There was a slight lift in the number of properties offered at the auctions monitored by interest.co.nz last week.

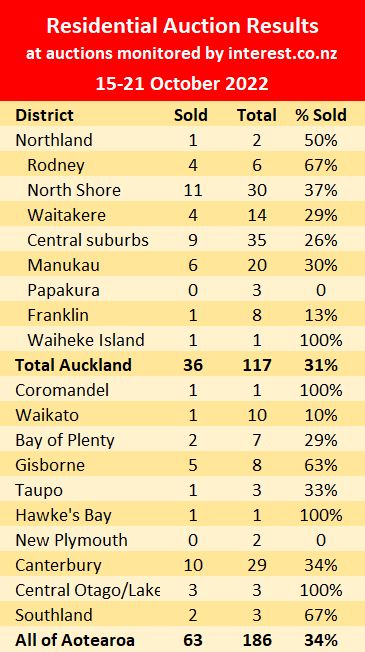

Interest.co.nz monitored the auctions for 186 residential properties last week, up from 164 the previous week.

However, that only took the numbers back up to where they were prior to the school holidays, so there still is not much sign of the usual spring lift in sales.

The number of properties selling at auction is also pretty flat, with 63 properties selling under the hammer at the monitored auctions last week, giving an overall sales rate of 34%, barely changed from 37% the previous week and 34% the week before that.

So the general impression is that auction activity remains pretty quiet even though we are now halfway through the spring selling season.

The table below gives the district-by-district results for the monitored auctions

Details of the individual properties offered at all of the auctions monitored by interest.co.nz are available on the Residential Auction Results page.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

93 Comments

A very flaccid state of affairs.

Thank you St Landers of Cheaper Tomorrow. Your Teachings are saving many.

Why Buy Today When It Will Be Cheaper Tomorrow !

Could just be the weather, it's been quite moist across the motu lately.

My question is, who the hell is, and dumb enough to be buying now? Most of the listings in Auckland are typical investor flick offs - easy to spot, they are usually painted battleship grey with tacking freedom furniture staging and a black mulch garden verge to hide the weeds.

Soon it will be starkling white with black trim and cool Ikea furnitures..

Given that the housing market is in correction mode, an auction clearance rate of around 30 per cent is respectable enough…….

Market recovery could well come sooner than certain people here would have us believe.

TTP

Which side of the OCR reaching 5.5 % will this new house bubble reinflate ... before the Reverse Bank has finished hiking , or sometime after ?

Market recovery will likely come much later than Tim and Tony A would like smart people to believe. Interest rates will decide the fate of the housing market, not these two 🤡🤡

Would they like smart people to believe it? Or would they like the majority of the sheeple, who aren’t so smart, to believe it?

Hi Tim.

When Property Brokers returns to its First Location In Havelock North at 17 Havelock Road then I will know you are serious. But the truth is even Ray White has taken over your original location, and that says something, how embarrassing, honestly, little Ray White ???

https://raywhite.co.nz/office/ray-white-hastings/2277/

Trick photography is actually making this office look bigger. Its a shoe box. Good for selling Tombstones though.

https://www.google.com/maps/uv?pb=!1s0x6d69cb13a253e1c9%3A0x596d4d450e6…

Wow times change fast. I thought they were still next to the mower shop, opposite the second hand dealer on Porter Drive. I should try driving with my eyes open.

No. They got demoted.

More very sad news.

https://www.stuff.co.nz/national/politics/300720422/prime-minister-jaci…

Nothing that an ejac** of cheap money and a defibrillator can't fix.

No where have I seen something similar to this before?!

A scheme to build one million new houses will be unveiled in Treasurer Jim Chalmers’ first budget...

https://www.smh.com.au/politics/federal/one-million-homes-to-be-built-u…

Someone promised a billion trees, and some plonker 100k houses.... then went on to try to sell us light rail... oh dear.

... we were promised fewer people sleeping in cars ... a reduction in child poverty ...

Somehow , it's all Putin's fault ... or the Gnats ... or Covid19 ...

... 5 years of failure / 5 years of lame excuses ... worst NZ government ever ...

Yep you cannot be in control for 6 years and keep blaming someone else sorry, I mean how long would you last in a real job underperforming like this lot ? Yep that's right about 6 months if you were in sales and had targets to meet.

True. Worst PM and Government in living memory. I was hoping for a quiet week while JA was virtue signalling in Antarctica but the penguins voted to send her plane back.

