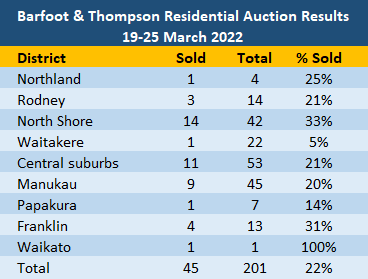

There was a slight lift in activity at Barfoot & Thompson's auction rooms over the last week (19-25 March), with Auckland's biggest real estate agency auctioning 201 residential properties for auction, up from 181 the previous week.

The number of properties sold also increased, to 45 from 38 the previous week.

That left the overall sales rate almost unchanged at 22% compared to 21%.

The sales rate was particularly low for properties in west Auckland, with sales achieved on just 5% of the Waitakere properties on offer.

Properties on the North Shore had the highest sales rate in Auckland at 33% (see the table below for the full district-by-district results).

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

104 Comments

Looks about right to me, the less desirable places to live are taking a dive. Not even an opening bid on similar properties down here in Tauranga but the more expensive areas that are "giant rest homes" for those with $1.5m are still selling with the retired money heading south. "Rental" type properties are trying to bail out of the market. Overall its hit a brick wall, just to much uncertainty with interest rates and the war. Sellers still wanting top dollar on properties I'm looking to buy.

Still picking small gains for Tauranga this year Carlos?

Its looking that way but only for my house cos its speshul

A "flat market" is exactly that - flat. Just as expected after a lengthy period of buoyant trading.

The DGM are attempting to mislead and deceive us (as usual)....... The housing market is not "nose-diving", "tanking" or "collapsing" - it is too resilient for any such outcome.

Rather, a soft-landing is now underway.

TTP

Save your tears Tim. You’ll need them.

Soft is an understatement. What we have here is limp, flaccid and dying 🥀.

In kiwi parlance, the housing market is goneburger 🍔❌ and the phoney economy is likely to follow 💥.

Astute minds are now asking what kind of career and life they could have in proper first world countries like Australia 🦘 or the United Kingdom 👑 for the same price as a dump in Ranui 🤢.

The bleak financial outlook and promise of racist "co-governance" will make the choice pretty clear for most skilled professionals ✅ ✈️.

People such as Brock Landers, Retired-Poppy and DDDDebt are extremists. They fail to contribute well-reasoned, measured comments here.

Rather, they attempt to fabricate that there is a crisis in the housing market - to induce people to sell houses, en-masse.

Seasoned house owners can easily see through their biased thinking and related mischief.

Those who are less experienced with the housing market should be extremely cautious. Take advice from someone who you can really trust: perhaps a parent, grandparent, registered financial advisor, or family lawyer/accountant. Also, be very weary of real estate agents...... Otherwise, you risk being duped.

TTP

"Seasoned house owners can see easily through their biased thinking and related mischief"

Seasoned house owners want prices to fall. 77% of kiwi's do, because they know that we've engineered a housing crisis that is causing major societal harm and no opportunity for the next generation.

https://www.1news.co.nz/2022/01/31/three-quarters-of-kiwis-want-house-p…

It's only those with heavily biased interests like you that are trying to stop the market falling to more affordable levels. It's out of your control Tim, unless you are the one that sets interest rates and the cost of debt - the basis of affordability.

Sadly, too many people were duped by property industry leaders like you and muppets like Ashley Church who said in mainstream media that interest rates are going to stay low for 20 years. They were at emergency levels FFS.

Now they're emailing him in panic asking him what to do. His response - "I’m not a certified financial adviser and my commentary tends to be at the macro, rather than micro, level"

What he should be saying is 'sorry, i'm just paid to pump the market'

https://www.oneroof.co.nz/news/ashley-church-four-ways-to-beat-housing-…

Those less experienced need to understand why we are in this situation. It is not unique, it has happened before. In time, it will be written about here to.

https://www.researchgate.net/publication/263725836_The_Role_of_the_Medi…

The Ireland paper is a very nice catch, thanks.

I used to keep mentioning Ireland to peps stating how safe are properties. I always been told that #NZ-is-different.

I only hope people will be burned enough to remember, this time.

Side note... somebody keep indicating people that believe we reached a mathematical limit as DGM.

I believe that Doom and Gloom are results of an overinflated cost of a primary necessity.

