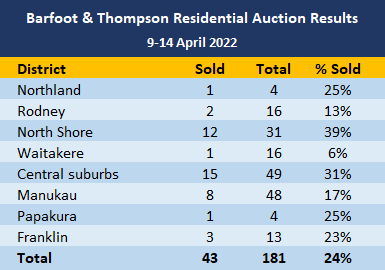

Auction activity remained inline with recent levels in Barfoot & Thompson's auction rooms in the week before Easter.

Auckland's biggest real estate agency marketed 181 residential properties for auction over the week from 9-14 April, compared to 200 the previous week.

That suggested activity was remarkably stable given it was short week.

Of the 181 properties offered, sales were achieved on 43, giving an overall sales rate of 24%, almost unchanged from 25% the previous week.

Around Auckland it was the North Shore properties that had the highest sales rate at 39%, while Waitakere properties had the lowest, with just one of the 16 Waitakere properties auctioned last week selling under the hammer.

See the table below for the district-by-district results.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

111 Comments

Headline : Housing Market Stable and Consistent .

After heavy decline from 84% properties selling under the hammer, is now consistent between 21% - 25%.

Has the downfall bottomed out and only way is up from here.

We'll see a big fall in the next release of figures followed by a 'recovery'. If interest rates settle at 7% we will then see 18 months of horror, circa 30% declines. Classic bubble blow off top followed by falls.

Amen !

25% of houses sold means 75% of houses passing in, going to negotiation and maybe even BEO, this is where sellers won’t get what they ask for. I’m not sure how many properties carry over week to week but these stats suggest a backlog of available housing. Each week there’s 4 weeks supply of housing going to auction is another way of looking at it.

What would skew this stat is how many houses are going on to sell in negotiation or BEO, but that’s a tough world right now. And also how many properties get carried over to the next week. It’s too early in the morning to go figure that out but you get the gist.

A stable lack of sales shows some support, but it’s a low support at a lower price (according to HPI)

Is it the beginning of the end of current housing bull run, which ran for over 20 years - bigger picture as deefinitely is the end of housing ponzi triggered by Mr Orr and Jacinda under guise of pandemic.

Next ponzi can only be build, once this is shattered to the ground and people forget the pain just like the trauma of stock market crash in late 1980s.

Will 2022 / 2023 will be for housing speculation what 1987 /1988 was for stock market in NZ.

Good morning property doomers ! how much has your property lost overnight ?

I’ll answer that question for you in 6 months. Anyone who thinks the property market isn’t on life support is extremely deluded. Big crash

As a non owner will you be better off in 1 year than what you are right now... nope. Rents higher, and less chance of getting a mortgage

Actually I will be a lot better off.

Average house price $1.2 mill, deposit approx $200K

Invest in my business $50K.

My products are expected to sell 400/ month at $20 profit per unit. By next year I will have 6 products selling. 400 sales a month is relatively easy to achieve whilst some people sell thousands.

6 x 400 x 20 = $48,000 per month.

We aim to sell 25 products in 4 years and then ramp up to 50 or more in 6 years once we truly know what we are doing and bring on help.

Easy sums.

25 x 400 x 20 = $200,000 per month. This is profit paid into our account.

Now we may not hit this exactly, we could do better or worse, but you should get the gyst that this is slightly better then anything I would achieve with property. We will build a business that can be passed to our kids and that can be grown and differentiated. Not to mention you can do this from anywhere in the world as its an international company that is done online. Property would never give me the lifestyle I can achieve with my business. This is just a normal business selling normal products.

I am sure some of those FHBers who bought in the last nine months or so are starting to worry. Their deposit is disappearing and the cost to service their large loan is going to increase when their fixed period runs out. Fancy being in their shoes?

I know of a few, paying a minimum $1000 to service their loans once interest kicks in. On homes at the bottom of the ladder so no downsizing options either. I hope for their sake they’re able to have savings and have a stable cashflow over the next 3-5 years…

I know someone, who was running a franchisee business, making decent money but hard work and is now planing to sell it to repay some debt out of million dollar borrowed to reduce mortage to minimum and opt for job.

