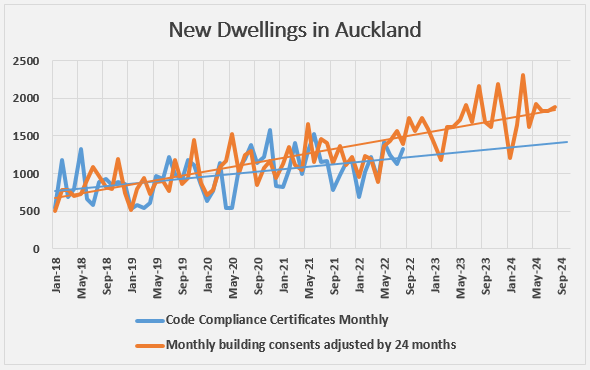

There is a widening gap developing between the number of new homes being consented in Auckland and the number actually being built.

It generally takes about two years from the time a building consent is issued for a residential project in Auckland until it is completed and a Code Compliance Certificate (CCC) is issued.

So the new homes being completed in August this year probably had their building consents issued some time around August 2020.

The graph below takes this timing difference into account by matching the number of CCCs issued for new dwellings in Auckland each month (the wavy blue line) with the number of building consents issued two years previously (the wavy orange line).

The lighter straight lines show the trends for both sets of figures by smoothing out most of the monthly volatility, making it easier to see long term differences.

This clearly shows a widening gap developing between the number of new homes being consented and the number receiving their CCCs two years later.

However, it does not necessarily mean there will be a downturn in residential construction in Auckland.

It's important to note that the gap first became apparent in early 2020, just as Covid pandemic restrictions were introduced.

These included periodic restrictions on construction activity and disruptions to the supply of labour and materials, which combined to stretch out the amount of time it took to complete a project.

That is showing up in Auckland Council figures which show the percentage of new dwellings receiving their CCC within two years of receiving their Building Consent dropped from 86% in August 2021 to 75% in August 2022.

As a result, the number of new homes being completed in Auckland has declined by about 10% since it peaked (on an annual basis) in the middle of last year.

That should not be a surprise, because if the industry is operating at capacity and projects start taking longer to complete, there's inevitably going to be a reduction in the number of projects completed in a given timeframe.

But there has been no such slowdown in the number of new homes being consented in Auckland, which continues to run at or near record levels.

Hence the widening gap between what is being consented and what is being built.

As the graph below suggests, if current building trends persist, the gap could get even bigger over the next couple of years.

However, there are a few things that could affect those trends.

Lockdowns are now behind us (fingers crossed) and there are also signs that supply line pressures are beginning to ease.

That should improve efficiency in the building industry and help to lift the number of homes being completed.

But there are headwinds blowing from the opposite direction, including the cost and availability of credit to both developers and their end customers, rising costs putting pressure on margins and the general softness of the overall housing market.

There are also uncertainties around where immigration numbers will end up, which could affect both the supply of labour for the construction industry and the level of demand for housing.

While the graph below forecasts an increasing gap between what is being consented in Auckland and what actually gets built, it doesn't predict a decline in new build numbers.

It merely suggests that growth in the number of new homes being completed will be slower than the recent growth in new building consents.

However, the graph should still sound a warning bell for builders, because pressures such as higher costs and the worsening housing market could start to outweigh the benefits of an easing in supply constraints.

If that happens developers could start putting plans for new projects on hold, which would inevitably lead to a decline in construction activity rather than just a levelling off.

But given the difficulties the building industry has faced and is continuing to face, the figures suggest it has survived in surprisingly good shape so far.

The comment stream on this article is now closed.

126 Comments

Was always going to happen. Still too bullish, Greg.

Possibly not as suddenly as what's happened. Speaking to various trades I know, new sales for new houses are basically non existent.

So things are already poked, but we'll keep going.

Of course they are poked. It’s not rocket science:

- High inflation in construction costs

- Crashing house prices

- Rising cost of finance for developers and buyers

It’s the perfect storm. And probably the most perfect storm ever - when did we ever before have high inflation and a crashing housing market (in nominal terms)? Answer - never!