National promised to reduce house prices when they were elected 14 odd years ago. Instead they did absolutely nothing for about 6 years and then sent out Nick Smith with some special housing zones etc. And now they intend on reversing Labour's tax rules and don't seem to have any other ideas.

Labour have done some very good things with property; plenty of houses have been built, speculative tax incentives removed. That is much more than National did, so not sure how that makes Labour the worst? Neither party plans to significantly change monetary policy, which is quite obviously the thing that caused all this mess.

National undertook tax measures on residential property 1. Removal of depreciation 2. Brightline test

Then brought in special housing areas, which Labour spitefully removed

National progressed social housing builds, I think including the rebuild of Mt Roskill.

Did they do any of that in their first 5 years?

I can't remember, I am sure they did. You have to remember that the urgency for housing measures did not exist early on in 2009 to 2011. The opposite was true. What I do know is that Labour claims ALL the credit for the state house building programmes that were happening at the time of the 2017 election.

Showing a lot of Labour bias there Jimbo.

you may recall National oversaw the amalgamation of Auckland councils and mandated the Auckland Unitary Plan. When said plan was notified, the government via Kainga Ora was instrumental through its submissions in getting a huge amount more higher density zoning.

the Nats also introduced the National Policy Statement - Urban Development Capacity.

With interest rates still rising, and inevitably so, it is also inevitable that we are still in the early to mid stages of the house price decline.

KeithW

With interest rates still rising, and inevitably so, it is also inevitable that we are still in the early to mid stages of the house price decline.

KeithW

Of course there is no historical precedent for what we are experiencing, particularly in the Anglosphere. A prolonged period of suppressed price of money followed by completely unexpected events and conditions that have repriced money beyond what economies, businesses and h'holds had prepared for.

After the 1987 share crash interest rates dropped and house prices fell at the same time, I fully expect that interest rates will start dropping soon to try and offset global depresion/recession, and house prices will continue to fall as banks worry about job losses from buyers and while the cost of money falls, its availibility is much more limited.

Just as fiary dust wealth was created in your own home without selling it, it will be extracted the same way.

Dropping rates now to limit the damage of the coming recession may ensure that we have inflation embedded in the economy for years that is above the 1-3 mandated band.

That remains bad for asset prices in real terms.

Its the opposite of the 1980 (ish) to 2020 trend where each recession resulted in lower inflation and interest rates which caused asset prices to rise.

The reverse may now be true where dropping rates to limit the damage a recession causes more inflation, which limits asset price growth even further.

(remeber that we still have massively stimulatory interest rate settings, while inflation is at multi-decade highs! Which if viewed in isolation, is completely nuts).

(remeber that we still have massively stimulatory interest rate settings, while inflation is at multi-decade highs! Which if viewed in isolation, is completely nuts).

Those settings "appear" to be stimulatory because they're below the reported rate of inflation. But be careful here. Remember that Japan's biggest issue has not been lack of cheap credit. It's a deficit of punters. Countries like NZ appear to have an endless stream of dunken sailor-type borrowers. But what if they dried up or were more discerning before signing on the dotted line? Things may have changed but are not evident yet.

True - I guess the cruicial issue will be whether this turns into a deflationary recession or not. At the moment I think we're heading for stagflation. But a deflationary recession that follows is still quite possible (after we've completely destroyed demand...but that will require quite high unemployment and quite a large drop in asset prices).

Japan had lots of corporate punters borrowing cheaply and buying international assets , look at Frucor etc......

just not punters willing to borrow and invest in Japanese assets etc

I have long being a proponent of the view that interest rates will drop, and potentially quite quickly, once economies slump / crash and demand destruction hits in full earnest.

I have been calling mid 2023 for that to occur/ but it might be more like mid-late 2023.

I put my money where my mouth is and recently locked in my mortgage only until mid 2024.

Time will tell.

You're guessing of course, just like everyone else.

There is no data or fact to base any call on. And some will guess correclty ..and then get called economic wizzzes in hindsight - overlooking that with so many guessing, someone has to get it right.

Notably, the DGM have a woeful track-record when it comes to housing market predictions - especially those concerning the future. 🤣🤣

Why would anyone believe you Timmy being the pricefixing / censured troll that you are..............keep em coming champ.

https://comcom.govt.nz/news-and-media/media-releases/2017/property-brok…

https://www.stuff.co.nz/business/farming/114671918/property-brokers-dir…

And this will be a reason why Property Brokers Offices are getting smaller and smaller.

