The traditional seasonal lift in activity is now well underway in Barfoot & Thompson's auction rooms with the agency offering 105 residential properties at its latest auctions (5-11 November), hanging on to the gain in numbers achieved the previous week.

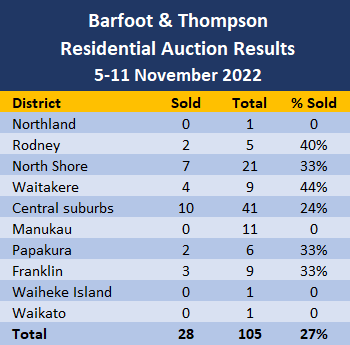

Of those, 28 were sold under the hammer, also exactly the same number as the previous week, giving an overall sales rate of 27%.

The coming week will be even busier, with around 150 properties on the Orders of Sale, which will mean auction activity will have more or less doubled over the last few weeks.

However the figures to watch over the next few weeks will be the sales rates, with between a quarter and a third of the properties offered typically selling under the hammer over winter and early spring.

Although the number of properties being offered at auction and the number selling under the hammer have both increased over the last few weeks, the overall sales rate has remained in the doldrums.

With little more than a month to go before the market goes into hibernation for the Christmas/New Year break, the sales rates over the next couple of weeks should be a good indicator of likely buyer enthusiasm over summer.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices of the properties that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

110 Comments

If you look at NZ Customs arrivals and departures, there's a lot more people coming in than going out, about 50k extra in the last 1.5 months. Can anyone explain this? Is it the effect of loosened work visa rules? It's probably a boost for the housing market on the demand side anyway...

In my industry we are seeing a big influx from South Africa. The vast majority I’d say. With their currency (Rand) being so diluted when they move here they all get shocked with the cost of renting and not many of them in a position to buy. Mostly tradies. I can’t really see how that particular situation will boost house prices??

The immigration spigot is going to be turned on full bore. Here and in other Western countries. Possibly something for the savvy property buyer to ponder. If nothing else it will be an army of tenants. Australia appears to be full with no rentals available, Canada is too cold and the UK too sad so many will likely be heading here.

Only problem is that your supposition is currently totally unproveable. Only with hindsight will you be able to say if you are "right". It sound more like a mantra you are repeating to yourself hoping to convince yourself it is true. Just saying.....

It's highly likely going by previous immigration numbers and now a labour shortage and a looming housing glut. The expansion of Auckland and the considerable infrastructure spend on motorways. Auckland and Hamilton and Rotorua have much improved motorway links.

Canada is not hiding its intentions to attract more immigrants also.

Canada wants 1.45 million more immigrants to fill labor gap

We will follow. Or are you implying NZ will not be attractive enough?

We were bringing in 100,000 a year pre covid yeah?

A lot of that demand won't have dropped off. And increased in some cases.

Country needs to bite the bullet and formalise a way to create new houses cheaper.

Country needs to bite the bullet and aim for a stable population.

The door is already open and the speed of people flooding in is only going to increase, this is not talked about on the “news”.

How about when recession bites in 2023 and job creation slows big time? There won’t be the same number of jobs for migrants to come to.

So I predict a little boom in terms of immigration but that will slow back down by May 2023.

There’s usually a bit of a surge this time of the year as young people come to NZ and work in hospo and tourism roles.

I'd have thought the timeframes involved in migrating wouldn't allow for such reactive flows of migrants.

Some of our shortages will take years to abate.

I suspect that this will be the major contributing factor to an increase in the unemployment rate. It will be created by increased population and business owners tightening their belts. We won’t see people being laid off as they have done in past recessions.

If I had a business about to go under, wages would either have to drop or some people would have to lose job. There's no alternative especially if most of my business you've already tried to trim costs. Whatever way it's not great for economy.

There are 50k more tourists in the country than there were six weeks ago, because tourists are coming back and we're getting closer to peak season. This literally happens every year - in fact pre-covid we typically saw a much larger increase over the same period.

Sorry if that doesn't fit the narrative you're trying to construct.