It will start getting interesting around May ‘23 when the huge number of current construction projects underway are finished.

Got to remember the rules are in favour of new construction which will help - lower deposit required, interest deductability for investors etc.

I'm sure the new builds that are completed will look more desirable as opposed to buying off plan with an unspecified build time frame.

Those rules will have marginal effect given the much bigger forces I outline.

It'll be a mixed bag. The last 5+ years have actually been a terrible environment to do development, those with decent pockets usually pick dead markets to start enacting plans.

A terrible environment? Yes, and no.

Terrible I guess in terms of the Covid situation, and resourcing frustrations. But pretty good in terms of booming house prices and high demand from 2019 to 2021.

Serious developers want cost certainty and resource availability. You obviously want a healthy market, but booms are a terrible market to get things done in.

Yep agree, but a large proportion of developers have not been ‘serious developers’.

I'm watching with interest the the semi bulldozed once perfectly good homes in our suburb that are been cleared for multi-units.

What will these guys do...carry on and pray or just pull the pin?

Must be incredibly stressful.

Indeed. Where the only one being built is for the original owners.

What I've heard from someone in the industry is that there's quite a few small time developers in South Auckland about to go broke (many of them new to NZ, who thought they'd lucked on to an amazing get rich quick scheme).

Yes, it was a constant growth, attention to numbers detail was low - done on the back of an A4 sheet of paper at 2k/m2 + an allowance per house.....auction rooms were just crazy. I watched it all in person.

Was crazier in the 2011s when some young chineese kid would buy a couple at auction in a row.

Yep, and you can see that borne out in sales of properties in the likes of Manurewa, that would have previously sold like hot potatoes well above CV, now going for well below CV.

Sparrow - well it actually was an incredible get rich scheme for many years. Looks like that has now ended. What are the chances a (new) government will try and revitalise it? What are the chances it could succeed in doing so?

It's the high cost of buying new that is putting buyers off. Especially in a declining market. Why pay top dollar on an asset worth less that the price?

Residential, yeah. Commercial, industrial and government are all looking ok, but of course then residential trades will want any work they can get and dilute those areas somewhat.

Agree. But numbers employed in residential is very high.

How long can commercial look okay for? The wfh trend is not going anywhere.

Don't know, for example I'm seeing alot more people travelling into Auckland CBD now... Traffic in general has picked up big time.

Traffic is still way-off what it was pre-lockdown but the commute times are getting bigger for sure. Rush hour volumes also seem to be passing through the motorway network for longer as well, but people can generally only shift their working hours so far. Once you hit that constraint it just all grinds to a halt.

My record pre-pandemic was 90 minutes getting home from Greenlane to Westgate. I wonder how long it will take us to get back there.

My take is that before covid you would leve work at 5pm , now people do 1-2 days in office often different days to there team then leave earlier 330-400pm to try and beat traffic, the rush hour thursday morning and evening is much longer things bad by 4pm...

That's my experience too. I'm in early, out about 4pm. Traffic is now bad as it used to be when I left at 5pm. Can't really move my day around a whole bunch more than I already have. End result: peak congestion, for longer, both earlier and later than it used to be.

Still quicker than taking PT or cycling, and not really practical anyway given daycare commitments. And total ideological opposition to actual proper rapid transit in our area thanks to MPs from places like East Auckland (busway) North Shore (busway) and Wellington (gold plated salaries and job security). But guess where thousands of new houses are going in the next five years?

Commercial sits in a different realm, as it's future focused.

But yeah commercial office space is pretty borked. But factories, warehousing, etc, pretty strong.

Yep, hope those who are after an investment don't plant their hard earned money into those construction companies offering 10% return, they will be very very high risk investments, but I see quite a few coming to the market now.

