Content supplied by realestate.co.nz

Real-time data from realestate.co.nz suggests that stock shortages will continue to pose challenges for Kiwi buyers at the start of 2021.

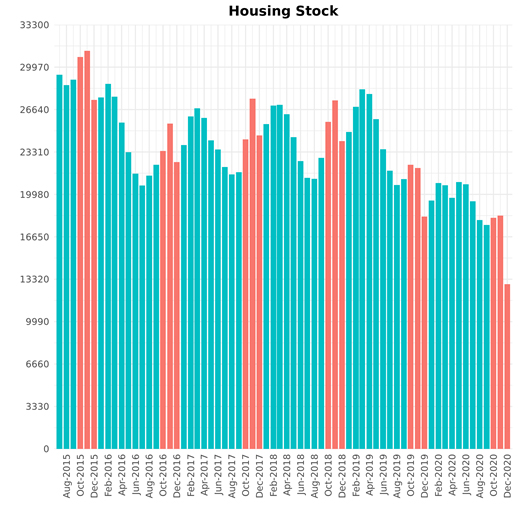

Housing stock was down year-on-year in almost every region in New Zealand during December, with 16 of 19 regions falling to all-time lows since records began 13 years ago. The national stock level was also at a record low.

Vanessa Taylor, spokesperson for realestate.co.nz, says this is despite a year-on-year 19.2% increase in new listings coming onto the market during December.

“There were 29.1% less homes available for sale at the end of last month compared to December 2019, creating a significant mismatch in supply and demand.”

“We’re still seeing a lot of competition in the market and I expect this will continue to drive strong prices in the first quarter of 2021, encouraged by low mortgage rates and a lack of international travel,” says Vanessa.

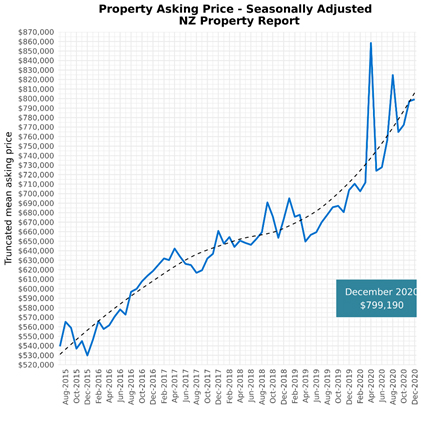

The national average asking price is now $799,190 – a 13.6% increase on December last year.

Average asking price up 13.6% on last year, with record highs in two regions

Real-time data from realestate.co.nz shows the national average asking price remained stable month-on-month in December with a marginal 0.3% increase on November 2020. However, this number increased by 13.6% when compared to December 2019.

The asking price for properties around New Zealand was $799,190 at the close of 2020, compared to $703,780 in December 2019.

“Asking prices nationally are now $95,410 more than the same time last year,” says Vanessa.

Two regions reached all-time average asking price highs in December, with Bay of Plenty and Central North Island recording peak prices since realestate.co.nz records began 13 years ago.

Bay of Plenty prices were up 8.1% year-on-year, with the asking price reaching a high of $780,475.

But it was Central North Island that recorded the country’s biggest increase, with the region’s average asking price climbing to $685,044 – up 20.7% on November 2020 and 38.8% on December 2019.

“Although this might be welcome news for sellers, it may not be time to celebrate just yet.”

“We saw a significant number of high-end and large lifestyle properties come onto the market in the Central North Island during December, which has pushed the average asking price up,” cautions Vanessa.

Stock shortage continues, with record lows nationally and in 16 regions

Property remains in short supply across the country with only 12,932 homes available for purchase in New Zealand at the end of December – 29.1% less than the same time last year, a 13-year record low.

Housing stock was down year-on-year in almost every region last month, with 16 of 19 regions falling to record lows.

“Only Auckland, Gisborne and Central Otago/Lakes avoided hitting 13-year record stock lows in December,” says Vanessa.

Wairarapa, Coromandel and Nelson & Bays had the lowest stock compared to 2019, decreasing by 58.5%, 50.3% and 49.2% respectively.

“The stock shortage will likely continue to prove challenging for buyers at the beginning of 2021,” says Vanessa.

