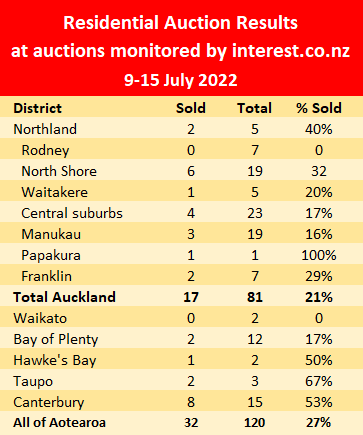

Residential auction activity continued to grind lower last week (9-15 July), with just 120 properties offered for sale around the country at the auctions monitored by interest.co.nz.

That was down from 175 the previous week which was itself a very low number.

Of the 120 properties put up for sale last week just 32 sold under the hammer, giving an overall sales rate of 27%.

That was down from 31% the previous week but within the recent range, which has bounced around the 25% mark for several weeks.

With winter now well and truly upon us and this week's announcement of higher than expected inflation with its likely flow-on to further hikes in mortgage interest rates, the atmosphere in the auction rooms could remain subdued for some time.

The table below shows the district-by-district results from all of the auctions monitored by interest.co.nz last week.

Details of all of the individual properties offered at those auctions including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

111 Comments

In this, a buyers market, sellers are largely exposed to buyers who are patiently watching for opportunities, that

they perceive, represents sound investment value - (que the smart money).

Rapidly declining prices is ample proof that the Hare is now chasing the Tortoise to the bottom - wherever that is......

https://www.stuff.co.nz/business/129305553/house-prices-will-take-back-…

https://www.stuff.co.nz/life-style/homed/real-estate/129312662/nz-prope…

There is no such thing as a Bargain in a Falling Market.

Just go home, don't bother with Auctions, sit tight, and Wait Wait Wait.

You will be rewarded for your Patience.

This is the worst advice I have ever heard.

Look for bargains and buy where YOU perceive real value. Timing the market is a fools game.

When no one else is buying will be your best chance of finding a real bargain.

Yeah ok. Well I don't personally perceive value anywhere and all homes are overpriced according to ME. So I won't buy, thanks.

I see your worst advice, and I raise you some (March 2021):

https://www.1news.co.nz/2021/03/24/property-commentator-ashley-church-p…

But one property commentator is urging anyone thinking about taking the plunge to get in quick as he expects house prices in New Zealand to double between 2020 and around 2026 or 2027.

Ashley Church told 1 NEWS it would be "nonsense" if anyone had been advised to wait for a dip in prices.

"It's just the wrong thing to do," he said.

"The boom is here for a while."

---

That was broadcast on 1 network news for the benefit of the sheeple wondering if the they should load up on 30 years of debt to buy

Timing is everything - but you don't need to worry about that any longer as when prices finally stop falling this market will stagnate for years

If you buy now by the end of year your deposit would be gone.

Prices are not only falling. The falls still seem to be picking up speed.

I think there is the odd bargain out there, but those might still seem like bad deals once they're in the rear-window mirror, especially if the OCR peaks higher than expected (which seems like a very real risk).

"Timing the market is a fools game" is a tired truism that has passed its expiry date.

"Timing the market" in property is very different to shares - you just can't DCA (dollar cost average) in ....while it's used by the property spruikers to spread FOMO ...however I would be, if I was buying, quite happy just to wait .........pass the popcorn thanks.

House prices are tumbling only people buying are selling in same market. In Auckland especially, prices were 12 x average wage couples yearly income for a 3 bedroom box on tiny section, this market has a long way to drop before hitting bottom and then will stay there for years depending on rates and inflation but all the speculators we certainly think twice before buying again.

Hi Jamin,

This is the worst advice I have ever heard.

You are certainly correct about that.....

Retired-Poppy (known as "Crash-Crusader") is the undisputed champion of giving dreadful advice.

TTP

You need to sharpen up fella, before having another troll, it wasn’t RP who gave that ‘advice’.

Have another read.

😝

Buyers should be aware now that they are trying to catch a falling knife. Best for many to sit out until the carnage is over, if its an option. Who knows when that will be given the need to tame inflation.

It seems like yesterday that the spruikers were spouting on about how this scenario “could never happen” and how stupid we all were for not pileing into the housing market to make our fortune.

I slept a solid 9hrs last night.