I wouldn't say it's the perfect storm, more a very unusual storm. So many negative factors, however we still have high employment, and historically reasonable interest rates (we started out paying above 10%). A lot of profit has been made over the last 2 years, and there's a lot work work that's getting put off until prices are more reasonable (ie: once the gouging stops) and the immigration taps are being turned back on and our low dollar means we're attractive to o'seas (USD) investors. Yep, a number of developers are and will be struggling - as always happens in a booming market and now that they have the down-cycle to contend with too, so we're going to see some hurt - but many I know are still working hard out to keep up with demand. I'm picking a k-shaped downturn, where the have-nots will end up with even less, and the haves end up doing even better, being is great positions to pick up bargains.

Yep I think you are right, i am in late 40s have a few friends mortgage free, good jobs, a few investments, and are just waiting on sidelines. So predict they be able jump back into market before some FHB 's, when time is right, guess its just picking when but don't think it will be for a year or so yet.

The problem is knowing when, and that's proving to be very frustrating. There are a few bargains about now, but they sure are hard to find and don't last long, especially when there's still a bunch out there, that seem quite happy bidding against themselves in an auction (face-palm) or snapping it up instead of being patient and getting it for a much more realistic price. I can't see there being bargains everywhere, in the near future, so would be quite happy to buy now if I perceived it to be a reasonable deal.

Bargains now, not sure about that. Most expensive time in history to buy, at last FOMO is gone. Can't see a bargain for a few years, I see a few years of tanking, people panicking, and people can't afford mortgages, not to mention divorces, high inflation, mortgages still rising, people leaving country etc.

Then a very long plateau, easy to time market, it's not as if it's gonna bounce like a basketball, then take off at a silly rate like a rocket ship, as it has done while interest rates have been at historic lows, not to mention all the other things that added fuel to the fire. The fuel is gone, only popcorn is left.

In terms of residential construction, I think it’s a bit weaker than you have suggested.

That is officially confirmed by the atrocious confidence readings in the sector in the past 2 ANZ surveys.

Personally I know several pretty credible mid-scale developers who are close to the brink.

It's sure still going very well in my end of the market, which is middle to high end designs. Plenty of customers with solid financial resources out there. But that's a very different animal from business confidence - eg: I am aware of high-end builders without escalation clauses that have been stung hard by material & labour cost increases, and losing key staff at critical times to competitors in an auction-like environment. These guys must be hurting and close, but then again it's not too far off situation-normal for them - trading insolvently is only a problem, if you get stat dec'd.

Upper middle / high end - sure. But overall that’s a minority of the sector

The turn has just started, it's been trending high for a very long time, it's a long drop in all senses of the word.

High end may lag behind, but if overall economy tanks in NZ and World high end people have business all business gets impacted by macro economy. They do not operate in silos even Oligarchs are getting punished.

High inflation in construction. Existing homes are going to look cheap soon, dont wait until everybody wakes up

Will be more than offset in falling land values which is where the bulk of the cost is in housing in NZ

Nah it won't. The raw land cost is a small portion of the section prices. Do you think those with bigger lots will accept huge reductions. Nope they won't. And the others in the chain incl councils and govt have fixed and/or increasing charges

You're either spruiking for personal gain, or delusional.

And you're just trolling. If you disagree that is fine, why dont you provide some basis

No he makes some good points.

Especially in medium and high density development, the land cost per dwelling is a small proportion of the sales price per dwelling.

That’s assuming developers continue to buy and build which is exactly what HW2 is saying is stopping.

Why is there an OR should be AND.

The absolutely delusional are those who think that because interest rates doubled, the price of houses will halve. Great name by the way

The bigger lots and development do have big reductions. Normally after the banks has appointed the receiver. Happens every cycle.

Yep that's the time to grab a bargain because the seller has a figurative gun to their head and there are few willing buyers. That tells you that not many see the opportunities when they are presented.

Why be surprised as is perfectly in tune with current market condition.

Be happy for now that are not witnessing default by construction company or going bust, which too is not far if the situation continues, which it seems will.

Read the market.

There are cashflow problems everywhere in construction, and once the pipeline closes next year many will go

Yes.

It’s an extremely slow motion train wreck.

…but about to speed up

Yep. Many of these businesses have been barely making it through for 2 years on the hopes things will pick up.

Why build house’s most of population in Auckland can’t afford.

