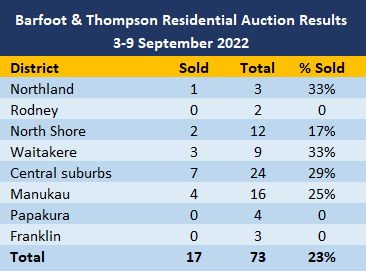

It was a hard grind again at Barfoot & Thompson's latest auctions with just under one-in-four of the properties offered selling under the hammer.

Auckland's biggest real estate agency offered 73 properties at their latest auctions over the week from 3 to 9 September, up from 69 the previous week.

But the number that sold under the hammer remained at 17 for the second week in a row.

That pushed the overall sales rate down slightly to 23% from 25% the previous week.

Barfoot's auction numbers remain particularly weak in Auckland's southern districts of Papakura and Franklin, although the number of properties offered at auction remained low in all Auckland districts.

Under the hammer sales remained in single digits across all Auckland districts at the latest auctions - see the table below for the district-by-district results.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz and the prices achieved on those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

110 Comments

Selling houses is becoming a grind. I’d be looking into making the transition into selling EV’s if I was a RE agent… or snake oil perhaps

No money in selling EVs. Tesla does it direct.

If only someone else other than Tesla made EVs.

They may find it hard to compete when paying a salesman commission. It seems like quite an old fashioned thing to do.

The system the car manufactures mostly use is pretty much direct. The dealers are kept very much under the thumb.

Why buy today when it will be cheaper tommorow?

Aĺl the REAs hate it when I say this......apparently I'm captured by the media talk of a negative market.

I point out the obvious that people's borrowing capacity is cut in half.....so what must prices do??

High cost of money, so prices must fall dramatically ...... then they sigh and know I can't be spruiked, like they did to every poor sop buyer of the last 10 years......

We are in a new paradigm now where a good yield is needed, capital gains are done or will be minimal going forward.

Can someone please inform the foreverbulls, pied piper likes of TA and AC?

Well put. It's a "the math, leave it out geeza" moment.

You go around open homes telling real estate agents their prices are too high?

They don't like it, then don't bloody list homes as "price by negotiation" then. Then they'd avoid these uncomfortable confrontations at open homes. Seriously if they only want buyers to offer more than $600,000 then list that on the website. Otherwise they waste the buyers time by dragging them along to open homes in the promise of negotiating a reasonable price then hit them with "you're asking way too little and we're not budging".

Not recently JJ...... just in the course of regular discussions with REA friends, who are living on rations currently, as turnover has plummeted.

They say vendors still want big money, yet the FHBs and smart buyers lending is now savagely clipped, as the banksters test rates are near 8%.

With many banks hiking their mortgage rates in the last week - it will be increasingly tough times for any seller/agent as rates are only going up, up, up from here and no relief until possibly 2024. Hard hats all!

There is a resurgence in fhb occurring now in the market as on a capital basis this is a buying opportunity. Many have had good pay rises and affordability is returning.

🤣

AC is on zb right now. Listen up FA

... damn , I missed that , accidentally turned the radio to the Rock 93.7 instead ... darn ...

But , lemme guess what the venerable AC said : this is just a pause , a mild correction in a decades long boooooom market in house prices , we expect demand will return next year , and prices will resume their upward trajectory ,the beginning of another doubling in the next 10 years ...

... am I right ? ... I'm right , aren't I ... AC said that , again ... & again ... its coded into his DNA , he can't help it ...

Good morning Mr Hero, yes he may have but you will have to listen to the broadcast to get the good oil. Search Zb week on demand, it will be the best hour you spend today... either laughing yourself silly or listening to every word, depending on your perspective. Hey up

... thank you ... yes , spend an hour listening to Saint Ashley from the Church of the Holy House Price Rises ... or .... or , spend another hour with the Rock's top 2000 countdown ...

Hmmmmm ? .... tough decision ....

We put an offer on a property this week in Central Auckland, 25% below CV. They haven’t said no yet…

Oooo do update us when decisions are made.

We put an offer on a property this week in Central Auckland, 25% below CV. They haven’t said no yet…

Don't be too cocky. You might find '25% below CV' is too high further down the line.

100% agree with you here J.C. We have been looking a while, like the area and keen to put it behind us.