The ones cheering for higher house prices are the real DGMs.

No probs Lucenera

The Ireland paper is a heavy read, complex, political, but references well the vested corporate influence on mainstream press in ultimately helping create the bubble that burst. The simple takeaway being:

"It is shown that prior to the bubble's collapse, the media made little mention of it, remained vague about it or tried to refute claims that it even existed, thus sustaining it"

Does that sound familiar?... or somewhat mild compared to our situation.

Our supercharged example is this: Oneroof is the property platform of NZME. NZME also own NZ Herald, NZ's most read News app.

Have you ever noticed how every day two (in 2020 it was three) pro property Oneroof articles appear in the top 30 of articles of your herald app?

Ashley Church provides the bulk of the stories refuting claims of a bubble, crisis or impending crash. Everything he says is to pump the market to greater heights.

"If I look back over my various OneRoof articles over the past few years, it’s apparent that a sizeable proportion of them are about the possibility of a housing market crash – or, more accurately, me responding to claims that a crash is imminent by reassuring readers that it isn’t"

"For all of these reasons, while it’s likely that the end of mortgage interest rate drops will slow house price inflation in the future, it’s not likely to happen any time soon. In my opinion, it could be as long as 20 years before we start to see any impact from this change in market conditions"

https://www.oneroof.co.nz/news/ashley-church-if-mortgage-rates-hit-zero…

"One thing is certain though. Mortgage interest rates are going to stay lower, for longer. Of that, we can be quite certain"

https://www.oneroof.co.nz/news/ashley-church-could-mortgage-interest-ra…

https://www.oneroof.co.nz/news/search/Ashley%20church

Oh, yes, there are so many similarities that is almost hilarious.

It is a very interesting read indeed.

I could understand (even with immense disappointment) that there is a specific agenda in trying to pump the housing market, or at least now to avoid panic selling.

What I don't get is how is it possible to defy pretty the simple maths that screams what is going to happen. I mean, how can people still believe in those bs?

I guess is me being naive... maybe, but in my world 2+2 is still 4

In the United States, one empirical study found that in the years prior to the crisis, the American media can be described as ‘the watchdog that didn’t bark’ since ‘the business press institutionally lost whatever taste it had for head-on investigations of core practices of powerful institutions’ (Harber 2009; Starkman 2009: 30)

That's the quote that stood out for me.

-> move away from investigative journalism to tabloidisation.

Checked out your stuff news feed recently?

Married at first sight this.. Little baby Jacinda that...

Be wary of convicted price fixing estate agents especially.

The very definition of price fixing is that multiple companies are doing it. It wasn't just Property Brokers.

Real Estate Agents are supposed to work for the vendor, but they also pretend to work for the buyer. But they actually work for themselves. Use that fact to your advantage.

22% not good you would get a big F in any exam. Just looks like housing market is tumbling and interest rates are still close to emergency levels. Anyone can see we are going back in time with this market maybe around 2016 so big drops deposit lost and negative equity for anyone who purchased in last 5 years. Investors and speculators will be wiped out this is why they are so upset but they must of made huge amounts on way up the smart ones left the market last November.

Another way to gauge what TTP Tim Mordaunt is panicking about is to simply listen to his Property Brokers radio advertisements. This will be painful. You will notice the connection with the comment section.

The benefits of price falls are already happening.

One family member who has start up is reinvesting heavily in the business, now relaxed that he will enter housing when it suits him - growing a business without fomo and so on, housing just being something he will do when ready and no big deal.

This is how an economy grows......not the BS of flipping houses like we are used to.

Thats what I like to hear, that's the way to grow NZ, and hopefully themselves.

New Zealand would be so much better if we rewarded this entrepreneurial type of person rather than folk just sitting around on their ass-ets.

Please tell us your on the next flight out of here. You do know we all see through your rubbish comments and it's clear your either very inexperienced or just a negative person. Either way anyone who actually listens to you should seek a second opinion

It always helps to know the difference between "your" and "you're" when you're trying to dismiss the wisdom of others.

Otherwise you end up looking like you're referencing your IQ in your username.

And he's a repeat offender.

As it turns out the people that keep banging on about spelling here are the ones least satisfied with life. You have made several along the way Brock but I cannot be bothered pointing them out as its totally irrelevant to the opinions presented. If you want I can start picking on your posts here and you will be forced to put every word through the likes of Grammarly and cut and paste it across, which would be pretty tedious I should imagine.

