Dominant Auckland realtor Barfoot & Thompson has finished 2020 strongly with sales volumes up +28% over 2019 and their median price exceeding $1 mln for the first time.

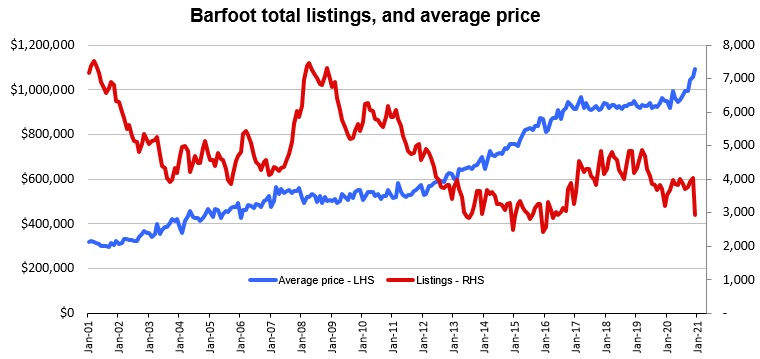

They sold 11,944 properties in the year, enough to give them about 40% market share in the large Auckland market.

In December, the finish was very strong, selling 1479 properties, almost double the 779 sold in December 2019.

Even more impressive, that 1479 sales level was a record high for any December for the company.

December average prices were $1,092,518, also a record high. Median prices hit a new record high as well, reaching $1,005,000, +3.2% above the November level, and a whopping +16.2% higher than in December 2019. That is the fastest price growth since May 2015.

Twenty percent of their sales are now over $2 mln.

Barfoots expects the surge to continue into January, 2021. A company spokesman said "What these sales numbers do not show is the large number of yet to be completed and conditional sales in the pipeline, many of which will show up in January and February sales data, and this will ensure that the market makes a strong start to 2021."

More properties are coming on to the market for sale, but not at the pace of sales demand. It is a market "desperately short" of supply. Barfoots listed 868 properties for sale, the highest number of new listings in a December for a decade. However, with sales numbers being so high at month’s end they had only 2938 homes on their books at the end of the year, their lowest number in five years.

Economics 101 says when demand exceeds the supply, the price offered will rise. When the variance is large, the price rise will be large. These effects happen at the margins, driving the market expectation that the 'value' of all housing is rising.

There are about 560,000 dwellings in Auckland. In 2020 about +16,000 new dwellings were added, increasing the supply by less than +3%. All up, about 27,000 houses changed ownership in the year, so the price is being set by these transactions at the margin which account for only 5% of all dwellings. The other 95% get "the wealth effect" even though they are not in the market.

For fun, a back-of-the-envelope calculation: If the median price is now $1 mln, that makes the value of all Auckland dwellings a massive $560 bln. This value rose 16.2% in 2020 which means the untaxed capital gain in Auckland in 2020 was $78 bln. Tax on that exceeds every Government budget line item - the cost of National Superannuation is 'only' $16.3 bln. GST only takes in $18.1 bln per year, company tax only $11.6 bln per year. Untaxed gains from housing mean taxes in other areas are higher than they could otherwise be. Ditto Government debt.

Barfoot Auckland

Select chart tabs

162 Comments

The message for many Auckland homebuyers (and other buyers scattered throughout NZ) will be, simply: "Let's get in while we can".

TTP

“Let’s keep moving” is so apt for 2021.

"Cause I'm movin' on up, you're movin' on out

Movin' on up, nothin' can stop me

Movin' on up, you're movin' on out

Time to break free, nothin' can stop me, yeah"

Stop this madness dead in tracks, I would be in favour of strong medicine

The message for most young people should be "Leave NZ, no one cares about you here and you'll have better chances elsewhere".

...and don't forget to keep making your student debt repayments.

yer we got it free but F you losers

Going to University is a choice, you either agree to pay the fees or you don't go. There are clearly better paying paying jobs in the trades now rather than coming out of university with huge debt and a useless degree. Get into a trade, I never regretted it. You most certainly do not need a degree to become successful in life, in fact it would appear that some of the high school dropouts are the most successful.

We need nurses and teachers as well as tradesmen. Either you think it should be possible for someone who wants to do the important work of teaching and nursing to be able to do so without incurring the kind of debt that makes it just about impossible for them to have the kind of basics we used to take for granted on their salary (like be able to own a modest home and raise a family) or you don't.

Quarantine free flights start on Thursday.. Young people, this is what you can buy for roughly 1 mil just 2.5 hours flight away, 15 mins walk to centre CBD. Or stay home and 1mil you can buy a rotty 3br home in Clendon Park..

https://www.realestate.com.au/property-house-qld-petrie+terrace-1348373…

Gosh, you'd have to sling an awful lot of ice creams over summer in a Tairua shop to afford something like that here.

Yeah, but the land on that property is about the same size as my garage in Auckland, so I'll stay put thanks.

And it'd be a pretty nice/big house in Clendon Park that sells for $1M, so be fair.

Have you been (or live) in Clendon Park, Manurewa? I used to work in the area, on average 3 stolen cars per week in our staff carpark even though we have security guard stationed there.

Btw, don't get mix up Clevedon and Clendon - they are chalk and cheese!

