- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

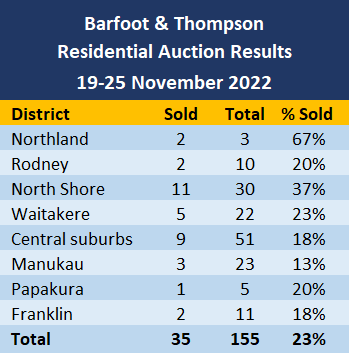

There was a slight increase in the number of properties offered at Barfoot & Thompson's latest auctions and a small decrease in the number sold.

Auckland's biggest real estate agency offered 155 residential properties at its latest auctions (19-25 November) up from 150 the previous week.

Of those, 35 sold under the hammer, down from 40 the previous week.

That pushed the overall sales rate down to 23% from 27% the previous week.

On their own the changes are not particularly significant and would not represent a shift in the market unless they were the start of a trend.

With just four weeks to go until Christmas, it's more likely the market will hold at around the current level until it winds up for the Christmas/New Year break.

Typically about a quarter of the properties being auctioned in Auckland are selling under the hammer at the moment.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices achieved on those that sold, are available on our Residential Auction Results page.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

177 Comments

Cool

Treading water.... another 'te mana o te wai' for Labour to tax

Agencies pushing Auctions in this market are not looking after their client's best interests. See lie agents use #12 here, https://www.noagent.co.nz/lies-agents-use/

For a property that doesn't sell at auction, a big percentage will sell soon after.

Sell...Yes but at what price ?

Ways in which Yvil will ban you, example 2.

That’s a great website cannot be banned for that

This makes worthwhile reading. The only sad part is that this tally of "Agent Lies" is based on real, and often life changing experiences. The skill of telling lies and being deceptive comes naturally for some.

Are agents or the likes of Homes.co.nz covered by the FMA? They both give advice on most peoples biggest financial investment, both are often misleading.

I have queried this before. If you listen to any type of independent advice relating to shares or investing there is always a spiel about "Speak to your financial advisor", "Markets can go down as well as up" etc etc but somehow the RE industry seems exempt when more often than not they are giving very specific financial advice that they are not necessarily qualified to give?

I had one last year say that they were better than registered values at giving you an accurate price and that valuers come to them for advice - that was during the time of very rapid price rises. Regardless I considered it to be very unprofessional, unethical talk and younger less experienced buyers probably took her at her word.

Yes if you start talking to a real estate agent about macroeconomics, the role of the Fed and its impact on NZ, the RBNZ and interest rates, the way that assets are priced using discounted future cash flows......their eyes glaze over and mostly (with a few exceptions..) they have no idea what you are talking about.

And yet they know and tell all of their customers that house prices will be worth more next year!

Not sure how this is legal.

Malamah, that's why Future got banned, the topic was the upcoming OCR review,

by Future | 20th Nov 22, 4:14pm

Oh your back Yvil. I guess you must be naked in that Padded White Room ? Or does that Straight Jacket come with Pants ?

Don't Bother Screaming at me either, it's sound Proof. Nice of that Nurse to comment for you though.

Nice one Yvil thanks

I wonder if the scrolls contain any prophecies about the over enthusiastic hall monitor being hoisted by his own petard.

30% falls by Christmas!

[I am just keeping the Prophet's seat warm. It looks like the prophesy may come remarkably close to coming true. Certainly -20% by Christmas is on the cards. ]

Should we have banned all those who have no good arguments that housing was over priced and yet their only rebuttal was that 'you are a doom golin?'

And yet there will be absolute silence from Yvil regarding these posts

#doublestandards

If you are true to your word - each time TTP replies to a comment of mine about housing affordability and simply calls me a 'doom goblin' with no reasoning or valid argument, I expect that you will report these comments please - for the sakes of consistency.

If not, your position and behaviour are highly hypocritical.

Future attacked me personally by insinuating that I belong in a mental asylum, so I took care of him. If you feel offended by TTP or anyone else's comments, don't ask me to sort it out for you, decide for yourself if you're going to do something about it or not.

Taken care of almost as if he were just another tree standing in the way of more money.

by Yvil | 26th Nov 22, 4:30pm

Future attacked me personally by insinuating that I belong in a mental asylum, so I took care of him. If you feel offended by TTP or anyone else's comments, don't ask me to sort it out for you, decide for yourself if you're going to do something about it or not.

I didn't realise this was just about your personal feelings - you made the appearance that you wanted to improve the quality of the comments across the forum as a whole. If this were the case, you would be consistent in what is ok and and what is not - regardless of who it is being directed towards.

And I don't think you 'took care of him' - you whinged to the teacher that you were getting bullied and the teacher kicked the bully out of school.

I wonder if I can dig up that post where Pa1nter said I have a husband and all the insinuations of that.

But nobody likes a nark do they.

Hypocrisy is one of the most detestable human qualities.

