Activity was particularly subdued at Barfoot & Thompson's latest auctions, although the fact it was a short week after the Labour weekend holiday may have been a factor in that.

Auckland's biggest real estate agency took 80 residential properties to auction during the week of 22-28 October, which was the lowest number since the week of 10-16 September.

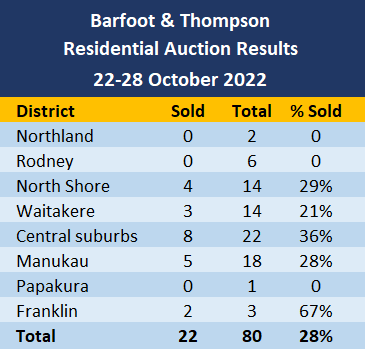

Of the properties offered at the latest auctions, 22 sold under the hammer, also the lowest number in six weeks, although the sales rate of 28% was about average for recent weeks.

The previous week (15-21 October) Barfoots offered 89 properties at auction and sold 24 under the hammer, giving a sales rate of 27%.

While a seasonal upturn in activity is still expected, it appears to be slow in arriving this year.

Details of of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

89 Comments

tothepoint - d… | 27th Jun 17, 4:54pm

“For folks like me, waiting for Auckland house prices to come down would be a poor strategy. The market in Auckland can't be relied upon to stoop down and pick us up”

“Guys like you and CJ099 are welcome to continue to try talking the market down. If you're successful, people like me will be enormously grateful to you. Please have no doubts about that”

Tim, on behalf all the "Doom Goblins" below, you’re most welcome 🙂

Can you remind us how much property has increased in value from 2017 to now...?

Nifty, its a work in progress, but we are getting there. Past performance is not indicative of future performance. Banking these gains you speak of is another story altogether. For those saving for their first home, keep saving for now as the amount of interest saved on a reduced debt load is a well deserved reward for patience and discipline.

The average house price rose by 6.6 percent to nearly $670,000 in 2017

https://www.rnz.co.nz/news/business/347860/housing-market-in-2017-price…

September 2022...with the national average value now sitting at $956,592. The average annual rate of home value growth (-2.1%) has descended into negative territory for the first time in more than a decade.

https://www.qv.co.nz/price-index/#:~:text=September%202022,value%20now%….

Long way to go to get back to where we were...

"Long way to go before we get back to where we were "

Patience.... 🤔. House prices are falling further and faster, interest rates are likely heading much higher, than your mentor😍 Tony Alexander even predicted.

There's no disputing how much they've risen, are you taking issue with how much house prices have already fallen?

Still seeing some good sales, some clearly don't want to put their lives on hold for X amount of years for pending dooms day... could be a chance to live in an area you'd never could of before. With decreasing stock, you're going to have to wait even longer for the right one.

Example - small 2 bedroom home:

https://harcourts.net/nz/office/milford/listing/mj52427-21a-stanley-ave…

Rating Valuation: $1,110,000

Sold for: $1,195,000

That’s certainly an amazing result, especially as it’s cross lease.

That second living room could definitely become a third bedroom quite easily, that might be a key reason it went for that price.

Still 75m2...

Bought in 2017 for $925k

You would of been smart if you'd listened to Retired Poppy in 2017 to wait...

Really good external storage which would mitigate the small floor area.

Still, I think someone’s paid too much for what it is. But each to their own.

Might be about getting into the schooling area since it's in Dual Westlake zone. The alternative is getting a 3 level townhouse at that price around Milford/Takapuna.

There's no need to put your life "on hold", or worse yet, waste the best years of your life in a lousy Milford dump.

Look at the lifestyle that could be had for the same amount of money.

https://www.realestate.com.au/buy/with-4-bedrooms-between-1100000-12000…

✈️ ✅

Just got to take exchange rate into account and you've gone backwards abit with purchasing power... then factor in moving costs, getting belongings across, pets across etc etc.

Don't be silly. That search was bracketed from 1.1M AUD to account for FX to the lousy 1.2M NZD bach in Milford, besides prices are falling over there too so an even better deal will be had by the time one gets there.

Jetstar is about $350 one way. A few grand to ship belongings. The average punter doesn't have pets because their current slumlord doesn't like pets. It's really not much more difficult than moving to the South Island.

A shabby two bedroom dump in Milford is always going to be there if one feels like seriously downgrading their life.

It's really not much more difficult than moving to the South Island.

Could you just not move to the South Island then? Cheaper houses, same currency, and maintain NZ benefits....

One could... but it's colder, there's not a whole lot going on and the houses are still lousy.