Well, the "spruikers" did have a good 3-4 decades of being right.. and they worked extremely hard at their narratives!

Pretty sure Orr is still running his Funding for Lending Program aimed at the Retail Banks. So.. yeah.. don't underestimate the power of the Ponzi.

Well done, Zack, on identifying something they have actually worked hard on. Most of them here in NZ do not seem good for much, other than watching their tenants do the actual work.

You have been asleep a lot longer than 9 hours, sounds like years to me.

Oh great, still a few around I see.

Feeling pretty good about sitting back and seeing more PBNs turning into specific asking prices in our next suburb of choice. Of course our current place will walk back a bit, but not by as much as they will. The real question will be how much interest costs on the extra mortgage will hurt us in the short term if we decide to make the jump?

Ditto. Even where rates are now it limits what seems prudent to take on, much less thinking about where they might be in 2 years time.

Yea, I'm mindful that my current mortgage servicing costs will be a lot higher when they come off fixed in two years time. If they have a seven at the front, I can live with that, but if I take on more debt that also ends up with a 7 in front of it, that's probably game over.

Households are going to face a real liquidity crisis as more and more mortgages get refixed, and there's a high chance the RBNZ will be as bad at responding to that as they are were to our current problems. In fact, given the heat they are copping over overshooting, I'd say that we'd see at least six months of huge undershoot before we saw an easing in their approach, even if things have totally ground to a halt (and they will).

There's no other way around this but for prices to fall and keep falling a long way until those frozen out can get a look-in. Otherwise there simply won't be any enough borrowers entering the market to fend off a credit crisis.

Even a 50/50 mix of 2 year and 5 year starts you at nearly 6.25%. Starting with a 7 doesn't seem unlikely. Even a DTI of ~4, which I had long thought ok, starts to seem tight if you're thinking about P+I repayments being ~11%.

That said I can't believe that swaps didn't move sharply higher on the back of yesterday's inflation figures.

That's my scenario, provisional DTI of circa 4, half of said debt I already have at a low rate, but the additional half at double (or possibly triple) the current rate is going to spike the average - and then if the whole lot comes off fixed into what is still a high OCR environment, then even a DTI of 4x becomes totally bonkers. It's still demographic-changing, family-planning changing levels of servicing costs, alongside all my other living costs which will have a couple more years of inflation by that point as well.

People do not understand what is coming and what it is going to take to fix this.

I think another down-cycle in interest rates after the economy tanks will do some of the fixing (the inverted yield curve seems to corroborate this). I think the rest will be a near-term drop in house prices (sadly not of the magnitude many commenters are hoping for) followed by a decade or two of limited price growth.

What if the economy tanks but inflation stays stubbornly high? The we won't get the down cycle in interest rates.

That's when the NZD will do the heavy lifting (i.e. depreciate). Once there is some slack in the economy to prevent a wage->price spiral I think you'll see the Reserve Banks look through 'external factors' and tolerate higher inflation.

I think this is probably right. But I also think there's a nonzero chance that inflation is more stubborn than currently forecast and that rates will have to go higher in the short term. In the first case, upgrading now would be ok; in the second case, it might get really ugly.

When the first Mainstream Bank starts to sell a 7% mortgage it will be time for the First Scroll to be opened . Once again it will be Revelation many will Despise, Ignore, Ridicule.

But those who Listen will be able to prepare and survive.

The Second Scroll will be opened once the Mainstream Banks start to sell their 7% Mortgages at a shorter term. And that Revelation will be even more difficult to believe than the First.

Let's Hope and Pray the messenger is not sent off to an early Execution like the Prophet.

The deflating of the biggest Ponzi in NZ economic history is about to start, and every new OCR increase is another push towards the edge.

Or we are close to hitting the peak in inflation and everything will be just fine.

Or we are close to hitting the peak in inflation and everything will be just fine.

Inflation is at 7.3%, well over double the upper limit for the RBNZ. Even when inflation does peak, we will still be a very long way from our happy place.

The amount of hopium that people are drinking is nuts on this stuff. Let's give a breakdown of the best case buyer right now for perspective.

Let's give a scenario, an updated version of one I posted in the past. So a young family wants to buy a home. Our best possible FHB, a software engineering team lead on 140k with a second job as an army reservist for an extra 8k per year. Stay at home wife, one kid under 2. Let's even give 4% kiwisaver match and set his rent for 750 a week (for a decent home, you will pay this). Still got a student loan too, so calculating that is something like 3100 per fortnight with say 300 per fortnight for reservist pay.

