The housing market is continuing to slowly lose steam, according to CoreLogic's latest House Price Index figures.

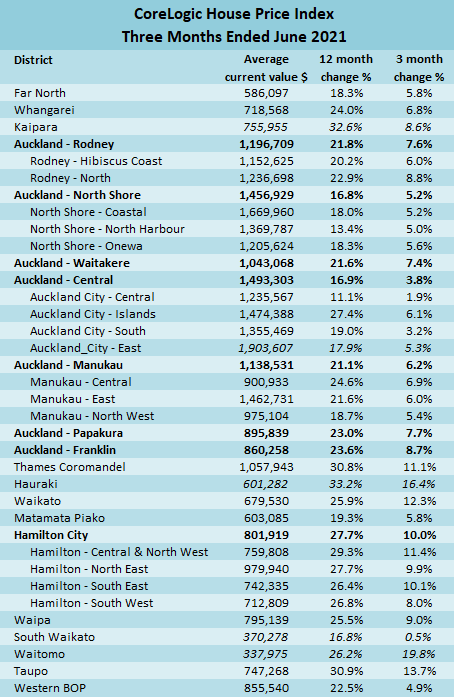

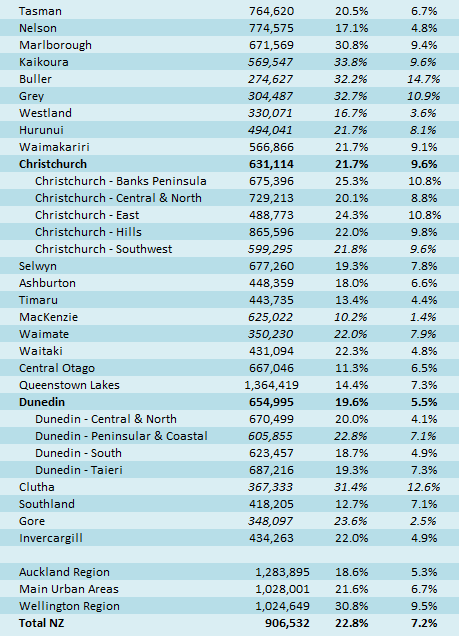

CoreLogic's figures show average dwelling values are still rising, with the average value of all New Zealand homes hitting $906,532 in June, the first time it has been above $900,000. That's up 22.8% from June last year.

However the rate at which values are rising is declining, from 2.2% in May to 1.8% in June.

"The rate of growth in June slowed in 12 of New Zealand's 18 largest markets," CoreLogic's Head of Research Nick Goodall said.

"The exceptional growth displayed during the past year was not sustainable, particularly with increased deposit requirements, market uncertainty driven by government regulation and the prospect of higher interest rates.

"The turnaround should perhaps not be too much of a surprise, though the timing of it certainly is," he said.

The latest figures suggest the housing market is a bit like a train pulling into a station - it is still going forward but is slowing considerably as it approaches the platform.

June also set another record, with the total value of all NZ residential properties passing $1.5 trillion for the first time.

"These milestones will not necessarily be welcomed by all, especially hopeful first home buyers," Goodall said.

"However the tentative signs of change may provide some hope for would-be home buyers as well as the Government, who are under pressure to tilt the market in favour of new market entrants," he said.

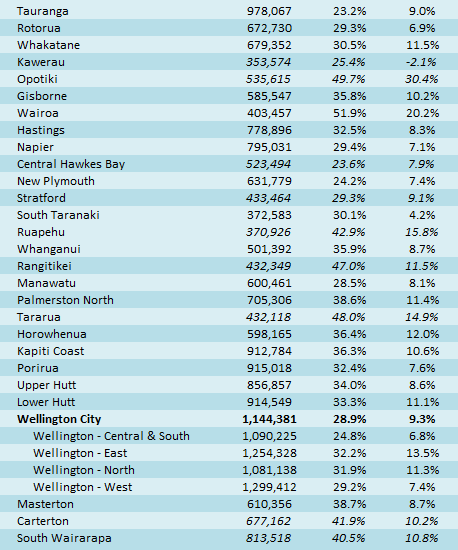

The table below shows the average value of residential properties in all major urban districts throughout the country and their percentage change over three and 12 months.