Am I guessing? Only partly. We certainly don’t have historic precedent of interest rates being hiked aggressively while house prices are tanking.

I am betting on that combination being a recipe for recession and demand destruction, which will suck the heat out of inflation within a year.

But yeah could easily be wrong. Maybe we will have prolonged stagflation while nominal house prices are falling. Again that would be a first (real house prices fell in the 1970s, not nominal prices).

You could well be correct. Will the Fed pivot seems to be the key.? Even the most astute/skilled/experienced investors are all at odds over this question.

Given time I expect they will be forced to pivot, however I'd be surprised if that stopped NZ property 'correcting'.

Who knows (apart from Tim)?

Survivor bias....

You locked in the mortgage short term because the longer term rates were a killer and now you just living on a prayer. There is still going to be plenty of damage even if things go to your plan, late next year is looking a long way off if things continue the way they are currently. People should have broken their mortgages early in the year but they waited and hoped and couldn't face the higher rates.

Living on a prayer? Yeah, nah. I would love it if mortgage rates were 3.50-4.50% by mid 2024. Will I be remotely financially stretched if they are around 6-7% in mid 2024? Nah.

But like most people I would rather have more money than less.

With inflation high rates will not come down if they do it will be the end of USD as a reserve currency which would bring in biggest financial crash ever.

Hahaha

Wow you lot have got the professor spouting your simplistic bs... repeat something enough and it becomes a truth

Dont take this personally Keith, but come to think of it you were pushing hard on the black swan event scenario in 2020. How did that turn out

HW2,

Yes, I did in the very early days refer to COVID-19 as a black swan event.

Actually I remain comfortable with all of the COVID articles that I wrote.

I would be interested to know where you think, with hindsight, there was a significant flaw in what I wrote.

KeithW

Haha, answer with a question. I guess you can always say that the use of QE was unprecedented in NZ and that it changed the Black Swans potential outcome

In reality, the immediate economic aftermath in 2020 did not result in the type of carnage that the sharemarket reaction would have suggested. Your earliest predictions (from memory in January 2020) certainly appeared correct at the time. And it was a worrying time for all. But perhaps those scary predictions from respected voices like yourself and others simply served to exacerbate what came next. 1. The tremendous sharemarket collapse and 2. The government's and rbnz masssive QE package. There was always going to be an economic package. The question was, how big, and the dire forecasts would not have helped to rein it in. Now of course we are dealing with the excesses.

Question: should there be, in your opinion, a nz royal commission or inquiry into the pandemic. I believe that many other countries are doing so. But it looks our NZ pollies don't want to be scrutinised.

Now hit me with the metaphorical sword Keith.

HW2,

My recollection is that I referred to the pandemic itself as a black swan event, but I don't recall using the term in relation to the economic outcomes. It was in late January 2020 that I first identified that COVID-19 was going to be a huge event, but my recollection is that it would have been some weeks later when I became sufficiently concerned that COVID-19 as a health issue was being under-estimated that I started writing about it in public.

My recollection is that it was in early June 2020 when I first wrote about excessive QE but I did not associate that with black swans. Given the response of central banks in NZ and elsewhere, there was nothing unexpected in relation to those outcomes.

By June 2020 I foresaw that excessive QE would inevitably lead eventually to inflation, but the asset inflation started to occur earlier than I had expected. It was November 2020 when I recognised that asset inflation was well under way and I made urgent major decisions about my own asset portfolio at that time. And I am pleased that I did so, although with hindsight I would have been better to have made some decisions back in June 2020 when I first started cogitating about it. Once I did make some decisions in November 2020, it was largely a case of sitting back and watching, but I did write multiple times in 2021 reinforcing the expectation that inflation was going to be a major issue as a consequence of excessive money creation.

I don't see much point in a royal commission re the pandemic. Apart from consistently acting too slowly, I think the Government eventually got most of the health related decisions about right. However, I do think that the bureaucracy was and still is poorly structured for such events. And I don't have much faith in royal commissions as learning exercises.

I have also consistently supported the Government's fiscal response to the COVID situation given the social importance of keeping people in work at that time. But I have been consistently critical of the RBNZ monetary responses. And i have little confidence that they will get it right from here on.

I never expected that the inflation would be transitory and I very much doubt that inflation can be brought back to the target levels without a significant recession. That concerns me greatly because of the social consequences of a recession. My concerns are greatly exacerbated by the extent of the external current account deficit of $27 billion in the year to June 2022. And so I see hard times ahead for NZ extending out for quite some years. I do not consider that any of the political parties have grasped what is going to be needed. I am likely to write more about that, but finding the time to do so is a challenge.

