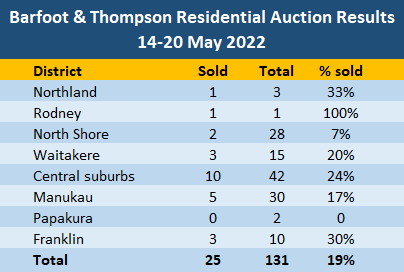

There was a jump in the number of properties offered at Barfoot & Thompson's latest auctions but the number that sold under the hammer took a dive.

Auckland's biggest real estate agency marketed 131 residential properties for sale by auction in the week of May 14-20, up from 90 the previous week.

However the sales rate headed in the opposite direction with just 25 properties selling under the hammer, giving an overall sales rate of 19%, down from 29% the previous week.

At the auctions where more than a handful of properties were offered, the sales rates ranged from 7% for North Shore properties to 30% in Franklin on Auckland's southern boundary.

The table below shows the district-by-district results.

Details of the individual properties offered at all of the auctions throughout New Zealand monitored by interest.co.nz, and the results achieved, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

80 Comments

Looking a bit closer at some of the sales in Auckland last week I see a few that had pre-auction offers selling at the auction with no further bids. All sales look well below the middle price estimates given in the various websites that do that.

However some reasonably good prices. This small house on a small section in Onehunga fetched 1.25M.

https://www.barfoot.co.nz/property/residential/auckland-city/onehunga/h…

Looks like probably only one bidder who was quite determined but had hoped to get it for under a million.

Market has soften but vendors are still holding to their price for now, with little flexibality.

No sell but lot of resistance in house price fall, may be, it is matter of time as unlike stock market, where price reaction is fast, property takes time to reflect.

Totally. Although consumer sentiment can get crushed pretty quickly, which has a flow on effect to house sales.

A lot of people just trying to sell as can see huge drop in market coming the one who managed to sell are very lucky.

Hi DTRH,

If people believe there's a "huge drop" coming in house prices, then they're likely mistaken.

The biggest benefit is already here: the housing market has slowed down, so prospective buyers have more time to look around and make better-informed purchase decisions.

TTP

Hi TTP price’s already falling and rates are still just up from emergency levels. At what point would you say the house price’s are falling because what we are seeing now is only the start of downturn.

What buyers?

For the stats:

~30% drop in mortgage volumes March year on year is made up of:

25% drop in OO commitments

33% drop in FHB commitments

44% drop in investor commitments

More notable is the distribution of income in the FHB bracket. The average buyer gross income (average used as median unavailable) increase from 2020 - 2022 has been 20%. That is FHB who are able to get a mortgage require 20% more income than 2 years ago to be able to buy a home that has already decreased in value.

The compounded wage inflation during this same period: ~5.5%

Also notable in buyers gross income is the shift in volumes for different price brackets. There is a distinct trend in lower income brackets declining in volume and higher income brackets increasing in volume.

What does this all mean?

Only those with high incomes (most active is 1.5 - 2 times median household income) have been able to enter the market at current prices. This is upper quartile earners buying lower to middle quartile homes. A little bewildering as to why but each to their own. Also worth nothing is the ~30% drop in $m commitments and ~35% drop in buyers. Less buyers borrowing more and more...

So as interest rates rise and inflation hits the pocket, as rental yields start to decline and mortgages roll over to new higher rates, again; what buyers?

I find quite fascinating the similarities in the reaction of the people to the downturn of the house market in NZ with any other crash in any other country with a bubble. In Spain, my country, in 2007-8 when things were going the same way as here, people were quite convinced that by no selling by the insane price that they thought their houses were worth (not as insane as now in NZ though) and just wait for months or maybe a couple of year they will get back the same money or more. Of course, it didn't happen and it took more than ten years to get back to the prices of 2007-8. In NZ it will be the same but the bubble is so huge that I wonder if it's going to take a lot longer (a bit like the Japanese house market from the 90's)

Great comment, and I love your home country.