“This is a long-term factor impacting the New Zealand market and the number of Kiwis returning from overseas, combined with low mortgage rates and lack of international travel, are only adding to the demand for property.”

| 13-YEAR RECORD TOTAL STOCK LOWS | |||

| Region | Total stock Dec-2019 |

Total stock Dec-2020 |

Year-on-year % decrease |

| Northland | 1,194 | 698 | -41.5% |

| Waikato | 1,315 | 789 | -40.0% |

| Bay of Plenty | 1,232 | 669 | -45.7% |

| Hawke’s Bay | 371 | 203 | -45.3% |

| Taranaki | 342 | 221 | -35.4% |

| Wellington | 571 | 346 | -39.4% |

| Nelson & Bays | 352 | 179 | -49.2% |

| West Coast | 324 | 201 | -38.0% |

| Canterbury | 2,786 | 1,766 | -36.6% |

| Otago | 394 | 287 | -27.2% |

| Southland | 314 | 252 | -19.7% |

| Coromandel | 441 | 219 | -50.3% |

| Marlborough | 245 | 125 | -49.0% |

| Wairarapa | 205 | 85 | -58.5% |

| Central North Island | 305 | 192 | -37.1% |

| Manawatu / Whanganui | 609 | 315 | -48.3% |

| National | 18,230 | 12,932 | -29.1% |

New listings up – but regions still in short supply

New listings are up 19.2% year-on-year to 6,592, with 1,064 more properties coming onto the market last month than December 2019.

“Although it’s promising to see pockets of new listings coming onto the market across the country, it was largely our major centres that did the heavy lifting last month,” says Vanessa.

Of the 6,592 properties that came onto the market in December 2020, more than half were in Auckland, Wellington and Canterbury.

“Buyers in regional New Zealand are still faced with little choice at the moment,” says Vanessa.

Auckland saw the most significant increase in new listings last month, with 52.0% more new listings compared to December 2019, while Marlborough saw the biggest decrease with 23.5% fewer properties coming onto the market.

Housing inventory

Select chart tabs

88 Comments

A friend of mine got emailed on the weekend that a product was available in stock. He thought to pick it up from Auckland and save the $160 delivery fee... after a 2.5 hr drive yesterday he finds out he missed out as the item had been sold to another customer... of course now he has learned the lesson to get in fast or miss out. So its not just real estate where that is a problem

It’s a problem that’s been developing over at least a couple of decades - and nigh impossible to resolve.......

Thus, house prices will remain stubbornly high indefinitely - and growing numbers of NZers have figured that out.

TTP

Rubbish.

The problem is nothing more than incompetent and spineless leadership.

These problems could be resolved at the stroke of a pen if we had a government with a brain and a central bank with a heart.

I agree. The only way affordability will improve is if house prices decrease and Jacinda said she doesn’t want that to happen despite campaigning in 2017 on improving affordability. I don’t think she is that naive so one has to assume she is just disingenuous . Even the blue party said that house prices needed to come down in some areas (although they would never actually implement policy to achieve this).

"The only way affordability will improve is if house prices decrease"

Wrong. The latest report I read said that affordability in the 25 percent quartile had not deteriorated from the same period in 2019 even though prices had risen. I think you might know this already, affordability is calculated based on home prices, wage rates and interest rates, all three factors are used to arrive at a result. However on an individual level, is a house unaffordable where one person cannot afford it yet the next person can

Feel free to share that report but it is disingenuous to not consider the deposit required to obtain a larger and larger mortgage when considering housing affordability.

Interest.co report. As you a regular here on interest you should have been all over it... again, if one person cannot afford a house yet the next person can does that make it unaffordable. The one who cannot afford the house could also look for something cheaper.

That report has major limitations as others have discussed. A clue to whether housing is currently unaffordable would be to look at ownership rates which are at historic lows and continuing to decline.

Well said Albert.

Leveraging yourself on unrealised capital gains to purchase a rental doesn't make it affordable.

I've been looking at open homes the last 4-6months and time and time again, beaten by investors overpaying on 2bd or 3bd starter houses who can rent for about what the mortgage+expenses are for the year. They are all banking on TAX FREE gains and interest rates at 2.5%. History tells us interest rates don't stay down forever. At some point these will go up and suddenly your servicing costs double. One hope's the mortgage is paid down but on interest only, that's a fools game.