And this month it's tracking at 2 - 3k people per day which is 60k+ for the month. Interesting!

My suspicion is that reality is starting to bite. We will see more and more properties going to market and there are buyers out there if the price is right, ie heavily discounted.

A place went on the market around the corner from me a few months back and sold within days, I don't know what it sold for but I suspect very cheap. It was a run down old house that needed a lot of work or bulldozing.

There are two other properties in the same area for sale that are still asking 2020 money and have been on the market over 8 months with little to no interest.

Buying a house makes no sense for FHBs or investors at the moment, rent is about half of mortgage repayments in Auckland, so you would only do so if you were certain of capital gains and the old double every 10 years theory which is clearly unsustainable.

Jimbo - why do FHBs buy houses and why do investors buy houses?

Investors should be buying for the rental yield, but at the moment a term deposit is probably a better investment with much less hassle. Of course investors are actually into the capital gains, I think those days are gone for at least a decade, more likely to make a capital loss right now.

FHBs mostly buy because they want their own place and for the capital gain, but I can’t see them throwing away $500 a week or more for the privilege plus maintenance rates etc with no capital gain.

I doubt capital gains is a primary reason for many FHBs. I think it’s having your own home, plus the financial benefit of one day having a mortgage-free asset.

It was in the 90s I think that the language changed from a home to the biggest asset purchase of your life. About then we became a nation of financial advisors.

Now people/media waffle on about ladders and other such shite.

Life's a bitch if you arrive at 65 and you still couldn't find that ladder so its not really shite.

Standard NZ thinking there. If you have an income stream that you don't have to get out of bed for it really doesn't matter does it.

When we bought our first house the main two reasons were to not be throwing money away in rent and to have a place we could do what we want with (massive capital gains were not really expected then). Now in Auckland at least you would be throwing away much more than rent just in interest payments, maintenance, insurance and rates, and you probably have to buy the same kind of new townhouse you would be renting anyway because stand alone houses are too expensive, so you can’t really do much with it. And at least with renting if your attached neighbours suck you can just move.

Hi Nifty,

People have been refuting the old capital gain theory for decades - but it has a very strong track-record of remaining relevant.

Property will remain the preferred investment in NZ.

TTP

TTP there has also been a very strong track record of interest rates going lower. If you think house prices will continue to increase while interest rates go higher you will be wrong.

Hi Jimbo,

Property prices will continue to escalate over the long term. If you think differently, then good luck to you…..

I’ve a very strong track-record of accurate predictions about the housing market - which is a thorn in the side of certain people here.

TTP

I don’t really need luck, house prices don’t really affect me as I own our house and don't intend to buy another. You on the other hand are always going to predict price rises as your livelihood depends on it. But surely you do recognise that it is both economically and statistically unlikely that house prices will continue to outpace wages by so much, the cumulative effects of that get ridiculous quite quickly.

Agreed.

The is one small flaw in your logic however. That being you expect a response from TTP that is also based on it.

I think rent has been close to mortgage repayments most of the time throughout history. It differs a bit by location but normally at least within a few hundred dollars. It is so out of whack at the moment it’s crazy, and interest rates are still going up. Hard to see how we won’t get a massive house price crash of at least 40% unless interest rates drop soon. Rents can’t really go up much.

Front page of our local paper today is all about the cost of living crisis, and how many children are relying on food banks to survive.

Rents are about as high as they can go (without more govt handouts).

Renters are quite literally starving.

It's crazy! Especially when all the "mum and dad" landlords around the country claim to be charging below market rent for their properties.

Eject t eject eject. Goose I cant reach the ejection handles....

Owners will be waking up from their capital gain daze. After a year of capital decline and a horizon of further interest rises and anti speculator policy, many will be over it.

Time to eject. But who can buy and who would want to as prices continue back towards local tax payer income leveraging capacity?