I used to work around Clendon also. It's a terrifying s**thole. You couldn't pay me a million to live there.

It's also less than 60 metres from the M3 motorway. There seems to be plenty at least as good, cheaper, in many areas of NZ. Check out what you'd get for around the same price in Napier.

Over many years as a reader on this site I'm bemused as to why the only alternatives people offer to Auckland are overseas and Invercargill, although out of respect for those commentators I'll put the latter down to hyperbole.

A huge part of the business world happens online nowadays, and the pandemic has shown us how easy it is for white collar jobs to be performed remotely. Why tell the young to just get out of NZ? Why not tell them to consider moving to the regions? Sure it's exporting the problem, but at least it buys the country time while the government sits on its thumb trying to figure out what's happening. Repopulate the regions with young families and they'll require services, which brings blue collar opportunities as well.

Auckland is pretty much a write-off for the young, and Wellington is fast heading the same way, but there's still plenty of opportunity right here without putting a bloody great stretch of water in the middle of extended families.

I am one of those white collar workers that is fortunate enough to be able to work remotely and offer services across the globe. The only reason we don't move to the regions is that we have a child with special needs where family support and proximity to Starship Hospital is a necessity.

Completely understand and you have my support. I too have a child with a medical condition that requires careful management. Starship staff do an amazing job, I've been there numerous times but I couldn't work there, I'd be a puddle of tears all the time.

Have you seen what house prices are doing in the regions? The reason Dunedin was the get-out was because it was a largely cheaper, affordable university town that still passed muster as a city. Now that prices have spiked there, people are looking further and further out. As for remote work, a job done remotely is a job that can be done cheaper by someone somewhere else. Not a dice I'd want to roll at the moment if I'm competing with leveraged Aucklanders looking for their next big capital gain outside of the 09 for a family home.

Nearly thirteen years living outside (and in) a small town while working remotely for a major multinational that has thousands of staff in much cheaper countries...yep I know exactly what it's like. I'm not saying it'll work for everyone, I just think the choice of "Auckland or gtfo" is a little short on options.

Totally agree. Housing prices in NZ are bad enough, however it is what you get for the money spent.

Not true we just bought a beautiful renovated freehold 3 bedroom weatherboard in lower North Shore about 20 mins from the city for less than 1 Mil. The repayments are less than it would be to rent it so it’s the most affordable I’ve seen Auckland in a long time that’s why the prices are going up.

Sounds like there's a catch to this equation... what's classified as lower North Shore? Was this sold at auction? Mind you, just under 1 million is still not affordable...by any means, especially if rates were to rise.

800K loan @ 2.5% = $385 interest per week. That sounds pretty affordable.

But can the average punter get an interest only 800k loan? Take a couple, both on 60k, who have actually managed to save the 200k deposit. Could they walk into a bank and say 'we earn 120k between us, we'd like to borrow 800k and only pay the interest, thanks'?

Likely not. But the extra ~$340 principal payments are effectively savings.

If you can't avoid paying it, you have to factor it in to the budget (whether it is effectively savings or not). Because there is no point telling someone that something is affordable because it will cost them $725 a week but $340 is effectively savings if they don't have $725 a week available. The number that matters for affordability is the number that's coming out of their paycheck every week.

The problem with being 20 mins from the city by car on the shore is that it's more like 40 minutes in traffic (if you are lucky). If it was 20 minutes by train, it would be different- but unlike most cities in Aus Auckland doesnot have fast reliable public transport options to most suburbs.

It’s 20 mins not in rush hour. In traffic it’s 35 on the bus and 30 on the Ferry.

Not an auction just very lucky to be in a multi offer situation during the Christmas break. We missed out on a few at auction before that and glad we did.

I met a couple over the Xmas break who are fresh off the boat from the UK. Both have well-paid jobs awaiting them in Wellington but can't get a house there for love nor money. They're staying temporarily in West Auckland and a casual chat to the neighbour revealed he owned 160 properties. FFS!!!

Ffs ... csb

Maybe they could ask him for a place to rent?

Many thanks TTP ol' boy .....you are keeping the plebs in line with your wisdom and this fine market ticking along nicely......always remember the old saying "pump and dump" - then rinse and repeat .....haw haw

Totally ill advice. There are already enough over-leveraged households which can barely pay their mortgages which is a risk for them and the country's economy. I can just assume one can say this motivated by a wish of further capital gains.

No disrespect but TTP has been right in his/her past predictions. Property has never been cheaper than today. This time next year our money supply will have increased another 10%, where do you think that money will get funneled?

I would expect you are not serious because it really looks like you are joking. Encouraging people to get into an overpriced market is just something someone with some vested interest can do. It is not about right or wrong, if I would say tomorrow will be sunny after a series of sunny days I will likely be right but asking people to not to use sunscreen is what the problem is.

It’s not overpriced. The nominal amount is not what you should be looking at. The serviceability is nothing on 1 million bucks right now and will stay that way for many years. If the economy starts booming and they hike rates rents will increase way beyond repayments I’d rather be owning than renting in that situation

Is this another joke? Mortgages must be paid in full regardless the amount of the payments. Are you forgetting that instead of paying in 20 years you will be now spending another 10 more years of your life paying back your debt when you could invest it in anything else or use it for your retirement? What happens when you still have a loan over 800K and interest rates go up a single point? We do not have 30y fixed loans as they do in other countries. Lying to yourself like this you are shooting at your own feet and effectively stealing from your future self. Let's please be serious about this.