This option is not only to repay major part of mortage but also not worth the time and effort, NOW to do business and possible as he is getting good job offer in similar industry.

There are always options. They could sell and rent.

IT Guy, yes the market overall is down but it doesn't mean everyone's house value is down. I bought a property in August 2022, Corelogic (Valocity) currently valued it $870k more than what I paid for it 8 months ago, but I know it's worth more than this, because I have made significant improvements to it, which are not reflected in Corelogic's valuation.

Ouch so you sold out early and bought back in at the peak... As they say, it's dangerous trying to time the market. What kind of improvements have you made?

Why "ouch"? I didn't sell the average house for the average price, nor did I buy the average house for the average price.

Ouch because the majority of interest.co commentators are expecting 30%-40% house price falls...

As for "what improvements?", I cut trees

If you bought in August 2022 you are staring down the barrel at a big fall in value. That was terrible timing. I thought you were smarter than that. When things are stupid you keep well away.

Sorry but this is a really dumb comment. Here's a person telling you that they've made over $1 Mill in 8 months on a specific property, and you come back saying "you're losing because the market is going down".

You too, clearly don't make the difference between the direction of the market overall, and the fact that individual properties can be bought or sold below or above average value and the value of a property can be increased if one is astute.

You can’t have made that much money in that time. The market was hot when you bought it and started to come off not long afterwards. The heat has continued to come out of the market throughout 2022 and will continue to do so for some time. Your credibility is certainly going out the window.

I can only repeat my post above as you must have clearly missed it

You too, clearly don't make the difference between the direction of the market overall, and the fact that individual properties can be bought or sold below or above average value and the value of a property can be increased if one is astute.

And yes, to be clear, I have made this much money in this time. I would have made it in a much shorter timeframe if it wasn't for the lockdowns

Too vague as always. We could all talk in generalities like you. Give us some real information such as an address. If you are not willing to do that stop doing what you are doing.

"stop doing what you are doing" Who do you think you are to tell others what they can and cannot write on this site?

Also, I'm very open and candid but I'm not silly enough to give you my address.

I'd just be a bit careful with valuations, especially if they are generic online ones without inspections etc. I got a valuation from Valocity 5 or 6 weeks ago, I reckon it's 10-15% too high, especially as the market is definitely dropping away.

Coredlogic will be working from old data if you sell soon might just lose 10% to 15%

Which part of "the value of the property has increased by over $1 Mill since purchasing it in August 2022" do you not understand DTHR?

Are you talking about paper gains Yvil? Where are you cashing in this $1million - homes.co.nz or oneroof.co.nz? How'd you appreciate the value by $1m cutting down trees...

Ever heard of "Million dollar views" ?

The problem with this discussion - as for many comments about the coming fall in values - is that those pushing what is gloom is that they are talking a short to medium term fluctuation (paper loss) where as owning a home is longer term. Most of those commenting do not seem to be able to comprehend this.

It seems I really do need to recount a personal experience yet again. I purchased one of my rentals in 2006 and during the GFC the RV fell nearly 20% below my purchase price. When I did sell it in 2016 I made a significant capital gain.

For most, the implications of short to medium term falls in value have little importance. For homeowners it is still the same home, for investors it is the same rent. Remember all the talk when prices were rising that it was commonly stated with glee that it was only “paper gains” until one sold . . . nothing has changed except some now choose to ignore this due to their bias.

I will also say this again; for those - especially FHB - who have recently purchased a home (or investment property) the more significant issue is rising interest rates. I have also said it for some years; they - especially FHB - need to be prudent and pay down the mortgage as much as possible and that is taking on increasingly more importance and urgency. Being prudent means putting off discretionary spending such a new deck or kitchen, or keeping that car for a year or two more.