Hi Carlos, correct spelling and grammar are extra important to shore up credibility when you are launching personal attacks on other commenters whose opinions may have rubbed you the wrong way.

Most of us do our best to avoid such behaviour as it's not very nice to pick on simple people unless they are really misbehaving.

While we are on the subject though, if you could put your posts through Grammarly before inflicting them on us it would be absolutely splendid.

important to shore up credibility when you are launching personal attacks on other commenters whose opinions may have rubbed you the wrong way.

Try and do that then Brock

House mouse, same clap for you repeat offender.... Really, Walk on boy.

BL well done on pointing out that my grammar is not that great, slow clap for you. If that's all you have jog on boy.

Hi Luke,

Here is a tip to help you achieve the greatest success in life. Get your spelling and grammar in order. Nobody is going to take your intelligence or your competence seriously if you continue advertising that you haven't even been able to master the English language. We can work together on the rest of your issues later, but this one is foundational.

Cheerio.

BL, you are a keyboard warrior who needs to realise that the people you target in here couldn't care less if you never commented again. I do very well for myself and my family and don't go without. Thanks I'll have to turn down your offer as whilst I'm sure you can spell, your life clearly sucks.

Hi Luke,

Nobody targeted you. You just got triggered about the thought of skilled professionals moving abroad. I would recommend reading the scroll back so you can figure out who launched into the personal attacks.

Or just look in the mirror if you're too illiterate to achieve even that.

Whilst not wanting to be drawn into this futile debate, I would like to reassure any would be contributors that I personally value the content of their argument far more than the quality of their spelling and punctuation. There are many successful people who left school at 15 due to dyslexia and then went on to prove themselves through business. Not being proficient with the written word is no indication of overall intelligence or good judgement.

"The housing market is not "nose-diving", "tanking" or "collapsing" - it is too resilient for any such outcome"

Said everyone soiling themselves with a vested interest. Every RE agent, broker, banker, developer, residential builder, property market ticket clipper.

The property industry has given up on the narrative that prices don't go down, so is now trying to engineer the narrative of a 10% correction followed by a flat market - a soft landing, as this is their ideal scenario.

But do you REALLY think that's going to happen? You wouldn't if you stopped thinking like the boomer mega-millionaire mega-landlord that you are.

Think about the market from the average FHBs perspective... someone under 40.

They simply can't afford to pay the ridiculous prices any more... because mortgage costs are going to at minimum double, or triple, and possibly quadruple if rates go to 8% like they were when we last tried to control inflation just over a decade ago - if you took out 1.99% rate specials.

No one knows what's coming, but all bets are on that it's going to get very ugly for those who put all their eggs in the property basket.

"engineer the narrative of a 10% correction"

Spruikers cannot see past their front gates. Little do they realise that as interest rates normalise, Central Banks will be the ones to blame for heal dragging in response to this inflation surge. Under the weight of increasing interest rates, house prices will likely fall 10% each year for say the next three years. This is unlikely to play out over the remainder of 2022. When adjusted for inflation, in the end, it could equate to a fall of 50%! In the 70s it was 40%...😭 Still some Evangelical Muppets will argue it as a soft landing (for those who bought 15 years ago that is) 😳

heal dragging

Dont you mean heel dragging, there is no such thing as what you wrote

"Imagine" someone referring to 'high heals' lol

This market is no more, it has ceased to be, it has shuffled off its mortal coil and gone to meet its maker….. this is an Ex market. You are misleading yourself. Any non biased objective analysis of the current situation would lead to the conclusion that now is not the time to be buying a house.

The property market can't tank. Not with COVID, inflation, war and security. Most of all, there are people who are not hedged for a reversal.

Let's see. A lot of debt is rolling over from record lows this year, and rates could be as high as 7-8% by the end of the year. Inflation will continue to hammer people's ability to save a deposit.

All adds up to most buyers being unable to touch last year's prices even if they want to.

The interest payments are the killer. A graph that Stuff posts shows that deposit weeks has actually come down for the first time in years, while fortnightly payments has shot right up. A new record.

For people who suggest it's a balancing act between falling prices and rising interest rates, it's really not. Both together send a clear message: Stay away from housing for as long as you can. It's the opposite scenario to rising prices and falling interest rates, where the winning strategy is buying earlier. Which sort of explains the FOMO. It also explains the reverse FOMO (or FOOP) that will occur.

