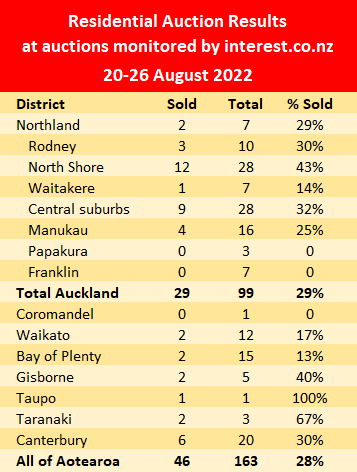

The number of properties offered at the auctions monitored by intererst.co.nz last week rose but the sales rate took a dip.

There were 163 properties from around the country offered at last week's auctions, up from 130 the previous week, with 46 selling under the hammer.

That gave an overall sales rate of 28%, down from 33% the previous week.

At the major auctions where the number of properties offered made it into double digits, the sales rates ranged from 13% in the Bay of Plenty to 43% on the North Shore.

We are now in the last week of winter which has brought with it some pleasant spring-like weather so we shouldn't have to wait long to see whether this produces the usual "spring bounce" in auction activity.

The table below shows the results of last week's auctions by district, while details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

88 Comments

It's alright. Bernard Hickey thinks that FOMO will be back soon.

Yep, all we need is a bit of that spring weather. She'll be right mate 🤣😂

Yes, Bernard Hickey thinks that FOMO will be back soon, but he thinks that, not because it should be true, but it will be made true by the MPs and managers of the RBNZ who have financial interests in perpetuating the PONZI and the power to distort the system in their own favour.

I doubt it can be made true by the MPs and managers of the RBNZ although they might want it to be. Just look at RBNZ and Orr, they might've thought they were doing well to bring a favor to the Ponzi by relentlessly dropping OCR and interest rate. But now they have to do the exactly opposite to cover their own asses. Yes, they might be able to continue to create FOMO to push housing price more unfordable, they will also just have to clean up a bigger mess later on down the road. Anyone who defies fundamental principles of economics will be left behind eventually.

We basically had a decade of very low inflation so the RBNZ held rates very low which is exactly how it was designed to work. Now that inflation has picked up, rates have gone up. Making out that RBNZ or government are corrupt seems like a bit of a conspiracy theory to me

*A decade of very low inflation when you don't take into account house prices

This is especially handy when using house prices to generate a 'wealth effect' to support the economy.

True, very low consumer inflation, not asset inflation. Maybe they need to start measuring assets too. But again i doubt you can call it corruption, the RBNZ have mainly just done what they were mandated to do (with exception to their covid response which may have been excessive in hindsight).

They had no mandate for the "wealth effect" experiment. It was not only a mistake, it was a corrupt mistake.

What frustrates me is people saying hindsight is 20/20. We were all there, why leave it to people on the fridge of society to worry about doomsday scenarios like heaven forbid interest rates going up while the reserve bank blissfully goes along with everyone else believing things will be ok. If its not corruption then it's irresponsibility at the very least.

We basically had a decade of very low inflation so the RBNZ held rates very low which is exactly how it was designed to work.

NZ has not had a "decade of low inflation". And why is that?

1. Inflation has been in asset prices, not the price level of goods and services.

2. Even among the price level of goods and services, the relative cost of these goods and services is 'hgh' compared to other countries. Cost structures in NZ are high because of weak economies of scale and low market scale.

True asset prices have gone up well ahead of inflation. But should the RBNZ try and control asset prices? A large number of the country barely own an asset, it’s irrelevant to them. And had the RBNZ kept interest rates high to control asset inflation we would have had consumer price deflation which would have caused all sorts of problems.

Are they assets?

A rental that's needs topping up 15K a year sounds more like a liability.Needs painting every ten years.

Its just one massive misallocation of capital that profited four large businesses, and made everyone that had a title to a property feel good for a while, provided lots of work for many...but left thousands living in motels and cars and without a dollar of savings to support themselves.

One big con job if you ask me.

Now for the hangover.

A rental that's needs topping up 15K a year sounds more like a liability.Needs painting every ten years.

Kaumatua Orr is on record as saying that housing is a 'consumption good.'

Be Quick.....

Looking forward to the monthly numbers, perhaps another 2-3% slide MoM.... these stats days are great as TTP cannot polish just how bad the MoM number is, month after month after month of drops.