Believe it or not its quite easy to transfer between currencies and I'm not sure that the fat controller still sticking his extra greedy hand up your backside is a benefit one wants to maintain.

... so true , Brocky ... you're better off where you are ... it's a bitter 25°c here in the Waimak ... nasty cold weather ... sitting in my typical lousy Sth Island house ... sobering up after being at the Dunedin beer festival yesterday .... not a whole lot going on , indeed ... those Dogstar beers were sensational ...

Don't get me wrong, I really love the South Island.

But in terms of skilled white collar profession and events it's a bit quiet.

Maybe it could be a place to live sometime when older. Houses are (in general) still pretty lousy though.

I don't get what "putting their lives on hold" means. So renters aren't getting married, stop having kids, don't change job, don't travel? What else? I don't see what not owning your house stops you from doing in life. Used to own my house, now have been renting for 5 months. Nothing changed, at least from me.

Yes. I'm not sure how it can be achieved but the journey to owning your own home shouldn't have to be such an epic saga. There should never be 'fear of missing out' or even expectations of significant capital gain. Somewhere along the way people's expectations became completely warped.

... something is very warped in our society when houses become items of massive speculation & of enormous tax free capital gains ... and as a consequence a huge proportion of our population , particularly younger generations , get permanently priced out of home ownership ... no affordable houses left for friends & families ... the fat cats tied it all up , wealth got further concentrated into fewer hands ...

Was it really wealth? Or just the wealth effect? Maybe the reverse wealth effect will also be concentrated into few hands.

And that is one reason why the OCR will go higher than you would've otherwise thought as well.

Because those people hoarding 'wealth' through leveraged property speculation weren't actually spending the money in the economy after all - they were just collecting more houses! Though anyone stupid enough to purchase a vehicle, boat, etc. on the house may well feel the pinch as well.

WTB debt concentration report, dear RBNZ...

Reverend Retired-Poppy ( aka, The Reverend ). Going by your top post of the comment section it is obvious you are making people aware of the Crash. Clearly Property Brokers is feeling it with their Havelock North Office reduced down to the size of a shoe box. Many people thought it was gone altogether, I guess Tim can thank me for the promotion . With nails for coffins going up in value due to supply and demand Tim is now selling half price Tombstones out of the Havelock North office to celebrate his new demotion, I mean relocation.

Notably, auction clearance rate is being sustained despite the lull in the housing market - to the despair of certain people here.

Housing market remains an excellent long-term investment - as savvy investors know well.

TTP

Sustained at the levels that are consistent with the recent trend of 1-2% monthly falls in property prices. The trend will change at some point but the tea leaves don't look promising at the moment.

Gosh, I just wish first home buyers could have a bite of the cherry 😢🍒

Blah blah blah

TTP

Gosh, we have an impersonator above - in the form of “Fitzgerald”……

His brazen attempt to mislead and deceive people means he’s an outright shister/crook.

TTP

You calling somebody a shister/crook is the definition of Pot calling the Kettle black.

RP, your attempt to ridicule TTP is backfiring on you, he posted that in June 2017. On this occasion he was absolutely correct, buying back then would have been a great call, the drop in house value now and next year is small pittance compared to the insane gains of the last 5 years.

Also, by now, some principal would have repaid.

Fair enough, especially in terms of principal being paid down. But if prices fall 30% from peak to trough, which is possible, that could eradicate around 80% of capital gain since 2017.

Within Auckland, six of the seven territorial authorities had annual price decreases, with the North Shore’s the largest at 28.6% (to $949,000).

Prices were down annually in seven of the region’s eight territorial authorities, but South Wairarapa’s dropped the most with a 27.5% fall (to $700,000).

So you agree HM, that even if house prices fall a further 30%, it would still have been a better decision to buy in 2017

Yvil, it was you that commented 11 months later we're all heading into a depression😲

by Yvil | Fri, 04/05/2018 - 13:36 "So be brave and let the great depression happen, it's the purge the whole system needed. It's much better than the long slow downward spiral we're on now, which will still lead to a depression"

I think you're conveniently missing the point about tothepoint. Its your usual modus operandi in order to create an argument🤕

I'm flattered you hang on to all my posts even of 4 1/2 years ago RP.

1) your link has nothing to do with our discuassion that it would have been a good decision to buy a house in 2017, I guess you're just changing the subject because you realise you are losing the argument

2) nothing in my post of 2018 says that a depression is coming, do you not understand the difference between "let something happen because it's needed" and stating that "something IS going to happen" ?

