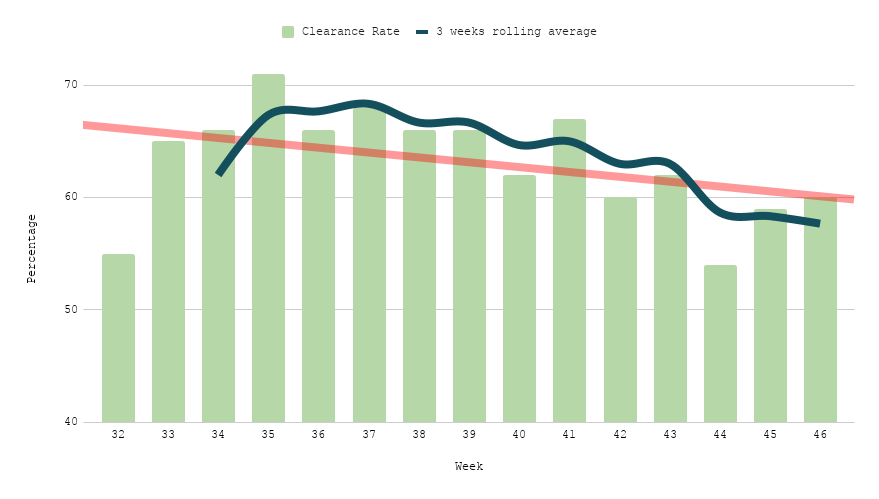

Clearance rates remain at levels lower than what we saw two months ago.

https://i.postimg.cc/4NhNGvtd/BT-clearance-rates-3w-trend-w46.png

{kind=link}

Pardon my ignorance but what is the relevance? I would expect the rates to be relatively flat as vendors set expectations (reserves) on what has happened the past few weeks so a bit of a lag effect, perhaps.

It shows the auction market seems to have started to cool down since a few weeks ago.

But has it cooled because of a downturn in buyers, or because vendors have raised their expectations? The nuance to me on a rate being between 55-65% seems more like settling in rather than a sudden change that indicates a hot or cold market. Surely there is a rate that marks the turn on either sides?

Note I have calculated the moving average so this accounts already noise. Either way prices will go down from now if B&T wants their vendors to sell at the rates they did at the peak.

"prices will go down from now..."

Here is the true reason for b21's posts, he/she wants house prices to go down, any real data has little relevance to him/her, he/she will nit pick in the hope of finding the smallest sign that could support a price drop.

Why are you being so doom and gloom Yvil, try to see the positive side of things. As much as most of us want prices to go down I am not basing my impressions in wishes but just in the data that all of us have access to.

b21

It is correct that the clearance rate may be showing a decline.

However your conclusion that your data "shows the auction market seems to have started to cool down since a few weeks ago" is not a valid conclusion if "cooling" means that the the state of the market is negative.

To be able draw that conclusion your premise negates three important measures; the number of properties bought to market, the number of sales, and prices achieved.

Your graph proports to show a trend of a declining market over the past 15 weeks - that is utter rubbish. Your methodology and conclusion are flawed.

Recent REINZ monthly data clearly shows the opposite to what you claim. The latest report shows that for October Auckland median prices were up 4.7% for the month of October (16.3% YOY) and sales were up 5.5% for October (50.9% YOY) and October - and this is within the 15 weeks of data you claim to show the market trending down.

You need to critically look at your methodology and data in terms of reality and question as to whether you have a strong bias and are simply trying to provide conclusions to support a case that is divorced from reality.

Personally, I am concerned about the unsustainability of current prices rises and the risks that it proposes - but providing such data to support a false narrative as you do does not add to the recognition of the extent of the problem nor the need for this to be addressed.

Note: You specify that the market has "cool down since a few weeks ago" is arguably not supported by your data which shows increases over that three week period.

Why are you being so negative? This is good news and based on the data reported by B&T which you can find on this website.

b21

Not being negative at all.

Just correcting your misleading assertion.

Your suggestion that "the market is cooling" suggests that we are going to see declining prices this side of Christmas - this seems unlikely and contrary to the many screaming for the the need for immediate need of LVRs to "cool the market".

I haven't made any prediction with the timeline you are suggesting, just shared the data for everyone to see.

At this rate, it should be compulsory for everyone to have a RE license...it will bring us all out of poverty. Forget tourism, farming, manufacturing...we have property. We can even export our RE agents, take over the world.

There is nothing stopping you from getting a RE license and partaking in the fun

Is it fun to you to have hyperinflation in an asset which is required for people to live in?

Seriously, I was thinking about it.

A long as you're not the grunt door-knocking and cold-calling to get listings. It's not that glamorous at the bottom, but you can write the Urus off against income on the bright side.