A simple statement but a good one. When interest rates were low many could afford them. But the equation has markedly shifted.

Could they afford them or banks were lending when they shouldn't. Most were at DTI of 10, doesn't sound affordable.

Why indeed. Why let new migrants bring in up to six parents per couple? Who could possibly say.

Because some can afford them, and they're the ones that'll buy them?

I'll give you a hint, not everything in life is created for average people to buy.

But a much smaller number can afford to buy them, and that’s why new home sales, sales off plans etc have fallen off the cliff.

Townhouse developments are going to fall away big time.

Sure, but DTRH has a logic that house prices will fall 80% or whatever, and that's dictated by what average incomes can afford.

Why stop at average incomes? Let's say 95%, so Bevan who still lives at home and does 15hrs a week pushing trolleys round the Pak N Save carpark can afford them.

Pa1nter you are getting upset again. Price’s are falling at a accelerating pace all I have said is it will find a bottom when average wage couple can afford to purchase a house for family. Facts are quite simple rates and inflation are climbing NZD is tanking putting more pressure on inflation. Pa1nter it’s obvious you have a lot invested in housing industry but this market is dead and people like yourself who did not see the signs are now holding the bag of debt.

Totally incorrect, I just like sensible trains of thought. Let me tell you a distinction:

- I think it's a good thing if the average income can afford a house

- the cost of houses isn't dictated by what average people can afford.

Therefore, I find spamming "80% falls are coming to fall in line with average income DTIs" the intellectual equivalent of making fart sounds with my armpit.

the price of real estate could find a floor around the replacement cost of the dwelling, although it may drop lower before it stabilizes. that may mean the land value declines somewhat.

the bigger issue is that the last time this happened people's debt levels were two orders of magnitude lower.

debt is a multiplier in inflationary times but a millstone in deflationary conditions. note I am referring to inflation/deflation only relative to the price of houses here.

Pa1nter you are crying again calm down, you are the only one making fart sounds are you in adult diapers. Lets get back to the point I have said housing market will find a bottom when average wage couples can purchase you mentioned 80% falls I was thinking 60% from peak. And the cost of housing is dictated by what the average family can afford this is why as rates raise less people can purchase, Pa1nter you really are embarrassing yourself today with a lack of basic financial knowledge. Go and see a financial advisor they will help you.

Where is the immutable law dictated by what average households can afford? 200 years ago, the average household were very unlikely to own their house. People have become more prosperous over time, but there is nothing to say prices have to be a certain level based on what most people can pay.

Average households need somewhere to live. If they can afford to buy their own, sweet, if they can't, someone else will probably own the house and the average household will be renting it.

You keep citing a wish, not a certainty.

200 years ago eh.

That was a safe timeframe. Even a hundred years ago, home ownership rates for the average income weren't amazing. It was only a concerted effort from about the 50s on to push home ownership that it's now in the common psychology of what's expected.

I can only hope you're right. I hope even more things will get to the stage that a single income family can afford a home but I'm not naive about it.

On another note, apostrophes denote possession or a contraction (usually replacing the letter i or o). So when you type 'photo's' ask yourself, who owns the photo? (The boy's photo, or the family's photo.) Or is it a simple plural (which doesn't need an apostrophe)? If the word is plural (photos), are you referring to an attribute belonging to all the photos or a single photo (the photo's finish was matte. The rest of the photos' finish was gloss).

Do you get free beer with that.

DTRH - May be close to that now, at least in some areas of Auckland. For example, the August 2022 lower quartile house price was $850,000 in Auckland. The 2022 average household income in Auckland is $146,509 which gives an affordable price of $732,545 (if affordable is defined as up to 5 times income)

Each month house price’s are dropping so if you are jumping into market now the chances you will be in negative equity within a year, with rates and inflation climbing and NZD tanking which will keep pressure on inflation it would be wise to wait, that 20% deposit you have could turn into a 35% deposit very quickly. Some people on here still find it hard to understand we have moved from cheap debt to a climbing debt tsunami could be a number of these people are way over leveraged and have a ulterior motive to keep pumping up housing market.

