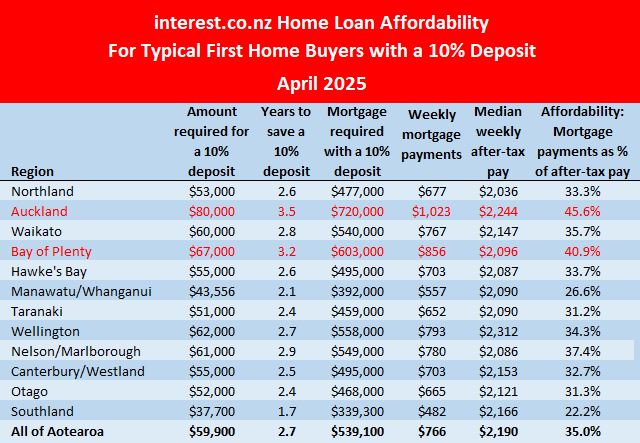

The financial position of aspiring first home buyers improved by 10 cents a week in April, as the housing market sat becalmed on a sea of economic uncertainty.

There was hardly any movement in either lower quartile selling prices or mortgage interest rates in April, which are the two main drivers of changes in housing affordability.

The average of the two year fixed mortgage rates offered by the main banks decreased by the finest of margins, from 5.08% in March to 5.05% in April. The Real Estate Institute of New Zealand's national lower quartile selling price increased from $597,500 in March to $599,000 in April.

Those changes saw the weekly mortgage payments on a home purchased at the national lower quartile price decline by just 10 cents a week, to $765.68 in April from $765.78 a week in March.

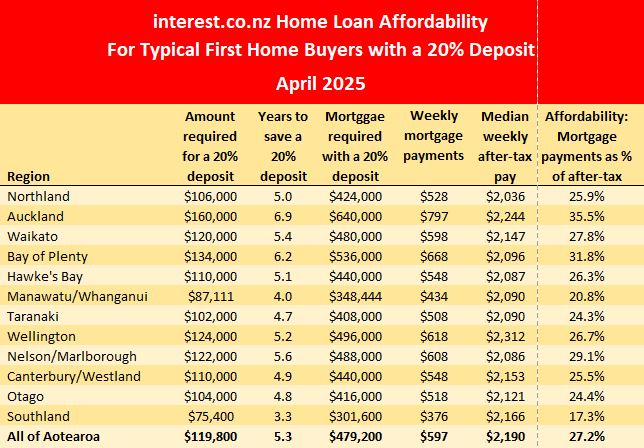

The savings would have doubled to 20 cents a week if the same property had been purchased with a 20% deposit, which would have seen mortgage payments dip from $596.98 to $596.78 over the same period.

The latest figures could signal the substantial improvements in affordability benefiting first home buyers over the last year and a half may be coming to an end, for the time being at least.

Mortgage payments on a lower quartile-priced home purchased with a 10% deposit peaked at $935 a week in November 2023, meaning they have declined by $169 a week over the last 17 months.

Mortgage payments on the same property purchased with a 20% deposit would have declined from $740 a week to $597, leaving the borrower better of by $143 a week.

Those improvements in affordability were almost entirely due to recent declines in mortgage interest rates, with the average of the two year fixed rates dropping from 7.04% in November 2023 to 5.05% in April this year.

Over the same period the REINZ's lower quartile price barely moved, dropping by just $1000 from $600,000 in November 2023 to $599,000 in April this year.

However with the Reserve Bank due to review the Official Cash Rate next week and another 25 basis point cut widely expected, we may not have to wait long for further improvements in affordability. Although of course that depends on the degree to which banks pass on any cuts in the OCR to their retail rates. The OCR is currently at 3.50%.