Fully agreed HM, well said!

Anyway, I'm done with these childish exchanges. Future abused me, so I got him banned. If you IO or Brock have complaints about other posters being rude to you, don't get me involved, deal with it yourselves!

I'm out of this conversation.

I have asked Interest.co.nz to review the posts that HW2 has made about me today....

Only because you're motivated by envy and nastiness. Anyway if you keep making rude shoutey remarks and trolling me then why complain and play the victim. Gee whizz

8th time? Lolz

Fortunately my skin isn't as thin as a paper scroll so there's no need for that!

Thanks yvil I missed that post too.

Haha I like this list. We have had all of these lies told to us at some point. The “We work as a team” is my favourite- they compete so much for commission that they actively discourage other agents through the house. We have had experience with information turning up very late to us in a tende/multibid situation when we are not working through the listing agent. We have even had them say bad things about their “team mates” to us.

Funny thing is now we ( all of us buyers and prospective buyers) have had so much experience with agents through many, many failed multibids that we are getting quite experienced at this game and are on to these agents and their tricks.

Only Agents with realistic appraisal to vendor can be successful as many agents to get a listing do high appraisal by cherry picking one sale in the area that may have gone for a decent price.

Many are still obsessed with 1.2 million or 1.1 million where actually the price that it will fetched is million if lucky or below.

Have you got permission to spruick your real estate marketing company here Fred?

A lot of truth in this list. Does this site also provide constructive advice about how to select a good agent or otherwise sell your house?

The best way to sell a house is to do it yourself and avoid real estate agents/agencies.

They’re parasites. 🦠

They love to label themselves “professionals” but they’re mere salespeople with pumped-up egos - who lack the wherewithal to hold down a proper career.

Avoid them like the plague.

TTP

Translated version (for transparency purposes) - "Agents, avoid them like the plague. If you deal with Property Brokers, we'll have your back"

Translated version - RE or Property Brokers agents produce nothing for society.

In Sydney they are still getting 60% clearance Auckland been 20s 30s for months

I thought I read Sydney prices are very bad at present?

Yeah even within Aussie auction clearance rates vary wildly from state to state, and are irrespective of what pricing is doing.

Even in a down market clearance rates in Sydney and Melbourne are higher than NZs rates in a hot market.

Its funny that in other markets like London auctions are not popular at all

They do have gazumping though, which is even weirder again.

I would attend auctions for amusement during the hottest times and never witnessed anything like the success rates reported in Sydney.

Gazundering is going to be all the rage for the next few years.

What a wonderful sounding word....... for FHB

Yes but the news from last weeks auctions is the prices. Watchitfall posted his/her summary of Auckland sales prices - for under 2.5 million dollar houses. 60% of those sales were below 2021 CV (8% below on average), and a good number sold 20% below the 2021 CV.

CVs rose 35% on average ( national average) between 2017 and 2021. So it only takes a 26% drop from 2021 CVs to get us back to the 2017 level. Looks like we are heading there fast.

The Spencer Terrace example was a big shock last week, selling below both the 2017 CV and the price paid for it in 2017.

https://homes.co.nz/address/auckland/hauraki/1-2-spencer-terrace/EKEAX/…

People are starting to pick up bargains... opportunities are out there for sure.

Only if sellers and agents are past the delusional phase.

There is no bargain in a falling market.

What looks like a bargain today will look overpriced tomorrow.

Ignore the teachings of The Prophet at your peril.

Is it difficult to chew with your forked tongue

Yvil. Is the comment above constructive or on topic?

Someone might be flying banned real soon.

✈️🚫

Priceless :)

The "comment above comment" refers to your biased and slanted remarks whilst you dont even follow your own advice. Thats priceless

You'll need to explain that one, champ.

Does anyone have any colour on the Spencer Terrace one?

That property only had a couple of weeks of marketing before the auction so it looked like a quick sale was wanted and achieved. Could be a bit of an outlier at this stage. Only time will tell if it is a bargain or not.

I still think it was a foreign asian owner exiting NZ Market....

Manukau region has gone for a toss.

Still the prices though have fallen has not fallen as they should have by now, compare to the rise as still lot of money in the system and last of few FHB who are still having FOMO are helping by getting one sale at a decent price out of 10 sold, giving some number for real estate agent to hold.

Also effect of recent Rbnz announcement still to be played out.

Carinaz is it FOMO because... "first home buyers feeling under pressure to snag a property before their mortgage pre-approvals expire and the amount of money they can borrow potentially diminishes."

https://www.oneroof.co.nz/news/42712?page=alt

This FOMO is due to social pressure.

FOMO is a FOMO, whatever the reason may be, as it is this emotion that has prevented complete whitewash but for how long.

This FOMO is due to social pressure.