Best of luck to all.

stjohn. We have an FHB child trying to get onto the wellington market, albeit at the mid range point not entry level, so I relate to the pain behind your comments. They have a solid deposit and good finance but repeatedly are out bid by investors. On multiple occasions where they've missed out the same houses appear on 'to rent' sites within a few weeks. Most are unsuitable as investments and returning pitiful gross returns at the lunatic prices new owners have paid. Clearly bought for capital gains. I struggle with fellow boomers ruthlessly outbidding FHBrs like you in the middle of a national housing crisis such as we have but my lawyer mate scoffs at me observing there are also plenty of younger and recent migrant aspiring landlord magnates who are snapping up as much property as they can. The retail banks must now step up to the plate and fulfil the terms of their social license to operate, by actively curbing lending to speculative 'investing' in RE.

A story told over many dinner tables around NZ every night...

My late grandparents would question is this the New Zealand they fought in world wars for. A greedy, me before you world. A shame we have chased the dollar at the expense of man.

The greatest oxymoron of our time:- The Free market and pumping $100billion+ into the economy. Capitalist in gain, socialist in loss.

I agree and feel for people wanting their first home but struggling to get it. Pardon me but your "FHB child" does not appear to be in that camp instead they seem to be struggling to get on the ladder bypassing the bottom rungs and entering "albeit at the mid range point". Maybe you don't agree with what they're doing but surely they need to adjust their expectations.

Point noted but the same scenario applies for entry point housing - ie they would need to massively overpay because of the actions of acquisitive speculators. The issues are systemic across all levels of housing largely caused by dumb decisions repeatedly made by politicians from 2000 on. For reasons not known govt advisers didn't foresee the obvious linkage between red tape constraints on expanding supply at a time when recklessly expansionary immigration policies were being implemented. And now it's our young people paying the price.

The current housing market may not be the best but it is the best we have. For now. I went to a property talk given by Brad Sugars about 5 years ago and he said then, when your child is one year old one method would be to buy a rental house and then let the tenant pay off the mortgage over 20 years. By then your child has grown up and you give them the house for their 21st.. I thought mmm not a silly idea. The property market needs fixing because the govt yielded to lobby groups of all types and restricted supply.

I remeber being told as a child to study hard, go to university, get a good education and well paying job in a professional field and you can have a good life. Are we now telling children to do all that and you may be able to aspire to the bottom rung! My advise would be to get out of this shithole country as early as possible.

The only way to solve the housing problem is to eliminate investors. There should be no tax deductions on interest on existing houses. It is all about self interest now,.

Jacinda will never eliminate investors.... did you see her guffawing with Jenee Tibsharaeny ... "therein lies the crux of the problem" investors are drawn to housing because of stable positive returns

And/or investors should have to build new and help be part of the solution

And interest rates can and will go up and can render that "affordable" house unaffordable overnight. Earnings, you can have some control over. And as long as people are unable to save for the required deposit they are screwed no matter how your mortgage repayments compare favourably to your exorbitant rent that you are just barely affording.

Your "next person" will likely have had the help of mum and dad, won lotto or already own houses from which the deposit can be obtained

Interest rates will only increase if the economy is really picking up again not likely and if so rents will also rocket up. You can fix for 5 years at current attractive rates. All the factors driving it are there imagine what will happen when the borders get opened up again. It’s absolutely crazy to be sitting on the sidelines with cash at the moment hoping for better prices when affordability is finally here right now.

SO while it may still be "afforadble", it no comes with having to get a significantly higher mortgage, and far greater risk.

A stroke of a pen doesn't build the 30,000(?) state houses we need to create a slight oversupply in the rental market.

With the stroke of a pen I just created an annual tax on vacant homes and residental zoned land.

With another stroke of a pen I banned immigration for non-citizens.

Suddenly the "shortage" seems to have vanished.

Lol, that vacant land is just going to start sprouting houses from seeds is it?

And the vacant houses trope, give it a break. There are some, but nowhere near enough where people want to live, that are in a liveable condition.

So landbanking is just a figment of our imagination now is it? When the parasites are removed the houses will sprout.