What if you're an ex-Shortland Street star or retired rugby player with a bit of a rep? Easy money.

There's nothing stopping people doing all sorts of legal things that can generate good income eg. Prostitution. Whether it is fulfilling and contributing to the greater good is another question.

Labour is doing every NZer a favour by saying but not delivering.

Property price will double during the next three years boosting by the opportunities, development, increasing income from ASEAN countries as a result of the RCEP.

Oh Yeah..

Keep buying guys.

There is in fact evidence that the market is slowing - RE NZ new listings per day.

Readers might take the trouble to keep an eye on this metric which shows push factor of sellers.

It peaked at 256 per day on November 5th

It then averaged 225 for a bit but is now below 180.

Turnover is dropping a little and consequently the total of all listings is rising, at last, but still 20% odd below last year.

Yes, noticed that too, following the clearance rate moving average tells the same story, check my post above.

Mike

What do you mean by “the market slowing”?

Do you mean that prices or just turnover is slowing?

Your comment has a negative connotation as to the state of the market direction. Be aware that listings could well be down as some - especially investors - are not listing as they see upside in prices; this is not a negative connotation as to what is considered market direction.

printer8 This is indeed a very positive thing, the market slowing down means the likeliness of more affordable prices in the future is higher. We all want a country where quality housing is available at prices people can afford. True it may affect investors but hey they took the risk and nobody asked them to do so.

b21

Your comment is really divorced from reality. As my post above in response to your flawed conclusion and Mike's assertion shows there is no cooling of the market.

REINZ Auckland median prices for October were up 4.7% for the month and sales up 5.5% for the month which from memory if not records for October were close to it. That is not a cooling market.

Yes, there is need for the market to cool - but both you and Mike are in denial and add nothing by saying that the market is cooling.

We are just looking at the data, of course REINZ is reporting also data (unrelated to this discussion BTW) which is relevant but it is delayed compared to this. Try to see the positive side of things.

b21

REINZ data is not irrelevant - it shoots a bl**dy big hole in your false narrative! :)

As for you "just looking at the data": a basic principle: don't look at data with a preconceived bias.

As mentioned I want to see a "cooling of the market" in terms of prices but please stop giving me false hope. Start looking at the data critically and stop kidding yourself that it is currently occurring. :)

I am not trying to give you any hopes, just presenting the data as it is, you get your own conclusions mate.

b21

I'm not stupid.

You are not "just presenting data as it is" but also drawing a conclusion - "the market is cooling" is a conclusion.

I do not take issue with your raw data - I take issue with your (selective) use and interpretation to the data to draw what I consider to be a flawed conclusion.

Now that we are "mates" - Cheers :)

Great post P8, spot on

Hi Printer,

no there is no negative connotation intended.

Rate at which new listings is slowing, ie going down. The 5.7 day average is 183, including today.

I use 5.7 because most listings are added in the morning.

I agree with your point re investors "not listing" for price expectation reasons.

However, that would be opposite of FOMO for buyers!

That seems to suggest you feel investors are also sellers as well as buyers, but of course a key unknown is what ratio is of buyer to seller in terms of investor class.

My general sentiment at present is that market pricing is not slowing but that seller flocking to market is slowing.

And that, at this time of year, that is not normal, as normally such a trend does not set in til around December 10th or later and then lasts for 5-6 weeks from then before accelerating again for the summer market peak. I feel that demand has been pushed into a concertina effect by removal of LVR, plus pulled forward due to lowering of rates. This set of facts is however in flux and push factor of it is not a constant, so seller input is reducing prematurely.

I remain of considered view that a mania phase of market could be driven by desire for lower pop density places to live, esp driving NSC and central Auckland sales

but primarily it is out of synch as demographic push is not present , as in 40-47 year olds in pop does not peak again until late 2023

Mike

"My general sentiment at present is that market pricing is not slowing but that seller flocking to market is slowing".

I have no problem that listings may be down.

However note that the most common used measures of the market - sales and median prices - for the month of October were exceptionally high (REINZ). Most people would not call that a "cooling market".

In fact a shortage of listings has the potential to drive prices up further and in such a situation please do refer to this as a "cooling market".

Thanks Mr Orr.

What I am finding hard to digest as a potential buyer is that of those 290 properties listed at auction you need to be unconditional. Every home that meets requirements and where people are prepared to make an offer, they need to carry out due diligence at the cost of $1,000+ (lawyers, building report, LIM). As you are competing with 30-40 others on a single property that is quite a bit of money collectively. So, 290 homes*35 offers*$1,000 = $10,150,000 just in one week, one RE agency, one city! Builders, local councils, and Lawyers must be creaming it. Would like to see some official figures in these areas.