So just under half of that income is going to be going to rent. Food at 350 per fortnight, fuel at 60, power/net/phone at say 500-600 in winter. Even then, under best circumstances, that is maybe 700 per fortnight to save for a house plus kiwisaver of ~300-400. So maybe a 1100 per fortnight saved including kiwisaver.

To hit a deposit, assuming a good 4-5 years post university, you can only save about 28.6k per year for a deposit on the worst houses in a metro. Pushing 600k in wellington, 700k in auckland. They need to save for effectively 5 years without fail or disruption to buy an entry level 3 bedroom place in a terrible area. Banks ain't gonna give you a mortgage for less than 20% down now.

Not just that, a 500k mortgage on a terrible place currently at 625k is going to cost nearly 1500 at 6% interest rates. It will be 1630 at 7%. No one with less than a top tier income can afford that.

The utter delusion of anyone pushing the narrative of price falls stopping now. We are going down for a while yet.

Couldn't the mother work to increase income/savings? Why don't they already have savings accumulated? Banks are doing loans under 20%... these would prob be prime candidates for this given Mr employment.

Childcare costs + transport costs are often essentially driving you to net negative return on that work.

Also a mother at home was the norm until very recently. Let's even give them a baseline of savings of say 60k. They still need to save another 2-3 years to get there.

And even then, why should parents be forced to buy a property for their children with their collective hard work to make some property parasite richer without doing the work?

It's been quite a while that FHB's in major cities have had to have both parents employed to make it work...

You're also assuming this couple has zero savings already aswell... one would question why if home ownership was their goal.

It's certaintly not easy, but this isn't new

It's been quite a while that FHB's in major cities have had to have both parents employed to make it work...

That doesn't mean that the costs of doing so actually stack up anymore. Booming costs (e.g. two separate cars being fueled, insured and run daily) on top of daycare fees mean that for more and more people the numbers no longer work, especially given the hours you can work being so heavily restricted by commuting.

We're not talking about whether it's new or not, we're talking about whether it actually makes any sense anymore. We're past the point where two parents working is getting ahead, we're now at 'make ends meet' territory because we've normalised hyper expensive houses in our cities and just keep expecting people to borrow more and more. That doesn't work anymore.

Well said

I guess it depends how badly people want to live in places like Auckland... is the trade off worth it? No doubt that's why we so heavily rely on immigrants coming here to live, they've seen it as being worth it compared to where they've lived. Kiwis seemed to think it was worth over the last couple of years too...

It is literally the situation I am in and we did the math, it wasn't worth her working for less than 85k after all the costs. But the emotional/developmental cost is the unseen part here, of missing your children's development so you can make powerpoints for 40 dollars an hour. Picked up soldiering as a second job to save a bit more.

No bank of mum and dad because we are both from poor working class backgrounds. Cut costs to a minimium, invested in electric tools (rather than any petrol) and a home gym, no subscriptions to anything. Brew my own booze etc. It is just the attitude you have to adopt to save money.

The childcare gets a lot cheaper and easier once they turn 3.

I agree its not really worth going back to work full time before then.

Its interesting though. If childcare was tax deductible then the numbers would stack up a lot better & more more woman would go back to work. For example woman 1 earns $90,000. Her after tax income is $68,129 on the current system. Child care costs her $30.00 an hour for a 44 hour week which is $68,640 per year. So she stays at home with kids. If you can deduct child care expences she would only pay tax on $90,000-68,129 = $21,871.00. PAYE on $21,871 is $2187.10. So her after tax income is now $90,000 - $2,187.10 = $87,871.29. It is now in her interests to go to work as her after tax income is $87,871.29 and childcare costs $68,640.00.

This is why many women get stuck at home even if they don't want to. The numbers don't add up. It is also why our birth rate is collapsing as many woman would like a kid however they are not willing to give up there career to do so..... All in all you would think some conservative from the Mississippi had written our tax code??

100% agree. We were lucky enough to be able to pay for childcare out of pre-tax as it's employer-provided. Makes a big difference.

But can your employer claim the tax deduction? My understanding was childcare will be considered a non deductible expense... maybe I need a new accountant?