The property market can't tank? You're kidding right?

He is joking. It already is Tanking. We are galloping towards a -30% Crash in home prices this year. RE Agents and Media already reporting 15-19% price reductions. 7% interest rates will be here this year.

Dunedin is in standoff mode, I heard yesterday of someone buying 50k under the asking price and the house wasn’t a dump.

I would not be buying anything at all. People who wait will be rewarded. You can literally save thousands of dollars per week by doing absolutely nothing. Here is a good overview of what is going on.

Will Martin North finally be right? It's been a long time coming.

Bloody love Martin

Some facts out of Welly from Lowe and Co. Prices soft, the most listings since 2015... https://youtu.be/XwQgHZJqkIc

Heard this before, if your buying to reno and sell its dangerous times, if your buying to get in the market on a 30/40 year journey, I promise you, 30k or even a hundy is nothing.

Luke83.. that’s a good comment, and a fair one. I think the real savvy investor who can buy and sell in a recession will do ok, but the leveraged and naive should be nervous. It’s looking uncertain, I agree with most commentators on here, it’s unpredictable and could surprise us by it’s resilience or by it’s drops. I agree with most, apart from TTP because he’s opinions are trash. I quite like CWBW though, smart guy and knows how to play the villain, what happened to him?

Not sure Tom, he has been replaced by a few doom merchants that are clearly very young or just not experienced in RE long term. It's called property cycle that some don't get, they fail to notice our dependants on housing, other countries such as Japan have other industries that drive their house prices and a lot more complex issues. Nz is very young and very simple. Will be an average 2022 but I still say positive territory by December?? Maybe I'm wrong. I take my guidance from those that are very experienced.

:|

Luke, are you guided by Obi Wan Kenobi or Master Yoda?

It sounds like he may be one of CWBW's "boys". Plenty of fuzzy logic.

I get cycles... I've been through em.

2007/8 was the end of the last cycle... caused by the GFC and interest rates fell drastically to support the economy which meant about a 10% fall from peak in values.

Commentators like to say the market survived the GFC without crashing, but they never say the real reason it survived - it was massively supported by lowering the cost of debt.

https://www.rbnz.govt.nz/statistics/key-graphs/key-graph-mortgage-rates

But it still caused carnage many haven't seen.

http://www.stuff.co.nz/business/3041761/Up-to-the-eyeballs-in-mortgagee…

I think that some of the spruikers have forgotten how property cycles end... but it should be a lesson for the very young and over leveraged.

But you're right Luke, NZ is very simple and when the reserve bank warns you that prices aren't sustainable, you'd be a fool to ignore their warning since they are the ones that effectively control the cost of debt and as such house prices

https://www.rbnz.govt.nz/news/2021/08/house-prices-above-sustainable-le…

Who know's what they're going to do, and while falling home values are very subjective, debt is very easy to measure

Won't be able to cut the OCR 2-3% this time to save the housing market!

Well put DDD, I agree.

Thats quite funny. Not sure its suppose to be, but very funny. You sound like TheMan, you could be TheMan2. Quite funny you mention property cycle, but the other DGM who thought property could only go up in NZ because we are special didnt think we were in a cycle.

Property is one type of investment as well many other types of investment out there. Much better returns.

100k might be nothing to you. To me, it's a shiny new boat.

Stabicraft?

Yea true that, nice stabi

The whole market is geared towards reno and sell though. That's why it's teetering on a cliff edge. First home buyers have long been priced out of desirable homes they'd want to spend 30 years in.

All the perfect starter homes that need a little work are gobbled up by reno and sell flippers. Meanwhile prospective FHB are told they should lower their expectations and look for properties that need a little work........

Lol. 100k is a lot if you are going to double, triple your interest costs over the next 3 years and your income stays stagnant.

Its the cost of a new EV. A new boat. 5 or 6 World wide holidays.

And we are not talking 100k. In Auckland the amounts are potentially much greater. We've already passed that 100k avg price mark and the fun hasn't even started yet.

the fun hasn't even started yet. <= well said

Most of all, there are people who are not hedged for a reversal.

Is this sacrassim? Whether or not people are "hedged for a reversal" has absolutely nothing to do with it?

Not sure what you mean by "tank" but the market is going south regardless of your reasoning.