P8 you should of waited to sell august 2022 Yvil would have bought at top dollar from you.

DTRH

The one I kick myself repeatedly about is my first home . . . $80k then and today the new Auckland RV is $1.2m. Should have kept it but back then people didn’t believe that property always goes up in value. 😪

"should of waited" but "would have bought". Make up your mind DTHR

Yvil you have criticised me for making below the belt comments, yet you do it regularly and have done it once again, here.

maybe we can both commit to playing the argument rather than the man?

I have also commended you below for your new commitment. Could you please point to my "below the belt" comment? I cannot find a comment here, where I called another poster any name or attacked him/her personally. Thanks

You have done it numerous times like me. Maybe we are actually quite similar? Both of us can do better. I am committing to it.

Sure HM, I'm happy to give you my commitment not to attack people personally (or call them names which I don't think Ido)

Good, I am glad to see you have acknowledged the errors of your ways just as I have done.

Time to move on.

I'm trying to get my head around how Yvil bought in August 2022.

Just for that Yvil loses here. Also you can't insist you have made anything until you sell.

Happy to be a "loser" in your eyes, when I'm making a vary large gain.

I can't really put it into words except for a vague feeling of disappointment.

So chopping down some trees has given you million views, dream on Yvil no way would house go up over million when market is on downward path in 8 months

Yes I agree, it’s a ridiculous claim.

And that’s not to bag Yvil for the sake of bagging him (I have made an Easter commitment to steering away from ad hominem). It’s just an objective comment.

unless he had two big scheduled heritage pohutukawa trees removed, that were otherwise blocking views, if Yvil was able to achieve that then yes the value could have increased significantly.

HM, great commitment you made! Well done!

Great, I hope you might also be able to commit to this as well.

DTHR,

What's the address of the property discussed?

How much was it bought for?

What is the view of?

What did it take to cut he trees to obtain that view?

Can you answer an of these questions? I can, all of them, precisely.

Lastly I did not claim getting that the view alone increase the property by $1 Mill, I bought really well (which surprises me given at the time the market wassail really strong)

To be fair, until you sell it you can't really make any claim of its value.

Right, so Elon Musk is worth nothing because he hasn't sold Tesla, bill Gates is worth nothing because he hasn't sold Microsoft and Warren Buffet is worth nothing because he hasn't sold his portfolio of shares. According to your logic, they will only be rich when they sell and put heir cash under their very big pillow?

I didn't say that your house is worth nothing, I said you don't know its value. And those people you mentioned also have a lot of money, beyond the value of their stock holdings (the values of which are known because people are regularly buying and selling the stocks). Your response is unusual.

True, you didn't say it's worth nothing but the value can be assessed fairly accurately. Actually the whole banking and mortgage industry relies on it, a whole profession is dedicated to valuing properties (valuers). If a value could not be attributed to a house fairly accurately, banks would not lend any money for said house and hardly anyone could buy a house. A house could also not be used as collateral for a business loan and a lot of businesses would not exist as a result.

True, whilst I agree with you, I guess my point is that in a falling market it become pretty difficult to tell. We bought our place in August too, and although the changes we've made to it have made it a considerably more desirable house, I do wonder if we'd even break even if we were to sell right now. Sentiment goes a long way.

Crispy

Until it sells you can’t make a claim to its value?????

It is common practice to put a “value” on a property - this includes a valuation for rating purposes (RV), for insurance purposes or a bank for leading purposes . . . and of course both a vendor and potential purchaser will have their own values.

The “value” or “valuation” of a property can be made by looking at land and floor area or by comparison to similar recent properties that have sold. A registered valuer specialises in determining a value on a property and there a range of algorithm apps.

One should recognise that those involved in property consider “sale price” and “value” to be two different things. For instance, it is recognised by investors to look to purchase a property below its market value - this can include properties where there is a degree of distress on the part of the vendor such as a mortgagee sale, a matrimonial split, or an estate sale. Arguably the sale price is below its market value . . . and this is not just about investors but many homeowners including FHB.