Jobs like nursing teaching do not provide enough income to buy a million plus house, over next few years as house price’s continue to crash this could change.but new build’s are just not viable at this time the wheels are falling of the housing industry and a lot of investors will get burnt, still a lot of people have made huge amounts from housing over last few years the smart ones moved on end of last year.

Lol - but when the average person can't buy the average house then something is going to break.

Either the housing market or the social contract between the classes of society.

We need to make houses as unaffordable as possible. So only those who already own houses can access the required credit by using leverage (they would otherwise never be able to purchase the houses surplus to their needs), and subsequently rent to those who don't have access to leveraged credit in order to derive a lazy income.

Not so long ago a couple say a nurse and teacher could easily purchase a home, now in Auckland you are looking at a million plus for a house far out of the range for a couple who are earning more than average wages, price’s are now falling but still way out of most of populations reach who don’t already have a property to finance this.

What about the average income earner instead of the average person.

Last month there was 5000 homes sold and FHB make up about a fifth or more of that number.

I would like to know whether you have a goal of buying a home

Because falling land values will make them affordable.

No they won’t make them affordable, unless the fall is huge ie. at least 35-40%.

Which I guess is possible, although only remotely so.

Only at the margins will you see these falls as most professional developers are land banking and have no need to sell. The good ones have been through this before, are not overextended and know how to live cheap when needed. It's the the normal credit cycle, happened before and will happen again. The inexperienced get burnt as they buy the hype

Most developers about to be ex-developers

I don't think that there's any uncertainty around where immigration numbers will end up.

All seemed that way even in March 2020.

-pandemic, borders closed, money trough enabled

- sad times

- national government in 2023, some property restrictions rolled back, immigration taps turned up to 11

- happy times come 2024/2025

Although admittedly it was hard to see Putin shitting the bed so bad in 2022, or how sick global economics look like they're becoming.

Retirement villages with security, nursing, shops and club are going to be a growth area in Auckland and around country.

The retirement village model relies on aver increasing house prices. They are effectively real estate investors using granny's cash.

Their business model is about to be wrecked.

There model worked back when houses where half current levels, it will work again but there will be pain as existijng righ tto occupy holders think what they paid will be recoverable less the 25-35% rules etc who really holds the risk? yep the unit license holders, and they will shuffle off within the expected 3-5 years

We all hopefully get old and retire this is the age of the baby boomers with the profits from housing purchased years ago it gives them a chance to live in a secure community with all they need.

Problem is:

a) Who wants to be surrounded by a bunch of old busy-bodies. (Well a busy-body maybe, but I am not one of those. Or I hope I am not!)

b) Once one or both get really sick, many rest homes are not set up to cater for that or are full of those high needs people. Hence one (and probably both) have to go elsewhere. And at that point any surplus funds derived from selling their family home may have been lost in the mists of time.

No thanks. We're 75 and have a mortgage-free house, but any money left over when we die (who knows when - could be next year for all we know) will be going to help our descendants, not retirement village operators. We don't feel we're old enough anyway to join that sort of community and will probably never be. My 91 year old neighbour used to say that too - that she'd never be old enough to want that lifestyle!

No, the retirement model has predetermined sale prices and buy prices.

The differential is hundreds of thousands and that is borne by the person selling the retirement unit back to the retirement home owner.

There is also the cost to refurbish the unit, that is borne also by the seller of the retirement unit.

A total cash grab from the retirees back to the retirement owner. Brutal.

Yes it is very brutal, the cost of providing the hospital level care in the big house is also very high.

Personally I do not see the model surviving a MASSIVE house price shock say 50% as more children may welcome parents back into mutigenerational houes instead of homes..... but a 30% no issues.

Big 5 bd rm houses in AKL are hard to find they hold price way better then 2's and 3 bd rms

You haven't thought it through Stephen.

The model relies on an ever-increasing lic to occ being charged. And for that to work they need new buyers selling their own homes at an ever-increasing price.

Plenty of grannies at the moment who can't sell their home at prices high enough to complete the contract on their new LTO - one living right next door to me!