"It's much better than the long slow downward spiral we're on now, which will still lead to a depression"

You can't even read your own posts properly lol!

Anyway, I can tell you're on your second bottle of wine 🍾🍾so you can argue with yourself now ok👀

So… you're saying that my prediction of 2018 was spot on, thanks RP.

The teachings of The Scrolls are spreading across the land.

Wouldn’t expect anything meaningfully different in these results for a long time.

Less properties going to auction. Be quick.

Agents are going to have to start telling the truth to sellers. #nosales #noincome.

Greg, why is a seasonal upturn still expected?

There is no universal rule that says it must happen. It certainly *usually* happens, but these are unusual times - especially the fact that prices are dropping AND interest rates keep rising.

Historical stats show there is always a surge in spring going thru to Xmas. Agents and agencies banks on it happening....

Yes but has there ever been a situation at this time of the year where prices are falling significantly and interest rates are rising aggressively?

I don’t think there has.

If you have experienced something for decades on end there HouseMouse you live your life in confirmation and recency bias.

Like Taleb's turkey - completely unaware that you're tomorrows roast dinner, despite again being fed well today, as you have been every day of your life.

I don't believe the Agents and Agencies will be laughing all the way to the Bank this year. Time to polish the Tombstones !

which if we take into account that the current sales reflect a seasonal surge - we can all look forward to after christmas when the decline in the Current surge occurs

Has retired poppy learned something new about financial markets because he has got the phrase "past performance...." on repeat these last two days.

Do you find it unsettling that others have hope that the future will be void of the absurd excesses of yesterday?

These historic gains you cling onto, can you still make them in a falling market such as this? Too much hard work perhaps?

No do you

I am more and more coming around to thinking that a severe stomping of the housing market is necessary and healthy. It will be very painful for some but a house shouldn't be going up 1-2k or more a week. If it is doing that then at some stage it's going to blow.

People do get significant benefits from owning their own homes and it earning twice the average income at the same time is quite some cherry on the top. Yet how can that possibly be sustainable?

This situation largely arose because of high immigration. The desirable cities in Canada, US, Australia and NZ were all affected in the same way. It was like a gold rush. Capital gains expectations went through the roof and this rubbed off on the locals as well. The high expectations bled out into the provincial cities.

Housing shortages and generous welfare policies fed the fire. Immigration continued at a high rate providing both investors and fresh people to farm.

To be healthy a time should come when escalating price rises stop and people get burnt. This will bring some reality back to the market. It's really only the flip side of high returns. High returns bring a risk of high losses.

House prices should only keep up with inflation as well as reflecting changing location desirability and improvements. So a property could still bring good returns. A clever renovation or taking advantage of a developing urban area could be profitable. However the returns should be realistic.

Who could have forseen the end result of this stupidity.

Doom goblins! Be quick!

I heard TA on NewStalk ZB this afternoon ... apparently house prices will not double in price every 10 years as they have in the past ... he says they'll rise at only 5 % p.a. on average ...

... ummmmm Tony .... that means they'll still double in price every 14 years ... that's not much improvement . .. considering wages are unlikely to rise that fast ....

Struth - maybe he really is an "independent economist"

He’s to be totally ignored. Lost all credibility. No more than a property Spruiker advocate, masquerading as a credible economist.

I think Zach, the consideration is the replacement cost of a home. So when it costs more and more to actually build a house new, it ain't getting much cheaper to buy one second hand. What do you think

Totally flawed.

Yes, totally flawed. Under the current conditions, all that implies is there is spiraling insurance costs for overvalued house replacement along side a bloating inventory of overpriced new home completions to consider. The ever increasing cost of labour and materials is a bubble in itself.

Its not sustainable and there will be tears.

Also much of the housing inflation has been in the land, and so too it will be for housing deflation.

To reduce the land price, one or all of the parties involved in preparing raw land into developable land will be cutting their costs and or margins. Take your pick from Original landowner, developer, contractors, council charges, govt taxes.

I can't see any of them being willing. Or is this totally flawed as well.

"I can't see any of them being willing"

Exactly, that's why there will be tears😭

They may not be willing, but unless they are loaded and can afford debt repayments, then they may be fine. Cause when people are not buying because it's to expensive, then something is going to break.

In my business I have prices and cost I try to make a 30 to 40% margin. But if I get it wrong and the market is highly competitive then one of my ways to shift product is reduce price, if I can't get rid of product even with price cuts then I liquidate, I'm better off cutting my losses instead of paying warehouse costs and other costs and moving on. Why are houses different. Customers don't care about my costs.

