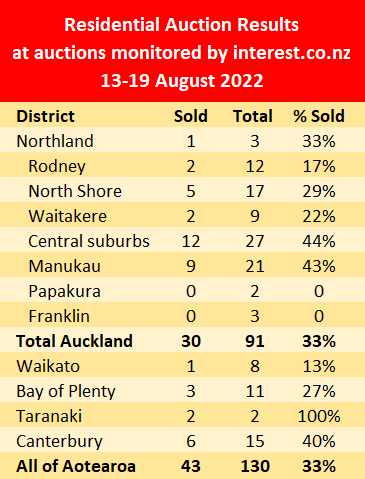

Activity slipped a bit further at the residential property auctions monitored by interest.co.nz last week.

Just 130 properties went under the hammer at the auctions we monitored around the country, down from 148 the previous week.

Of those, 43 were sold under the hammer, giving an overall sales rate of 33%, down a tad from 36% the previous week.

Auckland and Canterbury were the only regions where the auction numbers were in double digits.

Fewer Canterbury properties were offered last week and the sales rate dropped back to under half, down from 74% the previous week.

The table below gives the district-by-district results from last week.

Details of the individual properties offered at all of the auctions throughout the country that were monitored by interest.co.nz, including the prices achieved on those that sold, are available on our Residential Auction Results page.

The comment stream on this story has now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

43 Comments

Who is even buying at these prices? Who has the money?

Property junkies who cant kick the habit.

43 sold by auction across the country in a week - evidently not many people

The same people that have ALL the money. Some people are simply loaded and people that will be moving to NZ in the future will be the top few percent of the people in those countries with money. Hard to get your head around but some people have more money than they know what to do with it while the bottom 50% of the population struggle.

Some people are simply loaded and people that will be moving to NZ in the future will be the top few percent of the people in those countries with money.

Isn't it an urban myth that buses of Chinese will be scouring the suburbs of NZ willing to pay a king's ransom for houses?

I'm looking in nicer parts of Auckland. Very little on the market and it's actually quite tight, it's the average Kiwi who is going to suffer.

Almost at the end of winter and no crash has occurred.

It’s now about 10 months since the housing market started to soften. Through this 10 month period, prices have fallen at a much slower rate than they increased in the preceding 10 month period.

Further, auction clearance rates are up a bit recently.

All up, the market correction appears to be running out of herbs.

TTP

Pointy - appearances can be deceiving, your reply is pure spin (or just denial) - as I have said before just because it hasn't happened yet doesn't mean it won't happen. All good things take time......

It's the purest form of spin. What's most amazing is that his claims are completely contradicted by the facts. House prices have fallen faster in NZ than any of the other recent housing bubbles popping. 8 months after prices peaked here is where the each index from peak:

NZ 2021 -10.9%

US 2007 -4.1%

IE 2007 -3.6%

What's more, prices are falling close to as fast as they were rising before the peak. But once you look at it per region you find that the only reason prices have "fallen slower than they were rising" is that the peaks occurred during different months, masking what is happening in each region. Wellington prices peaked in Oct 2021 in the 9 months since are back to Jan 2021 prices. And Auckland prices peaked in Nov 2021 and are back to Feb 2021 prices. All other regions are following a similar trend, but peaked between 1 and 3 months later.

Hi Miguel,

Note that house prices have dropped by around 15 percent this year. Last year they rose by well above 20 percent (up to October 2021).

Further, if you scrutinise the data over the last five years, you'll see that house prices have increased by well over 50 percent. And that's before considering rental returns - which add to the flavour of housing investment.

So, there's little point anyone arguing there's been a crash. Just as there's no point trying to persuade us that black is white, or that night is day.

TTP

Why not use exact numbers?

Latest REINZ HPI shows latest index is 3814.

Prices peaked 8 months prior at 4281.

Prices 8 months prior to peak was 3756.