Thanks HM, yes, it's a wonderful country

Yep, my parents live in Spain and they saw the same thing. The only thing selling was mega-mansions to Russian millionaires and billionaires.

Meanwhile the "average" house price keeps climbing because of the composition of sales.

Yes - corelogic emailed me to let me know my house had gone up in value by 5% last month.....

Same in Uk early 1990 also ten years to recover price’s were only around 15% of price’s in New Zealand today. Once rates go up the Carnage will begin.

But NZ is spehcial!

Yes was chatting to a guy from Spain a few months back. He purchased an apartment prior to the Spanish bubble bursting (out of FOMO…)…he says that he still hasn’t recovered his losses…

He thinks the NZ market is crazy…worse than what he saw in Spain before the market tanked over there.

Hola Joaquin, fellow Spaniard here. I have been saying this exact same thing here for years and all I could hear back was all that confronting doom and gloom rhetoric from a bunch of commenters who just wanted the party (for them) to keep going, likely supported by the RE lobby. It is interesting to see the similarities in behaviour from the two countries, do you recall Alvarez Cascos saying that if prices were high was a good sign the economy was blooming, well it's happen with National politicians here during Key's first term, so yes NZ is NOT different.

do you recall Alvarez Cascos saying that if prices were high was a good sign the economy was blooming, well it's happen with National politicians here during Key's first term, so yes NZ is NOT different.

"A good problem to have", a "sign of our success" etc. Yes, remember those. While looting the young we were telling them that it was for their own good we were taking their wealth.

yes they have to realise with the 7.2% stress tests, the ones that could borrow 800k can now only get 650. They cant pay with what they havent got!!

Ouch, what a waste of the auctioneers time

Screw the auctioneer, they still get paid to show up. Waste of time for vendor, agents should be more realistic with their clients

It's the vendor's that won't budge - the agents will be sweating bullets trying to get price drops

Usually agents are the ones pushing for Auctions, because they're typically viewed as the quickest way to get a sale. The vendor gets sold on the prospect of achieving a high price in a competitive bidding environment.

yes looking at the small number of auctions says it all. Auctions are a waste of time in a falling market, except for the 3 mill plus properties.

Saw an ad, house for sale, asking price is about $60,000 more than last year.

And a section in Ruakaka, by the beach, not a beach resort, asking price $750,000.

Vendors can ask, will they receive.

Regarding the section, it seem there's a decent amount of near retirement age people happy to pay cash for a coastal section, then pump 3 million more into a build.

I don't know Ruakaka very well though to know how desirable the beach is.

The inequality in Ruakaka is very stark. There is a poor neighbourhood (with a heavy gang presence, wondering bully breed dogs etc.) right down the road from multi million dollar beach-front homes. Just something to be aware of if looking up those ways. You can see it in the local supermarket, rich holiday makers buying wine and cheese standing next to obviously struggling people buying basic white bread and NZ Lager at the checkout. It is kind of uncomfortable.

sounds like many supermarkets then.....

Haha that's true! I'm from South Auckland and it was shocking even for me. The poverty in Northland is something else.

Turangi the same..... is a polar world those who have and have not.

tothepoint thinks things stay at these high levels, its going to be a very hard wakeup for those who have a lot of money and are about to loose a lot of it, i saw this in the 1987 share crash, those who rode tasmon properties , ariadene, judge to the bottome etc.... property in NZ is way overvalued, those with nothing have nothing to loose!

Sounds like Royal Oak Pak n Save or pretty much all average Auckland suburbs.

In my part of the country RE agents are promoting a strong market and state that somehow we have avoided the slowdown in other parts of NZ. Reality is there are houses on the market everywhere, most not selling as asking price in the clouds. Place near me sold <2 years ago $700000, now want 1.15M having had nothing done to it!!! First few weeks had agents all over it, some open homes, last several weeks there has not been anyone near the place. Some people just refuse to accept that things have changed.