Sure TTP and the spruikers can polish a lot but hard facts do not lie. This market is not even close to sellor capitulation, so many delusional price by negotiation sellors still hanging out for Nov or even Jan prices, which are now 15-20% above actual clearance rates.

As these sellors wake up to the change, significant further drops are going to be required before buyers enter on mass, if there is a mass of buyers, seems every other "Story" has been proven incorrect.

Well, I'm still waiting for that almighty property crash that a bunch here have promised - hasn't happened, and looking less and less likely that it will happen - with banks saying intertest rates are just right, inflation likely under control, OCR near its peak. Sure things are a bit slower out there and I almost bagged what I convinced myself was a *reasonable* price for a good section, but no fire sales as of yet.

I say *reasonable*, in terms of prices we have recently become accustomed to - but certainly not reasonable in relation to what it would have been 2 years ago.

Nice try.

befuddled alright!

You characterise an accelerating downturn in prices that eclipses those seen in both the US after or Ireland after the GFC as "hasn't happened" - wow. The change in market dynamics is in the process of affecting prices. I'd suggest waiting for the story to unfold more completely before calling it.

The spruikers will keep spruiking to the bitter end!!!!

Spruikers gonna spruik!

"Waiting for the story to unfold before calling it"

That is interest.co gold right there, comment of the month. Please take note of this everybody, even though no DGM will

I'm saying there hasn't yet been a crash, which is different from a downturn. I can't see how we can avoid a more severe downturn or even a crash and marvel everyday that it isn't way worse than what I'm encountering, watching and waiting. Just the waiting whilst watching is getting tedious - I keep telling myself to be patient and hold off, but how long does one do this for, when the direction isn't really clear?

10k a week, 40k a month, not enough for you?

From an investment side I don't really know what I'm talking about but roughly speaking a $700k property needs to be able to charge $1200/week to cover a 25yr P&I 6% mortgage + rates + insurance etc.

In the areas we are looking in you can maybe get $500/week rent for that property if you're lucky.

So the numbers for investment work when you can get the $700k property for $300k (like you could 5 years ago).

Edit: As pointed out below, I forgot to mention the above example is using equity / no cash down for the 40% required.

40% deposit required for a rental at the moment. If you had money to pay for this deposit you would be fine. If you used only equity not so.

So just ignore opportunity cost on the deposit?

It is the step that gets you on the ladder. In the end, if you are still renting in retirement then it won't be as easy

What if you retire and you've successfully invested in the stock market getting better returns than housing? It doesn't need to be all about housing.

I'm 42 without a house but can buy a house with cash if I choose too, done through saving (mostly in Australia) and investing in stocks. I have to ignore some social pressure but otherwise I'm quite happy renting especially when rental yields are below 3% in my town and interest rates being much higher than that.

What if you retire and you've successfully invested in the stock market getting better returns than housing?

Then you have bucked a statistical trend.

I intend to continue renting, in my 50s, built a business that pays me 6 figures a year and I dont have to show up anymore. Most people dont have the risk appetite, and are happy with the housing security blanket. Personally I just see it as bank slavery that stops you living and removes all choice.

Hi Sluggy,

I hear you sell Tupperware.

TTP

Kirby vacuums and Encyclopedia Britannica are my go to.

Popcorn is selling well at the moment, it has good growth and strong future returns.

Perhaps you have significant non property assets to draw upon in your later years, but I know a handful of people who took your route (successful business, no house) who are now in their late 60s. Their choices are becoming fairly limited.

Depends on how much of integral part of it the owner is, also massively affects value if its wrapped around you as the owner/relationship holder.

I was meaning more about their housing situation.

But if you can liquidate the business for a decent wicket, sweet.

If you listen to the doom merchants they will say that you had to buy 25 years or even 35 years ago when the boomers were still young and virile. Not 5 years ago. But I agree with you there were lots of good properties 5 years ago. Few here would agree with that

Assumptions: 700k house, $560k mortgage, assume $4000 rates, $1400 insurance, 33% tax bracket, maintenance excluded.

At 2.5% interest only with interest deductibility - needs a rental income of $284/week to break even

At 5% interest only with no interest deductibility - needs a rental income of $642/week to break even

At 5% 30 year P&I with no interest deductibility - needs a rental income of $798/week to break even

To be covered by $500/week rent in the last scenario, the price would need to be $400k.

