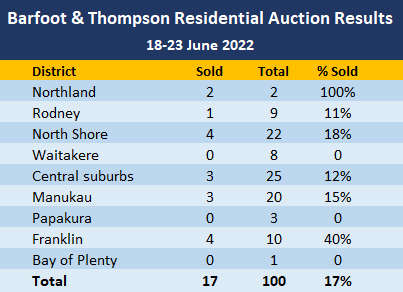

It may have been a short week leading up to the Matariki holiday, but there was an increase both in the number of properties offered, and the overall sales rate at Barfoot & Thompson's latest auctions.

Auckland's biggest real estate agency marketed 100 properties for sale by auction over the short week of 18-23 June, up from 80 the previous week.

Of those, 17 were sold under the hammer giving an overall sales rate of 17%, up by a smidgen from the 16% sales rate achieved the previous week.

As usual there was considerable variation in the sales rates around the Auckland region, with Franklin properties having the highest sales rate at 40% and none of the Waitakere or Papakura properties selling under the hammer.

The table below shows the district results, while details of the individual properties offered at all of the auctions monitored interest.co.nz, and the results achieved including the prices of those that sold, can be viewed on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

50 Comments

Just a blip, just a blip, it's ok the rapture is coming everyone relax.

No the markets just in a itsybitsy little gully right now.

It could go either way. Much of our prosperity now is funded by notions that the system provides security and stability to us, today and in the future.

We now have a roadmap that says the planets going to catch fire in what might only take decades. If that's actually true, quit your job now and go enjoy the world while it's still mostly in one piece.

We clearly have the budget and ability to make a nice earth, but we still waste it entertaining ridiculous notions like a war in Ukraine or fast fashion.

Everyone's got to get a slot smarter, a lot quicker.

"Much of our prosperity now is funded by notions that the system provides security and stability to us, today and in the future."

Pa1nter, this notion is not whotout any basis but comes from the action of RBNZ and government, which have repeatedly confirm by their words and policy that come what, will support the housing ponzi.

May be because is the main, if not only economy in NZ.

Sales rates may be up.. but this from a oneroof ray white property auction report suggests the sales prices are 'very' low...

A three-bedroom deceased estate in tidy, original condition on Antsy Place, Mangere sold under the hammer for $740,000, 40% less than its $1.225m ratings valuation, despite five bidders competing. A three-bedroom house in Belleek Close, Weymouth, sold for an undisclosed sum after bidding paused at $715,000. It had a CV of $900,000.

Here is that Antsy Place property:

https://rwmanukau.co.nz/properties/sold-residential/manukau-city/manger…

A full section too but unusually shaped. Still looks like a good buy. Probably a sensible decision to sell at this price, especially with five bidders present. A good litmus test of current expectations.

At that price its a terrible investment

Assume it yields $700 a week, 52 weeks a year, and rates and insurance total $5000, and no maintenance or other expenses.

4.2% return before tax with plenty of downside risk, yuck.

Not too terrible. Before the tax changes and when term deposits were a bit lower that return would have been considered pretty good. Most landlords would exclude the deposit from the calculations. That's the actual investment, say 150-200k. With inflation on top of that return that deposit figure could get a good return or keep up with inflation.

The trouble now is no one has any idea where interest rates will go.

You will not lease it long term at 700. at this price for this house you will only get trouble

A 3 bedroom / 2 bath townhouse in Pakuranga near good private college was up for auction, expecting 1.4 million but when auction failed were targeting buyers over 1.3 million and now is listed at 1.185 million being fully aware that will be negotiated ( may be ready to sell at 1.1million) but still high for a 50 year old townhouseand why this expectation, only because Auckland city council has been over generous with CV of 1.5 million which is on cross leased land ( not even free section).

Auckland city council went for very high valuation to get more rates ( cannot increase percentage so increase the value) and owners were happy to see high valuation in paper even though were paying extra in rates.

One million is also a good price for that townhouse but some may be influenced by CV and may feel that 1.1million is a deal.

Cookies are crumbling but FHB having already missed the bus are trying to jump as the emotion - FOMO was so strong that it still plays in their mind but that too should soon fade away.

The GV reflects the hubris in the market mid last year.

Your comment about council increasing GV to get more rates suggests you should learn more about the rating system before commenting

Agree. I am not an expert and comment what I observe without twisting.

If not for rates, wonder why Auckland city council was so generous with valuation.

Because those were the desktop market valuations for the properties at the the time the valuations were carried out.

The council doesn't carry out the valuations to increase rates. It carries out valuations to find out the market valuations to proportion out the rates (its net expenses) across the properties.

The market rates determined by us the crazy participants in the market for houses, not the council.

It will be interesting to see if we have a long recession.. where we have vastly reduced house prices and incomes - the council will go back and revalue houses, reproportion its expenses accordingly and reduce its overall expenses to meet the market?

It will be hard.. it is the reason councils (and government) should have borrowed less, been more careful with salaries, and valuations and saved money in the good times. So the bad times are easy

You can always apply for a revaluation. You'll stick out as the poorest place though if you go to sell.

But I think to be clear since it still looks like you don't fully understand RVs and rates. The amount thr council receives in revenue from rates is fixed and goes up in its yearly increments which Goff had vowed to be 3-3.5%.

To get uoyr rates bill it is basically the RV on your house devided by total housing stock value multiplied by total residential rate revenue.

Our rates went up by 'only' $15 this year due to our RV proportion not increasing as much as others and that component being a negative contributor to our rate bill

Council rating valuations were set as at 30 June 2021. This was top of market, or near top. Values have come down since then.