The new norm for city slickers will be only paying off your mortgage when you sell to go to a retirement home and/or relocate to a small town.

b21 you do not have the track record to be giving any advice,

Didn't expect you would understand nor support my point. Some of your best trolling so far BTW.

What you are overlooking is that people in jurisdictions that have good housing policies have housing at 3x median income and also low-interest rates.

NZ's median income/house multiple up to the early 1990s was also 3x.

But it is worse than it looks, as household income is now 2 or more individual incomes when it was originally only one, plus the quality of our housing compared to other developed countries is very poor.

Later this month the Govt. is meant to be releasing policy to either curb prices and/or make it more affordable to buy a property. But they have said this before and it only gets worse.

Yep, let’s be greedy. Stuff first home buyers.

haw haw jolly good show .....now to "short" the big 4 Australasian banks when it all comes tumbling down .....haw haw

I detect a bit of cynicism in some of the comments above.

TTP

TTP ol' chum ....you are "on the money" ....it's all about "turnover" ....the banks mortgage books increase , hence their profits .....therefore their ability to increase their capacity for more mortgages ...more profit ....and so it goes ....keeping the prices ever increasing ........haw haw

Just a tip from my genuine leather bound 19th century French Chaise Lounge - always have an "exit plan" when things just get plain "frothy" ....haw haw

How very nouveau riche of you, Charles. A genuine 19thC French item of furniture should be described as a chaise "longue" out of respect for both the language and the manufacturer. Please hand in your tie and blazer.

Bravo ! General C, you are spot on ol' boy.... I stand corrected....must have a word with my old French school master back in my Eton days ....toodle pip

Rockstar economy - more and more millionaires every day!*

*(Ignore the excessive debt they have)

Well, the corelogic property value estimate in the ANZ app has gone up $120k in less than a year, and the amount owing on the mortgage has gone down ~5% in the same time. So when we refix in 6 months our mortgage rate is going to drop about 1.5%. Seems to me like the debt number is getting less excessive by the month....

NZ Property and Bitcoin and now the same thing.

Yet more cynicism.......

But short on substance.

TTP

The substance of it all will become evident in time.

Ratus...hows your BTC going ...

Well apparently there's a shortage of houses in NZ and there's a fixed supply of BTC, so there's some kind of association related to scarcity. One thing there's no shortage of is credit for mortgage more or less created out of thin air.

By getting progressively more expensive until a correction occurs, yes.

In regards to what you are holding for your purchase, no.

In USD terms it would be even better.

Great back-of-the-envelope last paragraph. I'm following rental market data in the Hutt valley - generally, asking prices look well out-of-control. I wouldn't be surprised if yoy increases are 50%+ up between Q1 2020 and Q1 2021. Here's an example of how recent buy-to-let purchases have inflated asking rents;

2/518 Ferguson Drive, Upper Hutt

Block of five flats. Flat 2 purchased December, 2020 - RV $290,000. Purchase price not yet confirmed but assumed to be over $500,000. Rent estimate before sale was $340-420 per week.

Post-sale asking rent $545 per week. Rented within 10 days of listing.

That's an 88% rent price hike based on the rent estimate midpoint from the pre-2020 sale price

Google maps street view of the property here;

https://www.google.com/maps/place/518+Fergusson+Drive,+Trentham,+Upper+…

3 beds in 60 sqm and $545? For Upper Hutt, and it rented? The only logical explanation is money laundering because otherwise I really struggle to comprehend this.

Yeah, nuts. Here's another one.

9/37 Mills Street - 1 bed upstairs flat in block of 12

ASKING RENT - $390/WEEK

https://homes.co.nz/address/lower-hutt/boulcott/9-37-mills-street/09rNn

If we divide the current RV of $1.9m for the block of 12 by 12 - that's an RV of $158,333 per flat.

So, according to the rent affordability calculator (i.e., rent of no more than 30% of gross income) - you need a gross income of $70,000 to live in a $158K flat.

Here's the Google Street view of that one;

https://www.google.com/maps/place/37+Mills+Street,+Boulcott,+Lower+Hutt…

It's nuts, for sure.

What a s#%* hole of a flat

No kidding. And don't forget in order to comfortably afford that 1 bedder, you need to earn in excess of the average salary in Lower Hutt;

https://www.payscale.com/research/NZ/Location=Lower-Hutt/Salary

Need 3 beds in the Hutt? How's this?

5 Clouston Park Road, Upper Hutt

https://www.realestate.co.nz/3919251/residential/rental/5-clouston-park…

$560 per week

RV = $440,000. Bought in 2019 for $425,000 against a then RV of $255,000. That's a 73% increase in RV over a three year period.

Current rent estimate on homes.co.nz is $370–$460/week - midpoint rent estimate = $415/week

So landlord is looking for a 35% premium on the midpoint rent estimate and a 22% premium on the high end rent estimate.

#rentcontrolnow.