It sounds like it would attract FBT to me..... but I am no tax expert.

I don't think this would fall under FBT. I am pretty sure the second you try and deduct child care expenses you are breaking the law. If the company you work for pays for your child care as an employee they should be treating this as a non deductible expense.

TBH I've wondered that myself, but I don't know the answer. I can only say that it is definitely the arrangement available to all employees, and that I would be very surprised if it isn't above board, if through some kind of loophole.

.

Sponsoring child care is already part of working for families.

Family tax credit

This payment depends on how much you earn, how many dependent children you have, and any shared care arrangements. This is the most you can get each week:

Eldest child $127.00 Subsequent child $104.00

In-work tax credit

The in-work tax credit pays up to $145 a fortnight for families with up to three children, and up to an extra $30 a fortnight for each additional child. This is a payment for families who are normally in paid work. Go to ird.govt.nz/working-for-families to find out more.

Only low earners get this. If husband earns 100,000 and wife wants to go back to work and earn 90,000 they will get no child tax credits as their joint income is too high. So the wife is stuck at home with kids as it is in her financial interests to stay at home and look after kids rather than go back to work. NZ should allow childcare to be tax deductible, this is a win, win, win. The govt wins as they get additional PAYE from both the wife working and the nanny working in full time paid employment. The wife wins because she gets to go back to work and do what she enjoys. The nanny wins as she gets a job which is demanding but pays a lot better than the other minimum wage jobs.

Where are you that $30ph is par for child care?

"But the emotional/developmental cost is the unseen part here, of missing your children's development so you can make powerpoints for 40 dollars an hour."

We will look back in despair at selling the village and trying to rent it back.

Agreed. For 8 years now(got here in 2014) IT has been clear that New Zealand society only works for an ever shrinking apex of the society triangle. Unless they are married to wealthy spouses, or about to inherit, firemen, teachers, nurses, retail staff, and GPS cannot afford to live in New Zealand. They are simply cannon fodder to the capitalled Apex and trodden on by politics.. The politicians would rather flood the system with more off shore cannon fodder, than solve any problems.

Even to the quazi wealthy, if you have a couple of kids this system is unsustainable, unless of course you had kids so that you can talk to them on Skype. The housing market is NZs biggest problem, crash it now and build a society that is more sustainable.

Maybe they had medical issues, or their parents or kids did. Maybe they lost their money on crypto. Not all financial plans run smoothly ...

This is also very possibly going to be the position that many people who bought houses from 2020 - 2022 find themselves in - square one, zero equity, and that's if they're extremely lucky. So no savings or access to Kiwisaver is going to be a reality for more and more existing homeowners as well.

'but this isn't new'

ah there goes the schizophrenic Nifty1 again. One day the FHB's friend, the 'anti-spruiker', the next day quite the opposite. I'm starting to wonder if you are a troll.

'this isn't new' is frankly a ridiculous statement. It totally underestimates how much harder its become for FHB's over the past 3-4 years.

It's been unaffordable for a long time and it's obviously been getting worse. It's a surprise that some just seem to be realizing this now... and talking like it's a new phenomenon.

People have had to sacrafice to get into a home. Should it be so hard, nah... but the guy on $148k is in alot better position than alot and could make it work if they wanted..

Yes it’s been hard for a while, 10-15 years, but come on…it’s got much harder over the past 3-4 years

ah there goes the schizophrenic Nifty1

And you said calling someone a DGM was insulting...

Lol

Apparently it's not PC to say someone is schizophrenic anymore, It's still commonly used colloquially to describe someone whose viewpoints are all over the place, perhaps it shouldn't be.

Apologies if you have the condition.

Yeah and my appologies if you or anyone here has the DGM condition...

“Small family on $148k should work more for a home.”, lol this notion/nation is mad.

House prices in NZ must halve before they can reach sustainable levels. And they will ultimately do it, one way or another. You can cheat and suppress the forces of the market and the laws of economy for only so long. All asset bubbles deflate, sooner or later. And housing is no exception.

I doubt very much they will halve in nominal terms, but they might in real terms over say the next 7 years.

Before people point out the whole 'one income' thing, the flipside of two incomes now is five days a week of childcare. So of a second income of say $2300 net of SL and tax (around $80K for a second earner, maybe?), five days of childcare is going to eat close to $700+ of that in Auckland, plus the extra time and fuel required for a parent to do a pick-up or drop-off.