An example would be those who used the emergency rates to clear their debt, and find and build profit making businesses, vs endless stacking of debt while believing the seminars endless growth stories. Solid assets, no debt and strong income streams vs massive debt not supported by income.

Tanking will make the FONGO crowd FOOP their pants. It's going to get worse before it gets better.

Teeing off people, are you?

I'm seeing a lot more for sale signs around my place. Seems like a bad time to put a property on the market but who really knows? Buyers will still face strong opposition from the sellers. Even in these times buyers should follow the usual strategy of not falling in love with a property and be prepared to walk away. Recognising a bargain is difficult though and can often only be appreciated in retrospect.

There is no such thing as a " Bargain " in a falling market.

Sure there is, decent properties are decent regardless of the current market state.

What has that got to do with a "Bargain" ?

Yeah, buyers should keep that in mind when negotiating. If the real estate agent says, "This is a bargain!" it would be a good comeback.

It would only turn out to be a bargain if the market later began to rise. But then, I guess, that would apply to all properties. My "bargain" currently would still be just a gamble. In a falling market it would have to be considerably below the market value to be considered a good gamble.

Why do agencies push Auction? (now, let alone ever) ill tell you the inside secret. -201 properties, each owner paid about $3000 marketing - that's $600,000 we get for free to market our agency brand to the marketplace. Oh what, they didn't sell? Oh well.

Marketing fees alone are not going to sustain the over grown number of RE agents out there.

Going to be a long winter for some of you.

Auctions are pushed because they create a forced sale like environment. It's either a frenzy you as the buyer have to prevail over, or the "market" telling you that's all the property is worth so you'd better sell now.

In a tepid or cooling market there's a lot less call to action.

They have the potential to generate maximum reward for minimal effort, that's why

All Agencies will ask for a marketing 'contrubution', irrespective of the sales method you choose. Last time we sold a property we negotiated a flat fee for the commission, which included advertising. Did they like it, not really. Did they want the listing, yep.

Ray white 70 out of 198, barfoot and thompson are clearly not doing so well, haven't checked harcourts.

If your a buyer, why bother going to an auction. Just tell them to contact you once it passes in.

Because you can be the winner on the day, under the hammer with a vendor who wants his/her property sold. Way more transparent than the smoke and mirrors multi offer situation and the ridiculous tender process (looking at you Wellington).

Transparent LOL.... who's bidding on the Phone and Computer?

One should never associate that word or honesty with the property industry.

If they want to sell we can negotiate at any point. Don't force me to buy under your conditions when there is now choice.

Auctions are there to negate rational thought, and restrict due dillagence.

Its also easy work for the agent.

Why go to auctions when there are more and more properties flooding the market.

A failure to sell at auction is an emotional hit to vendor expectations. Its a switch from me chasing you to you chasing me.

Exactly. Let the auctions pass in and give vendors a bit of a reality check. It'll soften them up a little bit, take a leaf out of Roy Nong Fong's playbook and take advantage of the seven d's.

Mankiw's words: "There is no shame in figuring out what the market will bear."

You see a man drowning, you are about to toss him a life preserver. "How much would you pay me to toss you this life preserver?" you shout. "Blub" he replies. "I'm afraid 'blub' just won't do" you call back, beginning to walk away. Through mouthfuls of seawater, he manages to spit out the words: "I'll pay whatever you want, just toss the damn life preserver!".

The man drowning was any prospective FHB or renter, the tables are flipping and this now applies to vendors and potentially landlords.

There's almost as many houses for sale in my neck of the woods as there was in 2019, quick panic!

More pressure on prices.. the trend is clearly pointing downwards..

If you want your property sold quickly ( or even at all ) here is a tip. Never use an agent. Come to terms with the fact RE Agents and Media have revealed to the public prices have dropped by 15-19% already and more pain is to come. Set your price accordingly. Then take OFF a further amount that the RE Agent would have absorbed. Simply advertise it yourself on trade me selling the fact the savings of no RE Agent is being passed onto the vendor. At the end of the day if the price is right it will sell itself.

You dont need Tim Mordaunt there blowing the saxophone, or his own trumpet.

https://www.stuff.co.nz/life-style/homed/real-estate/128055412/just-how…

Beware sales people offering free trinkets. It is simply a distraction. Mind you theres one born every day so game on...