I think you would be surprised at how little due diligence is under taken. I know when we purchased that we were the only ones that had a building inspection done on the property, and we weren't bidding against ourselves.

I agree. In my experience builders reports are often simplistic and for most houses not worth the money. And given the uncertainty of the auction process in a hot market a buyer can't afford to get report after report done.

All of the properties I've been eyeing up are going for well in excess of their RV. The bank will lend 79% of the RV, but that will not get you anywhere on auction day.

As well as watching the market accelerate out of reach in the last year, I have also had my deposit depleted through the cost of unsuccessfully attending auctions. As Ryu points out: Solicitor, building report, valuation LIM etc)

It really does feel like its one big racket...

How about a system such as Scotland's, where vendors are required to provide a Home Report pack, including a building survey, valuation, energy report and details of any alerations/consents etc

You may need to get onto your bank to get them to provide better service. They should be offering free basic valuation reports (e.g. corelogic) and giving a pre-approval up to a certain limit in reference to it. I.e. the cv should be complemented in some respects based on the third party report and your serviceability of the loan. it's at that point they should be saying that proper valuation needs to take place prior to auction.

But I agree, auctions are rackets in that they do not allow conditional terms to avoid people wasting their money and any conditional pre auction offer will just set a baseline minimum that the vendor thinks they will get.

Try another bank, each of their criteria around this is quite different.

I'm glad I never ever took any notice of DGM's around property, 38 years in the market to date !

Yes, a lot of folk will be kicking themselves for short-sightedly being be born too late.... they wont be making that mistake again!

Not sure what advice I should be giving my kids now though. "Stiff biscuits, you've missed out?" or more helpfully "Don't get married or have kids, save every penny you can and by 2050 you might be able to pool deposits with other 40yr old mates to get into a house (in Greymouth)"

Slapheid

"Yes, a lot of folk will be kicking themselves for short-sightedly being be born too late...."

The reality is that a considerable number of posters on this site will be kicking themselves for being short-sighted, two months ago, six months ago, a year ago, two years ago, three years ago, four years ago . . . . for calling bubble burst rather than buying.

All knowing and confident at the time but now claiming their misfortune is because they were born too late - a lame self-appeasement comment.

Cheers :)

The reality is that a considerable number of posters on this site will be kicking themselves for being short-sighted, two months ago, six months ago, a year ago, two years ago, three years ago, four years ago . . . . for calling bubble burst rather than buying.

Of course you're talking about NZ houses not Bitcoin. The Bitcoin 'bubble' did burst. But it's now on its way up, partly because of all the money printing that is destroying value and propping up the NZ property bubble.

Funny old world.

6 months ago. The RB and all NZ banks were predicting house price reductions and increases in unemployment following the lock down. For a FHB do you think it would have been wise to enter the market at that point given these predictions?

Even Tony 'House Prices will never fall' Alexander was picking a 5-10% fall.

Slapheid, no doubt you will be giving your kids advice to "blame all the things that are out of your control in life and don't focus on what you can actually do yourself to improve your life"

How very presumptuous.. Actually Yvil, I'm more of a "own your choices and control your controllables" type of Dad. That and "never eat anything bigger than your head"

Seriously though, if property values keep outstripping salary increases at this rate, I really worry that my kids will struggle to ever have their own home.

Do you honestly see this trend continuing for the next few decades? forever?

I see mortgage rates settling at 2% long term. That is $24k per annum to service a $1.5m property with a 20% deposit - easily doable for a professional couple. That is where I pick the Auckland average to go within 5y.

Professional Couple - Auckland Average.. Are those the same thing?

Also a $1.2m mortgage at 2% interest is $53,000 PA. for a 30 year term...

I obviously didn't do p&i fibonacci.

It's only double the cost to service the mortgage to what you said. Lets say a bank will only lend you 5 times your income, you would need $240,000 a year to service a $1.2m mortgage. Average household income in Auckland is just over $100,000 so you would need to be earning more than twice the average household income to service a mortgage of what you are predicting to be the average house price.. Doesn't seem to add up.

About 1k per week, ahhh nothing!!! Don't forget rates and insurances - - oh just more small change!!!

Agree, 2% and lower rates will be there for a long time, which should alleviate the FOMO some seem to have these days, however your example is far from being realistic given the actual salaries we see, furthermore saving for 20% deposit on a 1.5m house (300K) is not something that is close to being feasible for most, not if you have a rent to pay at least.

I agree the deposit is going to be a challenge, but that is a $1.5m house so in todays market that would get you something ok?

I, like many, are resigned to "assisting" the kids.

Man what drugs are you on, I want some of them!

A 300k deposit 'easily doable'????

Well blaming the time when you're born is not, I quote you: "own your choices and control your controllables".