So all those extra hours spent commuting, working and not seeing your kid and you're only $800 a week better off in terms of disposable/saveable income, for a household income which is now $220K+ p.a.

Very strange that the FHB is a single income household. Sorry but this doesn't happen these days. Even if they had a kid, the software engineer you're talking about is unlikely to be shacked up with a gal who didn't go to uni. A more realistic scenario would have her working part time/30 hours a week and paying a bit of childcare costs.

An even more realistic scenario is them both working full time before they buy the house which they'll do before they have the kid... Contraceptives are free and plentiful, As a 30yo who recently bought a house, almost every woman I know has an IUD/on the pill. Of the people I know who have kids, every single one of them bought the house first.

BTW student loan is deducted at 12% of all gross income over $20k per annum. You're a fool to pay it down faster if you're staying in NZ since it's interest free. So that's $553.85 per fortnight for this guy.

Also, family money. Most FHBs have a bit of this. These guys are more likely to get something around the $1m range than what you're proposing even with the bizarre 2yo you've thrown in the mix.

In summary, this is a very strange scenario you've painted which makes things look a lot less affordable than they are. Add another $70k p.a for the partner's income, remove the child from the picture and throw in $100k gift from the parents and you'll have a picture that looks a lot more like what educated, well-paid FHBs are facing like your software engineer. The rest however....

Oranga Tamariki might get a bit upset if you simply 'remove the child from the picture'.

I'd rather not, you know, normalise the idea that millennials should put off having kids any longer (I was in my mid-30s), or that most FHBs have family money (that's a symptom of the problem).

But let's assume a more even split of income for a DINKY couple (say, 80/80) instead of 140/0. That would give our couple $2300 each a fortnight after student loan repayments. Assuming they get a family gift to get to a 20% deposit on your $1m house, that will cost them $2,000 at today's 2 Year ASB fixed rate; or around 45% of their net income, on an $800K loan, making the bare minimum repayments on a 30 year mortgage for what is probably a modest starter home.

But sure, if we ignore all the bits to the equation we don't like and assume everyone can just draw down on a gift from their parents, then sure, the problem goes away.

That sounds about right. Then factor in some pay increases as their career progresses, and the serviceability gets easier over time. I also think we'll be back in a down-cycle for interest rates before you know it. House prices won't do all of the heavy lifting.

If you're going to start factoring in hypothetical pay increases then let's also factor in the hypothetical child as above a few years down the line, six months of non-MAT earnings down the gurgler, the full week of daycare at $350 a week and the fact that their $800K mortgage will likely be covering an asset that is no longer worth $800K and they are effectively stuck.

You see how this not exactly a situation that I'm that keen on normalising.

The software guy is probably a nerd an would have hooked up with the first woman who came along. She got pregnant way too young. He may of worked super long hours and brought some bitcoin when it was crazy cheap an was once fabulously rich.

Now still quite well off. But has hidden most his real wealth from the wife incase she scarpers.

Lol at a nerd insult on the internet. What are you typing with? A football?

Von Metternich,

Why the Austrian statesman? An interesting post. It neatly illustrates the absurdity of our house market. There is no good reason why out of 92 cities studied by Demographia, Auckland should be the 85th least affordable.

My younger son's home in Auckland is apparently worth over $3m and though it's a perfectly decent house, that's an insane value. When we lived in Scotland, we were in one of the most expensive suburbs of Glasgow; Milngavie (millguy) where the West Highland Way starts and given the current exchange rate, you could buy almost any property there with that sort of money-say a late Victorian 5 bed. villa in a large garden. By the way, when i was last there in 2019, it boasted 8 different supermarkets, most of which are within walking distance of each other-but terrible coffee.

I don't know how we get there without major pain to many people-and our banking system- but somehow we need to have much more affordable houses-and properly built for a change.

Actually it's normal human behaviour in any crash of any asset. Denial until it's obvious you can't anymore, followed by fear (we are at the start of this phase probably, most still in denial), followed by capitulation (probably end of year if interest rates keep rising), followed by despair (2023-2024?). Despair phase is where people should buy and it can last quite some time.

Can you post the numbers for all of New Zealand please....

.

The crazy years of 20/21 seem to be over. Let's see if key players, investors, builders, agents, suppliers. earthworks etc return to normal.

