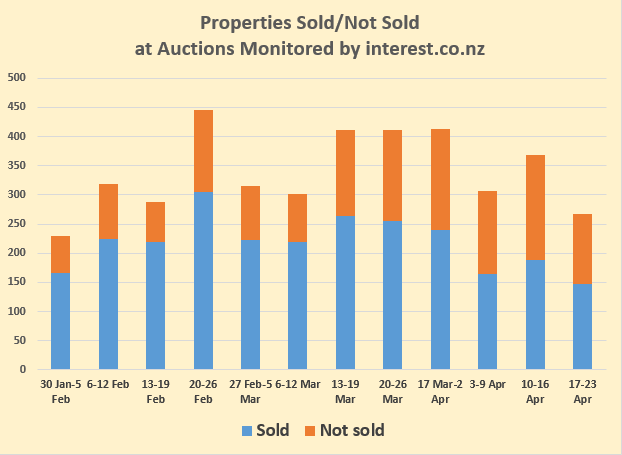

There was a sharp slowdown in activity at the residential property auctions monitored by interest.co.nz over the week of April 17-23.

There were just 267 properties offered at the auctions monitored by interest.co.nz over the week, down from 369 the previous week, which meant auction activity was at its lowest level since the first week of February when the market was just starting to spring back into life after the holiday break.

Of the 267 properties offered for sale, sales were achieved on 148 giving an overall sales rate of 55%.

That was broadly in line with the previous three weeks when the sales rates ranged from 51% to 58%.

However the sales rate has been in a more or less steady decline since it peaked at 76% in the week of 13-19 February.

The chart below shows both the trend in the number of properties being offered at auction and the numbers being sold or passed in each week since the end of January.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, go to our email sign up page, scroll down to option 6 to select the Property Newsletter, enter your email address and hit the Sign Me Up button.

76 Comments

Number of houses been sold are consistent compare to last few weeks but house prices that successful houses are been sold are still touching new high.

As heat goes out of the market the additional costs and some uncertainty will mean auctions become less preferred for vendors.

Currently some cooling but no indications (note “indications”) of any severe downturn: onset of winter season will be having some effect but still early days. This comment may indicate uncertainty but that is where things are currently.

No government in reality wants the house ponzi to stop. In any ponzi it is either up or down (no sideways), if touched and for this very reason neither government nor RBNZ are going after speculator and government timed their housing policy just before April for obvious reason and for this very obvious reason RBNZ is expected to announce just after April as both will be able to use April data which is normally soft, otherwise also to suit their narrative.

In short, the entire exercise is timed in such a way that are able to get away from taking any meaningful action to contain the ponzi.

Wait and Watch

Watch "Well, We Thought We Were Winning.... With Joe Wilkes" on YouTube

https://youtu.be/SYEFrJJK4wg

Listen at 3:45 someone (Martin North) let out an audible yawn as Joe fumbles on. Then Martin comes in having to update Wilkes

No video updates for 9 months since .... where is Wally??

Joe Wilkes used to be a regular commenter here, constantly and repeatedly warning about house price collapses in NZ 2 or 3 years ago... Listen to people who make correct predictions

Listen to people who make correct predictions

Like who? Ashley Church? Here's his predictions from 2020. Do a quick count and tell us how many your prophet got right out of eight. I can see 1 or 2.

https://www.oneroof.co.nz/news/national-back-in-charge-of-housing-my-8-…

Did you not realise there has been a pandemic, and a pandemic election that saved an all talk no action ardern. Thanks for reminding us of life before 2020

Thanks for reminding us of life before 2020

You should be thanking me for exposing the prophets and the fragility of the belief systems of middle NZ (which need predictions for guidance in the first place).

The belief system of investing in a new or existing residential property and over a period of time you pay off the mortgage, and match inflation has got to be better than the belief system you hold J.C. I know someone else who planned to build 100,000 homes over ten years, they havent got the nowse to pull it off but told us ten years ago to believe they had a plan which they didnt. So now they want to help others navigate the whole damn complicated RC system by bringing in a new even more wordy 3-part system but they say that will take 3 years of talkfest first until at least 2024. I know which belief system I prefer J.C.

The belief system of investing ....