PS According to the rent affordability calculator, you'll need a gross household income of $100,000 for that rent to be considered affordable;

https://www.calculate.co.nz/rent-affordability-calculator.php

Can you really trust homes.co.nz for market rent and/or sale price indication? Often it's wildly off. Where do they get their rent indications from? I saw an article on stuff showing how the site is manipulated by RE agents and likes aswell - in particular for house value.

https://i.stuff.co.nz/life-style/homed/real-estate/300179648/housing-ma…

I agree their numbers are certainly part-responsible for the rampant inflation we are seeing. The thing is this is where the 'market' goes to get a price estimate (I think TradeMe does them too) - be it house price or rent price. homes.co.nz are auto updating them much more frequently now - perhaps on a 3-monthly basis (maybe even more frequently). All they are doing is applying something similar to the QV formula on a quarterly, as opposed to 3-yearly, basis. This more frequent update is a nightmare for buyers and renters, for sure.

Kate and Njfty

Why are you not using rent data from tenancy.govt.nz. ?

It is updated monthly and obtained when all new bonds are lodged (bond lodgement forms require rent data). Note that these are not estimated rents as used by REA when marketing a property (which you may be referring to) but actual real rents obtained.

This data can be considered both reliable and current. It is used by other government agencies,recognised economists, and yes, landlords when determining and reviewing rents and as a basis for rent movements as justification for proposed increases to WINZ.

Interest.co use this data, along with lower quartile house prices; although arguably limited it provides a better and more reliable snapshot rather than individual properties which in themselves don’t necessarily reflect reality.

Yeah I referred to tenancy.govt.nz in a below comment re: rental. I questioned the validity of homes.co.nz

I like the completeness of your posts P8 they cut through the BS like a hot knife.

I could use it - it's not far off the midpoints I am using from homes.co.nz

I am collecting this 'real time' (i.e., daily rent listings) data in order to 'test' my proposed weekly rent maxima formula (= (RV/1000) +/- x%) in order to determine the appropriate variable ('x') in order to make the lower quartile rents affordable.

If we look at tenancy.govt.nz the lower quartile rents in the Hutt are already unaffordable - hence the accommodation supplement costs are rising, and the burgeoning homelessness and emergency/transitional housing we see in the area. And worse, what I'm now seeing in 'real time' ads is that asking rents are in most cases exceeding both the tenancy.govt.nz data, as well as the homes.co.nz rent estimates - by a significant margin.

In other words, the market is stuffed and needs to be reigned in.

#rentcontrolnow.

P8. I added the tenancy.govt.nz figures to my spreadsheet.

Asking rents are presently running on average 15% above the tenancy.govt.nz figures.

That is only across the 20 properties listed on realestate.co.nz since 21/12/20 - roughly new listings over the past two weeks.

I don't think that's even a one bedroom - the pictures only show a living area, kitchen and bathroom. $390 for a studio (and not even a flash one - the kitchen and bathroom look pretty tired) is ridiculous.

I've seen much nicer in the slums of Cairo... what a sh1+hole. Having said that, you pay a premium for a 1-bedder. I always flatted to save money, you really need to be a couple to make it work (or entitled).

That's pretty unfair on people who are single well into adulthood. I wouldn't call a 40-year-old who is over living with flatmates 'entitled'.

I agree, I was referring to 20 - 35 bracket.

From what I see and hear (and I would have a reasonable idea), that looks like a rip-off and you can get much better value in town.

Like this one?

https://www.realestate.co.nz/3919109/residential/rental/219-tama-street…

Only $320/week. Landlord bought it in 2005 for $91,000. Current RV = $270,000.

Concrete block walls - don't see a heating source.

And, you only need a gross salary of $55,000 to make that affordable. So, hey, an OAP couple could take on another single OAP to share with them and they just make it!!!! Yippie.

https://www.superlife.co.nz/resources/articles-guides/understanding-nz-…

This government needs to hang its head in shame.

Yes, and additionally there is the problem of solo parents taking in boarders and hangers on as a means to make the rent. This puts children at higher risk than they would otherwise have been in in a single-parent household.

You are passionate and well informed Kate. In most cities the price of houses has risen as well as rents falling, NZ appears unique in that rents are rising. The FT also printed an article on NZ house prices yesterday with >200 comments. They laid the blame at bureaucracy, council red tape and tax favouring housing. All Central Banks have ZIRP so they did not identify this as an issue.

Yes, I've 'heard' that theory - even TSY (Working Paper 09/05 - Andrew Coleman and Grant Scobie) modelled that;

“falling real interest rates result in lower rents, higher house prices and lower owner-occupancy rates”.

But I'm not seeing that. Early days, as I'd like to see whether these current asking prices end up being rented, but it's not looking good at all so far. Perhaps asking price will come down.

I'll have a look for the FT article.

The FT is subscription only - https://www.ft.com/content/2ec734f0-23b4-4aef-9675-f89d357ce0e1 "New Zealand's Housing Crisis Poses Big test for Ardern"

Rents falling in foreign cities is as much about the desire to move out of high density living under Covid and the ability to work remotely. NZ doesn't have the high density living of most cities, so we haven't seen that flight. I also read a report by an outfit called Demographia that had Auckland housing quite a bit more affordable than Sydney and not far behind Adelaide. http://www.demographia.com/dhi.pdf

As above, I just calculated the Hutt asking rents for listings over the past fortnight against the tenancy.govt.nz figures. A 15% average rent price rise over those past six month averages.