I'm definitely not a property investor or anti property. But I would like affordable housing for people on average incomes. But if your happy and have money then that's all that matters. People have different circumstances. We will buy in 2 years to 3 years time regardless of market as well, but its that time frame, as we are starting a business and it will be that timeframe to start making money that we require to buy house we want, so have to wait. We could be lucky though if prices keep going the way they are, or they may go up, who knows time will tell.

I have been enjoying going to open homes and on the way out asking the RE agent if they want to buy my Toyota yaris with a sympathetic tone.. I just love the look on their face..

The LOL look at you owning a Toyota Yaris?

The reality of them getting one sooner than later..

Pretty sure you own one by now

Heh, they're thinking "why's someone with a Yaris coming to open homes in Herne Bay?".

That would be pretty stupid of them. Some people just don't care much about cars and/or prefer to spend their money on something else.

Last three vehicles we bought new. Between $30K and $50K. Then the other day I was getting around in a Nissan Cube (value about $5K). Nice. Cute, Useful, Fun.

A Cube would certainly be the second car, herself would have the first car. But I'm seriously thinking a Cube would suit me fine.

... the good thing about a Cube is that if you crash one , they still look like a cube .... pug ugly little brutes before & after the prang ...

You would love the Toyota Sienta and the Nissan Expert... we happen to have owned both of these fugly models. Thank goodness not any longer.

... got a green Toyota vitz , it looks like the back has fallen off it , I call it " the Gherkin " ...

Solid little 1275 cc engine , but ... very fuel efficient ...

Like the one that cut me off going for the one remaining carpark. If I knew it could be you I would have put my foot down in my toyota aqua with racing stripes

I guess you know the saying about assumptions?

True, there could be swathes of millionaire, Yaris owner yucksters with nothing better to do than drive round trying to mike drop on agents.

Being a millionaire doesn't mean anything anymore. Anyone who's mortgage free in NZ and owns an average house is, surely many of them have modest rides.

The mic drop thing is an exception though.

Oh yeah, cars for me are utilitarian. I'll take an aging Jap Econobox any day of the week. Total purchase price is less than an average service bill on an Audi.

Agree. Cars just depreciate. Once you look at the math it is so much better to spend $10k on a s/h japbox and low mpg/servicing costs.

Means lots more play and less work than the 'badged up' motor folk. 🙂

Are you taking about yourself

The RS? Heck yeah.

You and NZGecko lead an odd existence…

My existence JJ, is based on the reality of the plummeting everything asset market (sold much of my shareholdings last year and have not over-collected on housing) and the current ongoing downwards trajectory.

What Lala land are you in or hopium for?

:)

Life would be too boring with oldies like you

So when RE agents pulled sh!t over everyone's eyes during the boom, did you tell them they lived an odd existence or are you one of those crooked RE Agents

... the Gummster clan no longer needs a house of our own .. we spend so much time in open homes that we've effectively become permanent nomadic open homers ...

Might've solved the housing crisis ...

Hahaha.. that's a novel idea.. considering the number of homes that are empty during the sale process, would definitely solve the housing shortage

The market is only just approaching the point where the pandemic party has being unwound. We haven’t actually encountered what I would consider a real drop yet.

Exactly, this is Ponzi collapse is just getting started.

We are still only in the first phase, unemployment rising is the next phase and then finally loan defaults and banking crisis, I estimated 50% falls in non-prime and 30% in prime residential. I'm begining to think that's too conservative now. I'm hearing it's very bleak out there, It will cost Labour the next election and Orr will depart,

Nothing to worry about. A housing bubble is a "first class" problem to have, at least according to Kaumatua Orr.

I wish we weren't all still in the dark about what really went down with the departure of the General Manager of Financial Stability last year.

Things have been a lot less stable without him...

What a DGM!

I don’t think it will be anywhere near that bad.

Unemployment will rise to around 5-5.5% by middle of 2023. You would need unemployment of more than 7-8% to really start putting significant downward pressure on house prices.

The RBNZ will start cutting the OCR by mid 2023 in response to rising unemployment and lowering inflation.

I am sticking with overall falls of 20-25%, peak to trough, with an outside chance of 30% falls.