Some is in fact greater than none. Houses are for living in.

Let's have a few more strokes of the pen shall we?

Bye bye accomodation supplement.

Bye bye front loading infrastructure costs.

Bye bye rural urban boundary.

Bye bye interest only loans.

Bye bye subdivision red tape.

Hello debt to income ratios.

Hello capital gains tax.

Lol. Reality be damned huh?

These are all strokes of the pen. Nothing more.

The people exploiting the current situation to enrich themselves can be damned for sure.

Yes, they are all strokes of the pen, but they aren't hands on nail guns, and the effects of cancelling accomodation supplements.. Instant tripling of state housing waiting lists..all good right?

State housing waiting lists have tripled by doing nothing.

That doesn't make tripling them again any better you loon.

I assume you think phasing out the accomodation supplement will triple the waiting lists.

In reality it will just cause rents to drop. Loony.

Oh, now we are phasing it out, not just cancelling it huh? Thats slightly different and the effect would depend on how you do it. But no, rents won't just drop without tons of people being forced into homelessness first.

The AS is paid direct to tenants and they have discretion as to how to spend it and some tenants live the high life. Believe me I have seen it first hand.

lol, that'll never happen.

I believe the words used were "bye bye".

The accomodation supplement increases rents and increases house prices. It must go.

I will agree with that... when govt state housing is abolished. A level playing field is fair and equal. So if one group gets subsidized housing and rent discounts so should the other. When state housing is abolished and that group paying market rent it would not be fair for the other group in private housing to receive AS

Yes, it must go, but first you need to build somewhere for most of those people to go, or tent cities.. but thats not going to fly. If you dont build houses for those people they will be booted out when they can't afford rent, and dont be bullshitting yourself they will go and buy a house, the house will be re-tenanted or sold to someone much better off than your average acc suppl recipient.

I note with a lot of the comments supporting the status quo or making changes ie that they are sometimes arguing at cross purposes.

As an analogy: if there was a car crash with injured passengers on a poorly designed section of road. Some would say the solution is to have better hospitals to treat the injured, others argue that increased signage to warn of the danger, and others would argue to redesign the road so you didn't need the signage or the extra hospitals. And of course, the latter two are needed if the road has already been designed, but would not be needed in the future when all new roads are better designed and older roads repaired. Thus a group of people could all be right and start correcting all solutions immediately, but they have to act rather than stand around arguing each point.

But there is another group I note that justifies their argument just because the law allows it, ie they just act what is right in front of them, they don't care there has been a crash. If there is money to made from it, whether it's robbing the injured, or hospital staff, stealing the road signage, to designing the faulty roads, they are in.

When you ask them why they do what they do, it's because it's legal, it's always been that way, if they didn't do it someone else would, etc. and they don't want to think too much about other better fairer ways because it's not in their best self-interest, they are happy to be in a 'Useful State of Ignorance.'

However, there is one more group that is fully aware but chooses to do it anyway. It's in their DNA to do whatever they can get away with. The classic analogy of course is the scorpion and the frog, when the frog asks the scorpion why he stung him after saying he wouldn't and knowing that if he did, he doomed both of them, the scorpion replies, 'but that is what I do, it's my nature.'

Actually the pen strokes required involve making it mandatory for every council in NZ to aggressively rezone land to residential - enough for 30 years expected growth - and the add more weight to doing this to provide housing to people over worries about losing pretty green belts or low productive farm land - Then have govt issue interest free loans to pay for infrastructure to service up new developments - the solution to land bankers is to flood the market - have so much resi land they simply cant bulk buy the lot and then effectively be the controllers of all land supply in NZ, which is the case as present

Yes, you almost have it right.

What jurisdictions do that have really affordable housing is zone out all the land they don't want to be built on eg elite soils, environmental habitats, future roading/rail designations, etc. and then allow any land left over the 'POTENTIAL' to be developed right now, as the market demands.

What this does is give a presumptive right to build on potentially 100's of thousands of possible sites, both out, in and up.

The issue with pre zoning, is it automatically highlights land to be land banked, plus the fact you have on paper 30,000 does not mean that 30,000 are available now, as land bankers will hold back (to force up price), much is being legitimately farmed so they should be allowed to do that, plus council limits the uptake based on their ability to supply infrastructure (which could be supplied by the developer or JV's, and lastly the market may require more one year, less the next.