I agree, some vendors still have completely unrealistic expectations. I sold a house within two weeks of going to market last month. I'm happy I got a fair price and the buyer got a good deal. The tricky one for me now is that I'm looking to get into a larger home for my family and all the suitable houses I've looked at are still way overpriced. One of them, the asking price is almost double what the vendor paid for it 2 years ago. I'm happy to sit tight and wait for now.

It's going to get worse. Money now costs...money. Wait till loans rollover off 2%, as many will this year and then see what happens. Will today's rates of 5% be seen as the bargain of the next couple of years.

Rates are going up. Negative leverage is coming.

Popcorn.

You probably want to know how much new debt was written since 2020, because anything older than that will mostly have been taken on in a 5%+ or thereabouts lending environment.

Further back than that. Depending on the term, rates haven't been this high since at least 2017. And if you're back before that it barely matters because the prices were so much lower.

Yes there are some that fixed long a while back. Five years at 2.99% was the best deal a while back. However it is well commented on here recently the significant amount on short term 2%. All due this year, and facing a doubling of its costs, or more if that now includes a principle payment as well.

I don't think a major correction will be as catastrophic as many suggest here. As you say, those most affected are the ones taking on large debt at the peak, so comparatively not really that many households.

It will look bad in the media, but houses were only worth that peak crazy money if you sold it for peak crazy money.

People may in thier minds feel like that's what they should still get, and that may affect current price expectation (there is many years of MSM conditioning to break) but end of the day the value is what you achieve today.

A lot of the crazy money was also tickling down, ie older types selling mixed housing family home to investors for silly money. They then buy a place for retirement at silly money but don't have debt etc.

I know we were writing record levels of new debt. But again. Relative to the wider function of the country?

We were probably always heading towards an economic slow down prior to covid regardless.

Nah, it will be really bad (but kind of good too, it needs to happen)

so much of our domestic economy is reliant on real estate, finance, property development and construction. All these sectors (and related ones) are going to be whacked.

The government can step in and employ the construction sector, including with more residential and HNZ building.

Harder on real estate and finance perhaps, because there's less intrinsic value that an employer of last resort could take up and utilise. I guess we could employ real estate agents in Jobs for Nature, or make them apprentices in the construction sector.

I guess it depends on how you define the peak. Is it the period between Covid stimulus and now or did the peak start before then? Remember the IMF and others have been saying that the housing prices have been overpriced and unsustainable for years. Here is snapshot report from 2013

https://www.elibrary.imf.org/view/journals/002/2013/117/article-A001-en…

Does this sound familiar?

8. Housing sector risks. Household credit growth, housing market turnover, and house price inflation have all recently picked up, particularly in Auckland where supply bottlenecks persist, and prices remain elevated by most measures of affordability.4 Recent developments also suggest some easing of mortgage lending standards. In these circumstances there is an emerging risk that sustained rapid price growth could give rise to expectations-driven, self-reinforcing demand dynamics and price overshooting. A shock to household incomes or to borrowing costs could cause a sudden price correction, reducing consumer confidence as a large share of wealth is in housing, worsening banks’ balance sheets, and impacting overall economic activity. There are some mitigating factors, with a declining ratio of household debt to disposable income and low concentration of debt among low-income households likely limiting mortgage defaults and the impact of house price declines on the banks’ balance sheets (figures).

500,000 new mortgages since March 2020

where you get that, its too high

I remember reading once on this site that something like 50% of new mortgages aren’t actually to move house, it’s for a refinance, top-up etc. during covid there were a lot of mortgage holidays etc and that’s probably reflective in that data.

RBNZ Stats. There is a spreadsheet you can download on this page.

https://www.rbnz.govt.nz/statistics/c40-residential-mortgage-lending-by…

Gives a breakdown of all mortgages. Total borrower column for March 2020 to March 2022 totals to 558000.

Yes some of those may be loans originated after March 2020 then refinancing with a different lender. But not too many in a tight time period of only 2 years. IMHO mostly new loans and refinancing to take advantage of lower fixed rates that were on offer.

7% on the shore. I can't wait to see how my favourite local spruiker spins this. Unsurprisingly he doesn't seem to be in a hurry to send the weekly update...