So 8 months of falls have almost entirely wiped out the preceding 8 months of price rises. Yet you said, and I quote:

It’s now about 10 months since the housing market started to soften. Through this 10 month period, prices have fallen at a much slower rate than they increased in the preceding 10 month period.

This statement is factually incorrect. Hence my comment.

Hi Miguel,

I've used nominal prices, because that's what most people understand - and what most of the discussion is based on here. Indeed, nominal prices are what most people go on when buying/selling houses.

But even if you choose to use the REINZ HPI (which is fine) there's been no crash. Price decreases since the market peak haven't even matched the price rises for the equivalent period prior to the peak. In fact (and perhaps unwittingly) you have verified that through your very own calculation!

It's absurd to suggest there's been a crash this year. There's been a correction - as was widely anticipated.

Like it or not, New Zealand's housing market is remarkably resilient. As has been noted many times here, housing prices are notoriously "sticky-down".

TTP

You seem to be using a new definition of crash - normally there is no consideration for what happened before the peak. Certainly when the stock market crashes as it does fairly routinely, not many are pointing out how magnificent the 5 year returns are still.

We all know that the peak to trough is not measuring most peoples experience other than the unluckiest people in the world, but that is a separate discussion.

I have to agree, the "crash" may be "faster" than other nations, but when you look at the upside going into it, it is not really a crash.

But I would also caution, the above sentence could still have a "yet..." placed at the end, as what starts small and slow could very much turn into out of control mayhem without much warning.

TTP, you are my favourite macro fauxconomist.

Still. Not really a crash tho is it and if you are not living in Auckland or Wellington it's even less so. Compared to many other things it's stills non event really. Sure things could be much worse in 6 months time when the OCR peaks but nothing is a done deal yet.

You are correct, no crash will occur, just a -35% correction to pre covid levels

No biggie!

Hard to test your tone on this but I'll riff off it anyway.

In an environment of increasing interest rates and declining prices, obviously correlated. I don't see how property investment is any different to taking a big pile of money and burning it.

We're just at the start too. If property was to say, hit a 24 month period of sustained declines, a lot of spruiking claims will be self evidently false and we could see a much larger unravelling as people realise "mate, you can lose on property!"

Well you would be wrong, you only lose money if you have to sell it. You are not burning a big pile of money, the money would be gone your house price will recover.

You are burning the opportunity to sell high, and instead be a bag holder.

Tim The Pricefixer is very careful to never define what constitutes a "crash".

Patience. -20% will be with us very soon.

You're right, much like that guy that never defines what 7% interest rates refers to....

It pretty much boils down to reasonable judgement, because there's no fail-proof or official definition of a "crash".

If two cars collide head on at 50km/hr, then reasonable people will likely call it a crash.

But if, as you open your car door, the wind catches the door so it hits against a concrete fence-post - scratching the paint and causing a small dent - reasonable people aren't going to call it a "car crash".

Use good judgement and commonsense - even if that's a lot to ask here.

TTP

There you are again, avoiding numbers.

“Welcome to Palmy Insurance, we can fix anything, including the price! How can we help?

…

A head on crash? No that sounds like a correction.”

Dunno about anyone else with good judgement and commonsense but moments before that head on crash, nobody is gonna be thinking “hmm no this is fine. This is not a crash.”

Not sure which country you are talking about, but meanwhile in New Zealand prices are steadily falling in a manner entirely reminiscent of a property market crash. Perhaps we'll get an amazing boost come spring and start to bottom out but I wouldn't want to be over-leveraged right now.

https://www.interest.co.nz/charts/real-estate/median-price-reinz

Rates still on way up only at the start of downturn, inflation is going to take a while to tame people have paid way to much for property over last five years, price’s will hit 2016 levels over next couple of years and if downturn is really bad who knows where we will end up. With these results looks like savvy people are just waiting as it is obvious to most house price’s have long way to fall.

Recent articles on agents leaving the industry, and FHB'ers in negative equity. More to follow. Lets remember circa 25000 agents got new jobs during the GFC. The retreating tide of cheap debt has just started to reach the regions so the correction as quoted by TTP will be much more widely felt in the next twelve months outside of Awkland and Welly.