Agree. I feel now more than ever there is a lot of pressure, perceived or otherwise, on people to prove that they are successful or doing well. I think many, many people jumped into the property market to buy an investment a few years back simply because "everyone is doing it" and they didn't want to miss out.

FHB's now is slightly different and I can sympathise to some degree, but no matter what your personal feelings are about owning a home, now more than ever you need to go in with a clear mind, common sense and a healthy dose of caution.

I actually think FOMO's never been lower right now, seems like a sentiment that it's a dumb time to buy with renting being cheaper or otherwise better to move overseas.

Good reason to put a house under the Xmas tree

Perhaps in 2023 or 2024. Might be coal this year for the naughty boys and girls who have been greedy.

By March rate resets be bitting, more motivated vendors, less able buyers.

Yes but I feel armed with information to give my local agents. For the past two years they have quoted me the outlier sales ….. “ well the house up the road sold for 1.8 million” ( remember I live in the provinces) when showing us a tiny, do up on a shabby bit of land by the main highway with a CV of $550,000.

I will delight in telling them auction sales are heading back to 2017 prices. But I don’t plan on seeing any agents too soon.

I know someone who bought similar 4 years ago, though not tiny tiny house and not shabby shabby land. It fronts a highway however. And she loves living there though. And now with almost consents for multi house subdivision, they will be rolling in loot before you can say "buying a home is catching a falling knife"

https://www.stuff.co.nz/business/130556747/from-bankruptcy-in-the-gfc-t… she gets it, its all about the yield

....highly likely. During the GFC, China was our "White Knight", not this time around. Its an "L" shape economic course I think.

She even admits that nothing is happening in that space. I had a neighbour who thought like that and he did not do well. Sold his property early thinking the market had peaked. Haha. He later wrote a book giving a spiel

What is the name of the book?

Can't recall, however it is not up your street. Believe me

Buy now for 1m you won't regret it. Within 20 years will be worth 2m while others are still paying increasing rents.

My sons bought last year, they are happy as. One is getting married in December, his future is coming together nicely.

Wait. Houses only double every twenty years now?

Aren't houses likely to double in 10 years if inflation is running at 8%?

I ran the numbers on this a few weeks back ZS.

Took a rental property with $30,000 income, increased that each year at 8% inflation.

If Mortgage rates stay at 3% (i.e. if somebody purchased last year) the property is worth $800,000.

If mortgaghe rates rising to 8% because we have 8% inflation, the property is only worth $400,000.

The impact of discounting those future cash flow (even if they are growing at 8%) using the higher discount rate needed to combat the inflation, means the asset falls in price significantly - in the vacinity of 40-50%.

Run a net present value spreadsheet yourself in excel and trying a 3% discount rate vs a 8% discount rate on those cash flows over 20-30 years and see what result you get. I got a 40-50% drop in nominal terms.

It is not good.

You cash flows at the end are great - but you capital value is poor.

So like a bond, if the interest rates increases, the face value of the asset falls.

Rising cost of capital is going to be a complete mindset/paradigm shift for people who have been involved in property from the 1980's to present.

Falling discount rates have had such an impact on bond and property prices because of the manner of those investments.

If we are now in a repeat of the 1930's to the 1970s (i.e. the reverse of the cycle that we've just experienced for 40 years), it could be very painful for people to move to a different way of viewing the world and asset pricing.

You're being a little too pessimistic as always. All sorts of things "could" happen of course. Here's how I imagine it will unfold: House prices will settle down, interest rates will vary over the years. The corrected price of the house will rise with inflation, possibly a little more, while still earning a rental income. Things rarely turn out according to the worst case scenario.

The above isn't the worse case scenario (to be clear).

You should open up a spreadsheet and run the NPV numbers there ZS with 8% inflation. As a property investor/landlord type, I assume this would have been part of being a prudent/professional investor (savvy isn't that what you call it?) so should be second nature.

By doing this, I can see why the bankers have been getting so nervous about their lending.

10 years 20 years 40 years ....it doesn't matter to me, as I am happy with level prices. The premise of owning an asset while others pay increasing rent still holds. For the record, I have never had a property lose value yet. Even so, I know how to buy low and add mega value, mega fast. Yeah yeah here comes the doomster poppy with some quip about Kim dotcom

The premise of owning a mortgage...

The premise of having a bank as your Landlord.

I said owning an asset, there is no need to twist everything to your own talking points. Isn't it funny how from my two posts you could only come up with some weak jibes.

Yes, pay off the mortgage over twenty or so years, own the asset out-right. While others are still paying rent even when retired, and crying about poverty .

They were constructive rebuttal. Not Jibes. Jibes are banned.

HW2, within just 2 consecutive comments, you say that you:

- own rentals and have done well out of them

- look forward to ever increasing rents

- feel satisfaction about tenants "crying poverty".

Does it make you feel good, and superior? Do you enjoy that feeling of power? Of being able to continually squeeze rents higher and higher, while your tenants are "crying poverty"?