The commercial banks will have their say in all of this. They're already pricing money at much higher rates than the OCR so that in itself will slow things down. They need to manage expectations otherwise they'll be caught out. They'll be choosing very carefully who they lend to & probably have been for the last 6 months. How much of all this is noise & how much is reality? Only time will tell. I'm picking 20% from peak (Nov 21) & I'm hoping it will take another 18 months to play out. I can hope.

Bernard Hickey on tv interview the other night:

"A global recession next year will have the RBNZ scrambling to bring the OCR, and thus mortgage interest rates, back down."

Many other economists, that don't seek the limelight like the melodramatic bank economists, think the same as Bernard.

My money is on Hickey.

Just who are the ‘many other economists’ ? I can’t think of any.

Bernard is saying now, what I have been saying for 9 months.

A handful have also been calling this in Australia..

None of the commentators who were ahead of the pack and saw the wave of inflation coming seem to agree. Bernard still sees inflation as "transitory", despite that fact that even central banks gave up using the term.

All of the people I read/listen to who predicted the wave of inflation we are now suffering through all seem to agree it will be more persistent, and many even predicting we will need to see positive real interest rates to get it under control. It surprises me that people still think inflation will magically disappear now that its firmly embedded in expectations.

The idea that central banks will see a weakening economy and drop rates just smacks of recency bias - Central banks have done this, over the past decade, as when the economy slowed they feared a deflationary spiral. But what happens when inflation persists through an economic slowdown?

People are ignoring the bigger picture shifts that are underway. The last 20 years of deflation were largely the result of bring a huge portion of the worlds population (India/China) into the global economy. Covid and now the Russia/Ukraine situation have highlighted the risks of this outsourcing model- and when combine it with the shifting demographics and rising incomes in China, this deflationary pressure will be considerably subdued over the next 20 years.

I don’t agree.

what say we get to April 2023, NZ is officially in a recession. House prices have dropped 25% from peak, and the OCR is at 3.5%. Unemployment has risen to 7%. The CPI has dropped to 3.5% - although demand has been sucked out of the domestic economy, there is still some ‘imported inflation.’

At this point I think the OCR starts getting cut. Remember employment is part of the RBNZ’s mandate. If the OCR isn’t cut at this point in this scenario, then unemployment risks rising to 9 or 10%.

Btw, I think imported inflation will have dropped significantly by this point, as most of the world enters recession. There will be downwards pressure on price of fuel etc.

Also remember there’s an election next year, and don’t for a moment believe the notion that the RBNZ is truly independent.

If unemployment is ‘only’ about 5% by April 2023, then yeah perhaps there’s less of an argument for cutting the OCR.

Yes I like Bernard but hes got this wrong again. 12 months ago he was one of those considering negative OCR or close to zero for some time.

In your opinion he's got this wrong. Only time will tell.

A recession doesn’t mean inflation will be tamed and therefore interest rates will come down. Do you see a scenario in the world right now where things are gonna get cheaper anytime soon? Um the war isn’t ending tomorrow, China isnt eradicating Covid tomorrow either. Germanys PPI is at 33%. Food scarcity and famine are a sure thing next year for many nations. I don’t se how a recession in little NZ is n going to halt our inflation and bring our interest rates down this time round.

Recessions, especially if they are deep ones, suck demand out of the economy. All things being equal, prices fall.

If recession is widespread internationally, this will also be a headwind for fuel prices that will mitigate the inflationary pressures on fuel coming out of the war.

Imagine how much destruction that might be required to reduce aggregate demand to the level you are insinuating. And if we have that level of destruction, do you have faith that RBNZ at the flick of the OCR switch can turn things around again (honest question?). All I can see is a very wobbly Orr walking a tightrope that I don’t think he has the skills to navigate successfully.