The sale price doesn’t set a property’s value. Does a house’s value change in a week if it is bought by a flipper to I sell a week later at a profit? There has been numerous court cases for a variety of reasons where a sale has been considered not the value of a property (think REA scams).

Have you ever bought something and not got value? Sale price and value are two different things.

In Yvil’s case, the key question is how has his value been calculated . . . how did the purchase price compared to a registered valuation at the time of purchase, what is the value of the improvements he has made including removing the trees (which can add value), how have sale prices for properties in the same locality trended as not all regions and locations have seen the same recent price movements. . . .

However, yeah, the value one places on a property may not be particularly valid. Trump appears pretty good at this depending on whether it’s about tax or use as a security or boasting of his wealth.

cheers

DTHR, the first step to a better life is to rid oneself of all feelings of bitterness, envy and anger. Only then will one be able to open his/her mind to the amazing things that are possible to those with a good, constructive outlook on life.

Life is really amazing, but it can only be so to those who believe that it can be amazing!

Yvil hows the view from the asylum . I think we have all worked out that you really don’t have a clue and make up story’s

It's a shame that you're not willing to open up your mind. I understand, I used to be the same, my parents were good people and well meaning, but they were very restricted in their mind, they had a mentality of "it can't be done" which I inherited. What changed me, is the open mindedness of my wife, although it took me years to accept that all sorts of things I though were impossible, could actually be done

That’s very funny coming from someone who calls him or herself Yvil. Why don’t you call yourself Goodness?

Yvil, I am interested in ‘outside the square’ approaches to investment and all things in life.

keen to know if you got resource consent to remove heritage trees to open up your views, if so that is a canny move, and if so well done as those processes with council are tricky.

I fail to see how cutting down a few non-protected trees would add much value, so I assume you took the risk of getting resource consent to remove scheduled trees that were blocking views.

Genuinely keen to know, thanks.

HM, you're very much on the right track, well done. They are Pohutekawas in front of my property on Council land, therefore not an easy thing to do, to prune them, otherwise the previous owner would have done it (I know he tried to). That's why it took so long.

Good work!

Good work? Sort of sounds like he got a public asset destroyed for private benefit. Sounds selfish to me. But perhaps they were rotten or something, in which case good luck to him.

That's a bit harsh. If he was able to get some Pohutukawa trimmed back a little to give himself a bit more of a view, then good on him.

Some trim! Apparently it was worth a mill!

You've said you are in St Marys Bay, Yvil, I'm guessing you are somewhere near the motorway if it's an area with sea views. I lived in that area once at a friend's place when I was at uni, can be a little noisy at times with the motorway, but great views!

Are you interested to see what the council has in mind for changes to the Unitary Plan? Could be more upward value potential there for you if they look to get rid of the Special Character overlay where you are.

I think I know which area it is (am local to that area) but I'll keep that to myself for Yvils privacy. Removal of those trees would increase outlook (and specifically reduce the amount of shade). Also, $1m as a percentage of a more expensive property isn't as much of course.

The story sounds BS to me and even if it is true it's for sure not a 1million dollar value add...

That's why I didn't say that cutting the trees alone added $1Mill...

Look at Waitakere. 1/16

Why the persistence with auctions? Such a waste of peoples energy, much more efficient methods that are minus the emotional PT Barnum style games the RE industry relies on to maximise their commissions, marketing back handers & volume/turn over.

Two reasons - on less desirable properties, an auction helps show an out of touch vendor that their asking price is no longer realistic. On desirable properties you may still get into a bidding war situation.

Why not Auction

Once upon a time during boom, real estate justification was that in auction market determins the value, so why not now.

What real estate agent does not say was that they were trying to exploit FOMO to get high price.

Now, Market is determining the value FONGO

Because auctions require the least amount of work for the agents. Same with open homes.