So true, I’ve bought privately twice and sold privately 3 times.

It’s really not difficult!

Don’t skimp on costs though, professional photos and a excellent write up on Trademe with all the documentation ready to go ( LIM, electrical report etc) and suggesting a lower deposit has helped get purchasers over the line.

We sold privately, we were going through an agent initially in UK. The agent was mucking us around and not conveying our thoughts to buyer. We wanted a completion date for the Bank, the buyer after 6 months who kept saying the deal was imminent did not give us a completion date. The agent was manipulating us and so was the buyer, it was quite a tough time.

We talked to our neighbour he had a friend, the friend offered cash, we took house from agent and took the cash and only used our lawyers. Done and dusted.

If I buy, I will make offers privately, I know what I want, in the area I want, so when we get money together we will make offers, no agents. Its not the costs for me, its the agents I dislike the way they go about their business, they are so two faced. They have no empathy and are only in it for themselves. We have children, one agent wanted us to wait while they sold our rental, so it gave buyers an option, to buy with tenants. No consideration that's a huge risk for us, just making their sale easier. What a joke. I have never had a good experience with an agent, or real estate agency.

CWBW and his "indian boys" will be sweating bullets as their leveraged flipping strategy doesn't survive contact with economic reality.

Be quick!

Quote CWBW directly please : "my indian boys"

Updated.

It's certaintly interesting seeing articles like this come out...

Slumping prices: Banks pledge not to strip borrowers of 'special' mortgage rates, if their equity falls below 20 per cent

https://i.stuff.co.nz/business/money/128141126/slumping-prices-banks-pl…

The tone from main stream media has changed quickly...

Here's a question: in the current market approximately what percentage of CV do you think would be a fair price for a small (1bdrm or studio) apartment in central Auckland? Assume it's in a reputable building with no issues.

about 4 times the salary of a single non too senior professional, so about 70k * 4 = 280k. That is a "fair" price, but still expensive.

Personally, I wouldn't touch any with a barge pole.

*Maybe* worth a look at 50% discount.

Thanks for the replies HouseMouse and lucenera.

For the record I offered about 10% below CV and got turned down. Probably lucky for me. It should be noted that central Auckland apartment values haven't gone up anywhere near as much as house values over the last few years, so it seems reasonable to assume they won't fall as much. We'll see - the next couple of months will be interesting.

New Build townhouse rental listings in Auckland on TradeMe pretty steady over the past week.

Dive dive dive, see the speculators start to moan. It's the sence of entitlement to vapor loss that's really funny. Speculand still fails to realise how exposed it is.

Popcorn.

Seeking re-election is pretty hard if you start causing financial hardship. It is more likely that the talk of large interest rates rises will, like other predications be just talk. Don't forget most governments are up to their eyeballs in debt and it won't only be mortgage holders forking out more. No, you can be certain this inflation has been planned to reduce the government debt load, so it won't go away. In 5-7 years time a million dollars will be like 100K.

That level of inflation would be extraordinarily bad for asset prices in real terms. If you discount future cash flows based upon the level of inflation that you are implying in the above, the denominator of the asset price = cash flow / discount rate equation becomes very large.

People are talking about the Great Reset. What they don't understand is the reset is all about government debt and future liabilities. A housing market crash with a few bank failures is not going to make the government debt go away. High inflation is the answer to their massive debt. Collapsing house prices and deflation makes the debt load even worse. What you are likely to see is a controlled level of inflation that slowly but surely erodes the debt load. If there is a major crash / depression then that will surely have been engineered for a reason. Some suggest a new digital currency is on the way.

On one hand governments are criticised for their incompetence but in the same breath are accused of some global conspiracy. This government can’t deliver on any of their promises, what makes you think that they could engineer a global depression. Don’t look for conspiracy when cock-up is far more likely.

Maybe Doggog, but with two-thirds of government debt in foreign currency, keeping interest rates low to inflate away the local bond liabilities could be a net loss. Hiking interest rates hard and fast (and above step with the rest of the world) to strengthen the currency might be an attractive proposition. This would also drastically reduce inflation for imported goods which is where much of the immediate pain resides...sounds like a vote winner to me.

https://milfordasset.com/insights/investment-data-shines-spotlight-on-n…

Overseas borrowings represent nearly two-thirds of total gross Crown debt with the remainder sourced from domestic investors.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.