Barfoot & Thompson's auction rooms remained busy in the week before Easter but the sales rate declined for the third week in a row.

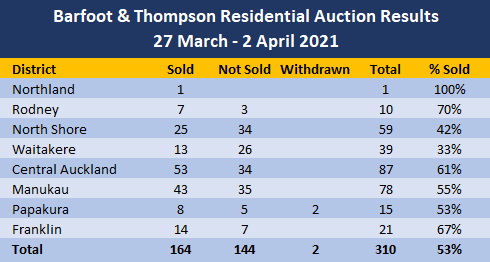

Auckland's biggest real estate agency handled 310 residential auction properties in the week of March 27 to April 2, up from 287 the previous week and 305 the week before that.

That was the highest number of auction properties the agency has handled in the last five weeks, since the week of February 20-26.

The high number of properties auctioned last week was particularly significant given that it was a short week, with Friday being a public holiday and many people taking extra days off on either side of the Easter break.

However while the number of properties being auctioned remained at buoyant levels, the sales rate declined for the third week in a row.

Of the 310 properties marketed for sale by auction last week, sales were achieved on 165, giving an overall sales rate of 53%.

That compares with sales rates of 59% the previous week, 61% the week before that, and 72% the week before that.

Waitakere properties had the lowest sales rate of just 33% last week, followed by those on the North Shore at 42%, while Rodney had the highest sales rate within the Auckland region at 70% (see the table below for the district sales breakdown).

Details of the individual properties offered and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

53 Comments

Happy to admit that my prediction of sales rate dropping below 50% was wrong

but certainly not that far off- it is a big drop off in 2 weeks- given there is still plenty of money available from the banks - just not the yield return for investors.

Banks are squeezing credit, they have already too many overleveraged clients so it will just get worse in the next few months. You could tell they are not confident when they decided to (allegedly) self-impose LVR restrictions at the risk of losing clients.

Yes, auction sales would have been expected to decline in the short week before Easter (will be the same in the week after Easter) as the many successful property investors take a breather and head to their baches in Omaha or Pauanui. What else did one expect?

Also, the purchasers could be at last wising up to the number of leaky homes crowding onto the market; the only homes that have sold since Xmas in my general vicinity are leaky homes.

As I have recently mentioned to Greg property statisticians at this juncture are going to have to separate good properties from lemons if their statistics are going to be valid and have any meaning whatsoever.

Like Literally every single home in your suburb? Did you get a builder to inspect every single one?

My SPECULATION - more property investers spent the long weekend crunching XLs at home, figuring out how much money they will start to lose and whether they need to sell.

The market feels like it is turning and quite quickly. Whats interesting is most people probably suspected the lower end of the market that attracts investors would drop away first but the middle end properties, which typically attract owner occupiers upgrading are also failing to sell - north shore auctions last week was a good example of this.

I live in the hutt valley and noted that 2 lower hutt properties in the +1 Million mark were taken off the market and put up for rent instead (no I dont believe they sold both were available for rent immediately). There were also a number of properties in the 900K+ range that were taken off the market unsold and the auction clearnace rate was also pretty poor. Went to a second week open home this week again to a $1M + property in the hutt in a nice area and only 1 other couple was looking at it.

Are the "upgraders" now also taking a wait and see approach" or are they worried they wont be able to sell their current properties for a premium so are reluctant to overbid on a "upgraded" property.

That theory makes sense, as upgraders have the luxury of wait and see

These three properties sold on March 31. Before the tax change they would have been quite good buys as would have been immediately cash flow positive especially with a decent deposit. Now probably neutral.

4/38 Bertrand Road 780k

2/15 Marne Road 480k

52-O Pilkington Road 683k

Someone with a spare 480k in the bank might have been tempted with the Sandringham one. The return could be about 3.6%. Compared that to a term deposit. 17k compared to 5k. Would make a big difference to a pensioner.

Imagine paying $780,000 for a crusty old 7x7 meter cube in the vibrant suburb of Mt Wellington.

Three times the return of a term deposit and your capital keeps up with inflation though.

Looks quite nice for a little people farming unit. Low maintenance, nice kitchen and fast Internet to keep them amused.

What are the calculations you are using?

Have you contemplated what happens to your leveraged capital should the unthinkable happen and "negative growth" occurs?

Very rough, ballpark, calculations:

780k 12mths TD at 0.8% = $6,240 ($4,181 after tax)

$26,000 rent - $6000 costs = $20,000 ($13,400 after tax)

I would be inclined to contemplate the fact that the term deposits are declining in value while the property is keeping up with inflation.

These figures aren't great but they illustrate the term deposit/property dilemma which may be a driving force.

add principal repayments to your calcs....the same or similar cost for renting

add a declining market and see the numbers....a bloodbath...(dont forget the leverage works both ways)

add interest costs increasing...give me your keys!

Property was bought with cash. Some pensioner's life savings.

No evidence of a declining market yet.

I'm just illustrating that a property, even at that eye watering price, is still much better value than a term deposit.

and im sure tulips gave a better return than other investments at some point

Zach...only if property does not start falling and continue to do so for years. Just to be safe you might want to run your figures again but factor in a 10% PA drop for the next 5 years and a 1% PA interest rate increase for the next 5 as well. Better to be prepared for these real possibilities. I always like to look at best nd worst case scenarios and try to calculate the possibility of the various outcomes.

Just looking at what's happening right now. Mortgage rates could go down. They're lower in Canada I believe. It would be kind of absurd to factor in these things seriously.

I just think there is a connection between TD yields and property yields. The new tax rules will have mitigated it somewhat.