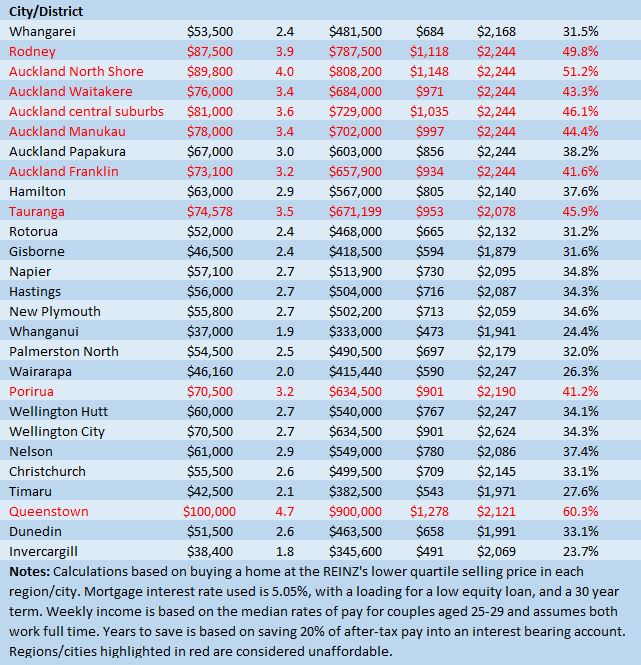

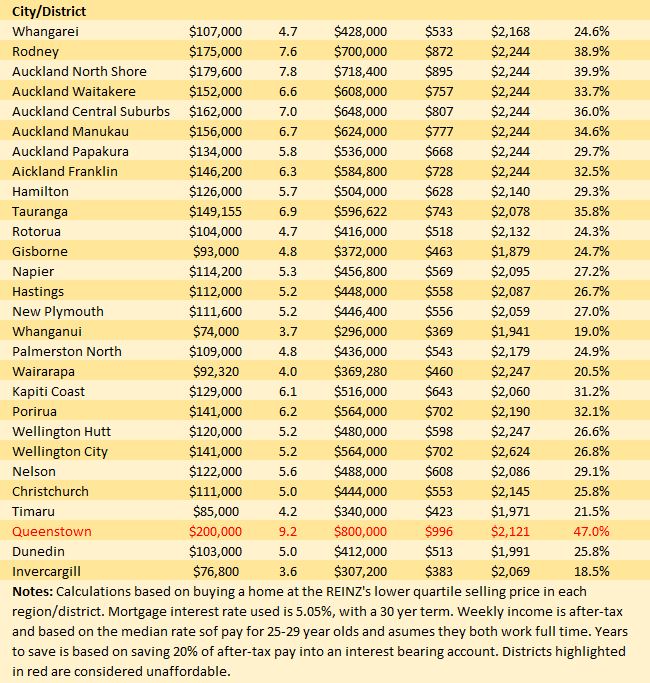

The tables below show the main affordability measures for first home buyers with either a 10% or 20% deposit, in all major urban areas throughout the country.

The comment stream on this article is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

10 Comments

If you have 30 10 cent coins

You could get yourself a 20 cent bag of lollies

We're all gonna be rich! 🥂

No change to affordability for first home buyers

That's quite surprising at a time when interest rates are going down and according to NZGecko "housing is going through its biggest crash in NZ history". Something doesn't add up !

The change in 'affordability' of houses being more than offset by the unaffordability of everything* else.

Throw in job insecurity and all those free 70sm metre sections available and the prospective of greater declines makes complete sense.

*BYOE - By 2035, Central Hawke’s Bay residents connected to the council’s water supply could see an increase per household from about $2500 a year to more than $7000

At that price you'd be better served storing and consuming your own water.

That's not how "Housing affordability" is measured Rastus. Read the article. Here it is for you:

There was hardly any movement in either lower quartile selling prices or mortgage interest rates in April, which are the two main drivers of changes in housing affordability.

I've taken the liberty to highlight in bold the real reason why affordability hasn't improved.

Widen the lens.

Mortgage rates have been dropping and take time to flow through. So even thought no rate change in April, many coming off onto lower rates from past changes.

First home buyers are people looking to buy their first home. For them, the effects of any change in mortgage rates, either up or down, is immediate. It takes longer to filter through for existing home owners.

yep fair point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.