This has got to be stopped in its tracks - in this area anyway!

Hi Kate,

A month or less ago, I read a comment on here that the Hutt had a huge glut of new townhouses/walk-ups coming on stream, and many were sitting stagnant or dropping price to capture tenancies.

As an Aucklander, I don't know the Hutt Market, have you see any of this conjecturally?

Yes, a great deal of new build two-story townhouses - many I suspect purchased off plan. Coming to the rental market now and yes, I'm watching them;

Asking $725/week;

https://www.realestate.co.nz/3918944/residential/rental/1-aporutu-stree…

Asking $700/week;

https://www.realestate.co.nz/3919106/residential/rental/113a-witako-epu…

Will let you know if I see any price drops before they are eventually let.

Cheers, thats a part of the market am really watching, as in auckland there is a huge amount of them in the pipeline, enough that I suspect it will affect the supply/demand balance in next 12 months.

It'll happen, despite people trying not to fold. If a market segment can only support $x per year, it doesn't matter if you get 100 landlords collectively asking $x + 1. Someone will miss out on rental income. How many Landlords (new or existing) are freehold?

When Labour runs a "War on Landlords" which results in large numbers of landlords selling up, then of course rents go up. Landlords have had to compensate for the loss of negative gearing, costs of insulation, and even more costs are being imposed on landlords this year as rangehoods, heat pumps and bathroom fans become mandatory so they will probably go up further. And the "bad tenants for life" rules that come into effect next month will likely see more landlords exit, so prices will go up again. Everyone told this Govt what would happen to rents. They chose to ignore that advice.

Is there any evidence that large numbers of landlords are selling up? Because that seems unlikely, given record low numbers of properties on the market. Also, it seems unlikely that the increased costs you point to would push many landlords out. Let's assume an outlay of 10k for all the things you mention. Any landlord who bought more than a few months ago would have had at least 10k in capital gains, so they could whack it on the mortgage. Any landlord who bought more than a year ago would have lower interest rates on their mortgage which would be enough to cover the extra payments. So unless you were a freehold landlord, or you bought very recently (in which case you would have been very stupid not to factor in the things you've mentioned) you're unlikely to be worse off.

Exactly. Which is why I'm also collecting data on the last date of sale (and the price paid) for rental properties advertised - as a means to quantify the rightness or wrongness of this argument that landlords will exit the market en masse. Certainly the majority (by a wide margin) of rentals advertised were purchased many years ago at far, far, far lower prices than their current market value. But, the trend in terms of rent prices is on the up and up.

Shows as only 2 bedroom on RE listing?

https://harcourts.co.nz/Property/933004/UH12318/2-518-Fergusson-Drive

Doesn't mean it's not 3 bedrms

Why would the agent only list as 2 bedrooms? If it had 3 bedrooms you would advertise as that. If it's too small to consider a bedroom you'd say study or atleast mention it...

Oops, my mistake - it was 2 bed. Sorry about that! Have edited.

Certainly looks like greed from the landlord & desperation from the tenant. Looking at Market Rent Upper Hutt - Trentham 01 Jun 2020 - 30 Nov 2020 you can see there's a large premium in rent paid on this flat. https://www.tenancy.govt.nz/rent-bond-and-bills/market-rent/?location=U…

Yes, I can't explain it except to say that the property data from 6 months ago is likely way out and (hence) bringing the reported average down. This isn't the only example from the 'real time' data I've been collecting for Upper and Lower Hutt since 21/12/20.

Yes its very shocking I agree with you... first, whos to blame for the runaway train that is the property market, second, the solutions can only be draconian measures and that has economic downsides the govt and rb will not want to deal with. Yes there are LVR changes but will that do much and could take a year before any change. Certainly agree more needs doing and immediately.

As I said, I'm only just beginning to collect the 'real time' data for the Hutt - but if the trend I'm seeing carries on and these places actually get rented at these exorbitant prices, then the only thing for it is #rentcontrolnow. And yeah, draconian - but otherwise it's a big increase in accommodation supplement subsidies, alongside unfulfilled demands on food banks.

A real crisis in the making for renters.

Do you think the rents are being achieved because of high emergency housing demands... EH pays 50 percent more than standard good quality tenants. Govt pays motel owners 220 per night vs 140/150 per night otherwise . Higher risk equals higher return.

No idea. But, if we assume it is HNZ renting these as transitional housing places - we're stuffed.

The government needs to act - and not by way of taxpayer dollars.

#rentcontrolnow.

I think #rentcontrolnow is not the answer to a supply and demand issue, and it will make rental properties more scarce going forward with little investment in this asset class due to draconian laws as opposed to market forces.

It will be great for the FHB and the share market IMHO though....

Yeah, I've heard it (the orthodox view) all before. The houses don't go away and will be occupied by someone, be it renter or owner.

Soooo how is #rentcontrolnow going to fix the shortage????

I think you asked me that before. I don't know that there is a shortage, some say yes, some say no;

https://www.oneroof.co.nz/news/ashley-church-the-housing-shortage-is-a-…

My concern is the price of rents for existing (not new) dwellings.