Not what I'm talking about. If people want to invest in houses, by all means, they can pile in like there's tomorrow. I'm talking about something different. About how people look for self affirmation through others' predictions in the media. I'm also talking about how the media creates 'prophets' to feed those self affirmation needs of those people. The media's business model relies on this.

How about looking in the mirror and see your own faulty belief system. You seem to be all about critiquing others

How about looking in the mirror and see your own faulty belief system

I'm not an appointed prophet nor do I want to be one. My belief system is not based around chasing prophecies. If you think that people should based their decisions on forecasts printed in Granny Herald, that is your choice.

You both criticize and defend two people for making wrong predictions and the excuse you use for one might as well be applicable for the other, the main difference is one gets paid for it.

"tell us how many your prophet got right" What prophets ? You mention A Church, I certainly have never mentioned him, not now nor in the past

You mention A Church, I certainly have never mentioned him, not now nor in the past

So who are the prophets we should listen to? That was your advice (unless you were just trolling). AC is arguably one of the most prominent in the NZ media where most people lap up this stuff.

Listening to "prophets" seems to be your thing, it's not mine. I simply said listen to people who get most of their predictions right not the ones who are persistently wrong, based on that, you can make your own choice who you want to listen to, wether on this site or elsewhere

You're welcome to identify these people (if you're not trolling). Personally, I think 'prophets' such as AC are influential or else they wouldn't be sought out by the media.

Ad-hominem is not an uncommon practice by you and other commentators around here, BTW says someone that just a few posts after this says he/she was wrong.

40% LVR kicks in today. Should be interesting.

Most banks had already adopted the 40% much much ahead than today, so I doubt it will make much of a dent. Removing interest only though will be crucial to starting the leveling of this game.

100%. The government must level the playing field, banning the use of interest-only and top-up loans to fund additional properties.

As well as using existing equity towards an investment's deposit.

I don't see how this is workable, given the prevalence of revolving credit mortgages. What is equity and what is cash?

Revolving credit mortgages are also mortgages, issued based on the equity you have according to your current home valuation, if equity cannot be taken into account as a security that should answer your question.

No, it doesn't.

We have paid off our mortgage faster than necessary. So if we draw that down, it's from equity? But if we'd kept it as cash (paid the minimum on the mortgage) it'd be cash? Perverse incentives at the least. And that's not to mention just drawing down the equity and taking the cash to another bank.

Please don't take it personal since it is not. In your case what you did what was right of course, but you need to understand this is not about people that already own a house, many Kiwis are being pushed out just because their savings for which they work hard cannot grow as fast as equity, it is just fair to give them also a chance.

I understand the sentiment and don't necessarily object. I just don't see how it can practically be done. Are you proposing that anyone with any mortgage debt at all effectively has no cash?

Not sure I understand your question, but everyone would be able to hold any cash, actually that would be preferred if you want to get another property, since cash shows a real ability to save and hence face mortgage payments, using equity only just shows you made a good investment in a given period of time but it may pose a risk not for the buyer but the overall economy in a case of a downturn in housing prices even for a short period of time. Implementation should not be that hard, banks can take into account equity as security for a new mortgage, the idea is to not to allow recursive investments, this is you cannot buy get a loan to buy one asset using the increase in price of another instance of that asset family. Wouldn't it sound crazy you could get a loan if the asset in question would be Bitcoin? With housing we seem to have lost some perspective.

The problem is that you need a way to distinguish between cash and equity. With revolving credit there effectively isn't any. Transfer from your revolving credit (equity) to a cash account at the touch of a button. So how would you implement your proposed restrictions?

I would suggest that LVR +DTI could accomplish what you intend in a way which could actually be implemented.

b21 is correct, the bank holds a security over any revolving credit's maximum amount, even if the borrower has repaid it in full. This is generally secured by property. Likewise even if a mortgage is repaid in full, the bank still holds an interest over the property until such mortgage is dischargeded through the solicitors

It needs to happen to stamp out this behavior. Comment from a property FB page

“Looking for advice. Have had an interest only mortgage on a 2nd home as a rental for my daughter, and the bank is asking to pay principal payments as well. Is this mandatory or can we keep interest only payments for longer”.

And follow up comment from same poster

“Thanks for the advice. I don't know if it's right or not but here goes. It's to never pay off the principal ( it's cheaper than renting) and we gain on the value of the property as time goes by. Whether I gift it to my daughter later on or it helps us to buy another property to do the same. Thoughts please.”