I think that is a good point to a degree.

Right...... How much of the replacement cost is actually fixed, and how much of it is suppliers/manufacturers all wanting a slice of the capital gains pie over the last few years? Ever consider that companies look quite closely at their price quality and opportunity? Existing house prices increased 30 - 40% in a year, not due to the cost of a replacement house, but due to loose credit and high demand. All the suppliers/manufacturers of building products will adjust their margins accordingly.

"House prices should only keep up with inflation as well as reflecting changing location desirability and improvements"

Correct - which has been my argument for quite some time (that even you have disagreed with in the past) - that prior to about 1990-2000, house prices were flat in real terms (i.e. they inflated at the rate of general inflation) for the previous 100 years.

It is only the last 20-30 years that house prices have inflated significantly above the rate of inflation - which is very dangerous and very unusual. Why my argument has been for quite some time that house prices could drop 50% in NZ in real terms in order to return to a sustainable trend. It could be more than 50% in real terms given what has happened in 2020 - 2021 (where inflation was near zero and house prices went up 40%). If intersts rates continue to moderate, and we have 5% inflation for the next 5 years and house prices fall 25% in nominal terms, we will see around a 50% drop in real house prices in this country.

If this happens, it will restore financial stability and most probably social/political stability as well. These are good things - not bad. Despite this view been called 'doom and gloom'.

IO, your scenario, should it play out, would be ideal. I certainly hope this can play out over a period of say 5-10 years so as to reduce the pain and trauma and temper the insane expectations, that sadly, had become the norm. These same people have become addicted to unsustainable returns that could now have put the financial system at risk.

"How dare these Doom Goblins stand in the way of us living the dream"

No person in their sane mind wants an asset price crash.

Article published 23-May 2018.

Westpac's David McLean says flat house prices for 20-30 years would gradually correct housing unaffordability without igniting the 'economic carnage' a big price drop would cause….

https://www.interest.co.nz/property/93884/westpacs-david-mclean-says-fl…

This speaks volumes about what the banks helped cause and what they already know. There are many out there who through their naivety have placed way too much trust not only in one commodity but that policy makers and bankers will always have their backs.

We will be seeing more stories like this:

Mum hit by big Auckland rates bill now worries she could lose her home

600k mortgage and having trouble paying the rates let alone the rising mortgage rates. On interest only too. Mortgage could go up a thousand or more a month.

She should sell the bloody home then.

All this handwringing about a homeowner needing to move.

Tenants of rentals are forced to move from their homes, all the bloody time. Ask any tenant for stories about the times they have been forced to move, at the whim of a landlord. Any tenant will have many stories to tell.

Why does one homeowner get a write up in the paper, all sympathy and sadness, when thousands of tenants get zero sympathy.

NZ has divided itself into 2 classes. The landowners, and the renters that nobody gives a toss about.

McLean could be right - however given the level of speculation we have seen, animal spirits could takeover if price falls continue/accelerate.

Its unusual for something that goes up like what our housing market, to have an orderly correction - especially with the rate at which the cost of capital is rising.

But high inflation for wages could be the saviour if wages keep up with the cost of living - meaning that we do see a significant drop in the price of housing in real terms - back to something that is financial sustainable/stable.

In the early 2000s I recall telling my wife that I couldn't see why house prices would go up excessively. Low inflation, stagnant wages. How wrong I was.

I blame immigration. The high quality immigrants would immediately observe the "houses double in price every ten years or less" phenomenon and act accordingly en masse. With there being no end in sight to continuing immigrant flows and rising wealth in their home countries it made a lot of sense.

"I blame immigration"

Does the price and availability of money play a part too?

Yes I was going to mention that. When I was working on my comment I lost it and had to start again and had that in mind too. I most certainly should have added, "aided and abetted by the banks".

I have always been somewhat opposed to importing "clever" people. NZ makes most of is money from primary agricultural exports. We could have continued to do that and all been very wealthy and educated with a population of 2 or 3 million. Perhaps had temporary farm workers from overseas with low ambitions.

Now, we have to compete globally for highly skilled individuals. On that stage, we are not doing so well. After the unprecedented money printing experiment and subsequent panic tightening, we remain in uncharted waters. Its sad when one reads articles where an elevated level of unemployment is required in order to temper inflation. This is peoples lives!

Is that because we just can't be bothered educating our own young people? There's always ram-raiding I guess.

Perhaps the solution to that problem is to crush all Mazda Demios and Nissan Tiidas and any related variants! Same process as gun surrendering 😂

Police can call it "Project Collins"

Another sign of financial and social instability that results from inequality and a system rigged against the 'have nots'.