Exactly. The math has not stacked up for quite some time. All about speculation based capital gains and tax rinsing. This is highlighted by the boom of new shoe box housing that still allows tax rinse.

In Lebanon, retiring teachers are being paid out a pension of about $120 USD, after decades of contributions.

You can always sleep in the house.

Not been to Lebanon Pa1nter are you from this country, you seem to know a lot about teachers pension in Lebanon don’t tell me you are retired teacher. How much is a house in Lebanon say in Beirut.

Banks are being really cautious with renewing interest-only mortgages now.

So what happens if we factor in a sudden jump to interest and principal? Add another $1.2-2.5k a month to costs? The sums are looking pretty scary

Capital gains have augmented yield for the last 5 years... so with no CG going back real fast..... its already a long way there but vendors not admitting it....

The retreat of tide of cheap speculative debt continues.

The further it does the more the beached debt whales will smell. It is true that the spring and summer see increased activity, but if we get another .05 increase on Oct 5th and Nov 23rd then the expected spring bailout could be similar to a deflated pavlova.

That spring like weather sure is going to make those beached debt whales rot faster

Winter over spring approaching is just being hopeful and positive.

Will soon know, if this time is different or are Sc$@d

We may see Spring bring increased activity from sellers unmatched by hesitant buyers with more stock accelerating the current down turn. This of course is an unmentionable if writing articles for the property sector.

Judged on the enthusiasm of people to participate in this blog, the housing market has a very bright future......

But you already knew that.

TTP

Just speaking to my neighbours, young couple with a two year old daughter.

Moving to Melbourne in a few weeks, they have bought a 4 bedroom house on a full section for $650K.

Yes, it's far out from central Melbourne, but not dissimilar to Pukekohe relative to central Auckland - and in Pukekohe the same new house would be well north of $1 million.

Good luck to them.

Most young kiwis should be seriously doing the same thing.

Pukekohe is paradise, it would be hard to beat...

Hi Mousehouse,

There are too many snakes on the outskirts of Melbourne. And further north there are crocodiles. Worse still, used car dealers and hifi salesmen lurk everywhere......

Think of your wife and children and stick to Pukekohe.

TTP

yawn. Cliches, and yet more cliches.

Move to enjoy hundreds of hours of commuting a year?

Terrible advice. Get yourself in a position to remove commuting from your life, enjoy your family.

Massive assumptions there. And wrong assumptions. Get with the programme, it's 2022 not 2002!

He will work near where they will live, and she is able to work part time from home.

Ok well then things will go better for them than everyone else I've known to buy in the Melbourne wops.

Success!

Well any one can make generalisations about anywhere, right?

I've made plenty of generalisations about places - like Hamilton - and many of them are probably unfair. You live there right?

Good on young people getting out of this god-foresaken rip off of a country and creating a better life for themselves.

Don't live anywhere near Hamilton.

All for people spreading their wings and exploring other opportunities. I wouldnt call swapping suburbia on the fringes much of a change though. Either live right in a city, or get the hell away from them.

“Ok well then things will go better for them ..”

Assuming them won’t have to move back for their parents one day.

Oh gawd

You can assume anything, for any situation.

Wellington, Queenstown, Tauranga etc might have a massive earthquake for all we know. But until then, pretty good places to live?!

46 sold via auction in one week for whole of New Zealand. Rates are going up inflation is still here NZD tanking will put more pressure on inflation. House prices were 10 times average wage earners income so overvalued compared to income, now house prices are falling around 2.2 per month this will accelerate over next few months how is spring going to turn this around? As the world downturn continues this will hit New Zealand hard and housing is one of our main contributor’s to GDP which will be crushed taking house price’s down could easily see price’s back to 2015 level

Agree, can see 2015 level being reached as well.

Wake me up 30% off peak Nov 21 prices........ summer should be here by then...

"10 times average wage earners income so overvalued compared to income"

I wonder what is the answer?? Wait I know!! Find a partner and buy together

In Auckland it was 10 x average wage couples income. HW2 you can’t be that daft.

Oh I am daft alright which is probably why I LOLed your comment... so how daft are you

Blood has already been squeezed from that stone.

I am not sure that Investment makes a lot of sense at these yields. Hard to see many "smart" investors coming in if you remove capital gains from the table... do we need yields back to 5-7% to cover long term maintenance.....