Even when they quote say 30,000, they always then say eg an average of 3,000 per annum for 10 years, but when you ask them what the range is (an average means nothing without knowing the range), they have no idea. What this means is that supply cannot match demand, thus we will generally always have an undersupply which adds to the rentier behaviour and higher prices.

That's all very well in theory. But once you do that in greater Auckland you aren't left with much land, especially if you 'zone out' hazard prone land.

What you will have left over is bits and pieces of land in often isolated locations. Much of that land will also be highly fragmented, and with challenging topography.

They do this in practice in countries with affordable housing. Sometimes the only difference in theory and practice is doing it.

And if you remove the restrictions, then there is no 'greater' anything.

Also, you don't need to zone out hazard-prone land as the market will price it accordingly and it may well be at a price where the hazards can be mitigated at a price to bring it to a competitive market. If not, it would stay empty.

Also think of 'isolated' locations as ideal work from home locations, villages etc. Which would be perfect for many people, but in doing this, it would make all housing more affordable, and in fact encourage those that wanted to live closer in to be able to do so.

But, as you are inferring, if it will not make much difference, then there is no harm in doing it, and it would remove a level of bureaucratic cost at the very least.

Hi Brock,

When have we ever had a government with a brain and a Reserve Bank with a heart? Not in living memory........

That’s why the problem remains insoluble, Brock. It will persist indefinitely.

While it’s tough on renters like me, there’s nothing we can do!

TTP

Insoluble? It won't dissolve in a solvent?

We haven't had a government quite this brainless or a reserve bank quite this heartless before.

That's actually a perfectly acceptable use of insoluble.

The wrong solvent is being used.

Lol what dribble

Cockroaches swarming to beat the LVR restrictions.

We may need to up the strength of the insect spray to 50% to clear this infestation.

With all due respect, Brock, we'd prefer you contribute something of substance - rather than your tiresome ranting and raving.

TTP

If you find the truth tiresome feel free to find something else to do. Perhaps proof read the signs your agents are putting up.

Why don't YOU contribute with something o substance - rather than your tiresome ranting and raving?

B21

The problem with this was that once the RB said the restrictions would be changed a lot of stupid money would rush to the market, they knew that of course. Restrictions should have been introduced with immediate effect to avoid this which will get a lot of households under the water.

Do our land transaction datasets capture sales to non-resident New Zealand citizens?

Are existing property owners sitting tight & holding off making the next move 'up the property ladder'? It seems there's alot of people stuck at the moment, unable to sell and buy in the same market. People are faced with the predicament that if they sell, likely they'll have to increase their mortgage two fold & have the uncertainty of finding a suitable property. Existing owners can feel rich on paper until they need to upsize/improve house in the same market.

We have thought about downsizing in the current market however with nothing obvious to buy it remains just a thought. Who wants to rent for months or possibly years until the right property comes up? In the regions it may not even be possible to find good rentals, and that may become worse with the new laws.

Perhaps the reason for this reduction is that agents are simply not using realestate.co.nz to advertise properties?

The major RE agencies own realestate.co.nz, and why would any RE agent not list it on one of the biggest RE websites? More eyes = more offers/bidders = more commission.

If agents are relying on advertising to find the best buyer, then trade me has all the same buyers anyway, so to use both sites is a double-up and a waste of money, that's why not all agents are using both sites.

Personally never look at realestate.co.nz - always on the assumption that trademe covers it all, with a better layout & usability. It would be interesting to know how many vendors/RE agents choose to advertise through both with the added costs.

When we purchased I used re.co.nz almost exclusively, trademe's search wasn't as good imo.

I found these numbers from realestate.co.nz to be a little odd - as of today there are 19687 properties for sale on trade me nationallyy - and 640 houses for sale in Wellington with just 35 been added since the 1st Jan - meaning as of the end Dec there were 600 houses on the market on trademe. Even if I took out the 160 sections (of which the majority seem to have a house on them so I assume we would classify these as properties people can live in) I still show 440 houses on the the market as of the end Dec- 100 more than the "supposed" real estate.com figures. Looking at hawkes bay they are showing 339 properties for sale on trademe. Maybe people just dont use realestate.com for selling properties anymore.