But as you say in your original post, a general fall in house prices will be a good thing and I agree.

If we can give people hope that if they work hard that they may experience some success and prosperity, then this will reduce the social instability.

As it stands, those in the lower classes (and even middle class now) have lost that hope.

Why would you play by the rules if you've lost all hope of experiencing success within that system?

It's not that we can't be bothered educating our own young people.

We gave them heavy debts, poor housing choices, and then we couldn't be bothered employing them.

Until COVID closed the doors, it was pretty hard for a fresh graduate to get a job in NZ.

I watched many many young graduates over the last decade despair at trying to get a job. It was never that they weren't qualified enough - at the end of the day, someone from overseas would do the job cheaper.

I laugh at schools that whinge about not being able to get teachers. I've watched some complain they need UK teachers, knowing NZ-qualified teachers those schools didn't even bother replying to their applications.

I've watched the tech industry complain we need skilled workers, all the while using it as an excuse to funnel cheap 'skilled' labour from overseas into the lower echelons, who cost $30kpa less than a NZ graduate, simply because the NZ graduate knew what it actually cost to live here.

Two years after we closed the borders, I don't know any graduates who are unemployed.

Before that - those that could, left the country. And are probably far better off for it.

Yes, you are right. It's actually worse that we train them then refuse to hire them and also go on about attracting "quality" immigrants.

In the early 90s, 1994, a renowned NZ economist (Not TA) gave a talk that NZ house prices would stay low and what we were seeing at that time was a small bounce back. He recommended that kiwis buy shares. I met this person at an end of year function and got talking. Do you think he was following the sharemarket strategy. Absolutely not, he was hoeing into residential property in the upmarket suburbs.

Poor me, I had to make do with investing in working class suburbs.

The following article was published in 2003. All spruiking that contributed to this giant ponzi some see as a symbol of "success" should have been treated with the suspicion it rightfully deserved. Sadly - it wasn't.

https://www.nzherald.co.nz/nz/scam-warning-over-property-seminars/FJZZX…

As a consequence, all we may have to look forward to is a financial train wreck. For those in the legal profession - a nice little earner indeed.

Pathetic. Is that the best you can do?

by HW2 | 30th Oct 22, 9:53am 1667076808

Pathetic. Is that the best you can do?

Predictable response. Thank goodness you're not in the legal profession. Que the name calling too?

"Que the name calling"

Poopy poppy you don't have a leg to stand on

by HW2 | 30th Oct 22, 10:35am 1667079305

":Poopy poppy you don't have a leg to stand on"

Ooookay, so what part of my comment could you not understand? Perhaps, like Yvil, you're being purposefully obtuse because it makes perfect sense 👍😁

"I blame immigration. The high quality immigrants would immediately observe the "houses double in price every ten years or less" phenomenon and act accordingly en masse. With there being no end in sight to continuing immigrant flows and rising wealth in their home countries it made a lot of sense."

Good points and I don't disagree.

Unfortunately its first order thinking (at that time) without care for the 2nd/3rd consequences of that behaviour/environment/effects if nothing was done about it - which has been the basis of most of my posts on this website.

We appear to be at or approaching the 2nd/3rd order consequences now, which were visible if using 2nd/3rd order thinking many years ago - but that level of thinking wasn't politically popular (perhaps still isn't) and needed to be called 'doom and gloom' by those who were profiteering from the dysfunctional and unsustainable status quo.

If you used "and then what" thinking years ago - the outcome we are seeing now (financial and social instability) was quite high probability.

From about 2013, I've been thinking, with about 75% confidence, that if nothing changed with our policies towards housing, immigration, taxation and monetary policy, we were heading for financial and social anarchy - over that time I've been told that house prices falling was impossible, and belittled as a doom goblin - oddly only by those who were getting rich while quite likely sowing the seeds of social and financial misery. Such is the state of the society we find ourselves in.

Reading Dalio's 'The Changing World Order' you realise this has happened before - but it usually ends terribly unless we can work well together and find equitable solutions to the problems we face. If not, eventually the 'have nots' will forceably remove the current system that is in place and the wealth of the 'haves' will be taken from them. To most people who have experienced the last 50 years or so will say this is impossible, but if you read enough history, you realise it is not. Especially unless we beging to move closer together, as opposed to further apart - and current monetary policy and political views are driving people further and further apart.

.

Great comment and I totally agree.

why would you not wait and watch? seems a common sense approach as the market is subdued.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.