I have been provided with sale data for a trendy Auckland suburb that has several four bedroom homes selling for $100K below market-listed price, after being on the market for months. So there is the price on the sign and the price on the line. They are very different things.

Roaring silence from Ashley's Altar Boys

AAB

If you have a negative disposition and a weak heart please close your eyes and do not read on.

Every city in nz (of the 7 I follow) has less homes for sale than one month ago. What happened to the flood of FONGO sellers and the disappearing FOOP buyers?

We could be in for a robust, or dare I say resilient spring

one side of the equation - supply.

How about the other side?

One side ... I would say both sides as stock on hand is summation of market activity. Isn't it funny how when levels were increasing, you and every other DG were all over and singing it from the rooftops

Stock would have to fall quite a bit further to get supply and demand close to equilibrium.

however it is true that lower stock levels may reduce the extent of house price falls over the next couple of months.

I find it difficult to see your point.

It is pretty clear:

- on one side people don't want to spend too much (or more precisely they can't afford even the most humble of the houses in the current market)

- on the other side sellers try to don't make a loss (selling for less than they bought)

for a seller is a choice, for a buyer is not

even an idiot can see how it will end

Btw... again, you call DGM (how boring) people that predict/want/prefer lower house prices.

May I know why?

Would you not prefer to live in a productive country where the vast majority of people is not hostage, not busy is paying for shelter for more than half of their time?

Is that gloomy for you?

’DGM’ is just a lazy, disingenuous and unintelligent put-down that spruikers use because they know how weak their arguments and positions are now looking.

It’s desperate and unfortunate.

Homes for sale goes up by 80% over last year, then come down by 1% and you think thats a robust of resilient spring lol are you for real HW2.

He's one of the few spruikers left on this forum.

Him, TTP, who else?

Have made more of the folding stuff ie cash, than most others so I would say very real and thanks for asking

And some of us have also done very well thanks very much, but not from property speculation.

Sounds like you have a lot of skin in the game, must be one of them who missed all the signs of this downturn. Still HW2 giving back some of that cash will not bother you, hopefully you have listened to most of people on here and are not over leveraged as this will make the folding stuff disappear very quickly, maybe talk to yourself and let TTP know as he is also very misguided.

With that patronising comment you are sounding like IO. It might surprise you that I am capable of making decisions for myself without the help of well meaning people like yourself. Thankfully I do not chop and change. And with that I have to go and ride the ride-on

Is that a ride-on mower? Surely with all the folding stuff you have a car would be better or are you doing a gardening cash job.

Yes ride on mower just like the guy on the lotto ad. Maybe I could get a sheep and feed it so that oneday it will feed me. With the hide I would make ugg boots and also use the wool to knit a cardy. I would be both saving the planet not burning fossil fuel and saving money in this cost of living crisis. I'm not sure how my landlord would feel, but lucky I don't have a lord of the land. Btw satire button is on but you know that :)

If the writer of Hutt Valley Property report is correct, many sellers have taken their houses off the market (after months of being unable to sell them). I only follow Wellington, but the number of houses being sold here seems to be quite low.

Not many reasons to sell atm -> if you are moving location (same value) or buying bigger there arent many decent houses available to buy, if you are downsizing there is a lot less equity to release than before so its prob better to wait a few years. Not many first time buyers in the market at the moment.

We were thinking to move location... but its real hard to sell and nothing we like on the market, and nothing coming on. its dead.

For now if people can stay put, or rent their house out is the obvious choices. When we get forced sales the market will start to tick again

Property has been a winner for so long that there are a million landlords who'll sit by and watch $200k in equity evaporate each year rather than sell for $50k less than they paid. Most of them can afford to, as well, stupid as it is. Much like those who'd rather have a place empty for six months of the year than drop the rent by a fraction to attract a tenant... plenty of them out there.

Are there actually plenty of Landlords out there that would keep a rental empty? Or are they Dunning Krugers spinning a tale about how they're such astute investors that they don't "need" tenants, they just pay the rates and insurances out of their own pocket?

I think you are right HW2. I keep a close eye on 5 central Auckland suburbs (west side), and total listings are down to 174. Three months ago they were at 230.

This Ponzi will be very difficult to revive.... I suspect a bit to go yet to be a housing market again. We my have a compass at an open home soon rather than a tape measure.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.