If you consider my thinking to have been flawed, then you are welcome to systematically lay out those flaws. But please be explicit so we can all learn.

KeithW

Thank you Keith a very well laid out reply.

a black swan event, but I don't recall using the term in relation to the economic outcomes

That intrigues me, because probably all of the interest.co commentators did. The 'black swan' economic outcomes was a major discussion point

I mainly wanted to respond to your comments associating interest rates and house prices. Yes I partly agree. I'm surprised that you seem to have accepted such a simplistic1 for 1 premise, wholeheartedly. It has little merit as there are many factors involved that influence house prices. As for a basic example, in the world of commercial property cap rates are used to obtain a market value of a property. Even still a systematic cap rate should not be taken too blindly.

HW2,

I think excessively low interest rates were the dominant policy that drove the housing ponzi and the current rising interest rates (which also affect cap rates etc) are now the key factor (but not only,factor) reversing that ponzi. Excessively high immigration rates from about 2014 helped set up the situation. Regardless of government policy, I see relatively low immigration in coming years as the recession bites. Skilled people will be leaving rather than arriving. I see no black swan element to the economic conditions we now face. Everything has been playing out much as I expected given the monetary policies.

I acknowledge that a very few people had recogised the threat of a COVID-type pandemic prior to it occurring. But for society at large it was a black swan. However the economic outcomes that we are now starting to see were entirely predictable given the monetary responses. I emphasise again that I do not criticise the Government's fiscal responses in the first months of the pandemic - they kept people in work. It was the grossly excessive QE that set off the current inflation. If Milton Friedman and Keynes were with us today I think they would both shake their heads in wonder and say 'what a monetary mess!' And both of them would now fail to find a painless solution.

KeithW

A lot of ppl including me were calling covid a black swan. No shame in that.

Covid a Black Swan? Not even close.

Good of you Keith to indulge the troll.

They appear to have become more and more frantic and unhinged over the last few weeks, I suppose it is normal when their world view is crashing down around them and all the people they mocked for being DGMs and failures turned out to be right in the long run.

Piss off, there is enough other trolls on this site. Go after them if you want to show some balance, which you have no intention of doing. It was a fair question and observation. Pompous git, stop fucking up this thread

You need a hug houseworks. The market is going down regardless so just chill out man.

Thanks Amokk you don't have to worry about me. It MAY go down, I can handle that. I will leave it there

Aroha

Arrivederci

Spring has sprung, but the spring is broken. The weight of unrealistic expectations is simply to great. All the while interest rates continue to climb, and those accepting today's prices continue to ratchet prices downwards. Capital gains continue to vaporise like smoke, oh the humanity.

No sales equals no income. Lets go!!!

Real Estate agents leaving inductry and polytechs say appplications to join industry courses are down by a third.

Most importantly real estate does not look cheap to me on a yield basis vs cost of maintenance, tax deductability, rate bills, retal levels. Indeed its not looked that flash imho since about 2015, every since then its looked like the main reaon to invest has been the leveraged capital gains you get. Now we have leveraged capital losses, its no suprise no one is buying on an investment basis, and FTB are, in general, sitting on hands as prices are still falling.

Auctions are a perfect way to cover up lack of building conscented work as well, oh dear places like Ponsonby....

Yeah you can get 4.5% in a TD now which is better than most gross rental yields. No expenditure or management required! After all those years of yield not really mattering in the face of never ending future capital gains - we took this storey to it's inevitable limit with a blow off top in 2021.

5% 1 year TD rates at all the major banks by Feb 2023.

What is it about auctions that cover up unconsented work? Do you mean buyers generally do less due diligence, or something else?

The property is yours on the fall of the hammer warts and all, if there is competiting buyers you are happy to take the warts.

on a offer basis the lawyers get involved and start asking the vendors lawyers why a conscent was issued, but no inspoections ever carried out on that bathroom refit etc etc. It does not mean that the work was bad... but the competition of buyers means if you want the property you have to suck it up and take the risk.

Now the vendor has to answer questions, if they say to you the work was to standard (but not inspected) you have them later if issues.

Trust me this is massive in villas. Look at how much work is done as the council never held detailed interior drawings ....

That is true - The old Auckland council culled all interior records back in mid 2000's. Many DIYers took this opportunities to re-arrange their interior without major consequences..