What happened to Housing Corp and the building of govt housing? Is the govt preferring to fill up motels now instead for low income families.

And is it no longer politically correct for councils to develop low cost sections (which once were common).

They are building as fast as they can in some areas, but there is a huge backlog they need to catch up with. Not enough builders and most prefer to work for other companies. Try finding a builder in Auckland at the moment, developers are selling off the plans properties they won't even pour foundations for another year+

Houses can be prefabricated in factories and in which case qualified builders are not required, just as engineers are not required to assemble cars. Building houses on site is slow and expensive. All we need is a government with some vision and a minister of finance that doesn't believe that taxpayers create our currency.

Yes, this is true, and it would be a good way for housing NZ to build a shed-load of the houses its needs quickly. Can't see this useless govt doing anything that progressive tho.

Without leadership the situation won't change.

What the stats. don't show is how much of the demand is from either pent up demand, or developer incentives such as no/low initial deposits on off the plan presales that are pulling future demand into the present.

No stock because people like me who want to move see not stock....so we sit and don't release our stock. Market lock up until the forced sales arrive.

There's no stock because we've let speculators purchase 1,000's of houses with leverage from equity from their tax free capital gains they've acquired over the years. They then buy up vast sums of the bottom quartile of houses, thus shutting the door on FHB - who are more likely to trade up and release stock to the market.

Investors, now that they have a pile of houses, with the long term capital gain hand in play, interest rates at near zero, there's no need or want to sell off. thus the stock pool is so small. Its a hoarding of houses in the investors pockets which is driving no stock.

Keep in mind, of houses which are owned in NZ, 30% of them are owned by people with 20+ houses...

Meanwhile the aussies banks have posted profits of $1billion+ dollars EACH every year for as long as I can remember with 60%+ of their lending to residential housing.

It's crazy when you think of it at a macro level and not a micro level. I own my own house and would rather prices were affordable for everyone, than my equity go up and inequality grow every year.

That’s an excellent post I totally agree with the points you make

X2 on good post.

For some reason they left the Auckland number out of the table in this story . They also left out Gisborne and Central Otago. Just mentioned in the story that Auckland was one of those 3 regions that did not have a decline in Stock vs 2019.So what are the Auckland numbers for the December period? New Listings for Auckland in December 2020 were 2161 up 52% vs Dec 2019 . December is not traditionally a month when houses are listed due to the majority of people being on holiday for half the month. Everywhere you look around Auckland dwellings are still going up like crazy. While the population is declining. What do you think will happen to prices?

More needs to be done to encourage people to build. No shortage of sections available in my area at least and plenty more subdivisions ready to start as needed.

I am a new first home buyer myself and we have built new for our first house partly because their was not a lot of choice for existing houses and also because building was really good value.

The only issue is though, it takes about a year to build a house these days.

Maybe Kainga Ora should be buying up more house and land packages and putting them on the market when nearly complete, same as they have been doing with Kiwi Build houses that haven’t sold. That would take away the barrier of having to finance a house you can’t live in for a year while paying rent or another mortgage somewhere else at the same time.

Today I heard Ashley Church say, on radio, for all to hear, the reason there was a shortage of houses was because people who owned houses weren't putting them on the market.

I sincerely hope I do not have to explain why that is the "Doh" of the week

Same as BTC market prop up? in this case who the hell will need to put their house for sale? when last year alone with RBNZ, Banks & Govt actions causing the rise of 20% - only desperate will try to sell, when clearly if you can wait at least until 2025 the price will go up by another 80-90% - CullenCGT off, LVR off, DTI off, Banks TD off, Banks CAR off, QE/LSAP on, FLP on ,flexi-wages subsidy on, low OCR on, Banks deferral on.

I had a post on Facebook appear from Ashley.

I checked out his profile and I would encourage others too... he seems to be a very angry man.

gnx...his senseless rants on the persecution of Israel are epic. They make his property commentary seem balanced.

No doubt he did not express a view as to WHY not?