The comment stream on this story is now closed.

62 Comments

Still wait and watch approach even as all data / news suggests that whatever RBNZ and Government has done so far is not having any effect.....still..... supporting and promoting housing ponzi.

An anyone economist or experts decline ....

by Cowpat | 4th May 21, 4:38pm

"Wishing Mr Orr a speedy recovery as Mr Bascand takes the reins for tomorrows FSR. If a country the size of New Zealand has 1.5 trillion NZD in apparent housing wealth( excluding vacant land) does that have a destabilizing effect whether it falls over or not."

"The latest figures suggest the housing market is a bit like a train pulling into a station - it is still going forward but is slowing considerably as it approaches the platform."

This train has left the tracks...

More to the point - which direction will it go after it stops at the station?

Run backwards down the hill with passengers scrambling to escape or move forward to utopia as they comfortably sip chardonnay in premium class?

Hi Nifty,

The train has been more akin to a rocket-ship the last year or so.

Property markets are cyclical: a slowing down is inevitable.

TTP

it is not a market anymore, you forgot?

It isn't a market, its basically the NZ economy. Houses are making the owner about $10k a month in tax free capital gains, more than most people make working full time. When the PM said house prices can't keep going up like they have been, she was right, it had only gotten worse. The problem is a lack of inventory and cheap money pushing up prices. We should have enough actual houses, but to many are left empty or used a weekenders or airbnbs, to supply the capital gains the owners make tax free. It is a rort

I have just the checked the latest values for all our children’s houses and ours. The market is insane. Where are you Jacinda? Are you actually working? You are certainly are not dealing with poverty issues. Oh you own a house in Auckland. Let the market run.

Higher house prices are the price we have to pay for keeping Covid out of NZ.

Don't knock Jacinda and Adrian too much. Being Covid-free is a hugely important achievement.

I'm a renter - and destined to stay that way. But I'm very content with the way Covid's been handled in this country.

Some people here put a huge value on house ownership. Certainly it brings benefits. But there's a great deal more to life than property.

TTP

A house owned is a stable home, no risk of being kicked it, no inspections, plus some retirement security. The ability to downsize and have some financial freedom. There are other ways to invest your money for sure, but housing is and always will be a safe easy way to secure your future. I for one do not want to be 60 and still moving around as a renter

Here we go again. The great scapegoat called COVID. The convenient event that every politician and banker can blame for the absolute balls-u they have made of running the show.

The scene was set well before COVID came along.

TTP, I may be misremembering, but I seem to recall from previous comments here that you have owned property in the past, or own investment property, or possibly both - is that right?

The reason I ask is that there is a big difference between someone who has already made a lot of money in property in the past and is currently making a choice to rent when they could pretty easily buy somewhere if they wished, and a typical first home buyer.

He is the chairman of a certain real estate agency.

Just between you and me, TTP. Most property investors I know quietly support Labour. Jacinda has them in her pocket. As you know she's pretty savvy, is our PM.

Wellington's prices have gone up 30+ % not because of any politician but because of the present rort that real estate agents have got going here, aka tendering. It's by far the most predominant real estate practice and exploits FOMO big time. When I bought my house 15 years ago, it was a tender. Horrible practice.

But they could also drop in price. Someone actually has to be willing to pay that amount, in order to realise that value, and in bad times houses can be difficult to sell. These rising prices hinder home owners because it means if they move, but they want to upsize, they are likely going to need to get an even larger mortgage.

No surprises. There's still much room for upward valuation.

Waiting is costing you dearly.

Be quick.

Stupid daily FOMO comment.

Are you even thinking about what you write or are you just being told what to do? Increases in interest rates are here, they will have the exact opposite effect as when they went down.

The entire economy of this clown country is built on perpetually increasing house prices and very little else.