It appears to me that the classic market phases are playing out in an recognisable pattern. Mania phase obviously in the past, " Blow-off" phase well underway. With repeated OCR increases and restriction of credit, the bull trap " return to normal" was very muted ,although many commentators ( T.A, AC ,& various bank economists tried hard to suggest amelioration of falling conditions ,for several months)

Now we are in the Fear( fongo) , capitulation - despair plunge. Capitulation not really here in full measure yet, will be in 18 months though, then despair stage maybe muted if labour market remains strong and inflationary wage increases can nearly keep up.

4 years from top to bottom, in my opinion ( not worth much, but I have traded 3 property cycles in the past). Why 4 years? As we were nearly topped out end of 2019,then RBNZ kicked can down the road and over the hill,with 70 billion effective input, meaning we got a double peak,and second peak was grossly excessive. It's not going to be a short & pretty trip to the bottom of this cycle. Inflation adjusted values similar to 2016 prices is my humble prediction. Nominal values will be bit higher. But by 2026,wages will be up 70%+ on 2016?

Seems a possible scenario.

However, I don't think inflation will be subdued for a while, and this time round there are fewer economies that will benefit from the typical rates drop effort.

Who knows though, maybe the Reserve Banks are going strong for long.

Good analysis. Although you could well be right, I see peak to trough at two years, not four years. I think the market will have bottomed out by November 2023.

Why?

- OCR hikes over by mid 2023

- A chance of an OCR cut or two by late 2023

- Renewed economic optimism with the election of a National government

I think once prices have bottomed out there will be a slow lift from the bottom. Nominal house values back to late 2021 peak not until circa 2026-2027.

Bottom out, Yes but has to be seen at what level.

Any further from here after 18% fall could be deciding factor as till now it has been absorbed by vendors with a pinch.

How much further fall from now on, will decide if we are able to avoid a crisis or will see bloodbath on the street.

Auctions in Auckland this week saw some pretty good prices being reached on select properties with some even being passed in with bids at the CV level and higher than what the vendor had paid only a year or two or three earlier.

Good locations and those with development potential seem to sell. Plus the odd one with a realistic vendor.

I have noticed a couple of properties being advertised as "this will sell", "owner moving" etc and yet still being passed in after receiving what appear to be healthy bids. Don't believe the agent's advertising blurbs!

From what I can tell and of course these auctions are a very small sample, properties haven't reached 2019 prices yet.

Real pain is not yet felt as have just cleared the froth but the cup is still full.This is reflection of the magnitute of money pumped by RBNZ and Government.

It is those few properties that are still receiving two or more bidders that is holding the race to the bottom supported by FHB, who are still under FOMO but changing fast.

Next few months will determine if it is just a simple crash of 20% or much more though all indication and data suggesting that worse is yet to come.

And there are examples of sales well below CV. Anecdote is worthless, hold on 2 days and we will have the HPI to mull over.

Is there a particular day the HPI data comes out every month?

Usually around the 13th/14th but sometimes earlier or later depending on weekends. Just head over to reinz reports and you can see the dates of recent reports

I wouldn't call auction results an anecdote - a short amusing or interesting story about a real incident or person.

I've generally been on the money with these sorts of things in the past. It's all we have right now, today. What the previous owner paid and the ratio of that with an earlier CV I have found to be revealing.

Of course we await the more complete data.

ZS - ok I’ll be blunt. I’ll take HPI over your cherry picking

Yeah but people come here and make "it's the end of the world!" comments and the auction results actually, not anecdotally, beg to differ in many cases.

I've been through this all before and last time it was like clubbing baby seals.

Do you eat those as well?

No animal is safe.

Auction results are useful to help give some commentary to the broad stats (HPI). Agents I have talked to are not doing this…. They are pretending things are ok and vendors are still getting good prices ( not true nothing is selling and listings are climbing steadily), so finding examples of sales gives some real-time examples of what is selling, very useful also having the QV estimate link on each property, they are surprisingly close to sale prices.

Yes, I like that, "commentary to the broad stats.."

That's a really good way of putting it.

I would say this fits the definition of an anecdote, unless you only use half the definition to show your point (which a lot of commenters on this forum do).

==Anecdote==

- a short amusing or interesting story about a real incident or person.