You may have had a rough childhood, I don't know. You may have a congenital lack of empathy, I don't know. But quite frankly you sound like a horrible cold blooded son of a b. It sounds like you have enough money for therapy, I suggest that you consider it.

BS. Perhaps your misconstruing has something to do with your constantly negative views. If someone has to own the rentals it may as well be me. For your info I dont buy FHB or owner occupier property. Investment properties only from two homes to twenty in one parcel

A house is a liability, not an asset.

Better to have a business? Not if it is going down the plug hole

Ahhhh the old safe as houses brigade.

"Better to have a business? Not if it is going down the plug hole"

Like all the professional business people whinging on the Property Investor facebook pages that they can't claim interest deductions on their rental properties despite being in a valid property investment business.

Didn't work out that way for me but each to their own I guess. Buying a house was the single best purchase I ever made.

“A house is a liability, not an asset.”

It is if it is bringing in cash flow after all the expenses.

Completely agree

The deflationary spiral will prove you wrong.

Well spotted the changing tune, its 40 years further down the page....

THIS IS NO WHERE NEAR THE BOTTOM HW2 thats both bad and foolish advice, people who bought in November ARE REGRETTING IT do you want some introductions ???? getting your kids in at the top, yeah way smart.

Why not be smart, play the cycle, get your kids into 2 houses at 500k each..

I think your past strategy may be tainted by luck. No need to sell FOMO in the fastest falling market ever seen in Auckland.

Your financial advice is as bad as the guy on the radio... "the only time better then today to buy... was yesterday", yeah right.

Don't worry mate, all that bold-type is a bit OTT

Did those "introductions" get a long term fixed rate mortgage. No need to answer, its rhetorical

Yes some luck I agree as the property market ascended. However someone doesn't go from a 1 bedroom flat in Hamilton (poppys assessment) to multi-multi millions without even the teeniest amount of know-how.

Apparently you own a LSB in Diary Flat. Can you please do me a favour and learn how to spell Dairy 🤣 Obviously newly minted to the area and rural life

Sorry to correct a wide assed guess. I was born on a 700 acre beef and cattle station in Hawkes Bay.

You make some fast and interesting conclusions about people HW2. You seem very level headed.

I have noticed many spruikers, sorry commentators on this site make massive assumptions about people on this site, and time and time again, they are proven wrong.

I've been told on here for years that I'm a doom gloom merchant and have no credibility by many spruikers - because I warned that at some point we could see significant falls in house prices in real terms and that this should be considered before buying a first home....because the ramifications of getting your timing wrong could be very bad for your financial well-being in the decades ahead.

Despite living through the GFC in the US and seeing the parallels in the FOMO and greed in our market that was present in the US before their property bubble burst, I was told I had no credibility because I had no track record of making millions of dollars in the NZ property market - or because I was a poor renter!

It was simply that because I warned that at some point house prices could fall, it was of most importance to property spruikers that my views be silenced by them (and their vested interests). If my views were right and scared away potential buyers, then this would be bad for their capital gains. It never ceases to amaze me how quickly men (and woman, but mostly men) lose morals and ethics when their is money to be made without consideration to the long term and that method of making money will impact the social and financial stability of the nation as a whole.

Similar things happened in the US and when those same people go silent, you know what I've been warning about is happening. As it stands, out of those who have disagreed with me over the past 5 years or so, only HW2 remains. Take from that what you wish. Perhaps he knows something all of the other property spruikers do not.

Lets just add that you've been selling fear about the resi property market since 2013 at least. Which of course is a huge chunk of someone's life. I have never heard you mention commercial or rural property and it's like those ones dont exist lol

by HW2 | 26th Nov 22, 7:01pm 1669442464

Lets just add that you've been selling fear about the resi property market since 2013 at least. Which of course is a huge chunk of someone's life. I have never heard you mention commercial or rural property and it's like those ones dont exist lol

Firstly I haven't been a member of this site for that long - so not sure how I've been selling fear about the market since then.

Sure I've said that I thought a damaging and unsustainble property bubble started forming from 2013 which there is no turning back from. But that differs to what you say above.

I've been the owner and a beneficiary of commercial and rural property - including running a rural property. Commercial property investments include NZ and overseas.

You see it is possible to have experience with the property market and still warn people that at some point, there could be significant (life changing) falls that risk the social and financial stability of the country as a whole.

Property shouldn't be a ponzi scheme where if you are in on it, you become a sales person for it.

For example, I own some shares I acknowledge there is a risk they could lose 50% of their value in the next few years given the market conditions we have. The property I have exposure to could also do the same.

...HW2. You seem very level headed.

Is that meant to be sarcasm ITGuy. I will take it as it reads, as a compliment.

Thank you

Forgive my conclusion if incorrect. But townies often move to an LSB although not usually 15h. You did say that you moved from Devonport. Good on you

It’s pretty low by even your standards to insult someone on the basis of a typo. Pretty pathetic.