And just how severe will the damage be to markets and the economy to reduce aggregate demand to such a level that inflation doesn’t go right through the 1-3% band and become deeply deflationary. If Orr can pull it off in parallel with the rest of the western world…I’m going to be thoroughly impressed! 🙏

And if we have that level of destruction, do you have faith that RBNZ at the flick of the OCR switch can turn things around again (honest question?).

No, I don't think they can turn things around at the flick of the OCR switch. But they will try, with one of the only blunt tools they have and know.

When I make my comments, I'm not necessarily saying that what I think they will do will make any difference. These comments are predicated on their past and present behaviours, as well as their mandates.

It surprises me that given the known behaviour of our governments and RBNZ over the past 20 years, people suddenly think that they WON'T try and stop the freefall of our housing market and economy.

In my scenarios above, they would probably only be able to stimulate the economy significantly if they made deep and repeated cuts to the OCR, bringing it back down to 1% at the highest. Little token cuts back down to say 2% would make little difference, but that's what I think they will do, given that inflation will still be 'in the room'.

I realise mine is a very minority view, and I could well be wrong. I think JFoe aligns with my view, and if you go to Macrobusiness you will see a similar view to mine represented by their lead writers and economists.

People here can take or leave my view, it doesn't bother me in the slightest. I'm just putting it forward, FWIW.

Only time will tell if there is any validity to my view.

Agree with you HM...

Always find it surprising how DGMs think the Govt/RBNZ are going to sit back and let the market crash...

They’re walking a fine line trying not to pull the handbrake too fast, let mortgages roll through to a rate not too high to not let the market crash. Seems to be all they have at the moment, all indications suggest 3-4% OCR early 2023. Hard to say where it will land but available credit will be a fair way down from the peak by then if that’s the target

The conventional wisdom is to pump interest rates, let the market sour a little, maybe raise unemployment to 5-6%, and see how it plateaus.

BUT

The Storm clouds are global. The RBNZ know this, and should things get worse internationally, the conventional wisdom plan is out the window.

Basically, we have economists and accountants trying to respond to far more complex, and unreliable scenarios.

good comment

Gobsmacking, really

I always find it surprising that people believe the Govt/RBNZ are somehow able to prevent the market from crashing.

It implies that other governments and central banks throughout history have just decided to sit back and watch their economies collapse.

Yes it almost sounds like desperation to me rather than analytical thought.

ie ‘if the central bank doesn’t save the market my investment portfolio is screwed’

As opposed to ‘I am going to actively manage risk and remove the unknown behaviour of a central bank from my decision making’

All you have to do is look back at history and see what the RBNZ & Government have done with NZ property over decades... why would they stop now? There's never been more vested interest...

Yes, I obviously agree.

Continue to hike the OCR aggressively up above 3%, while the housing market tanks, would be totally counter-intuitive.

Knowing how incompetent they are they probably think there will only be a mild housing market correction, and that the market can withstand aggressive hikes...

I think you are confusing cause and effect here.

And I also think you vastly over estimate how much control government have over the housing market.

As I’ve pointed out elsewhere, it’s a situation where you don’t want to be Talebs Turkey - but that is what you risk with this line of thinking.

How far back in history are you going Nifty?

And the perma bulls who assume that government and RBNZ will always save their bad investments remind me of Talebs turkey! 😂

I don’t disagree…just providing a contrarian view for consideration.

What happens if the RBNZ are now scarred from 2020-2021 knowing that emergency interest rate cuts only increase financial instability in the economy…as opposed to promote financial stability? They know dropping rates in a manner they did causes prices to rise 30% p.a.. Are they foolish enough to do that again? And I doubt they will remove LVRs this time…so in an economy in recession, with rising unemployment and no wage appreciation (assuming deflation) where are the buyers coming from to stabilise/increase prices?

As an observation, while living in the US as the bubble burst there, price’s continued to fall as interest rates dropped. Assuming that dropping interest rates will stop house prices from falling is a false paradigm - it’s a potential sign of recency/confirmation bias that past performance = future outcome. If enough people see others taking significant losses in the housing market this year, people won’t be rushing in to buy as interest rates fall because the psychology of the market has changed. Then again, kiwis might just be a very special bunch who are forever optimistic about future price rises, regardless of the economic/market conditions. Or perhaps we will find that we are the same as everyone else who has experienced the level of euphoria that we have in our housing market.