-

an account regarded as unreliable or hearsay

Auction sales results are "hard facts".

HPI for Auckland will be 21-22% down from peak.

This is again a misleading title. More properties auctioned but sales rate around the same (if not slightly lower).

It's weird how the title from the main page often isn't the same as the one at the head of the actual page.

It’s called clickbait

Yep, the headline gets people to click, the discrepancy between the headline and the facts in the article is bait for people to comment, and both clicks and comments are what advertisers want to see. It feels manipulative to me, and I think people would still click and comment if headlines more accurately reflected the content of the article so I don't know why they do it.

I agree it is very misleading, this website should be better than that, sorry to say. From the title I was expecting to see sales rates up to 35% or more.

The spring lift gathers pace in Barfoot & Thompson's auction rooms

Again the headline though not wrong is deceptive. Also if number of properties in Auction rise and number of properties sold remain same, it is fall in sale on percentage basis.

Many houses for auction, next week and if the success rate does not improve, next leg of fall from 15% to 20% will take off.

Single digits worth of lousy Auckland houses being auctioned in most districts.

Tremendously exciting.

It's the only barometer, albeit a fairly deficient one, for measuring what is happening in real time with NZ's favourite obsession.

Its hard to get excited about buying property knowing interest rates are going to 10% next year, guaranteed.

Also knowing property in areas like Wellington and Auckland have crashed already buy almost 200K, and we are just warming up for what is to come.

Who would want tot buy in the North Shore considering it has tanked by -28.6% already and many have not even renewed their mortgages to the new rate.

Renting has become very exciting.

Renting is certainly looking exciting Future...

Stats NZ reported an unusual surge in the cost of rent in October, the second most in one month since before the onset of the pandemic. Over the past decade, they have only risen as fast three times. It is a North Island thing

https://www.interest.co.nz/business/118420/review-things-you-need-know-…

Losing 4K per week on the value of your home, and sweating bullets to pay the new interest rates makes renting Exciting.

It leaves enough each week to buy popcorn, Extra Butter. ( only if you are renting )

What makes renting exciting: Not knowing how long you can live in the property, not knowing when you're next going to have you rent increased, not knowing when you're going to have maintenence done to the property, not knowing when your next property inspection will be, not knowing what will be in your next property inspection report card, not knowing when you'll ever be able to afford your own home...

Nifty1 do you think it is a good thing that so many Kiwis are forced to rent for life?

You describe almost a second class of citizenship. A lower, less stable, more deprived, way of life. Are you comfortable with living in such a divided society?

The NZ that I grew up in was much more egalitarian. Ordinary workers could buy their own houses. You describe a debased lifestyle for ordinary people.

What are your thoughts on this?

The New Zealand you grew up in was mostly the same. You were just younger and more naive.

Fitzgerald - didn't say it was good thing, it's just the reality of renting. A large reason why people still seek to buy their own home.

Some of missed the meeting that said it'd be easily attainable for everyone, forever.

It's called a rat race for a reason.

Actually, most of those things are predictable - if you're aware.

1. How long you can live in the property - if you're on a fixed term tenancy, it's until the end of that at least (house sells with you remaining the tenant). And you either renew or it automatically commutes to periodic (or find somewhere else if you wish). If periodic, house has to have actually sold before you can be given notice. Only time that changes is if the owner wants 'family' to move in, or you have been proven unsociable.

2. Your rent can only be increased once per year, and it has to be inline with market rates - which you can monitor via bonds lodged.

3. Maintenance - you can issue a 14-day Notice to fix. If they don't respond, take them to the tribunal. If they respond in any negative way, take them to the tribunal. Retaliatory action is a $3000 fine.

4. Your property inspection must be given at least 48 hours notice, and no more than 14 days, in advance. Whats on the 'report card' - wtf? Property inspection is a two-way deal: it's an opportunity for both parties to give feedback. The house is only required to be clean, tidy and undamaged bar wear-and-tear.

Of course, a lot of slumlords don't want their tenants to know these things...