Why not be smart, play the cycle, get your kids into 2 houses at 500k each..

A little judgey, as how do you know they did not do that last year by getting a little help from their fathers insight and nous. They are happy with the one house each. If you want to encourage your kids to wait, that's up to you.

Winners will be those who are able to ride out this cycle, unfortunately there will some who ain’t able to.

Bigger winners will be those who buy at the bottom of this cycle. Its a long way off there is no need to Be quick.

Auction sales drop 12.5% in a week while offerings were up 3.33%.

Soon we won't see the sun past the stockpile of houses for sale.

If it's not for capital gains and trying to get rich quickly, there is no real benefit of real estate investing as it doesn't add much value as an individual investment.

We need to grow the country as a whole, need good brains to invent something new which will benefit all and add value.

Just adding more and more low quality house build and selling it for Millon a piece is not good growth in any sense.

Hence now we see such a situation is housing market in NZ. Please enhance my knowledge and tell me if it makes sense to buy a 4 Bed town house on 250qm section for 800k+ in a tier 2 city in NZ?

As I have commented here before, I am all for home ownership. In particular owner occupier, as long as it a positive life changing experience. Outside of this, renters too can achieve financial and emotional security, happiness and freedom with a healthy and growing bank balance. Renters can save too - right? Right now, those who bought in the last 2-3 years will understandably be feeling anxious that there timing was wrong and all they did was line the pockets of the vested, which they certainly did. I suggest that FHB's watch this correction play out in its entirety. Lets see how much house that growing bank balance will buy and therefore save in interest (dead money). That's where the true satisfaction goes to the next level. I think this is a pretty safe bet because once house prices stabilize, the likely introduction of DTI will prevent this debt driven froth from happening again. People will think twice about speculating on houses.

From experience, "debating" these points with any Spruiking "debt junky" is pointless. Some here view saving as the ultimate cardinal sin.

I'm a bit of an outlier on this. I have rented for the last 17 years, and have built a business up that pays me for not showing up. Renting has many advantages in my book.

Renting is better for people that don't know how to change a light bulb. If you are a can do it all handyman, then you are probably already in your own home.

I have previously owned a house, just doesnt work for me anymore. I'm pretty handy, have restored half a dozen cars over the years. Currently refitting a yacht.

At 198cms tall light bulbs aren't too much of a challenge.

That's a weird statement being a handyman is not a pre cursor to owning homes. I would say there are many millionaire business men, doctors, lawyers the list goes on who are not handyman. Making money is not exclusive to property investors.

Mid next year it will become obvious who was correct in forecasting a crash, part of the debate is to get some of these posts onto the record......

Then we will be able to look back and see the true folly on their side. I note there are not many left saying now is a great time to buy.

TTP has gone quiet once his spring bounce failed to appear, even Yvil is no longer a full on spruiker, just HW2 left?

Of course not everyones kids are like HW2 whose daddy could afford to help them into homes, and thats the issue for the market........ Most FHBers are going to wait till there is blood inn the streets.

I am not alone in assisting financially, they also saved and got mortgages. Its been 18 months now, and I have seen my kids grow as adults so I think the decision has proved to be the right one. The oldest one shared photos with his partner and both are truly happy, the happiest I have seen them. At least let me enjoy the warm glow instead of berating me 🤔👏 If I want I can write off some debt and subsidise the house but there is no need for that.

Cheers

HW2, and ‘Flying High’ occasionally appears for a spruik or two. Nifty1 is very hard to work out, has some distinct Spruiker qualities but sometimes seems quite the opposite.

Yvil stopped being a Spruiker some time late last year. Some of us have long memories though of how nasty he was to those of us who had bearish views on the property market and questioned the dominant rhetoric about property being a sure bet.

TTP is welcomed for his comedy value, something the other spruikers offer nothing of.

HouseMouse , it;s so obvious, there are so many different types of post on this site, from Interest rates, to terms of trade, to Chinese paid for pieces.... Some userIDs ONLY POST on the real estate posts, they seem to have no opinion on anything worth sharing apart from the property spruiking.....

Its all about data and the analysis of it....

I read and comment on wider issues, and I see other posters comments, and I form a greater respect for them as I often see logic in their posts. I don't need to agree with all posts to respect views on some posts, I am not partisan. But you can see straight through the spruikers. I would love to be able to download all posts and provide an analysis of the time based clustering of posts by userid... data never lies.