Pa1nter - as you know many have never been able to afford to buy, the issue is, at what price level is investment housing worth buying on a yield based analysis, now that so many things are NOT DEDUCTABLE one suspects a lot lower.... so investors may well return OR NOT...

I guess the problem is viewing it like a traditional investment.

If it's an active investment, you're going to want to see at least 10 cents on the dollar.

If it's something more passive, people will stomach less. Rental yields generally haven't made sense to me for quite some time now, but for shits and giggles, let's go for 7%

But you cannot deduct interest.... for tax, so to achieve a 7% yield how big would the rent need to be, or actually how low must your purchase price be? at the bottom of the market whoever is in governement will need to reverse that one to help attract people back into the market.

I mean, if you knew what you were doing you'd rent the house to the government so interest deductibility was back on.

Kind of a hard question as are we determining what sort of property exactly we are dealing with, and how much are we borrowing?

non commercial residential real estate, no hotel rroms, normal rental agreement via loacl property manager.....

do the maths

1mill cost 300k down funding 700k at 6.5% interest = 45.5k interest... rates lets say 3k maintenance lets say 5k (clearly deffering) rent perhaps you get 700per week less agency fees 8% so 33.5 ish

so 33.5 - 5 - 3 = 25.5 tax able..... because you cannot deduct interest... not even paying the interest bill or providing a tax rebate....

lets do numbers again at 500k

500k cost 300k down funding 200k at 6.5% interest = 13k interest... rates lets say 3k maintenance lets say 5k (clearly deffering) rent perhaps you get 700per week less agency fees 8% so 33.5 ish

so 33.5 - 5 - 3 = 25.5 tax able..... because you cannot deduct interest...now its starting to pay for itself as you tech lets say you paying 40% tax on the 25.5 = 15.3 less interest at 13k mmmmm

still looks sad with no cap gain, you need at least ? to cover inflation your 300k could be making ?? in a term dep?

Yeah so if you were at ground zero today, no other assets or decent holding income or experience, stock standard house borrowed to the max, she dont stack up.

I wonder if all the dynamics in your equation are permanently fixed or shorter term.

What iif this happens in NZ or is NZ immune :

https://www.telegraph.co.uk/business/2022/10/13/house-market-crash-will…

we are not immune but with increasing build costs its hard to see quality new builds falling back to 2013, the prospect for 30-40 year old sh*tters is not so flash as they where almost land value in 2013 and def are 99% land value now.... funny how villas hold there value when they are cold and drafty and have small windows and not enough entertaining spacs for young famillies.....

2013 would imply about 55% fall for pure land value from the nov 21 peak, yeah I can see that happening , if developement grinds to a stop who wants pure land.....(unless you want to live in the old sh*tter until you can rebuild).... try that with a young family... many of the sites will still cost 1 mil for 800 sq m

dont see falls like this on newish stuff thats sub divided , maybe 30% from peaks ie 1.6 becomes 1.15 ish

non paywalled below

A decade of house price growth will be wiped out as the Bank of England more aggressively increases interest rates, economists have warned.

Simon French, chief economist at Panmure, predicted that average house prices will fall 14pc over the next three years, a 29pc slump in real terms.

He said: “This would take the inflation-adjusted average price for UK houses back to a level last seen in [the] first quarter [of] 2013 before the Help to Buy programme was instigated.”

The impact on household wealth from the price falls would reduce consumer spending by £35bn per year over the next three years, Panmure predicted.

Mr French added: “The UK housing market faces up to its biggest challenge since the global financial crisis and arguably, given that the huge monetary easing that took place during that period is unlikely to be repeated, the coming years look more similar to the challenges of the early 1990s.”

The forecasts came as it emerged that banks were preparing to slash mortgage lending by as much as levels recorded during the depths of the financial crisis even before Kwasi Kwarteng’s mini-Budget triggered chaos in the market.

The Bank of England’s credit conditions survey, which tracks bank expectations for mortgage lending in the fourth quarter, slumped to a net balance of minus 41 as the housing market is buffeted by soaring interest rates.