It's a centrally planned economy with centrally planned house prices and particularly vile people in control. They will not permit them to fall in nominal terms. Period. They will allow the NZD to depreciate rapidly when economic reality forces their hand. Don't hold it.

It's not fair and it's not right but it's the way this joke of a country is and nothing is going to change. It's time to accept this and move on.

If you plan on owning for 5-10 years and plan and budget for that period, it is still a good time to buy today! Constantly being negative and waiting for a "bubble to burst" will cost you more in the long run. Exactly the same with the stock market - time in the market always beats timing the market.

Thank you for your unsolicited FOMO advice. Please highlight the points where I am being negative about falling prices. This would be the very best thing it could happen to this country! Of course, some mistake negativity with whatever goes in their own selfish interests.

I've listened to enough of it over the years, it stopped me buying a property in 2014, as everyone was talking about another "crash." Biggest mistake I've made. Every purchase I make now is for long term gain and I just ignore all the negative nancies on the sidelines, like yourself.

I have to agree with you. My father thought the bubble would burst in 2006 and talked me into waiting another another year and I watched housing in my area go up by 40%. In other words my cash in the bank dropped in value by 40%.

Might need longer than 5 years. 2016 was the last time house prices went ballistic, and certain categories of buyers were pouring money into housing and overpaying for property by several hundred thousand dollars. Now those buyers are selling, and in the case of one vendor at auction today, they found that the house they paid $900k for in 2016 only managed to sell for $960k, which would be a big loss if they were paying interest on a mortgage. Oh, and the reason for selling? "The vendor cannot get back into the country" LOL.

Whats the address of the auctioned property?

Genuine question, are you a bot?

20 X median household income

I m telling ya.

You may be right. NZ and HK have identical town planning and similar housing dynamics.

20x is absolutely within reach for us.

You make it sounds like a goal, a target, that if we work together on, we can achieve.

Good to still have 3 earners in the the household - me, wife & the house.

Yeah but you know something is wrong when the house is earning more than you and wife combined.

The contrary. I see houses going up as the opposite to being an earner.

Every rise is a step closer to economic and social breakdown - and its happening right before your eyes.

You are earning nothing, you are going backwards (just not as fast as the non asset owners)

If you are so confident shouldn't you quit your jobs and live off the capital gains?

Cos cap gains in your house are not cashflow.

Pretty disappointed my place only went up 1.05% last month so that's only $10K according to OneRoof. Going to have to cut back on the champagne and the caviar.

Hi Carlos,

Sorry to hear that poverty is closing in on you.

TTP

If only you could take your valuation into the supermarket to buy the groceries...NZ make up will be

55% Asset rich cash poor

40% Just Cash poor..no assets

5% Asset Rich Cash rich.

Labour have really balanced out the poverty..NOT

Who cares about groceries, You take your valuation into your bank and they give you the money to buy a new car on the house. Rack up that debt baby, go you good thing.

You are joking here, the problem is that the media and housing lobby are making people believe this is true and we'll be in trouble when they realize there is just as much they can buy with unrealized capital gains, which will never materialize if they still want a home to live in.

Did exactly that! Our car loan portion of the mortgage is sitting on a lower interest rate than the rest of the house.

Fortunately our DTI is still less than 2.

1.5 trillion in housing wealth ( excluding vacant land) and New Zealand struggles with issues related to poverty.

Interesting, REINZ data was giving falls of -3% in the past couple of months in areas where Colelogic gives +5% increases.

Different data bases and the implications as discussed many times on this site.

This CoreLogic data will include considerable number of sales where the sale and purchase agreement were entered into prior to Government's 23 March announcement.

Perfectly aware of this, just highlighting the level of accuracy of the data we have available. Disclaimers should be placed next to a headline like this.

b21

Not about accuracy at all.

Both are based on large pools of data and will be accurate on the basis of that data.

However, CoreLogic data is dated compared to the more timely NZEIR.