Looks like we are in the situations that we will soon have more agents than houses for sale. We need more workers in horticulture.

I totally agree. I've been looking for a property for a couple of months now and don't even look at anything being sold by auction.

All doom and gloom in the housing market

There is more talk about mortgagee sales on the horizon

It takes normally six months for mortagee sale to trigger so its effect will be felt only by end of year or early next year.

Looking at the sales in the north shore, looks like the vendors are more realistic...

Do they know something that the rest of Auckland is missing?

Unless you live on beachfront Taka or Devo and don't have to go anywhere, the Shore is a dead horse

Worse hit will be newly constructed matchbox houses in Auckland.

Not very popular and were selling only under FOMO ( Better than not having house feeling) and now supply will grow at much faster pace than demand in that segment and more important will be holding capacity of first time mum n dad builders as time will come when they will be happy to sell as long as not making loss or with minimum loss.

House on our street was demolished and four small townhouses were built on it and are in market since few months but the owner is rich Asian so has now decided to rent them out to avoid selling in loss and is possible as is cash rich but not all new first time builders may be in that posistion and some may have overstreched under advise from friendly real estate expert.

Yes that sector is going to be a bloodbath, for both recent buyers and developers.

There is so many of those now, if rented it will be really low.

Will also need maintenances as this developers used the cheapest materials if they planned to sell it in the first place.

Yes there’s going to be a huge oversupply of new two bedroom townhouses for rent. You can see it building on TradeMe. Lots of the places sit around for weeks, and then ultimately reduce 5-10% in asking rent before they are let. Quite high turnover too, it seems, if the rental properties where we live is anything to go by.

poor investments, in my opinion.

Be quick!

If we really wanted a free market, sellers should not be allowed to have a reserve price and the the sould go the the highest bider whatever the bid is.

Vendor's Bid!!! How on earth can a Vendor buy his own property? Ridiculous & a phony bid to pump up prices at auction.!

Nothing wrong with having a reserve price. But it should be required to be disclosed 14 days before the auction.

Auckland housing market is so over valued even if people started selling 30% off they would struggle.

Does anyone have any examples of 'bargain' or 'discounted' prices in Auckland...in particular North Shore? I'm not seeing it yet. Still seems to be quite abit of demand at well presented properties and in good locations. I've come across some properties with multiple preauction offers.

That's a very good question. The doomers are going to have to front up or shut up on this matter soon.

Why?

Official data, rather than anecdotal sales observations, is the best measure, and the HPI is showing Auckland as being down 8% from peak, so far.

Of course there are always exceptions to averages, on both the up and down sides.

I just wanted to write "front up or shut up" because it sounded badass.

It would be interesting to see a genuine bargain though. Very hard to judge. I suspect these khaaaark clowns wont buy even when it's staring them in the face.

What type of properties are selling lower HouseMouse? Crap X rentals in crap locations? Or is it across the board? This is where boots on the ground helps get a good feel of what's actually going on.

Are you in the market to buy a house in the North Shore Nifty?

Always looking for a bargain Yvil...

Be patient. You might not hit the bottom which is a long way off yet. Increasing interest rates and a worsening cost of living in general are going to make life hard for many of us unfortunately.

I know not everyone is able to, but we stocked up on a lot of day to day, household items and clothing / footwear late last year, mostly on sale with big discounts, as a hedge against inflation.

That was also a reason why we bought a new townhouse 2.5 years ago with all new whiteware, and a 10 year Masterbuild guarantee. With the Homestar certification nearly done, we will also be eligible to get a 1% discount on our mortgage rate. We also bought a new car, which we will pay off end of this year. We shouldn’t have any big expenditures over the next 5 years.

Also, I have just been to the supermarket and while prices are certainly up, I think if you shop smart and also make some healthy diet decisions, the pain at the supermarket check out can be limited.

I’ve never understood why someone would buy a brand new car on finance? Seems like a great way to lose money twice.