I let him know that IRD will be wanting their capital gains share when he sells it based on his intentions

Albert, you might be outing on who you are and might be kicked out of the sacred group. The paranoid investors skim through all sites. IRD are useless anyways. Let me try find that article on how investors barely ever pay CGT or income tax or whatever name it is called and that IRD never chase it up.

Haha, I’ll take my chances. It does highlight how messed up our banking system is though.

Albert, this investor asks a good question, you threatening to dob him out to the IRD is nothing more than petty behaviour

It’s not a good question at all, it’s complete ignorance of basic lending requirements. And where do I ever imply that I will dob him into the IRD?

Exactly, this shows how luck has played a role in capital gains in the housing sector. The bank should have made sure this investor knew how the mortgage structure works but regardless, somebody taking an interest only loan that doesn't know principal must also be paid does not seem like a good target of wealth redistribution.

From Alberts comments, I didn’t see him threatening the investor or insinuate that he would dob him in but was merely giving advice that the investor was seeking.

"I let him know that IRD will be wanting their capital gains share when he sells it based on his intentions"

Yes Yvil, thank you but I still genuinely don’t see it as a threat. It is a just fact that he is pointing out.

Yvil if that’s your interpretation then that’s on you.

Yes it totally is.

Poor Albert, give him a break Yvil. His rental does not have a jacuzzi and he is not allowed to paint the walls psychedelic colours

No need HW2, your wife is more than generous with hers.

No that is just crass and weird.... but like I said you need a break

Interesting comment from the poster. The bank requesting principal payments may indicate that the banks have been told of forthcoming changes to interest only loans. When the RBA stepped in Australia’s interest only loans in 2017 a number of home owners were told they needed to start paying principal early. When this didn’t work they upped the interest only rate by .35% and told home owners they could keep their existing rates only if they started paying principal. It should also be noted that the Melbourne and Sydney house markets declined by 10% over the next 12 months

Hi all, I'm paying principal + interest on my 00 (mortgage is $440k) as well as P&I on my rental property (mortgage is $375k which is also the value of the property). Started this set up in March, rental is under an LTC. The rental SHOULD have been interest only, but the bank has made a mistake and its coming out P&I.

Q: Should I alert the bank to change the rental BACK to interest only...? It would be cash flow positive by about $5k a year if I did this and I'd be better off with those additional $$ hitting my 00 as a lump sum in 12 months?

I need to top up the rental by about $1500 per atm to pay principal+interest+rates+insurance.

Thoughts appreciated, please be gentle new to all this cheers...

Here's my thoughts: I don't think the bank has made a mistake.

Nzdan, I believe the mistake might have been having the residential interest rates for the IP. Should be 2.5 time OO rate and ofcourse with principal, that’s no mistake.

Passerby. Yes, the 40% has been applied for some time now but was often lowered for existing customers depending on their value to the bank. So it will perhaps have more impact than a 'dent', certainly so where buyers have maxed out their ability to tap the bank of mum and dad. NZ's migrant community is a significant player in the property frenzy in some of our larger metropolitan areas, including constituting a high ppn of mortgage brokers. Where their clients deposits fall short of the required threshold this is often bridged by money the buyer is able to source from others in their circle. The prediction of some senior people in lending circles is that this will continue, albeit for now higher amounts, resulting in not much change in activity levels for that group of property speculators. Time will tell.

Middleman, anything that will put a downward pressure on the property market is very welcome news. If the 40% kick off today helps with that then great.

I agree with the statement that migrants make a large group of property investors. I know personally of a migrant from years gone by, more than a decade. Husband and wife move to NZ, buy a home, have children, wife’s parents come to help out on a 1 year visa. In that time residency to bring parents were processed. The couple bought another property and now that the parent’s are permanent residents, they were eligible for dole and accomodation supplement. The supplement became rent and the parents lived off dole. The couple went back to work, children looked after by the couples parents. Within 2 years the sons parents are here, same story, another property with tax payer accomodation supplement. Before you know it they amassed a few properties. I don’t think he has paid much tax in life other than GST on household goods he has bought. Always claimed losses in his income. Never really contributed to the wider economy other than buying fancy cars and eating at restaurants. No daycare fees even. Now the children have grown up and starting uni, the couple are well retired with rent flooding in from all their “investments”. They own many rentals, housing NZ homes and recently bought a property near uni for their children as they are off to uni. Interest only, 4 beddy with 4 rents from students. He is planning to get a few more as he is cash positive. Pays peanuts in interest only and rents each bedroom near uni for $200.00. He moans and whines about tenants. Regrets not buying up motels so he could have rented it to the government and is beside himself with the tax announcements but already has accountants doing clever calculations to significantly reduce his tax obligations from moving property into parents names, children’s names etc etc etc. I know many other immigrants who are heavily into property investments. Sad world we live in when one cannot afford a home they desperately need and others can afford several houses they don’t need. We would be screaming if this happened with another basic human need like food but housing is fair game.