Great post Retired-Poppy

Last year definitely was not the most sensible time for FHBers to buy. They and their parents obviously did not understand the RBNZ had us on emergency interest rates and that at some stage the RB had to put them up as housing inflation was out of control. Greed gets the better of us generally. Young people listen to their parents saying they cannot lose with property. Personally I would have acknowledged the fact that interest rates had to go back up as we cannot live with high inflation forever. I would have paid my kids rent if need be as it will be peanuts compared with the tens of thousands if not more equity that people are going to lose because they bought last year or early this year. If you had waited to buy next year or even 2024 you will probably have borrow at least a $100k less than you would have last year. In Wellington it could be $200k currently. Paying rent and waiting is paying peanuts compared with interest on $100k to$200k . And you have to pay back the principal. Why don’t people use their brains, be patient and eventually borrow a lot less. If you think the housing market is tough now you have not seen anything yet. When interest rates are 7 to 8 per cent or more it will be very tough. And everything else including food is costing us more. Agents retailers and car dealers are telling me it is tough in terms of selling. The RB says it will put us into a recession if we don’t stop spending. That is a scary thought. High interest rates, more unemployment, businesses failing and more asserts such as houses on the market. If you can save some cash! If last year your child was looking at buying an $800k home and you told them there were risks in buying now as the market was bonkers and it was and if you waited for a year or so and you could buy that same hose for say $650k what would any sensible child do? Paying off $150k let alone paying interest on it over time takes some doing.

Spend it before the reserve bank inflates it away.

I am doing that Brock. Helping our kids before we kick the bucket is important to my wife and myself. I am watching the prices of luxury EVs currently as I would like one. Like houses they are tanking price wise. I am going to be patient.

I could possibly give an answer to most of what you say.

Media, including interest.co and others tend to express house prices by affordability rather than outright price. Hence the almost outrage that the affordability has dropped with the rise in interest rates but the total lack of acknowledgement for having to pay $200k less. My guess is this is because everyone thinks that buying on credit is totally normal which the banks just love but entirely distorts the price of a house. Infact I'd suggest second hand houses are 80% over priced. It make no sense that 50year old house can have a similar price to new but it is cause banks willingly lend to make it so.

It's the land price that is most important.

The 'affordability calculation' Interest.co.nz use is poor (sorry interest.co.nz team) as it assumes that the FHB's deposit erodes at the same rate as the housing market.

Ie. if you had a 20% deposit in Nov 2021, the affordability calculation assumes that you still have a 20% deposit in Nov 2022, even if houses have fallen 20%. For example if you had $100,000 in 2021 as a 20% deposit on a $500,000 house, but you waited as you though prices would fall....and in the last year you saved another $20,000 and the house you want to buy is down 20% and is now worth $400,000, you now have a $120,000 deposit to buy a $400,000 house. That is no longer a 20% deposit, but a 30% deposit. Instead of taking on $400,000 in debt, the FHB is now taking on $280,000.....that is a $120,000 less debt!

The affordability calculation interest.co.nz use is only meaningful in a rising market - they haven't figured this out yet or decided it is too complex to workout how affordability is improving for FHB's who chose to be rational and wait and not buy in a bear housing market. The current model assumes every FHB buys the very moment they save a 20% deposit - but in a falling market that simply isn't the case. I know a number who are waiting on the sidelines saving and who are in a far stronger position now than they were a year ago - i.e. affordability is improving dramatically.

'Stronger position' .. higher incomes, smaller mortgage

Weaker position: unable to buy the same house they could have bought a year ago. Banks more conservative and lend far less

But, I hear you say. Less available credit means the market will nosedive. No, its not necessarily causative as there are other ways to get finance by boosting ones income or borrowing from relatives or shared equity.

My own rellies have promised to help me when I have a better deposit. Being single, its definitely more difficult. Lower prices help but I am just hoping they dont pick up anytime soon

I think some here who always push for BUY NOW may well be involved in the industry and are a bit short of income, if this plays out like most international crashes have from these types of unrealistic DTI, agents are going to survive on very thin pickings for 3-to-5 years.

Perhaps some here are a bit scared of this prospect..... Adrian Orr is not your friend.

To me, you sound like an agent pushing the fear game. However even FHB are smarter than you.... put that in your Diary.

Are they doing that out their HW2?, are agents being realistic with their vendors..... selling the fear ? You can almost smell fear seeping off the web pages of Trademe listings as houses go from Auction/Deadline sale to Price by Negotiation..... to just not selling. Be Quick....

I am not a Real Estate agent HW2, and have never been one. I am an IT guy.

I have put a note in my Diary for June next year to see where the house market is vs now, for NZ and AKL average price....

Maybe those FHBers are smart? if they are, its going to be real bad for agents pay packets over the next 3 years, Be Quick.

Boy I wish you would spell correctly and use the right form of there/their. As well as 'Diary' Flat. Easy mistake for newbies? If you really are an IT guy then you would know the importance of accuracy.

Just recently, FHB have taken a record share of purchasing and borrowing. And I heard today the FHB are trying to use their lending approvals before they expire and have to pay higher interest

by HW2 - "And I heard today the FHB are trying to use their lending approvals before they expire and have to pay higher interest"

WTF?