Zach...Why is it absurd? A year or so ago over 90%+ of people would have said it was absurd to suggest houses would increase 10% in 2020. If you had said 20% most would have said you were insane. And it happened. (incidentally I bought in March 2020).

Yes, mortgage rates could go down (who knows) but I would suggest that you are far more reluctant to discount scenarios that are a real possibility. I cannot tell you the chances of the possibilities I outlined (in my previous post) but what I can tell you is that the chances are much much higher than what you think.

Canada? The whole fabric of Canadian society has been destroyed by one man fixated on his self-image and virtue signalling grandstanding. Perversely the only winners in Canada have been the wealthy, and the poor whom he pretends to champion (again purely for self-image) are the ones his policies have hurt the most. And the most disturbing part of this is that we seem to have a PM that is almost modelling herself on him.

Mortgage rates will unlikely go down. GDP dropped, our productivity has been down, but we are out of recession. CPI is going up, inflation pressure is on the rise. Until housing price is under control, I highly doubt RBNZ will drop OCR again. This is as low as it could go until housing crisis is under control.

Why are you putting money in TDs? TDs are dead we all know this.

Use a dividend index fund, a better comparison.

Quite a lot of money in TDs currently. My dividend index fund seems to be getting hammered at the moment. A lot of people don't like shares, would go for TDs or property.

Fluffbunny...I have about 20% of my wealth in TDs and it is highly unlikely that you are either more financially literate or able to correctly assess risk than I am. Bob Jones recently stated he has significant funds in TDs. Maybe you should give Sir Bob Jones a call and help him out by explaining to him the errors of his ways.

Buy BTC and keep on renting, and keep tabs on the property market data heading into winter, HODL your deposit FHB. Careful on the roads there are some angry rent lords hurtling around the place.

How many bitcoins do you own frazz? I ask because people keep asking landlords how many properties they have. It would be in your interests to encourage people to buy BTC if you also owned it.

Ask me at the end of the year Zach - maybe we can makes some predictions on NZ house price movements and BTC price?

A better question would be how much as a % of thier total net worth.

Ie yeah I bought $200 of bitcoin with my stimulus cheque!

Vs yeah I just sold the house to buy just bitcoin baby!

Got our deposit ready to bowl some ground grubbers

Please stop treating housing as it is an investment that does not affect other people's lives in a negative way, we cannot continue ignoring this. If you want an investment that will give you profits higher than a deposit there are many other productive and speculative options available.

This is an article and comment section that discusses recent auction results. We are exploring what might be behind the high prices. Property investment remains a popular activity here and in many other countries. Certainly feel free to expand upon what may be better options.

Certainly this is a comment section from an article, that does not invalidate the point that housing should not be treated as an investment. Feel free to rebate my point.

I don't think your point is relevant to the discussion.

Thanks for confirming my point.

Humans have been ignoring this ever since the the beginning of organised society.

Not to say we can't do better, but there will always be land owners.

Feeling envious that someone else can afford it and you need to talk down on what others are buying?

Au contraire clown world, affording that dump is a piece of piss. That doesn't change the fact that its an overpriced dump in a crappy suburb of a crappy city.

Haha, “give that man some milk!”

For 1.2million you could own this dream home in Wellington 124 Brougham Street, Mount Victoria

My heart flutters.

Oh yeah found it:

https://www.tommys.co.nz/property/124-brougham-street-mount-victoria-60…

Looks like about 15 flats I lived in down there. To think that I could OWN it now!

You know it's the end of hope if you had to live in that.

I can almost feel the water gathering in my lungs....

Devastating results, owners should really dump the idea of going to auction for the time being.

I think around half selling at auction is a good result. I'm always uncomfortable when the sales rate is too high as it seems like a frenzy. 50% is about where it should be imho. 10% could possibly be described as devastating although I would use the term disappointing.

Last time we were getting results like this we saw a shift to asking prices, so most sellers won't agree with your opinion.

53% sold so more sold than didn't. Many will sell a few days later as well.

100% sold in Northland , 1 out of 1. I can also see the glass half full.

Help. Close friends are FHB's in Whangarei and have been trying to secure a home for 9m now. They are totally at the end of their rope and just want to get it done. They are making a pre-auction offer on a relatively new but uninspiring home on a slippy site. It's overpriced, everything's over priced. I've suggested waiting a month or so longer than 90 days (notice period) after labours announcement to at least get a feel for where this is sending the market.

Any thoughts anyone wants to share? My friend is the mum of an 18m old and is worried she'll get kicked out of her rental as a result of the same. It's a vicious cycle. I really feel for them!

A one-way flight to queensland is $300... just sayin.

Her husband is from Brisbane so don't even say it. Good friends are hard to find.

They should be able to find something for $9M, not central obviously, and frankly we dont want their kind of riffraff next door, but might find something out by Pokeno.

Is this the highest number of auction sales in weeks because less properties are selling prior to the auction? eg less buyers are offering crazy high prices to get it off the market prior to the auction. Or are buyers expecting far more than previously and are less people willing to offer those sort of prices prior to an auction?

I have noticed in my town, although there are far less properties on the market than usual, over the last few weeks some of those that were being sold by deadline sale, have failed to sell. I suspect there are a lot of speculative sellers, and they just remove them from the market , and try to resell in spring. During which time they probably expect their house to continue to earn 10k + per month.

With to tax washing, and a risk of interest rates clambering (ex global levers) one should think twice before jumping in.

Sales may be declined, but prices has been setup to skyrocketing up. No one can argue against this NZ housing cost. The excellent part, that many don't know about.. is that govt & RBNZ will ensure whatever they can to keep it on the steady path up even with varying angle up, but up nonetheless. Very little NZ economic academia, that reached Professorship level would argue against what constituted in NZ as F.I.RE economy.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.