I am not sure which specific data you are referring to in your original post. However, rather than being about accuracy; CoreLogic data is based on registered sales which includes agreements made prior to Government's announcements and onset of winter, whereas REINZ is heavily weighted to include agreements made after those factors became significant.

Rather than being about accuracy, the difference is more likely about a cooling of the market.

Yes, one needs to be careful as to what is asserted, but the CoreLogic conclusion and the headline seem appropriate.

A slowing increase is still an increase.

Prices are still rising.

And there's still no real reason to think rates will go up -- with every passing month it gets *less* rather than *more* likely, as the mountain of vulnerable debt grows. More warnings might be issued, to join the dozens of previous warnings which are now completely ignored by the market. No one *really* believes rates will go up, so a million-dollar shack that barely pays its own way still looks like a good investment to the average schlub.

With every passing month of more inflation on top of inflation, we are defiantly heading for interest rate rises. This is not an event that is transitionary or we can simply see through if it keeps rising and then doesn't fall again. The slower this is delt with the greater the pain down the track. Its out of control already and those that can do something about it are like a possum in the headlights.

The CPI rises are still modest. And yes, CPI as a measure is cooked, but that's what they use.

And I think the central bankers may be right that supply chains will readjust and commodity prices flatten out -- demand has been dragged forward by stimulus.

Of course I might be wrong, but I think the bigger picture is still more deflationary than inflationary. And that massive pile of mortgage debt is one of the deflationary factors.

This whole car-crash of a housing-based economy has trundled along much longer than I had imagined it could -- as far as I can see, nothing has really changed except a slight rise in CPI, so why would it stop now?

Housing markets don't slowly lose steam, the data catchup is slow to compile. Housing markets are every bit as irrational as their owners.

Jacindas and Robertson's legacy. Wow indeed.

Today the house down the road from me sold for a 45% increase on what it was purchased for a mere 13 months ago. It was in exactly the same condition as purchased. You think prices are slowing down? I'm not seeing it.

The medium hourly wage in NZ is currently $25.50 according to google. So with the medium Auckland house price at $1.12 million that represents 21.5 times annual income.

Sustainable??

Unfortunately the answer is yes. There has been a total disconnect between wages and house prices for decades. The very fact that houses are still selling should tell you its sustainable. Obviously there is an upper limit and it has to be very close now and prices simply have to flatten out, its not possible to have another 30% gain over the next 12 months....is it ?

Had a look at homes July 1 new estimate valuations and f me it really has gone insane.

It has my place valued at a min of 200k above what we paid for it at the end of last year. At the time if purchase I thought even if it was flat to slightly declining I’d still be happy as it was such a considerable discount to own compared to paying rent. Well if the new vals are accurate it really does seem to be over inflated.

Wow yes just checked myself, even the minimum price just clicked over the $1M. Well I did say it would hit this by Christmas. Same timing bought September 2020 and its up $200K. Vals are all relative, compared to rot boxes in Auckland mine is a bargain. However, we are so going to get spanked with rates increases in the new July 2021 valuations.

Increases in house prices have no effect on the calculation of rates, unless that increase is a result of something very specific to your house and not the houses around it (eg. rezoning, renovation, extension etc).

Its been so good for so long with every lever pulled in its favor (rates, immigration, foreign capital, money laundering, dysfunctional supply and council, scared govts, tax treatment etc etc). So long and so good that the true believers are cult like in their conviction that it can only continue to go one way.

Math's, long term stats, and logic suggests otherwise for some time, but gotta say it like housing speculation is protected by an anti gravity machine.

Prices likely to go up if fiat is your denominator.

Consider changing your denominator to Bitcoin.

I expect house prices will continue to drop drastically over the next 10 years denominated in Bitcoin.

Obviously with volatility on the route.

Cheers.

The Reserve Bank need to remove these emergency low interest rates urgently. When we only have 14k houses for sale in the entire country, down from 60k a decade ago, the limited inventory and low interest rates are hiking up prices. With real world inflation increasing, there is no need for them to be so artificially low

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.