While upping the cvs doesn’t directly = paying more rates , higher cvs make people feel more wealthy and , I think, less likely to push back on rate increases in general. So I agree it is a tool of councils to increase rates, just not in the way some people mistake.

Oh and Happy Matariki.

Yesterday in Tauranga, Eves auctions were 0 from 12 with only 1 bid placed during the session.

The atmosphere in the room must have been riveting

The poor auctioneer would be sweating rivets.

They earned a lot last couple of years. They still getting paid for not sold as well.

Not enough Adam's in the room eh?

It's been interesting seeing main stream media ramping up DGM house articles... the complete opposite to what we've seen over the years

It's what the media do... sensationalise it.

Whatever gets the clicks...

17% sold. Still terrible.

17% and 17 sold in total how can anyone put a good spin on these results

It looks to me like 70% aren't even getting any bids so if one were very keen to sell it would need to be communicated clearly to buyers in the marketing phase.

It's no good indicating you are desperate to sell and then advising offers over the current RV value will "be considered".

With any house that is less than very desirable it would likely be best to hunker down for the next three years if you can afford to.

Oh and if you do get an offer that gives you a good return, take the money and run. Now is not the time to be greedy!

Another townhouse in Botany ( street off botany road) had an auction last weekend on site but as no registered bidder, had to pull out though had the usual open home before the auction, hoping that some will register but alas !

CV 1.4 million ( generous Auckland city council and the very reason for high expectation) . Now expecting 1.2 million or may be 1.1 million as have asking price just little over 1.2 million ( keeping room for negotiation).

Many may feel that is bad but if one sees the bigger picture, is still good if it sells near around million as before pandemic it would have been between $800000 to $900000 . It is how one looks.

Yes, a few sellers don't appreciate a good offer when they see one. If you bought prior to 2020 and you get an early 2020 value offer you may be wise to take it. I am a bit of a pessimist when it comes to these things and have been wrong before though.

Agree with you ZS that now is not the time to be greedy. People who decided to "hunker down" at the start of the Irish crash regretted it. It took almost 2 decades for prices to recover.

Best to sell now, cut your losses, IMHO.

Better to sell at a 10% loss now than a 40% loss later. Things are going to get much, much worse.

Wow, sales rate is getting better by the week..

Death by a thousand (price) cuts

In for a soft landing according to TTP.

Lack of sales is a lack of oxygen for anyone owning a RE business. Hard to cover overheads with no income.

Time To Panic

As a former boss used to say, any landing you can walk away from is a good landing.......

Can anyone explain to me why property in Selwyn, rolleston, lincoln etc still holding its price quite well?

Doubt that will continue for long. Rolleston listings 341 on Trademe in a town of 20,000. Lincoln listings 144 in a town of less than 10,000. Listing numbers more than doubled. Most properties now listed with a price. Just six weeks ago very few named a price. Massive subdivisions opening into an oversupply. Hundreds of sections sold last year settling in coming months. Solid numbers of equivalent properties listed nearby in Christchurch. A single large local builder had over a dozen properties (and growing) waiting for plasterboard in April, didn't expect to receive any plasterboard until end of June. Glut incoming.

Rolleston houses are going for close to the RV, and lincoln has had too few sales for there to be any notion of sales "holding", no one knows what the market price is now as the interest rates are changing so fast. Selwyn is also a bit behind the curve, both on the initial rise in late 2020 and likely in the down turn.

Our politicians are making this country a basket case, the biggest investment in the last couple of years especially, happen in real estate.

And real estate has zero contribution to the upliftment of real economic growth in the country. It is not an industry that produces and exports anything. It just produces more and more groups of deceivers and tricksters which we know as real estate agents and bankers. Also more and more innocent kiwis are on a steroid called DEBT which they believe is the only scheme to get rich quickly.

Now is the time to wake up and work toward real growth which can only happen if this Ponzi gets bust and give a life lesson to property investors.

Back in 2019 people would often use the analogy of an aircraft gliding down to a crash landing to describe what was going to happen to house prices. COVID changed everything however the analogy still seems apt. The government and the people pulled back on the joystick hard. This was when I began to worry as what happens to an airliner when you do that? It stalls and crashes usually.

That house at 8 Antsy would have been worth about 350k in 2009, where have wages gone since then inflation wise.... thats what its going to be worth at the bottom, its all relative to incomes and DTI levels will be enforced by RBNZ as soon as they can..... they will be no rebound.

8 Ansty place ,@$740k sale,

From Infometerics, median household income in Auckland 2009 -90k ,2022- 146 k.,

So on household income,lets say it was 360k in 2009, 4x HI.

THEREFORE 146k household income 2022, X4 =584k value in 2022? That leaves a long way to fall yet.

Yes but relative to current employment, expectations of recession and rates dropping (once recession occurs) etc, imho if i had sold a few at 1.2 mill i would not be scared of grabbing this one, as a FTB , maybe less, its always going to be a shitter as the site is not suitable for dev, its a gd first home...... we are just arguing about the price.....

Agree. Will get back to where it all began price wise. a few of the US investment groups are picking a long shallow recession this time.. so there will be no green shoots of an uptick perhaps for a few years. In that case people needing to sell will face a lot of competition to market to an ever decreasing pool of buyers who only want bargains. Fhb's will rent til prices start to rise.

Some years after all this fall prices will rise again .. human nature will mean history will repeat itself.. and will will convince ourselves it will all be different "this time" lol.. we are a funny old species

Yes its all about teaching your kids about the the economic cycle (that the fed is now being FORCED to recognise) things happen slowly if you follow financial markets...... easy to read.

It's going to be ugly when everyone realises our rocket to the moon is actually The Challenger

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.