As for the ever being able to afford their own home, most tenants already know the answer. Never! They are cattle who's working hours are being farmed by the bourgeoisie, in their race to 'get ahead'.

Nifty1. I rent, and I know the answers to your doubts, thats what contracts are for.

Its those that don't know yet that property values are going to Crash way past -30%, some as much as -80%, and interest rates going to 10%, those are the people that don't know what is coming.

Renting is exciting. And for those that would like to buy your own home, well, common sense would say to wait wait wait !

Losing 4K per week on the Landlords house is the fasted way to get into your own home when the time is right.

Living like a monk and working like the devil is arguably more reliable.

Doing anything like the Devil is never "reliable".

Future, how much $ per week were homeowners 'gaining' over the last couple of years? How about decades?

Sorry this is a frustratingly binary discussion!

Renting can be an excellent option, as can buying. Totally depends on circumstance.

We rented for many years, the biggest reason was we wanted to live in a good, safe area with very good schools. We could afford to do that by renting, there’s no way we could have afforded buying in those areas.

We also didn’t want to be slaves to long commutes.

We bought three years ago because our son had left home and our daughter was safely enrolled in Baradene. We could then justify buying in a lower value location because school zoning was no longer an issue for us.

Also, a longer commute - which actually isn’t that long at all - becomes less of an issue when you can work from home for much of the week. There was less freedom to do that just a few years ago.

And not caring about any maintenance ...pricelss

“What makes renting exciting: Not knowing how long you can live in the property, not knowing when you're next going to have you rent increased, not knowing when you're going to have maintenence done to the property, not knowing when your next property inspection will be, not knowing what will be in your next property inspection report card, not knowing when you'll ever be able to afford your own home...”

Or telling your children to take their decorations off the wall because it is no longer going to be their room, the room where bedtime stories were read every night…

Desperately trying to settle for anything you can find/afford within the same school zone. It gets even more sad if there is a lovely family pet involved…..not good.

There are some benefits though. if the local p dealer moves in next door and you are renting you can easily move. If you own you need to sell and buy in a falling market it will be stressful and probably very expensive.

I have been renting for 16 years while building a business.

None of what you describe has been my reality. We have had 3 tenures in that time, moved when needs changed. Had 1 rent increase per tenure over that entire period. Had great landlords who weren't adverse to fixing stuff. I'm pretty handy so generally just fix stuff myself. We have had a dog this entire time. The flexibility renting gives us works well for my life. I could go and get a mortgage and stop living. But instead I bought a yacht and intend to sail away.

Pretty sure I'm not the only exception to your pessimistic view.

Hi Sluggy. What is really going on here is Nifty50 is just a R.E Agent desperately trying to keep the Ponzi alive. He needs a job, and mowing lawns is not his thing.

Even the property investors admit that buying property so you can lose 4K per week before going Bankrupt due to the 10% Interest rates coming is NOT a good idea.

Notice how TTP always gets 4 upticks ?

Rates are not going to 10% next year the entire economy will capitulate and you will find yourself living in a tent.

Yeah , heard the same talk over and over about 7% Interest Rates This Year, Guaranteed ! And the Prophecy was Confirmed.

Same people said we would never see a 30% crash in home prices. North Shore already at -28.6%.

The entire economy is going to capitulate.

Remember the days when The Prophet would find out what your predictions would be for the OCR increase ? And he would just call the exact opposite because you were always so wrong ? Yeah. He was right .

What ever the Vested Interest say - Believe the Opposite.

Ahh so Future is Retired Poppy... so clever writing my name as nifty50? Must take alot of time logging in and out of multiple accounts. Chill and enjoy the weekend mate. There will be another article for you next week that you can go on about scrolls & BS, making you look desperate for a market crash like your life depended on it.

Yeah but imagine having to pay rent and floating interest payments on a new build that hasn’t been finished and is dropping by $4k/week. That’s the worst of both worlds.

More common scenario: being given notice to leave your rental you've been in for years, you have kids who are settled in schools, you're close to work and you have pets... You're under the pump to find a new place, rents have increased, no one wants pets, any property you find you like has lines out the door of applicants & you have to provide your life resume, with references & financial details to compete...