"runaway train"

The gravy train of young girls career move and then those kids needing care and income support too when they get older... responsible for much of the emergency housing need

Sorry to burst your bigoted bubble but;

The rate of teenage pregnancy in New Zealand has halved in the past decade, the Ministry of Health has revealed. The Report on Maternity found that in 2017 the teenage birth rate was 15 per 1000 females. In 2008 it was 33 per 1000.

https://www.rnz.co.nz/news/national/387028/teenage-pregnancy-on-the-dec….

No I will ignore your ad hom, you should say fiscally and socially responsible

The demand from those in EH was massive and ever growing the last time we rented. We dont target that sector and why would you, the risk is not worth it for us. But for those who do they can easily justify a premium imho

Well, yeah, that's definitely orthodox economics - the market punishes the most downtrodden. And my mother always taught me you can't get blood out of a stone... but the market is sure trying its hardest.

Judging by the RE agents facebook post (https://www.facebook.com/lwalkerSOLD1T/photos/a.639378359532681/2090215… ), it sold for $525k

OMG.

I'd calculate it sold for $525k

"JUST SOLD - Trentham - Upper Hutt - 81% over Rateable Value

No typos here - you've read it right! We have just sold Unit 2/518 Fergusson Drive, Trentham. This delightful 2 bedroom, 60sqm unit was beautifully presented and won the hearts of many. 14 days on the market, 9 offers at Deadline. RV $290,000."

"This value rose 16.2% in 2020 which means the untaxed capital gain in Auckland in 2020 was $78 bln"

Perhaps this could be re-worded as "Unrealised Capital Gains"

Capital Gains can only be taxed when realised on sale, just as Capital loses could only be realised on sale.

Bring in a CGT by all means but it HAS TO BE inclusive of all sales including the family home, business, art, cars, Bitcoin, everything so we are on a level playing field.

And that is the issue with a CGT: you can effectively realise those gains by borrowing against them at incredibly low interest rates, so why would you sell (unless you are certain values will go down).

Hence why some kind of land / asset / wealth tax paid annually makes more sense. In fact give up taxing income and consumption altogether and move to 100% wealth taxation. The other taxes are very arbitrary.

How is it more arbitrary than a wealth tax? At least with income tax, income is taxed when it is earned, not on and on and in perpetuity. I'd think taxpayers would want some assurances around government performance and accountability to the electorate (now just a forgotten relic of democracy) before handing over the right to tax accumulated already-taxed income over and over and over again.

Because a wealth tax covers all wealth; an income tax only covers suckers like me that work for someone, and GST only covers suckers like me that spend a good percentage of their money not buying assets.

It is very common for people to think something makes sense just because it has always been done that way. But if the goal is to ensure the richer people in society pay the most tax and the poorer people pay the least, income and consumption taxes will often do the opposite.

But that depends; we have an outcome with our current tax system where high earners pay more tax - in fact we're super reliant on a very small group of highly paid, likely highly-skilled workers. On the face of it, that's good and bad. But when it comes to wealth, It's just not that simple. How does a wealth tax work from a compliance point of view? If the one house that I own is going up in price faster than my income does, then the government gets more revenue from me, even though it's a paper gain, while government inaction and incompetence is the largest key driver in inflating the underlying value of the asset. Given that we can't even stomach adjusting income tax brackets for something as simple as inflation, you're putting a lot of faith in the people who got us into this mess to design a better system than the one we have now, which could be far effective with some basic tweaks.

I’m not sure the current system works as well as you think. Someone on minimum wage who owns nothing and ends up with no disposable income after expenses probably pays more tax than the average property developer who has millions of dollars in appreciating assets. People who spend 100% of their money on living expenses get taxed another 15% in GST than those who earn more and can funnel it into assets. I think your theory that it can’t be fixed so let’s not try is a convenient cop out.

A business that makes no profit after expenses pays no tax, yet an individual that makes no profit after expenses typically pays a truck load.

I'm not a huge fan of the current system, I'm just not pretending a wealth tax is a silver bullet for everything or going to end up any easier to administer or be worth the effort involved in shifting away from our current system. I also said we'd be better off making the current system work than try to make some simplistic Robin Hood-attempt at making the same people ultimately pay the same amount of tax, so not sure where you're getting me saying "it can't be fixed" from. And of course someone earning a wage is going to pay more than a property developer on assets held, much in the same way we don't tax businesses for having inventory on their balance sheets. One's revenue and one isn't. As for businesses claiming expenses but individuals not being able to (at least not personal expenses) - that's how you end up with a hugely complicated tax code with idealogical allowances and deductions that get so politically charged, they can never be repealed without a political shitstorm. Look at the harm that Accomodation supplements have done - we all know it, but we'll never be able to get rid of them.

. . . . just observing; and last March the common post was for bubble burst with 50 to 80% falls by the end of the year.

. . . . again just observing; RBNZ won against Covid, and expectations of economic down turn, high unemployment, and consequent bubble burst.

I suspect RBNZ will not be wanting to see this action all undone.

I still hope to see a flattish market this year and beyond as current growth rates seem unsustainable without increasing risk of a correction.

Those FHB who bought last year seeking a home will be relieved.

Those FHB who have held off will be sadly feeling frustrated going into this year with properties now $100+k more; for them I hope that market does cool and a further fall in interest rates will result in increasing affordability.

just observing; and last March the common post was for bubble burst with 50 to 80% falls by the end of the year.