More OCR increases forecast. Inflation rate in the UK and the US circa 8.5-10.5%, and both countries asking wether the real inflation rate is double that manipulated number. Will 2023 be the start of the eye of the financial storm...?

From the, There is only one cockroach school of thought..... multiple credit events coming our way curtisy of China property collapse and lockdown madness, European energy crisis and emergency gas pipeline maintenance (Yeah Right) situation, and the USA equity market correction which is just starting its 2nd leg down today. No Liquidity in the housing market means forced sellors are going to get hit real hard here.

House at the end of our road. 5 years old. Bit of land, double garage, 3 beds, quality build decent schools. One came person to the open homes, no bids at auction. Real estate agents plan to put a price on the listing to differentiate from all the others that are simply 'by negotiation'. It has a good rental value too. Owned by an investor.

I read enquiries for new build are down 80% too.

No point being involved in building or selling houses for the next couple years. I cant see why we need more immigrants when there will be so many real estate agents, mortgage guys, developers and tradies with nothing to do soon.

We are looking to build on our current site in the next 5 years. Went along to a showroom of a well known designer/builder. Sales person said inquires have dried up but building supply costs have plateaued.

Yep. Construction cost inflation like many other areas of inflation is dead in the water.

Perhaps a business opportunity for me as Open Home "padding". To try and put some pressure on real buyers, if there are any, for a couple of bucks a time I could do a circuit of open homes on the weekend, drag my kids along and make it look like we are desperate buyers full of "Oh please let us be the winners this time!" FOMO.

Its quiet out there...... too quiet.

Beginning to mid to late 2023 going into 2024 is just around the corner. I hear prices will take off then, The Fed has our backs 👀

Just as nothing goes up in a straight line, so nothing goes down that way either. No one can predict where interest rates will be in a year. That said, my guess is that the rising trend has recently merely stalled temporarily and that they are headed up further, perhaps sharply. Today's large stock market fall suggests as much.

Given that NZ house prices are wildly out of line with fundamentals (average income/price ratios), along with the continued upward pressure on interest rates, it is most unlikely that prices have bottomed. I suspect they have a long way to go yet. Not good for me personally, but very good for NZ society on the whole.

It is amusing that some here appear to think that the huge price rise in recent years is reason to think that they won't fall just as far or more. In most speculative markets, the opposite is true.

I enjoy your comments JS. What are your thoughts around the soaring UK inflation (18% predicted), Europe (energy shock) and the US and how this is going to influence the RBNZ's ability to manage domestic economics?

My gut is that when the RBNZ is ready to start reducing the OCR, it will not be able to due to the NZD's vulnerability. NZ will have its feet closer than it wants to the economic flames and we'll see a contraction for 3-4 quarters as a result. Pure speculation on my part but I'm interested in your views if you have a minute?

Thanks for the kind words. I think NZ's ability to manage its economy and especially monetary policy is definitely limited, as one would expect given its small size and heavy dependence on foreign capital and goods. I'm glad that the country retains its ability to set interest rates (15-20 years ago there seemed to be a lot more talk of NZ possibly adopting the Australian dollar, in which case rates would of course be set in Canberra). But RBNZ's ability to act independently of the FED is sharply limited, and I agree that we may see an indication of that in the next year if house prices and/or the general economy contracts more or faster than the government wants to see.

Thanks Joe - lots of spinning plates offshore.

Indeed.

The biggest uncertainty for me around inflation is how much war there will be over the next few years (war generally being inflationary). May as well read Tarot cards to predict that.

I think the median asking price of listings can be used to predict short term property trends. I have the Auckland median down 150k since peak. 65k has already come through in the latest REINZ report so expecting to see around 85k more in the next couple of property reports. Interestingly Auck asking prices stopped falling a couple of weeks ago hmmm temporary pause or has the market adjusted to the higher interest rates?

Many have switched to PBN that I am watching - would that change the data set?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.