If anything, a few are waking up to the fact that when their approvals expire they'll be told their borrowing limits are reduced based on a tighter serviceability test. They're only kidding themselves if they're buying now to avoid this. How on earth is this a strategy to avoid paying higher interest on a mortgage?

(edited)

How was your naptime poppy

by HW2 | 26th Nov 22, 3:25pm 1669429524

How was your naptime poppy

Yvil - for the sakes of consistency and to avoid hypocrisy, can you please report this comment or ask HW to stop posting irrelevant comments that add no value?

Hardly.

Would it be any different if I said poppy you have no idea what's happening.

To me you are on thin ice with the rumours and untruths you openly repeat. Making untrue claims about what me and others believe.

by HW2 | 26th Nov 22, 4:12pm 1669432364

Hardly.

Would it be any different if I said poppy you have no idea what's happening.

To me you are on thin ice with the rumours and untruths you openly repeat. Making untrue claims about what me and others believe.

That is good - we are in disagreement and that is what this forum is for. To be in disagreement but to provide arguments with reasoning. Not just to say "poppy are you having a nap".

Please list all of the untruths I'm openly repeating and the untrue claims about what you and others believe and I'll respond to those.

People should only be banned for both not being funny and being repetitive. That was Future's mistake. I'm sure he got a couple of warnings.

People should be banned for using this site as a portal for marketing of property too. Although I have noticed your posts have become more balanced as of late :) Keep up the good work and keep revealing the true state of the market.

I did take on board your comments and I too see little point in dignifying shite comments with back and forth responses.

Although I have noticed your posts have become more balanced as of late

As are yours. Although as per usual you are "boaring" and "trotting" out the same old attacks on Zach 🐖🐗

Where is the evidence that I was doing marketing? I had on topic comments deleted that had links to B&T sold properties that were examples of significant losses on an article about B&T auctions. I honestly thought I would be paraded on the shoulders of the Doom Goblin community as a hero. I'm sure you can appreciate my disappointment at what transpired!

I've always tried to present reality whether it be a hot or cold market.

Second this. This guy just seems to want to pick fights with everyone and insult them without bringing any relevant arguments or data to the party. It's almost as tiring as Future.

Wow Four times in a day, a personal attach vs rebut the argument.

First you say I must be new to the Rural community.

Then you question if I work in IT.

Thirdly suggesting I am an agent selling fear.

Number four you seem to DiVrT the argument about house prices collapsing off topic to my use of bold etc..... very sad a bit DEsPErATe really.

Are you questioning me personally to try and distract from my view that house prices are falling? questioning my spelling, but why not engage with my argument? That prices are going to fall considerably.

You seem to be very different to most posters here,

1. Hardly anyone now believes that house prices will be double what they are now, in ten years time?

2. Hardly anyone here has enough money to help their kids into homes at the very top? or admits to this...

3. Hardly anyone posts so shortly after Yvil does agreeing with him.

A statistical analysis of the posting and timelines of various posters posts, may well suggest a linkage.

Anyways it does not matter, the only thing that matters is the cost of credit and the effective risk free return vs yield.

All your past wits and nous is not going to save the markets.

The reason why you are the last spruiker left is so well summed up in the quote below, which can be aplied to any Past ponzi.....

Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one. Charles Mackay

personal attach

rebut

Definitely not good with computers. Yes different to others, but are you having a "personal attach"

Have you heard of the description, a fair weather friend. If you are in for the long haul with your 15 hectares you better learn to be there in fair weather and foul

There you go again HW2 ... very sad to watch.

5th attack today is about my spelling ability.....

so sad....

I think you should engage about the topic, comments that add no value like this may get you banned.

An accountant knows the cost of everything and the value of nothing

Banks have little regard to "Value" they want income, expenses, cash flow, yields etc.

I am sure that todays prices will look cheap compared to 50-100 years, but banks do not care, they offer credit based on your ability to service the loan.

Under CCCFA they have to legally access your ability to service the loan, with the prospect that directors offering loans will be personally liable if this is not done.

Indeed Accountants know the cost of Property.

Assess

Cant help yourself........ once again rather than debate the topic..... keep digging.

See below. Anyway you pretty much started the personal argy bargy today as you have a problem with my perspective and opinion. Identifying and isolating me. It's your own fault if you dont like my responses back to you

6th attack....

Gee wizz 🐖🐗

7th?

by HW2 | 26th Nov 22, 4:17pm

personal attach

rebut

Definitely not good with computers. Yes different to others, but are you having a "personal attach"

Yvil - this comment also adds nothing to the argument about housing. Could you please also report this for the sakes of consistently please.

Seems rather churlish now. Time to get back to the topic dont you think.

Great to see you want to return to having good, fair and reasoned, dialogue now after a few indiscretions above that have been called out.

My work here is done.

where do i report comments please ? don't worry found it and done. probably made a spelling mistake as well.....