That’s what I used to think, but not anymore. We put 50% down and zero interest on a 3 year loan.

I have had so many issues with second hand cars in the past that have cost a small fortune. Once we have paid the car off late this year we should have at least 7 good years with the car.

0% finance will be much more valuable as interest rates increase. Two years ago when homeowners had access to 2% finance, not so much.

Peace of mind motoring. As HouseMouse states, we have also had problems with second hand cars. Our last car (a Toyota bought at 150k) we ended up spending over half what we paid for the car in fixing things. Power window, alternator, valve cover gasket, water pump, steering control arm to name few.

It's not so much the cost of the repairs, although I can think of better things to the spend money on, but it was the hassle of it all. So we ticked up a brand new Toyota on the mortgage last year, our mortgage was around 1 x DTI so we had room to do so. Never looked back.

That’s kind of what to expect if you buy a second hand car with 150k on it. Try a car 2-3 years old with under 50k and that’s the sweet spot for not paying a premium to drive the new car off the lot.

Is 0% readily available on used cars 2 or 3 years old?

for us the 0% finance was a big draw card.

No, I wasn’t suggesting it was. Just pay with cash.

Not that many people have 20 or 30K in cash just waiting to spend like that on a car.

I'm VERY happy with our decision and purchase.

In my neck of the woods, this place sold for $1,180,000, which is 17% under its CV (of $1,425,000) and for 30% under its QV (of $1.7M):

https://rwhowick.co.nz/properties/sold-residential/manukau-city/northpa…

Trying to make some sense.

25% clearance rate - this portion of buyers and sellers expectations were met.

75% could not agree.

The majority of vendors expectations exceed that of willing buyers. But, we do not know if any were sold after the auction by negotiation.

From the low sales numbers, is it safe to say that some vendors chose not to sell.

In Auckland, lots of townhouses are popping up. Some buyers will choose these.

Prediction- the price of older rentals will be the first to go, should a correction happen.

> But, we do not know if any were sold after the auction by negotiation.

Generally, sold straight after is counted as sold at auction by REA.

Where I live the houses in the $2-$6m range are not selling. They have been on the market for months. Especially the large character homes. As interest rates rise this will only get worse.

Absolutley. Seen stuff for sale at crazy markups that have not sold in the last 24 months. Usual formula, auction, the POA, the priced, and the a 25% discount and still not sold. The only thing stopping people selling anything in the last 24 months has been excessive greed.

Hows that greed taste now...?

You have to wonder...how many people can actually afford to buy a $2M-$6M property? We must be talking somewhere in the top 1%, so new entrants to the bracket would be few and far between.

I found this so I would say a lot less then that.

"Tax data from Inland Revenue highlights that the number of earners who earnt over $150,000 a year has risen from 19,240 in 2001 to 110,650 in 2018, and the number of people earning $250,000 has gone from 5470 to 32,430. As a proportion of all earners, in 2001, just 0.64 per cent of all earners made over $150,000 a year. In 2018, that figure rose to 2.87 per cent."

And that is earning over $150,000, with the way costs of rent, petrol, food and beer have gone up. Nowhere near enough to buy 2mill plus houses. I earn't over $200,000 before I became a pauper trying to start a business up and I struggled to buy the kids apple juice and cake when I went to a cafe for a treat. You buy 2 coffees, 2 apple juices and 4 cakes and that's probably $40, then if we went for ice cream that's about $8 for 2 easy. Thats on top of rent or mortgage you would be lucky to save for anything. Thermos flasks with your own coffee are your friend and muffins from New World. So 2 mill plus houses not sure who's buying that.

The HPI suggest otherwise. Median prices have still gone up in March whilst the HPI is down, this means one thing, expensive houses are selling more than the lower priced houses

Exactly right.

Although it certainly does not mean the market for expensive homes is buoyant. It's just that it is less sickly that the market for lower priced homes.

I imagine the ass-end is falling out of the shoebox townhouse market.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.