Happened to us a couple of years ago and was the sole reason we bought last year. Many of the social issues that NZ faces originate from unstable and poor quality housing.

Sorry to hear Albert.

If you dont mind?' What term did you fix the original mortgage at and is the time and new 2022+ % rate to refix at concerning?

Hi nzgecko,

We broke our large mortgage up into 4 terms at 1y 2.85%, 2yr 3.25% and 3 yr 3.49%. We also have a $200k offset facility that is fully offset. We just locked in the soon to be expiring 1 yr term for 3 years at 5.65%. It’s a big jump but not a material increase in payments as our whole mortgage wasn’t exposed to the new rates.

With 60,000 surplus houses already and many many still been built its working in the favour of the renter.

Losing 4K per week is a much worse situation, not to mention failing to pay 10% interest rates coming soon.

The new home owner would be bankrupt and back to square one looking for a home to rent anyway.

10% interest coming soon, do you mean for credit card accounts?

Was 7% Interest Rates This Year , Guaranteed for credit card accounts ?

Don't be a Silly Yvily .

Not fair for the children.

Rents usually bump up in October, it’s not that startling.

Boomers downsizing and helping each of their children getting into housing. Some have even opted for renting and enjoying retirement. Capital gains recycled back into the market as first home deposit.

Future, what's with this ridiculous statement; "knowing interest rates are going to 10% next year, guaranteed." There's absolutely no guarantee about interest rates going to 10% next year, that's just your own opinion. How are you guaranteeing this? What are you paying out if you're wrong?

Agree. It’s nonsense.

by HouseMouse | 11th Oct 22, 4:26pm

It’s getting very boring.

I long ago admitted I was wrong on interest rates.

And Btw there’s no chances fixed rates will get to 7% before Xmas. They almost certainly won’t get there next year either.

The Prophet has inside knowledge, and he passed that onto us in the Scroll.

"Interest Rates will continue to go Up from here and Stay Up for a Long Time."

"Banks will sell Mortgages at 10% +. ( Double Digits ). The OCR Forecast Peak Goalposts will continually be Moved Higher and Higher ! 10% Interest Rates Next Year, Guaranteed !"

Yvil - I suggest you print off the Scroll and put it on your Fridge. This will help you know what is coming !

You have already had to learn the hard way about 7% Interest Rates This Year, Guaranteed ! Don't make the same mistake twice.

Child

Imagine paying $810k for this place and today the lower end estimate is almost the same as your mortgage had you paid 20% deposit.

https://homes.co.nz/address/auckland/panmure/127c-queens-road/kOG0j

Renting would of solved that problem. And you forget to imagine what the 10% interest rates coming soon would feel like on that big mortgage .

Chances are it was probably an investor who bought it. The next rent review you know who's going to be hit...

Not the tenant, if they know their rights.

It's already been ruled in the tribunal that rents are a function of market value, not the landlord's costs.

So there's going to be an awful lot of disappointed landlords who may find out the hard way they can't just dump the extra interest costs on their tenants.

The Landlord will take the hit when all those with the same apartment in the complex fight to get a tenant as the owners compete to sell off against each other.

Considering North Shore has already Crashed by -28.6% it is going to be cheap.

Within Auckland, six of the seven territorial authorities had annual price decreases, with the North Shore’s the largest at 28.6% (to $949,000).

Prices were down annually in seven of the region’s eight territorial authorities, but South Wairarapa’s dropped the most with a 27.5% fall (to $700,000).

Future, how much $ per week were homeowners 'gaining' over the last couple of years? How about decades?

-28.6% lose has completely wiped away all the big gains over 2020 and 2021. Gone.

You are scraping the barrel if you are living your life in the past.

Future, what does "would of solved" mean?

‘Ex’ leakers…

Two thirds to three quarters unsold will continue to put downward pressure on prices. Some of these unsold properties will be removed from the market but the ones who stay in the market for sale will just have to drop their price expectation, there's no other way around it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.