Agree. I think the comparisons people draw on here to the Irish crash are a bit far fetched. Ireland has an economy that has manufacturing and other productive investment options. People there chose not to invest in property as there was an over supply. Kiwis are blinkered when it comes to property and get frothy at the mouth when considering another property purchase.. it’s all we know and it’s all we have. One trick economy that will likely be saved… eventually

In other words, NZ property market is a highly emotional market.

It is the emotional, irrational, markets that crash the hardest. Blind greed turns to blind panic.

".........I am sticking with overall falls of 20-25%, peak to trough, with an outside chance of 30% falls........"

We might have got down to there already House Mouse.

We know lots of people are deciding not to sell at these prices, yet, but there will be the inevitable few who have to and that 'few' will grow over time,

Can you tell me the next draw Lotto numbers, HM (short for His Majesty)

Hard to come by anything firm, but as a narrow range I reckon the numbers will be 1 or higher or 40 and lower.

More accurate than HM economic pronouncements painter ;)

Agree with you TK.Our house going by QV estimate has dropped from peak 1250000 to 830000 this week.Thats over 30%.

It’s Like Groundhog Day housing market falls and has bad news then a number of people on here pretend all it’s good just a mere flesh wound. Time for people to understand this housing market is in free fall.

Yes we are currently falling at well more than twice the rate of the first year or the very correlatable Irish 70% property crash, from 2007.....

We are leaving the Paddy Doolins in the dust!

All really comes down to whether you're of the belief this is the crash to end all crashes, or a sustained period of malaise.

The former is a big call, the latter isn't something people should be getting too paranoid about, if theyve been even partially financially sensible.

70% correction is on the cards. Not much holding up house price’s,rates climbing, inflation high even EU is starting rate hike season.

70% must be the new 7%

I'm not sure you can comprehend what 70% would look like. No need for dinnerware anyway.

Your predictions increase by the week. 70% drop takes us back to mid 2000s pricing, AKL average house will be 450k. Will you be buying when it drops to that?

Sounds about right. A DTI of 3 or 4x household earnings would be great for the average Joe/Josephine.

It wont be so devastating to the existing market, if it happened over 7 years. Just ask your local Paddy Dooligan.

Big Ben 60% to 70% from top end of last year but 450k is about all average wage couples can afford so thats around where the floor would be found. It’s only money on paper until you sell. I am happy to see house price’s fall most people are. I have been through this before in UK around 10 years from top to bottom and back to same level so you looking at 2032 back to level we were in beginning of 2022. This housing market is so overvalued compared to incomes recovery could take a lot longer. If rates do go really high people will just have no way of paying million plus mortgage in UK had a lot of friends who just drop keys off to bank and moved out, I was fortunate as I worked for large bank and my mortgage was fixed on employee low rate.

I worked for large bank

You must've made them billions when you called the last downturn down to the nearest %.

Pr1nter You sound upset are you over leveraged don’t worry just 10 years for turn around hope you have fixed for a long time or 7% rates will be your destiny at best. I have seen a number of people on here trying to warn you but it’s not part of your programming to listen or take advice from people more knowledgeable.

I'm pretty good thanks, I just find your claims somewhat ambitious. But you worked for a bank so much be pretty onto it with these sorts of things.

Pa1ner it’s not rocket science rates up and climbing, inflation high, average house in Auckland 10 x average wage couples income, believe me you will look back and say how did I screw up so badly.

I must confess to not being the world's best financial soothsayer, so I find the game of predicting percentage rises and falls to be somewhat of a crapshoot. On the flipside repeatedly stating DTI and price to income levels MUST mean a 70% fall extends beyond the realms of rocket science and into something in another dimension entirely.

Capital gains and residential real estate isn't really a market I'm tied up in, but it will be interesting to see how on the money you are.

Pr1ner Just a matter of time most central bank are raising rates, inflation is highest for 40 years around the world, energy crisis happening in Europe, food shortages in many countries, wars continue, one third of Pakistan is flooded, wheels coming of in China housing crash bank runs lockdowns. I could go on but I am interested to understand why you think New Zealand housing market is immune to all this bad news and will just turn around and grow again.

I'm questioning your repeated assertions of 70% drops. That's not the same as claiming the NZ economy and housing market isn't immune to negative global and domestic events.

Maybe he gets it wrong and its 40% - 55% - 60% drop and a long long plateau, depending on drop. Not sure its that big a deal he said 70%. But if BBQ conversations anything to go by sentiments have certainly changed, from 6 months ago.