Passerby. Yes, the hard scrabble environments many immigrants come from make them adept at doing whatever it takes to maximise any advantage. A good thing if their efforts are directed to genuine value building entrepreneurial endeavour as some so successfully are, including creating additional new housing stock. But NZs social support and financial systems are wide open to the type of abuses you describe and compliance is so poorly monitored that we deserve to be ripped off. I chuckle at millennials (justifiably) ranting on forums such as this about greedy white boomers with multiple properties buying up large and thus excluding FHBrs from the market but the timid little luvvies tip toe around the other big bloc of property speculators currently active ie NZs immigrant community. Because it's, you know, just so racist to say that, isn't it. Ironically the extended nuclear family nature of our two main immigrant ethnicities and their greater willingness to pool family financial resources could see the ppn of properties acquired by them rise relative to generally more individualistic non migrant NZrs, as a result of the 40% rule.

Selling by auction is only one method of how agents sell.

It would also be helpful to know the % of properties taken to auction against the other forms like tender, exclusive, and general listings, and the % of sales achieved by those different methods.

Auctions original use was for those 'special' properties that benefited by selling by such methodology, and generally, a sale would result, ie a sale success of 95% plus.

The general push by agents over the years to get the vendor to pay the large auction budgets (with a large picture of the agent of course), and the lack of housing supply ie high demand has made almost all properties 'special' and 'worthy' of going to auction.

Yep, it's a system made by agents for agents.

In a hot market the vendors do well and the buyers get jerked around. In a cool market, the vendors get reamed and the buyers get a good buy. Either way, the agents get their money in 4 weeks.

I honestly expected clearance rates to drop well below 50%, I was wrong

You being wrong does not make it a less of a devastating clearance rate (50% is a psychological barrier but also arbitrary), taking into account how much it cost and long it takes to organize an auction compared to other methods of selling. You should also acknowledge you and others were wrong when kept saying the past trend would last forever, the market is in clear decline for the profit of most New Zealanders.

b21

“kept saying the past trend would last forever”

That is absolute rubbish - simply a desperate slag in an attempt to put others down.

Feel free to quote an example to the contrary as I am not aware of any such as Yvil who have been commenting on the property market making such a claim. “Property always goes up” is often posted by dgm as a pathetic slag off - it is not the words or a claim made by the likes of Yvil.

Those with experience of the market over considerable time know that is not the case. I for one have experienced three declines and have previously posted that an investment property purchased in 2006 received a RV in 2011 which was 10% lower.

At best you clearly do not understand when posters talk about short term fluctuations and long term trends.

You really love the "rubbish" word in your mouth. I can see my comment touched the right spot, happy to see that.

From canstar.co.nz "On the other hand, a low clearance rate around the 60% mark or below suggests buyer interest at auctions is low and house prices are in decline."

Well that's clearly incorrect, house prices are not only, not declining, they are at all time highs. They may or they may not decline in the future but we don't know this now.

The houses that sell might be fetching "all time high" prices, but what's the price of a house that doesn't sell?

Kinda like if one month nobody went out and bought $25k Corollas, and only a couple of people bought $150k Maseratis dragging the "average car price up", it doesn't make the Corollas worth $30k.

Canstar definition states 'suggests'.

Winning an auction means paying 10% of the purchase price on the day. Given that median house prices are still on the rise, there will be fewer buyers who have that sort of cash available for purchasing.

A lot of FHB's would be finding it increasingly difficult to do this, especially since you can't use KiwiSaver for the auction deposit, as you only receive those funds at settlement, and even investors who have predominantly leveraged existing equity still need to find that cash.