A return to normal would have been nice. Say, a 20% reduction in house prices, slowly achieved by ONE rise of the official cash rate, then housing prices staying stable in nominal terms, but falling in real terms due to inflation. THIS would be a return to normal, after a few years of nominally stable house prices houses would have become much more affordable due to the price level being devalued by inflation - and this process could have been easily achieved with ONE raise of the official cash rate by 25 or 50 bps.

However, what we have seen is THREE steep OCR hikes. This, if left unchecked, will lead to economic disaster. Bankrupt banks, nobody can bail us out (we are not in the EU unlike Greece or Ireland). People who got lured in to buy homes by the ultra-low OCR rate of 0.25% just one or two years ago are now stuck: They face a liquidity crisis due to rising mortgage costs, they face negative equity, and thus cannot even move cities to find a new job, because they cannot sell their house. Mass unemployment may follow. Inflation may continue due to our currency collapsing, despite or because of the steep OCR rises, as our economy goes to shambles, facilitated by an incompetent socialist government and a mad central bank.

Thank you Central Bank of New Zealand! You've trapped people in a liquidity trap, and now you are hammering those trapped with massive interest rate increases. Well done! We are now facing a collapse of a relatively peaceful and relatively prosperous society, with much economic harm.

A house close to where I live, just sold for 12% less than RV. One and a half years ago, an agent told me that the GV was a meaningless number.

They were correct!

Oh dear the RE tells you whatever it takes to get the sale. I paid over $100k more than the old 2018 RV and was also told to ignore the RV. The house is ultimately worth what you are prepared to pay for it or in most cases all you can afford to pay for it so big difference.

Offered a $1m on a property they want $2m, but paid $1m for in 2017. The agent did a good job of bluff and bluster, but couldn't answer whether the doubling in price was due to work had been done to improve the property (they have done nothing) or was it just speculation on cheap debt (clearly). I did point out that money was not artificially cheap anymore and fast heading to being more expensive than 2017. Also suggested if they didn't make a call on reality they ran the risk of their cheap loan expiring and it being worth less than they paid.

Lets face it if you cant sell something in the last eighteen months, then clearly you have been to greedy.

Plenty of places in *trendy Auckland suburb goes here* which is still having new builds added to it (but many currently empty) all over the show are still showing with asking prices $300K above what they sold for in late 2020 - which is even then a bit after things had really kicked off post-Covid. So there is a lot of fat in some asking prices, or owners who just don't want to let go of the idea of making a fat gain for doing literally nothing but live in a house for two years.

I drove past my childhood home in a very working class suburb of outer West Auckland the other day and saw that three houses have been bulldozed to build a couple of dozen of the sardine slums of the future.

They are asking for $750k+ for 72sqm floorspace / 2 bedrooms on 55sqm of land with one carpark.

Just about choked, will be interesting to see what they actually get.

"Just about choked, will be interesting to see what they actually get"

It will be interesting to see what the bank gets "post foreclosure"

Is that West Coast Road?

Massey

Are we in a home owners market yet? or are we still measuring the section and doing the math?

12,200 Auckland listing and weekly sold in auction 17 houses. :)

Papakura going gang busters, 100%!!!

What do you mean? I have 3 apartments in a building I own there. I've had one empty for 3 months, no decent tenants.

He was Taking The Piss. 1 sale of 1 so 100%.

Oh right, gotcha. I totally missed that. Ta.

Time for the 'ol "Dutch Auction" ....the silence would be deafening.

Greedy vendors who have done nothing to the property since buying in 2016, expecting 2021 prices

The greed and "living beyond your means" in this country is mind blowing and just "crazy" !

Unbelievable ‘journalism’, article over at OneRoof saying that we are nowhere near a housing crash.

Apart from Wellington it’s not a crash yet, but it’s not far off one in many other locations.

unbelievable. The NZ Herald is one sorry newspaper.

Remember it is just one of NZME's outlets,hence why you need to take Hoskos forever positive property market views in context with the anti government stance he takes...he is part of the ponzi scheme..

NZME owns the Herald/One Roof & Newstalk ZB

Yep and I feel real good having cancelled my Premium subscription :)

Does Tim know that Wellingon house prices are crashing? ?

by tothepoint - d… | 8th May 18, 12:23pm

Hi Gingerninja,

We've had this discussion before. If you can buy a house at a discounted price close to the city in Wellington in xxx months or years time, then I'll be genuinely happy for you. But I wouldn't bank on it, because Wellington's a relatively stable market that doesn't tend to fall in price.