Yes I honestly see the trend of higher house prices continue for this decade at least. (note I'm not casting a judgement of it being good or bad)

The real danger in what you're saying is the attitude it encourages people to take towards politics. The decisions made by those in government affect housing affordability, and those decisions arent - and shouldn't be treated as - out of our control.

A lot of our hard won rights - womens suffrage, the 8 hour day, land rights - have been achieved precisely because brave people didn't just assume that the decisions made by government were something they just had to put up with, and because those people focused not just on improving their own lives but on the lives of others too

It was an easy thing to do in the housing market from 38 years ago, much different from the one the newer generations need to face these days in which they must be very careful if they don't want to end up in a lot of trouble.

b21

Latest RBNZ mortgage data shows that September was the highest number of FHB since data collected and first published in August 2014. :)

What this comment has to do with mine has me intrigued.

I believe it is reference to the the storming collective of first home buyers who are currently willing and able to trample all paths into home ownership. It should be noted in fairness that April , was the lowest month for FHB since the RBNZ commenced this data series.

Yes the first home buyer, who's deposit has had to be begged from their parents or by guaranteeing equity from their own home.

Just received aLugtons Hamilton flyer in my mail box very proud of the fact that they had sold a nearby property for 155k over the CV.

Sold for 865k.

Presumably the new buyers will think that their new purchase will be worth a million in a couple of years.

You would have to be brave to say it wouldn't be.

One near me recently went to auction with "must be sold on or before auction day, ignore cv". Didn't sell on the day, now asking 98% of cv....

Well they wouldn't send you a flyer with the information about those properties they sold under CV right?

NZHerald today - "Prime Minister Jacinda Ardern has hinted the Government is looking into ways to help first-home buyers onto the property ladder by tinkering with the restrictions of its home-buying subsidy scheme".

Does she not realise that subsidising FHBs into the market will send house prices even higher.

The road to hell is paved with good virtue signalling.

This is exactly what Morrison did in AU, resulting in prices of home and land packages going up pretty much overnight by 50K. The solution is not to push from the bottom but from the top making already existing closed homes available to the market.

I’m listening. What are you proposing? Has it been done elsewhere and if so what was the outcome?

Yes house prices rose immediately

Federal Government First Home Buyer Grants coupled with State Government First Home Buyer Grants

Prices rose by the amount of the grants of $50,000

It is not that there are not realistic and feasible options we could use, although the neoliberal textbook seems to act as a blindfold for our politicians. Just as a starter, reimpose LVR restrictions and ban housing investment until we reach the same affordability levels we used to have 30 years ago, or at the very least impose a CGT which would discourage investment in first necessity assets at the levels we see these days. Also a tax on closed properties in high density population areas (~50K just in Auckland) would encourage making those available for rent, and in some cases we will see those back into the market which will increase offer. We do have options.

By banning housing investment, you surely mean banning private individuals, who already own 1 or more houses from being able to buy houses, whether existing or new. You want only first home buyers and government to be able to invest in houses. I also suppose you want the government to lend FHB to buy their houses. It will be an interesting experiment. I think it will work if the new neighborhoods that are constructed are as attractive, or hopefully even more attractive to the existing suburbs. An ambitious and very capable enterprise may be able to deliver on that. Otherwise it will be a total flop.

On CGT, you are being very hopeful. Money is not in property because of lack of CGT, it is a cherry on top of the cake, but as long as there is absolutely no business opportunity for investing, money will flow to property.

Agree, there is no silver bullet, but at least we should start shooting somewhere that is not our own feet.

Yeah WTF is she thinking ' damn, prices are getting high...let's increase the FHB grant, that'll help things right?'

Yep, she doesn't have a clue.

If the market is booming, why are the Shore Auctions lacking? Only 25 sold out of 56? Whats going on Barfoots?

There is a higher proportion of asian people living on the shore, since CV, there has been more asian people leaving NZ than arriving into NZ

Could be. I'm hoping to see an increase in the French population over here in the coming years.

Moi aussi, merci ; )

Harcourts does a reasonable job in the nsc. Last 7 days they have sold 26/36 on nsc.

https://www.cooperandco.co.nz/harcourts-cooper-co-auction-results-2020/

It's fascinating how obsessed some people here are with property prices. There's a few people who post a lot on house price articles and are nowhere to be seen on Interest's many other interesting articles.

The vendors have now got very greedy - so much reporting across all forms of media has seen vendors put their head in the clouds and increase their reserve prices. Many auctions now becoming negotiations on the auction room floor rather than classic auctions, often reserves are adjusted mid auction. Also have a problem now as the council are no longer issuing urgent LIM reports - now you have to wait up to 10 working days for a LIM.

Some sellers have even pulled their auctions at the last minute and decided to try again in March in the expectation of getting 10% more - and they probably will the way things are going.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.