Without a doubt this is definitely a bit of a malaise period, I'm not sure anyone is denying that. It should've been 2 years ago when the global economy was shut down. Instead we got a phony war propped up by low rates and what I can only describe as psychological hysteria by a population a little too relieved that the pandemic wasn't a zombie apocalypse.

But 70% for 10 years is calling for a world I don't think most kiwis, home ownership or not, would enjoy. By year two, governments will be pulling whatever levers they can to juice things up again.

It's a prediction that'd require a few more bad events, and for governments to just throw their hands up and say "ok that's it, we're just not going to do anything about this anymore". Pretty ambitious, and makes anything else DTF says a little suspect.

65% happened in Ireland from 07-12. We're not Ireland, but because it happened there shows that it's not impossible. Arguably we're probably more likely to have a 65% fall from our peak than Ireland on the pure basis that our houses so much more overvalued than they were.

- During the property bubble, a disproportionate number of people were employed in the construction industry.

- The banks: were accused of too loose lending practices

- Inadequacies of the financial regulatory structure "It is clear that the actions we took were insufficient and were not taken early enough,"

Many things are possible, and we can look for historical parables. Fall of Rome, Japanese bubble economy, that sort of thing.

Usually it's better to determine what's likely instead of what's just possible. The actual bus that hits you isn't one that's predicted, and most predictions never come to pass.

Half the people on here seem to think they're Michael Burry 2.0.

2032 in nominal terms maybe. But real terms? Maybe there will be another bubble in 50 years…?

Canada just raised 75 basis points.

Because that’s the problem - we’ve become accustomed to houses being 10x incomes as being financially sensible when in reality it is financial insanity.

"if theyve been even partially financially sensible."

half the country doesn't have a grand on them this weekend

I'm not sure that's the demographic DTRH thinks they're schooling.

Mary Holm: Ripped off, renting and 65-plus — don't give up

https://www.nzherald.co.nz/business/mary-holm-ripped-off-renting-and-65…

Premium content

Older couple lost their home after 2008. They are still resolved to buy another home within the next ten years.

Not many people have the backbone of these boomers to get up and bounce back. Def not the younger gents

These boomers probably fell for scams the younger generations would have easily spotted and avoided.

Gen-Z are the best generation I have seen in a while.

Smarter, better educated, usually not polluted by religions, a bit confused in terms of identity. They look like a better younger version of Gen-X, but less f@#$ed.

They know that boomers have one good thing.. they are going away soon.

Thats fine that's good being confident to have life worked out already at a young age. There is a lot of time and water to go under the bridge for a 25 yo until reaching 65. Some teenagers think know everything don't they

I just don't think that generational identities define individuals. It is about as absurd as saying, look at the old person, they must be wise.

It isn't absurd. Surely partial, anyways.

Many Boomers think in the same way about their rights.

Many X think they have been foundamentally sold and exploited, with not much hope for the future.

Most millenials try to get what what boomers had, while being laughed at.

Almost all Gen-Z I have known don't even want to try to compete. They know that the game is rigged.

I hope all of us are wrong.

There may be a lot of boomers who would have loved to have what many of the younger generations have been blessed with. As they say, the grass is greener on the other side of the fence. Why indeed would you have said that gen zeders are the best etc. But who can choose their parents or their circumstances. Maybe just be grateful we do not have the trials and awful things which many are facing in other countries right now. Nz is a great little country

wow... first time I could have a constructive exchange with you.

thanks :D

I have nothing against you. But I prefer people without extreme predictions

My pick is that the housing market will continue it's 'correction' through the summer months & possibly into next winter. We may see a small levelling off over summer (seasonal) but the harsh reality of our recent fiscal & monetary stupidity is still to play out. There are so many moving parts that it's hard to pick anything but Te Kooti's version is pretty close to my worst case scenario. I remain hopeful, as I am mostly always hopeful, as we live in an age of abundance, never before seen on such a scale as this, however, PDK's constant reminders of having increasing prosperity on a finite planet are starting to be noted, especially in Europe right now. The fact that their leadership has been woeful for the past 40-50 years is a significant factor, but not one they will admit to. Their relational management of their Eastern European neighbours has been poor to arrogant, which has seen it blow up in their faces, which I will use here as a warning to all western socialist leaderships. That whilst your theories on life are wonderful things, your realities are a long way away (from them) & that if you cannot achieve any upside in our overall living standards, whilst continuing to create more & more costs across the board for the average person, then would you please step aside & let somebody else (with half a brain) have a go. Thank you.