If realised, it would be the second-weakest mortgage lending since the credit crunch in 2008 after the lockdown-impacted second quarter of 2020. It compares to a score of minus 13.3 for the past three months.

Banks pointed to a deteriorating economic outlook and expectations for house price falls as reasons they are preparing to rein in lending.

However, the credit squeeze could be even worse as the Bank’s quarterly survey was conducted before Kwasi Kwarteng’s mini-Budget. Lenders also expected to rein in unsecured lending, such as credit cards, but less dramatically.

Andrew Wishart, property economist at Capital Economics, said: “It shows rising interest rates and the darkening outlook were already weighing on both the availability of and demand for credit.”

He pointed out that since the survey was taken markets have ramped up their bets on interest rate rises. Investors currently expect the Bank of England to lift rates to 5.5pc by mid-2023, a major drag on activity in the housing market.

That's because they have stood the test of time and you can be reasonably sure they won't leak and rot.

There is still lots of room for builders to reduce their margins. I calculate many are working on margins of over 60%.

Good Point.

During GFC when world was falling apart, house value in NZ dipped only 10% to 15% (Correct me if wrong as remember reading it), will this time too NZ will escape from what happens in rest of developed world or will it lead just the way it was leading in house price rise during pandemic.

Wait and Watch

During the GFC the OCR dropped more than 6 percentage points. This time it's reversed.

a fact that is somewhat obvious to way too few.... espescially RE agents

Sure interest rates dropped, but the banks weren't leading and were foreclosing as fast as possible without panicking the masses. Interest rates in nz were very high prior to fix Michael Cullens go for growth mess.

The 20+ year bond exchange traded fund (ticker TLT) in the US has dropped back to 2010-2013 prices on the back of rising interest rates. As long term bonds are priced in a similar fashion to mortgaged land/houses...that is discounted cash flows of a set quantity of debt over a given duration, this index might provide an indication of where house prices are heading unless we see a significant change in inflation or monetary policy in the near future.

The TLT bond index is currently down 40% and dropping.

iShares 20+ Year Treasury Bond ETF (TLT) Stock Price, News, Quote & History - Yahoo Finance

In separate - and far more provoative -comments made earlier in the day during a JPMorgan investor seminar where he led a fireside chat moderated by JPMorgan's Gergana Thiel, Dimon made some extremely outspoken comments which however you won't hear on the mainstream media, telling a small group of listeners that was closed to the press that the

"President of the Unites States needs to stand up and say we may not meet our 2050 climate objectives because this is a f%$king war”.

He also said “time to stop going hat in hand to Venezuela and Saudi and start pumping more oil & gas in the USA”

Echoing what he has said before, Jamie said this is the way the USA maintains its standing, as the future of the world is by pumping more oil and gas and using energy security to ensure Western unity.

And he did say when it comes to ESG “investors don’t give a shit” warning not to "cede governance to do-gooder kids on a committee”.

Finally, he stressed the need for strong American leadership that is not being provided by either party. His conclusion: the world needs American diplomacy and neither Trump or Biden can lead the USA.

A decade of house price growth will be wiped out as the Bank of England more aggressively increases interest rates, economists have warned.

Simon French, chief economist at Panmure, predicted that average house prices will fall 14pc over the next three years, a 29pc slump in real terms.

Puts into perspective how crazy Auckland got, we are already down 14% add in inflation and we only back to early 2021 type levels, a decade of wealth loss in NZ will cause a few issues as much is borrowed / leveraged.

Imagine your CV halving.... but the debt does not...

HPI down more than 17% in Auckland from peak

HouseMouse if we went back a dacade from the top Nov 21 so back to Nov 11..... what would the HPI tell us about the % falls required?

this rate of land devalue would decimate all bank retail and agri lending books, I would think we would be looking at huge printing for funding again and possibly a nationalised banking system. Aussie is less vulnerable land value to book wise, but would be in as much trouble due to resource company revenue collapse as china imploded

Nobody is even contemplating that if the housing crash in China continues at its current pace that there is a decent risk of property sales worldwide and a relocation of some of the capital the Chinese have squirreled overseas. This could have a significant effect on the top end of the NZ housing market.