Article: What it's like to be renting for life by Kim Knight, feature writer, nz herald

What's the house like? "It's pretty bad," says Jaxon gravely "we don't have two toilets"

Is this reporting by Kim Knight, a late April fools joke??

https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12438923

Paywalled but I dont know why I pay for this moronic journalism

Read the whole article. It's quite sad. Jaxon is a child. He's probably comparing his house to his mates' houses.

' "Renting is where you have to keep on paying less money, but it stacks up to more" he says'

That's it in a nutshell, 5 percent return pays for the asset over 20 years without any change to the figures. Apparently said by an 8 year old who must have more brains than the majority of rent paying adults eh Mountie

The most interesting statistic over the next few years will be the % of mortgagee or other forced sales at auction.

If it ever gets above about 0.000002%, the RBNZ and government will jump in to save the day.

Even in worst of times ie gfc, NZ has disproportionately low levels or mortgagee sales.

Kiwis hang on to their house if at all possible rather than go mortgagee. I imagine this will happen again.

Mortgagee sales that do occur are unfortunately often pacific Island families forced to sell up after sending remits overseas particularly to pay for island funerals.

The expectation from relatives in the islands of their brethren in their own Kiwi home is unrealistic and the offshore family often think if they're wealthy enough to own a home, they should stump up for an all out week long funeral.

The pressure and shame not to do this is often too much for the kiwi based family to refuse. As a former insolvency advisor I saw this example many times.

The other big cause of mortgagee sales is unexpected health crises forcing unemployment.

Would not wish a mortgagee sale or economic environment or conditions leading to them on anyone.

Last week shows the lowest number of houses sold by auction in the whole trend. Auctions are no doubt looking less attractive now since it is a less competitive market. Many of those unsold will go by negotiation or set unrealistic high asking prices (and will take weeks to sell), just bear in mind sellers are still expecting prices from before reintroductions of LVR restrictions and tax changes, which is a massive change in the market and which you should not pay.

If there is a housing shortage then the season doesn’t matter. The data suggests many buyers are waking up to the overpriced rubbish that makes up most of the NZ housing market.

These results look pretty normal going into winter? Govt still stalling to take any meaningful action...

Have been contacted more often lately with details of silent sales (unlisted) and general trend of vendors wanting property snapped up quickly. Maybe some motivated by desire to cash before crash but beware if vendor intent is to keep window of opportunity so small that there is no time for due diligence to discover house has underlying issues but certainly has been the case where a 'cutie' or 'stunner' turn out to be a glittery turd- chronic leakage, rot, earthquake damaged, house by bush built over 2x storm water culverts. Regarding auctions of course less sales will happen that way as auctions make glaringly obvious the FOOP

The peak of mania has passed.

Question now is how long til bill comes due.

The bill being for all the additional debt taken on by RBNZ, government and private citizens to buy property with no extra income generated to service that debt.

Prices we know will slow and sales too, but no figures to fairly compare to in 2020, for April and May

So really will not know much til mid July, when June REINZ comes out.

meanwhile, auctions will continue to decline as a method of sale, in % terms

For the last couple of weeks I've been looking for a small apartment in central Auckland. It does feel like there is some weakness in the market, but nothing extreme. It's hard to know how much is due to recent legislation changes and how much is caused by the reduced number of foreign students. Probably the interest deductibility changes are having limited impact on demand for very small apartments because banks are reluctant to lend on those anyway.

Tax change will have some effect but the real change that is in waiting is change in interest only loan as stopping it will directly target speculators unlike tax change which has affected more investors than speculators as speculators are not in for long term and will speculate accordingly unless their multiple buying source - IO loan is contained.

True Intent of government and RBNZ will be out soon.

Does having a 40 percent deposit, whether cash or equity, make any difference to the debt servicing equation. Less debt overall must mean more excess ability to service the loan principal surely. That is also a principle!

The retired couple we bought our house from (offered in December, settled in February), are still renting and looking for a place to buy.

They had a place on the cards when they were selling but the purchase fell through. Don't know why. They've tried to buy 2 other properties since then, both at auction, and lost both to buyers who were willing to pay silly money.

Being retired, it seems the most they want to get on finance is 300k, to add to the 700k they got off us, but a $1 million just doesn't buy what it used to.

Heck. They probably couldn't even buy their old house back off us for that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.