I believe low stock levels to be the 5 year Brightline Rule having an effect from March 2020. ie. Houses that would otherwise have come to the market after 2 years are now being held for another 3 years before sale in order to avoid paying tax on gains. So I would expect another 3 years of compounding low stock levels before houses purchased from March 2018 are eligible to be sold.

The NZ dear leader already said so, it's just 'supply issue'. Give short simple but choose answer which fall into prolong, complex, impossible/super hard.. so the usual political answer can be uttered in the future 'it's work in progress'. Any prudent economic regulatory input? - 'we're not nanny state, it won't work etc.' one can choose to hear from myriad of economist and still won't do anything, but one can choose to listen to scientist at short notice, yielding result - instead shifting wages/subsidy/unemployment to CB, recently try to shift RE as well wa'

Its almost as if we had a decade of rampant immigration with no plans to house them. If you are a central or local government, long term planning is literally your job. Fail.

Whilst everyone seems to have a view on why there is more demand in market from buyers, no one ventures a view on why people do not want to sell, or rather why about a third fewer want to sell than a year ago. Well here goes: fear for one thing and uncertainty as to what is coming economically. Plus, less desire perhaps for mobility of labour. Also, major moves in prices above CV (30 - 65% above CV sale prices ie) seem focused on property priced $1.4m and above, which is mostly bigger, more land, out of central areas. Which again rep a drive to have more space. Apartment sales and 2-3 bed stuff nowhere near as popular in last 5 months. People in general trying to get away form others. Investors are not buying for themselves but for income, so they are probably buying up all the stock that usually pads out inventory, hence inventory has dropped like a stone and what is OTM over 3m has too. All this applies doubly in Auckland

And asking prices for rents in the Wellington region grows worse by the day.

A/20 Ludlam Crescent, Woburn, Lower Hutt

2 bed top flat in a block of four - $500/week against a tenancy.govt.nz market rent of $385/week

https://www.realestate.co.nz/3920949/residential/rental/a20-ludlam-cres…

RV $410,000. Even my initially proposed rent maxima formula of RV/1000 exceeds the tenancy.govt.nz market rates for low end properties at the moment in the Hutt. And, if you want to buy a 2 bed flat to rent out in future - you'll need a cool half mil (and this is in Upper Hutt!);

Buyer Enquiry over $500,000

https://www.realestate.co.nz/3920912/residential/sale/flat146-keys-stre…

#rentcontrolnow

If you pay $500k for a property you should be getting $500 a week rent. That's called a return on investment. The Labour Govt abolished negative gearing, so the days where landlords offered properties to tenants at a rent that doesnt cover their costs are gone. The Labour Govt was told removing negative gearing would push rents up, so they can't say they werent warned. Insulation and Healthy Homes Standards upgrades will add to that $500k purchase price as well. It all has to be paid for by someone, and landlords have been told they should be recovering those costs from rent and not relying on future capital gains. You cant have it both ways.

Bring these 3 factors into the mix and the high house problem solved :

1. Land tax on all land in urban areas that is being "landbanked" for future gains and not being used for industry, commercial, business, agriculture, horticulture etc ....this will encourage the owners to sell sooner rather than later.

2. All homes in urban areas, that are empty and the owners are NZ residents or not, will attract an "empty property tax". If the taxpayer has to pay an accommodation supplement to top up rents that are unaffordable to many people, why should a property that could be rented sit idle, just on the possibility of future capital gains, that at the moment are not taxed.

3. Capital gains tax for all second or subsequent properties, including the holiday house EXCEPT the family home. I know there will be people that will put their rental property(ies) or bach in the name of a trust, family cat or a second cousin, but if it's found to be the case, capital gains tax will be due immediately, as if the property were to be sold at the current market value.

All solved :)

Any particular reason the family home should be exempt?

We can crush Covid19 in 2020 but house prices now that just impossible to solve via our great leaders.

Maybe 2021 will bring another blackswan event and this may be the final straw before a great reset of interest rates and financial markets.

By the stroke of a pen - include annual House Price increases in the CPI measurement for inflation - result - inflation would then be running at around 9 to 10 %. ( which of course it is with all this printed cash around ) Reserve bank then has to take action to curb inflation, mortgage rates increase, LVR returns, etc

- sanity returns....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.