The book Tipping Point by Malcolm Gladwell comes to mind. Sometimes groups of people unexpectedly change their behaviour. Knowing when that is happening can be hard to see at the time and the cause uncertain. But afterward it appears almost silly to have not be able to observe the change at the time. Perhaps we are at a tipping point?

I don’t think cutting the OCR is anything like a silver bullet. I / we know it’s profound limitations. Cutting it next year, in my stated scenario, would offer *some* support for an economy in deep recession, and perhaps some is better than none.

I think you, but not everyone here, understand that when I say the RBNZ might do this or that, I am not necessarily saying that’s the *right* thing to do.

Carlos was saying yesterday that the RBNZ should hike the OCR 100 BPs. I actually agree with that. Do it once, do it right! Do I think they will do that? Not a chance.

This article in today’s Herald below aligns with a lot of my thinking, although I think one flaw in it is saying demand side factors are not an influence on our inflation picture - maybe far less so now, but certainly they were when the OCR started hiking.

But certainly at this juncture, supply side factors are much more influential and it’s very arguable to what extent hiking the OCR will quell inflation. At the same time, it could significantly contribute to throwing us into recession:

https://www.nzherald.co.nz/business/david-mcleish-what-if-rate-hikes-do…

Interesting times ahead. Especially next 6-12 months. I just wouldn’t put much faith in deterring central banker behaviour based upon the last few decades. I’d be more looking to the 1930’s-1940’s to see what they did. The likes of US have war time debt levels and walking a tightrope between deflation/inflation spikes. The behaviour of the likes of the Fed might catch a few people off guard, who think 1980-2020 central banker behaviour what should always be expected. That trend may now be a thing of the past.

if rates come down its means that houses have come down faster and further than expected, ie a global asset bubble bursting lead by real estate and equities. OCR cuts will not reflate the bubble, but may help those who manage to stay in the game. It is not a time to take risks or overpay for assets like first homes.

A recession eg lower gdp numbers is likely, from lower demand in the economy. However, it doesn’t mean prices will drop because global supply of goods remain constrained. Base inputs like energy eg fossil fuels are constrained. Food supply is down eg Ukraine Russia, fertiliser tripled costs resulting in lower yields globally. So inflation will run hot. Reserve bank will have to keep OCR up and hope to run inflation 4% if lucky. Stagflation.

We are facing both demand and supply issues here. In the past, supply was hardly constrained. That’s why this time is different. It’s not the one dimensional response oh gdp is down let’s drop OCR and stimulate economy, send out some checks, tax cuts etc. Hello… inflation is running super hot due to limited supply! And believe me, if govt thought they could fix these they would have. These are driven by wars, ESG climate change, Covid policies.

Choose a recession or 6% inflation in the economy. There’s a reason why reserve bank targets 2 to 3% inflation as a policy target.

Great summation RR, bang on.

I read somewhere that climate change is like a 200bps charge on the economy....

the Reserve Bank also has employment and financial stability mandates.

For sure. You can add into this mix that China pursuing the zero Covid strategy is impacting supply chains for pretty much everything.

Scarcity for any product invariably means a bidding war for components or materials which is exactly what we are seeing in construction and a slew of consumer goods.

With RBNZs inflation mandate it seems inconceivable we don't have further rate rises.

What I find slightly interesting is that up North agents are no longer suggesting auctions as the optimal way to sell. This is driven by slow mortgage lending decisions limiting the pool of potential buyers. Difficult to believe its not the same in Auckland.

Looking at the cycle in the UK it also seems likely pleasant places to live within a couple of hours of Auckland are likely to fair better than Auckland itself. I.e. the wave takes time to ride its way out or back.

There is a view that the central banks will need to cause demand destruction to beat inflation back.... that means deep recession for those kids who are in their 40's or younger.....

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.