There was a small decline in Barfoot & Thompson's auction activity in the second week of November (6-12 November), with the number of properties auctioned and the sales rate both taking a small dip.

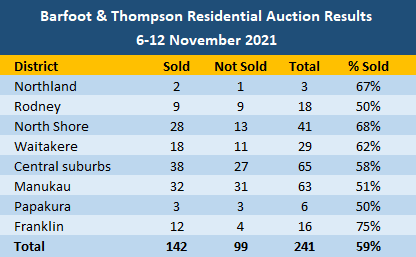

Auckland's biggest real estate agency took 241 residential properties to auction last week, down slightly from 250 the previous week.

Of the 241 properties offered, 142 were sold under the hammer, down from 156 the previous week.

That pushed the overall sales rate down to 59% from 62% the previous week.

The sales rates were weakest for properties in Rodney, Manukau and Papakura, where about half the properties offered sold under the hammer.

Within the Auckland region the sales rates were highest in Franklin on Auckland's southern edge at 75%, and on the North Shore at 68% (see table below for the full district results).

In the equivalent week of last year, Barfoot & Thompson took 291 residential properties to auction and sold 175 of them, giving an overall sales rate of 60%.

Details of the individual properties offered at the auctions monitored by interest.co.nz and the results achieved are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register (it's free) and when approved you can select any of our free email newsletters.

12 Comments

Where are the DGMs at?

They've gone. That's all that matters.

TTP

Banks getting tough down country too TTP ?

....moved onto cryptocurrencies :) ......bye bye residential property investment in Auckland anyway.

When are people going to sell? Isn't this meant to be peak selling season, what is everyone waiting for?

I suspect everyone is awaiting AL2..

Everyone holding on to avoid pay tax on the gain. A gain that until they sell is speculative. A lot of 12 month fixed loans due to role off in the next 12 months. Headwinds building with DTI on the runway ready for takeoff. Will they make the new lending targets when they have to refix...?

The historical tax status of housing, and RBNZ inaction has caused this mess.

If it's owner occupied property there's no implication on tax right... Not everyone's a property investor.

Averageman

You sound as though you feel a little sorry for investors or is it just wishful envy?

I wouldn't be too concerned about investors if I was you . . especially as you have a few weak assumptions there.

- Any new DTI requirements won't apply tp rolling over an existing mortgage rate and term as it is not a new mortgage - a new mortgage is when a mortgage is first registered against a property and simply relates to the lender having an interest in the property and the terms of the mortgage (such as time, amount and interest rate) and are not included in that registration. It would only likely be new lending subject to DTI if there was a wish to increase the amount of the principal.

- I wouldn't worry about tax if they are liable; a $99,000 tax bill on $300,000 CG over the past couple of years or so still leaves a healthy $210,000 in the pocket (plus yield)

- Rather than waiting to avoid tax - for those purchasing prior to March the BLT is only 2 to 5 years and the vast majority have owned property for longer than that. For those who a CG is the important factor could be thinking now is a good time to lock that in as the market is likely at best flattening or possibly show some correction in which the correction could well be larger than the tax.

The reality is that the property party is fast becoming to be over, however those who had investment properties over the last few years or so have done exceptionally well and will be very pleased.

The lower number of properties going to auction is likely to be a reflection of the change in the market . . . . auctions are preferred when the market is either hot or significantly falling. In these cases there is price uncertainty and vendors want to test the market. Auctions have additional costs and risks if the property doesn't sell; with the likely cooling of the market, there is going to see more properties marketed "by negiotation" rather than auction.

The old wishful envy line...Im good but I may have been good to buy some crypto...

I agree the debt stack tax rinse party is over. I just wish they would get on with the inevitable asset reset, bankrupt those that need it, remove the risk from the banking sector, and let everyone else get on their merry way. I do however disagree on your DTI statement. It should apply to all loans at the end of their current fix period. Lets see what future announcements bring?

Looks pretty steady to me all things considered when looking at Auckland. I still think its last gasp time for the NZ property market this summer. The only thing left to pump it now is the resumption of immigration. Open the gates and let another 100,000 into Auckland in the first year, that will fix it.

That's what I call a free market- a market that continuously searches for the demand and supply equilibrium.

A sales rate at 58.9% is a sign of a healthy market.

Unless people are expecting a major all encompassing deflationary environment, waiting for price falls to enter is a bad strategy.

There's still room for upward valuation.

Be quick!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.