Really? One of the more recognized prophets of the NZ property bubble Ashley Church said house prices would fall in 2020. He was wrong. As were 6 out of 7 of his predictions. No wonder Bindi jumped ship.

I have not read any comments with the exaggerated numbers as the ones you say, but in case you didn't notice something happened in 2020, now whether the bubble will keep going is up to our Government and central bank. If they do nothing it will burst rather soon than late, but they can of course keep manipulating the market as they did recently to push the inevitable a bit further.

I never recall ANYONE saying prices would drop 80%....

Fritz

Incredible as it may seem there was a group of three or four mooting a fall of 50 to 80% and getting a number of up-ticks for doing so. It is just worthy of noting in light of subsequent events. (Putting it into context even the banks were forecasting 10 to 15%)

The claims were pretty extreme and reflected a lot of the baseless assertions being made prompting me to record them at the time to show at a later date the credibility of these posters. I did subsequently remind a couple of these posters later much to their embarrassment and reaction of wrath. One of these was Foreign Buyer (who no longer seems about) and his standout comment was that “anyone considering buying is officially stoopied (sic)”.

If you really want me I can reference them but are currently away in holiday away from my laptop and the world and house prices have moved on albeit not as they expected - but if you really want me too, I will give it thought on my return

The extreme claims being made in March are worthy of recalling.

Since 2007/8 (some might argue longer) Reserve Bank monetary policy has prodominantly been aimed at credit creation, it would be interesting to hear how they intend to extricate themselves from this given they are now almost holding the accelerator right to the floor but CPI is decoupling from asset prices at an increasing rate.

For every action...

It is plainly obvious that central banks around the world are creating asset bubbles such as housing, bitcoin, etc. But apparently that is not inflation. Time for a rethink...

It is plainly obvious that central banks around the world are creating asset bubbles such as housing, bitcoin, etc.

How do you measure a bubble in Bitcoin? Furthermore, the conversation is starting to shift towards the idea that there are no bubbles, but the value of your currency is being destroyed.

Measure everything relative to gold?

True, it could be a rush to assets (not necessarily a bubble) or currency devaluation. Either way some funky stuff is happening, and I am not sure its going to have a very good outcome. We would be better off with higher interest rates IMO.

We would be better off with higher interest rates IMO.

Or better off with 'sound money' principles, which is a key tenet of Bitcoin. Interest rates are just a mechanism to control behavior.

Depends what you define as money I guess. To me Bitcoin is more of an asset than money (and a pretty useless asset IMO). The core purpose of money is to allow people to exchange goods and services and Bitcoin will never be good for that.

Do you think money should be a store of value? At the moment, young people's income is being deflated away rapidly while the old farts get to 'benefit' from asset appreciation (the young bucks will possibly be attracted to BTC but that's another story).

I think most young people think money "should be" a store of value. There is an incentive to save. It seems to me that the old farts don't care about the currency being destroyed. They're closer to leaving this mortal coil. Quite selfish if you think about it.

Our Core Logic mid-range valuation has increased 11% since 8 November. Pushes us past 70% equity (purchased Mid 2017 with a 23% deposit). It's a bit of a joke, yeah cool we've done well on paper but for many of my peers home ownership is unattainable.

NZDan congratulations; a younger (millennial?) “Covid winner”.

Nobody can be critical as you looked to buy a home mid-2017 just after the peak of the Auckland market and when some on this site were calling bubble burst - but you had the b*lls to go ahead.

Previous comments indicate you aren’t leveraging off this (I think you did possibly mention a new car at one stage) so you are clearly being prudent.

Whatever the market does in the next few years, a significant correction is irrelevant as long as you can manage the mortgage payments; in that regard I would be paying down debt even though rates are low at the moment but over the term of the loan there is some risk of rate increases.

Bottom line, you will be feeling secure and enjoying the intrinsic value of homeownership.

Despite affordability issues and the varied market predictions, as you have done, I wish potential FHB well.

I'm in a somewhat similar situation, and don't see how my house increasing in value is me 'winning'. It's largely outside my control and only makes me a relative 'winner' thanks to high house prices creating so many losers.

Yeah that's the way I see it. The only way i'm "winning" is access to low interest rate lending from the equity, some insulation from price falls and a "feel good factor" from my opportunity to lock in my purchase at a lower price than today.

I would like to see house prices at least 30% lower than they are currently, we'd be buying/selling in the same market so spot prices are largely inconsequential but makes home ownership much more attainable for my peers/relatives.

I think we're in the same boat, Nzdan, and it absolutely makes a difference even if you're in the same market if you're planning on moving up in size or changing areas. I'm on the verge of having to start looking for an extra bedroom and if I did it at the moment, I'd still be facing roughly doubling my mortgage to move to a nicer part of Auckland.

Yup a Millenial. Leaving the equity untouched aside from a new car purchase. Our trusty 20+ year old Toyota has clocked up over 250k kms and is starting to become a liability, particularly as it's our only vehicle.

Tempted to leverage the equity into an upgrade/new build, but will see how the next 12 - 24 months pans out. If the market continues to take off then we'll just have additional equity to leverage from.

NZDan

Great having options.

CLs figures seem way way higher for my house, than other estimate websites like trademe, and homes. What do these agents use to get their estimated value of a property?