Indeed Chairman

Expectations are its going to be pretty flat over summer. With rising building costs and wages, new builds are going to go to zero so at that point prices will hold. People that bought a couple of years ago will be fine and should have been paying down that debt as quickly as possible while rates were crazy low. Its going to be bad news for anyone who bought recently at the peak and didn't fix their mortgage for 5 years in time, reality is that's a small percentage of people.

Great insight Tony.

With rising building costs and wages, new builds are going to go to zero so at that point prices will hold....

It may be counterintuitive to how you think markets and buyer behavior work, but pressure will be on prices to "fall".

On that basis the irish property crash should not have impacted many either....

IMHO the people who will lose the most own the developement sites... without developement its just bare land with a token rental from an old crapper..... whats a 800sq m Manurewa site worth in that market, they rent for arounf 600 per week.? lets say you have to hold it for 5-10 years before it makes sense to develope it.

You get 31.2k in the door, paying rates and perhaps interest on 800-1000k of borrowing. Most would rather pay the 20k difference per year then admiot it but a number are going to be forced to sell so they can focus on keeping their own house.

The marginal forced sellors set the price for the entire Manurewa suburb. be easy pickings some of these sites where in the 280k rang about 10 years ago, peaked around 1.2-1.35 mil, so these guys not hurting that much even at 500k sale point.

Good comment, although I know for a fact that many of those ‘development sites’ bought in places like Manurewa, were bought in 2020 and 2021. Often for stupid prices like circa $1.2-$1.3 mill. Those sites will be worth about 900k now, every chance they will fall to 800k or less. Many of the people who bought these kinds of properties are in for some serious pain.

Bad suburb you have to often pay stormwater for entire street to get council signoff, council would rather not invest in pipes for entire suburb. Anyone forced to sell Manurewa has to be wondering where the bid will come from..... Turkish : Well the rabbit gets f*&ked. Tommy : [pauses] Proper f*&ked? Turkish : Yes, before "Zee Germans" get there.

Yes the places where prices have got out of sync with rents the most will hurt the most. That is probably both the high end of the market and the development sites.

Of course with interest rates going up so much rents are well and truly out of sync with asking prices across the board.

So Jimbo, if you owned a bond and it was returning 2% and suddenly other investments of similar risk started returning 6% what is your 10 year bond now worth......... Houses are just bonds plus some capital gain..... now capital loss most amatuer real estate investors use massive leverage just like UK pension funds where, of course the RBNZ isnt going to falsely hold up a bid in Manurewa to solve our amateur investors ass, like BoE just did UK Pension schemes..... just saying.... who is the patsy now?

"new builds are going to go to zero so at that point prices will hold"

Running through this scenario....if this happens what will all of these people involved in the building industry do for work? Will they chose to remain in NZ or will the leave?

If they stay but have no work, how will they pay their mortgage or their rent?

And if they leave, that is tens of thousands of people (perhaps more) effectively gone from the economy and not contributing tax, nor paying rent on somebody's rental, or leaving another home empty for a FHB to purchase.

Its like a bit hole or a void that needs to be filled in some manner - and if it is not, something deflates.

I suspect a lot of the slack will be picked up by Kainga Ora developments. It has taken a few years for their major development areas to be prepared for redevelopment.

Not so sure about that, they are another basket case of a public organisation. Also, their funding model for places like Mt Roskill is based off a third of housing redevelopment of their sites being market housing, with that drying up it will impact their model.

How many times do people need to be told the cost of a new build is irrelevant in comparison to accessibility of credit? Many I guess.

Is that sarcasm?

None of my colleagues nor friends have ever fixed for 2+ years. They were all greedy for those low low rates and bought new cars/splashed on overseas holidays.

Is that sarcasm?

No it is carlosm. When Carlos writes that most people took out 5 year fixed mortgage it should be read as most people didn't do that.

We're halfway through spring but there's no sign of a lift in residential auction activity

Only a die hard positive person will be expecting a miracle in spring.

Maybe there will be a Winter 23 bounce?

Maybe there will be a Winter 23 bounce?

There is a total lunar eclipse on November 8th, maybe that will do it???

'Only a die hard positive person will be expecting a miracle in spring."

May be after Sunday 9 April 2023 (Easter Sunday).. some do believe in resurrection!

We are graced less by the charming presence of spruikers in these comments. They might have disappeared entirely in 6 months. And that would be the sensible thing for them to do, as their views will look increasingly moronic.

Indeed. Well done Tim for making an effort to sell the magic of defying financial gravity.