Lower prices will start to bring some demand back to the market, and it will find a new equilibrium.

I think TA is picking that to happen too soon, but he’s correct conceptually.

A lot of people here don’t seem to get the concept of demand shifting upwards once prices are 15-20% lower.

That will minimise the falls.

Say a $1M house becomes $800k, is that still affordable to most people @ 7% interest rates? I remember years ago when the average price went past $500k and we all shat the bed then. Its not like wages have moved that far since then either.

Why 7% interest? Fixed rates are at 5% and economists don’t see them going much if any higher.

An economist would as soon s/it on you as tell you the truth. Don't listen to economists. Look at real world data.

- Look at inflation rates in Europe.

- Look at Canada just doing a single hit 75 basis point rate rise, and promising more to come.

- Look at the inflationary energy crunch in Europe that is radiating out through the world.

- Look at the China lockdowns. The world's biggest factory is running on 3 cylinders, which is highly inflationary.

- Look at the speed that the FED is now raising rates, and their agressive tightening.

- Look at our crappy dollar vs the US. It is down ~15% just this year. Imported inflation.

- Etc, etc.

Well, you know my thoughts on economists :)

However current and former bank economists must know a thing or two about this, and most of them seem to think fixed rates won't go much higher than 5%, even if the OCR goes to 4%.

Mate, if you can look at that laundry list of massive, global, disruptive inflationary pressures and STILL believe the economists, then there is nothing more to say.

Same economists, who were saying that inflation is transitory and that low OKR is the new normale?

The Big Dog here is the US FED imho. NZ is but a leaf on the US ruled tide.

Finally Powel has grown a pair, realised his 2021 story of "transitory inflation" has screwed the pooch, and now he has to over react big and for longer.

FED funds to the moon 5-7% and as is the rule, NZ by bigger.

Our RBNZ does not want to scare the horses with such talk and will react and change the story over time, when they need to (when the US FED moves).

And the media dosen't want to scare the horses. And the economists don't want to scare the horses. And the talking heads like Tony Alexander don't want to scare the horses.

Which is why none of them are saying the truth out loud. The truth is that now is the time to batten down the hatches in case REAL inflation becomes entrenched.

2020 was the time to start battening down the hatches, because the inflation was on the cards all the way back then, irrespective of what central banks were up to.

Instead everyone wanted life to keep being normal, and that translated to things being healthier than they had a right to be.

Demand will shift upwards once prices start rising.

It depends. Lower prices could bring some demand back to the market, but will it be the same as before? I.e. 2014 to 2017 investors outnumbered FHB 2.5x. Prices falling 20% might enable more FHB to qualify to purchase, but how many investors are going to pick 20% as the bottom and start piling in again?

Total Lending per month

- FHB Average $656m

- Investor Average $1.6b

Total Number Borrowers per month

- FHB Average 1800

- Investor Average 4700

Exactly. I am not saying demand will be as before. But all things being equal, assuming fixed interest rates don’t go too much higher, prices dropping back by 20% should start to see demand increase, potentially quite significantly. That will then limit how much further prices fall.

TA sees it happening late this year / early next. I don’t see that happening in a meaningful way until

late winter / spring 2023.

TA sees prices falling another circa 5%, I see another circa 10%.

B & T must be a very generous and forgiving employer , 'cos if I only achieved 23 % success in my job I'd be booted out quick smart ...

Tenant claims his termination was served as revenge by landlord after learning of his Covid views

https://www.nzherald.co.nz/nz/tenant-claims-his-termination-was-served-…

The landlord/tenant realm! ... no wonder they produce tv shows about it

I expect discretionary retail spend to fall based on the following but it's been quite strong. But data usually lags the reality.

Australian home values are now shrinking at an annualised rate that exceeds 15% based on the three months of CoreLogic compositionally-adjusted index data to 10 September. In Australia's largest city, Sydney, the annual pace of house price depreciation has stabilised at a hefty 22% since late August. Property values in the nation's second largest metropolis, Melbourne, are falling at 14-15% annualised clip.

https://www.livewiremarkets.com/wires/aussie-house-prices-now-falling-a…

Lies and statistics eh.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.