Nobody publicly contemplating it. I have also ,imho, thought , that. If immigrant owners have significant leverage issues in property owned in their home country,it would be a considered move ,for many,to release equity from NZ held property,to shore up home country property investment. Not all,but if it was a significant number,then ,yes ,it will also depress the upper level of the local market. Also probably an increasing urgency to make that decision,as CNY / NZD is going rapidly against the benefits of repatriating capital,at the same time the capital to be released from a sale here is diminishing by the month.

I mentioned this as a possibility a number of times a year or so ago. It certainly doesn’t appear to have been borne out, or at least not yet.

I imagine many Chinese nationals would be desperate to retain their property ownership here - it’s freehold and away from the mitts of an authoritarian dictatorship…

Take it back to china? I doubt it, NZ houses are like swiss bank accounts, but even less transparent

You don’t have to guess what might happen in this scenario, only need to look at what did happen when Ireland actually experienced it. House price falls continue….more People with mortgages underwater….unemployment rises/people emigrate….banks have more non-performing loans….banks become insolvent (hopefully stops at this point in NZ because banks become foreign parents’ problem)…government bails out/nationalises banks….bank debt bankrupts government….IMF comes in to sort out the mess. Takes about 10 years. NZ is beginning year 2.

I’m glad to see house prices quoted in inflation adjusted terms as these are the prices in reality.

when adjusted for inflation price rises are always smaller than reported, but falls larger than reported.

Lots of technical stuff which I don't quite understand, but my guess is that today, we are half way there/down. Global housing markets are still way overpriced, especially in China, with ours right up there, with British Columbia, most of Australia & parts of the US & UK also very high. The NZ Govt will try to reopen everything next year which will help(?) but the global fallout will be severe & unavoidable for most. The UK markets are already quite shaky & it will be something like this that starts the first domino.

Back at the ranch, we're minus 10-12% to date so my 25-30% correction from peak, by this time next year, is still possible. We/I can live with that, but many can't, I know. Home buyers be patient. And if you don't have to sell for the next 6-9 months, don't. It may level off a bit over summer(?) but this is feeding in from multiple points on the compass still & no one trusts Putin. Or Biden. Or Jacinda. Or Trudeau. Or the EU. Or the ALP. Or Truss. Or.....

Plus the quality of many new builds are pretty shocking these days, best to stick with existing quality built.

Big generalisation. A lot of older homes are poorly built too, and then we also have the huge stock of leaky / potentially leaky houses.

Certainly noticed in our 1925 property. Currently renovating the kitchen, knocking out the old in built fireplace. The bricks come away alright, it's all the 16mm (5/8ths) rebar in the 150mm thick concrete top at 150mm intervals (900 deep) with stirrups every 200mm across the width.

An advertisement just popped up, all new homes from Sentinel Homes come with a 5k holiday!

I said many not all and I am not generalising, many contractors only work on small jobs and never return to the same property, many don’t give a crap about the job they do, specially younger ones.

I know that, much of my work revolves around the residential construction sector. Some of the quality of new builds leaves a lot to be desired, sure,

my point was that a lot of existing builds have problems too. I would say overall quality between new and existing builds is fairly comparable. One benefit at least with new builds is that they are generally much better insulated.

The sector in NZ has always been plagued by quality issues. It’s been a sector that cowboys have flocked to since the early days of the country’s colonisation..

Fair enough and in term of insulation, the new builds are far superior no doubt.

From what I see the quality issues in new builds are typically not so much about fundamental issues, such as structure and waterproofing etc, but more around finishing and more superficial stuff. Still annoying.

A lot of developers will now be trying to run their sunset clauses out. They can't afford to build the houses anymore.

Tony Alexander had charts that showed this months and months ago. Sales. Cliff. Off.

I'm surprised they can't share stats showing the number of dwellings they have done the various interim inspections on. If the slab is down there's a good chance the owner intends to finish the house and that's more current data than CCC, no?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.