According to an "expert" those wanting to get the best prices for a Wellington property, shouldn't sell in this market!

https://www.stuff.co.nz/life-style/homed/real-estate/129306380/wellingt…

He's an NPC.

Couple of Observations

Sure auctions are not working right now 32 sold last week.... so 120-150 per month but if we look at sales in NZ for June 2022 - 4,721 sales. So just looking at auctions is no longer informing us of whats actually happening apart from the fact the buyers are not buying at auctions. Overall sales are much lower (less 38.1% year-on-year).

In the GFC I sold a place very early in the piece in Summer St ponsonby and rented something for a while..... very different market GFC to here, Rates dropped from a high of 9.85% 1 year down to 5% in about 6-12 months.) This time owners are sailing into the wind, with no OCR help from RBNZ and no serious tax help from Labour ... In fact Labour have done everything possible to detract from residential investment.

So who is even interested in buying here? Cashed up investors looking for SERIOUS bargains? FTB who want 2017-19 prices or less?

I am willing to bet most buyers / sellers are transacting in the same market, downsizing/moving cities etc.

During the GFC one of the best bargains I saw was a house at Onetangi valued at 3.5mil sell at auction for 2.1, happened early... sure its different this time BUT you cannot buy a 50% off pek property if you are not in the room.... I have seen people sell at huge discounts to secure cash in environments like this, the key if you are bargain hunting is being able to access a property visually , be mainly cash buyer... relationships with agents who know they need a sale.... I always feel comfortable buying old villas without an inspection as long as i can get under and in the roof.

Bargains don't come to you, you have to buy them, I spent 840k on an old wreck in the middle of the GFC from a couple divorcing, only one open home, they just wanted an unconditional buyer for personal reasons..... sold it 3.25m at the peak and spent max 35k on it, land value only.

Sure right now we may have a seller strike and a buyer strike but it will change real quickly. You will not score a 50% off sitting here.

Cashed up investors.. Me! 🎉

I'm starting to head out to view properties now. Want a family home upgrade and another rental.

Been building the vulture fund for the last three years. The carcass is starting to smell, but it will stink further.....kaaaaarrrrkkkk.

Question re: buying and selling in the same market - it’s not that simple is it? All things being equal you need to sell first, right? What happens if the ‘best’ price you can get for your property is way lower than 2021 peak and way lower than your expectations, yet the property you are wanting to buy, for whatever reason, does not go for much of a ‘discount’?

I think the notion of selling and buying in the same market is a bit oversimplified. I think it’s seldom straightforward or equivalent.

‘Restrictive setting’: ANZ predicts RBA will raise cash rate to 3 per cent before Christmas

ANZ has dramatically revised its interest rate forecast to warn of four more massive rate hikes by the RBA before the end of the year.

Selling a house right now is like selling a V8 Holden when petrol price is heading north..

From wikipedia on the Irish housing bubble... Some eerie parallels with today

A property price crash hit Ireland by the first half of 2009. It coincided with the 2009 recession as both had started to develop in late 2008 following the global economic slowdown and credit control tightening. By June 2009, it was reported that around 40% of the price escalation that had occurred during the property bubble years ("Celtic Tiger Part 2") of 2001–2007 had been lost. As of 2012, house prices are below the 2001 prices and more than the entire gain during the Celtic Tiger years has been erased

Here's hoping.

Agreed. Very similar debt bubble dynamics. Ours required 2% rates to really go stupid which they never did in Ireland. They also let some of their banks go broke. Hope we do the same.

They also adopted the Euro in 2002, so no longer had a sovereign currency to bail out their banks with.

That's a good point. It seems highly unlikely that the RBNZ would allow any bank insolvencies. Also, quite a few macroeconomists seem to think the US Federal Reserve will give up on inflation later this year. If that was the case then I guess we'd follow suit, and it would be off to the races again for all the asset markets.

There is no point selling a house via auction when there are so few buyers

Still lot of resistance in price fall.

Houses that should ideally be near million are still holding between 1.1 million to 1.2 million with expectation to get as near to 1.2 million as possible despite failed auction and offer forthcomming, still many are holding.

Is Wait it and Watch.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.