I was looking at some articles from the 1990's, and house prices and GVs went down back then in Wellington. So house prices don't always go up over the shorter term.

Love that last paragraph. From another angle, national house values are now around $1,250 billion. So, a 1% property tax would raise $12.5 billion - enough to make ALL earnings below $60,000 tax free (and still have plenty of change to put the top tax level back down). With a 3% property tax and an increase in GST from 15% to 20% - you could eliminate income tax altogether!

Imagine the incentive to keep property valuations down if subject to a value based tax!

That's a great idea. Also worth noting is that for a couple on the pension who own a $500k house, they would essentially be no worse off, as the amount they would have been taxed on the pension instead goes to property tax. People who don't own property would be a lot better off, and most importantly, it would incentivize a big sector of the population who currently don't have to care about the ridiculousness of rising house prices (property owners) to agitate against massive increases, as for once it would be hitting them in their back pockets.

Another cliché. "The rich get richer and the poor get shafted some more." Something like that.

FOMO being created as market about to open.

Get ready for an onslaught of articles creating FOMO from all media outlets. Wonder if it will work aswell in 2021 or has your average punter had enough of the same ol' spin.

I think people are now starting to see that much of it is propaganda. Like all the stories that are drip fed on a regular basis, of young couples who managed to buy their first home by making the sacrifice of forgoing their avocado on toast and coffee each day.

But I am now seeing people who own rentals, who are thinking of leaving their rentals empty depending on how their new tenancy laws work out.

Exactly, those conceding to FOMO now will be the worst hit I'd stay out as long as you can and watch the house of cards crumble from the outside.

"watch the house of cards crumble from the outside."

Until it doesn't and the ground you lost is gone for good.

Firm ground here my friend. Plus you need to think of future generations, or we just care about getting in now and screw our children?

Been saying that since 2012 (duh) not to mention 2019 and 2020. Those who trusted that were scammed by well intentioned fools

I do not think anyone was talking about that at that time, prices were relatively affordable, nothing compared to the unsustainable mess what's become now. (duh) Just think what would happen if the RBNZ would decide to increase rates to the same level from a year ago (which they can and might have to do), that shows how brittle everything is.

The rbnz could remove interest only loans... effectively putting up interest rates on a quarter of mortgages and changing the numbers drastically for speculators as they would need to find on average $15- 20k a year to hold their position

And it could be easily explained by Jacinda why it is necessary

Probably a good idea, although too mild as a measure at this stage in my opinion. A total ban of housing as an investment is needed, at least in high density areas or those with lower inventory until incomes can catch up with current prices to 3-5 income-to-loan ratios.

Completely impractical

idea... how would that work in practice?

Totally feasible. Banks already must know whether mortgages are issued to investors or owner occupiers. Plus they already apply different LVR restrictions to each one of those groups so they can just be directed by the reserve bank to not to issue any debt except for the latter group. I know some might feel even offended by this since might feel like is personal if you are making an income out of this but it is not, it is just what needs to be done to fix a very important issue.

Ok, I can see what you suggest but I think the public will go bonkers if you ban landlording....partial or full.. for some, actually a lot of New Zealanders,it is their only hope of affording a standard of living that they have become accustomed too...that’s the sad thing about this whole affair... all the money has been directed towards unproductive investments... if the houses don’t keep going up then so many people have nothing to retire on...a future of really bad outcomes for some

Graeme wheeler explained that the house prices will revert to mean when real interest rates increase... once the market smells that the house might be worth less in a years time watch how the market changes

Agree, investment flows towards unproductive assets are a huge problem, however I have not proposed banning landlords as you suggest, we would just not be increasing their number for some time or allow already existing ones to accumulate more properties to give the chance to those that still do not own to have their own house if they wish.

Ban foreign buyers...

Oops done that already.

They banned them after the horse had already bolted, and the number of overseas buyers had already dropped. Now we are selling them to ourselves/mum and dad investors earning zero interest in the banks.

800 people looking at one apartment in Perth City the other day (inquiries to agent via email)... Im assuming plenty of young kiwis that want to get paid heaps and start to 'live the dream', are about to come over...welcome! It is the best decision you can make!

800 people looking at one apartment in Perth City the other day (inquiries to agent via email)... Im assuming plenty of young kiwis that want to get paid heaps and start to 'live the dream', are about to come over...welcome! It is the best decision you can make!

Why do real estate people insist on using the 'median' price instead of the 'mean' or average price? When their is a small sample, the median price could be well off the average/mean price..

You're right that when there is a small sample, the median could be well off the average. That's why it is used. Assume for example than 9 houses sell for 500k and one house sells for 2million. The average house price is 650k, and the median is 500k. The median is more useful here because it gives more accurate info about what most people are having to spend to get a house.

The Reserve bank said they wanted the government to implement things such as a Loan to Income ratio. According to a property expert in NZ, this would kill the housing market in NZ if they did this, and sales would slow right down. But isn't a loan to income ratio a smart thing to do , as it is about reducing risk of a crash occurring. NZs property bubble has to be the worst in the world , especially compared to incomes.

They should have a tax on non rented secondary houses and land. This would reduce the land banking that happens and free up houses for people who need them. It would also improve the culture and communities of places like the Mount.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.