I think they are too busy making repetitive "worst government ever" type posts (complete with pathetic attempts at humour) in other property forums. It makes their day to get a bunch of likes from other property investors that hate paying tax at all.

Real estate seminars/training events have shifted from fully catered to bring your own sammies😮

"Please notice all the bitcoin promoters who have tucked tail and vanished In the next 12 months, I predict the same thing will happen to the "passive income real estate" bros. It will be glorious."

Ramit Sethi, Author of the New York Times bestseller, 'I Will Teach You To Be Rich'

https://www.iwillteachyoutoberich.com/podcast/

Property Brokers bus trip to Flaxmere for the Investors will now be on Bicycles. Tim will be leading the way on his Raleigh 20.

step down the property ladder into the depths of hell does not have good radio appeal... go on Step it Down

Property Brokers Country , Property On The Slide.

Meanwhile in Melbourne

$5m sale in Melbourne’s holiday playground triggers pricing debate

Michael BlebySenior reporter

Oct 25, 2022 – 4.42pm

Save

Share

Banker turned Bradman Foundation chief executive Andrew Leeming has sold a 50-acre property on the Mornington Peninsula for a little over $5 million – almost $2 million below the last guided price before it was pulled from the market in May.

Mr Leeming’s 19.7-hectare property with a three-bedroom home was passed in at auction on Saturday and after negotiations sold for an undisclosed price just above $5 million, said sales agent James Redfern of RT Edgar.

The 50-acre (19.7ha) property with 3-bedroom house at 101 Meakins Road, Flinders, VIC.

The sale shows a huge decline in the pricing of properties on Melbourne’s holiday playground for the wealthy, but also triggered a debate about marketing practices in a falling market.

The 101 Meakins Road estate was marketed until May by Peninsula Sotheby’s International Realty agent Rob Curtain with a price guide of $7.5 million to $8 million. Before March it was priced in the $8.4 million to $9.2 million range.

“It’s still positive but it’s changed,” Mr Redfern said on Tuesday. “We’re not in that crazy COVID market where buyers were throwing everything at something that was available to buy. In a dynamic market, it’s really important to price property carefully.”

The result for the acreage property also triggered concerns of a major devaluation that would skew market expectations.

“No one would think it’s worth that,” Melbourne buyers advocate Emma Bloom said. “It’s really buggered up values down there.”

Potential buyers of Mornington Lengthy makeover: Peninsula properties are concerned about time delays if they want to build a new home, the agent said.

Pricing has changed sharply on the Mornington Peninsula. In February, a neighbouring four-bedroom house on 10.5 hectares at 18 Meakins Road sold for $9.85 million.

“[The vendor] was obviously encouraged by the sale across the road, but it fell on its face and auction actually worked against him and the market,” Mr Curtain said.

“Results like this can make markets move just as record sales move them in the other direction.”

Mr Leeming – who in 2018 told The Australian Financial Review of his experience in 2007 warning of, and then navigating, the impending global financial crisis – declined to comment.

Last year, he was appointed chief executive of the Bradman Foundation based in Bowral in the NSW Southern Highlands, which is dedicated to preserving the memory of Australia’s most famous cricketer. Records show Mr Leeming paid $640,000 for the property in April 2000.

Time is the enemy

Mr Redfern said there was a reset in prices. Buyers who wanted to build family homes or estates on large pieces of regional land were also increasingly hesitant because materials and labour shortages had turned the process into a three-year ordeal, he said.

“People are concerned about timelines for construction and building new houses,” Mr Redfern said.

“There might be a reset a little bit on price, but I don’t think it’s going to be dramatic. There has been a shift in people’s desire to buy. It’s still there, but we’re in a more balanced market now.”

Another agent, who declined to comment publicly, said his advice to the vendor was to wait longer and achieve a better result. Mr Redfern said the vendor had been patient.

“The vendor was very patient with the last agent for nine months,” he said. “I don’t think that strategy was working.”

Michael Bleby covers commercial and residential property, with a focus on housing and finance, construction, design & architecture. He also dabbles in the business of sport. Michael is based in Melbourne. Connect with Michael on Twitter. Email Michael at mbleby@afr.com

For sale | 3c Scenic Drive, Hill Park, Manukau City, Auckland - homes.co.nz

https://homes.co.nz/address/auckland/manurewa/3c-scenic-drive/gnKD

1.63m sold tonight

Not that great a price for a new, large ‘home+income’

Cheap land, Manurewa. Even shows that manuwera is gentrifying

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.