Can people try and be a bit more careful with spelling though? People don't appreciate how disturbing it is for readers who are on the spectrum. Loose instead of lose, boarder instead of border, your instead of you're, their instead of there, of instead of have, breeches instead of breaches, then instead of than, west instead of West...it really makes me spin out! We should endeavour to keep standards high.

I think it's me being on the spectrum.

In a verbal debate you would not be aware of my Dyslexia/Spelling issues, but on here obvious.

I ask that people do not shoot the messenger re spelling. Try to stick to the message.

Today HW2 attached me 5 different times, never about the message, always about me or the way I used fonts, spelled things.

I have asked for it to be reviewed.

It is blinking hard to understand you. I am doing you a favour

You have not asked for clarification once today... keep digging.

Double tick Zach

Oh come on man. I am sure many people whip off comments pretty quickly. These are comments not edited articles!

Its only disturbing if you are pedantic, personally spelling is largely irrelevant these days if you can work out what the poster is trying to say then just move on. What's next my commas are not supposed to be there or I missed one ? We are not Tom Clancy trying to write a book here there are mistakes all over the place its a waste of time pointing them all out because nobody else cares unless your top subject was English in which case you probably failed Physics. IT Guy has used the word attached instead of attacked above, Woo Hoo ban the Guy, so he is not a great speller but bet he can probably run rings around most people on Computers.

Yip I post the occasional comment from my phone and there's a high chance I make grammer/spelling mistakes from there.

Its okay to make spelling mistakes, I make heaps on my phone. I often suffer from "fat finger syndrome"

I vehemently disagree that it's "okay to make spelling mistakes". The odd mistake is understandable but consistently spelling lose as loose or border as boarder after having the error pointed out means the writer need not be taken seriously. As HW2 pointed out we are just trying to help improve people's comments. Keep in mind that comments are read by a lot of people. We wouldn't tolerate these mistakes in the article itself.

Saad.

Since becoming a hypercarnivore I have become so hyperaware that I can see the matrix. Disturbances are more apparent. I think it's the ketones.

"As HW2 pointed out we are just trying to help improve people's comments"

There are not many comments that leave me void of a sanitized response....

Again, it is okay to make mistakes. The edit button is there to correct. Its a bit of a hoot that HW2 once told me off for correcting my mistakes - lol!

I think what really happened was that I robbed him of the victory of calling me out for making them!

Zachary, you'll have noticed that on multiple occasions, twice on this thread alone in fact, the images "🐖🐗" posted.

in an apparent effort to belittle and appear funny at the same time, does it concern you when someone re-posts the same image day after day? Some readers (English Teachers in particular) might interpret the poster as being more of a try hard than anything substantial. Now that you've made it clear how you take issue with the same repeated comments, does this apply to images too?

I'm not a big fan of the images. We should minimise tit for tat exchanges, cheerfully consider helpful advice, rarely take things personally and keep comments on topic, succinct and intelligible.

A constructive and helpful response - thanks :)

Could be the scurvy.

By critiquing every comment, the poor lads given himself a migraine.

Or jump on Interest.co on a Friday afternoon at 4:30 when the brain is fried.

Hang on Zac, "west instead of West"? The "w" would only be capitalised if the "west" was part of a proper noun, such as "West Auckland. But not, for example, "I am driving west today."

Standards please.

Yes, I should have been more precise. My intention was to highlight that people often wrote "the west" instead of "the West" when referring to the Occident. Thankyou for clarifying that.

https://www.oneroof.co.nz/news/we-need-to-buy-first-home-buyers-rush-to…

Real estate lobbyist trying to stir FOMO

Better be quick before 2 year fix gets to approx 7.5% (based on 5.5% OCR) ........ and stays there for 1.5 years as per RBNZ statement.

whats 800k at 7.5% plus principal at 30 years....

Per ANZ online calc

Your minimum repayments: Monthly

$5,594

Your minimum repayments: Weekly

$1,290

Thats $67,080 per year in mortgage before council rates (another 3.3k?) wow 70k PA to own your first home.. 350k before your fixed term even ends.....

Better to wait......

Perhaps an even smarter strategy for those who think they are smart, is to buy 6month out of the money Puts on Aussie bank shares....

EDITED - to fix spelling mistakes........................

BofA Securities investment strategist Michael Hartnett released his top trade ideas for 2023, which includes shorting select banks like Canadian banks.

Hartnett placed as his tenth top idea shorting Canadian banks, as well as similar institutions in Australia, New Zealand, and Sweden.

It's going to be very hard for ANYONE to get credit in NZ if this trades starts to pay off big time.

Zollner says it is clear the Reserve Bank is not trying to engineer a recession on the scale of that seen during the GFC or the early 1990s.

That doesn’t rule out the country getting one, she says.

The Reserve Bank forecasts house prices will fall another 10%, which would mean they would drop by 20% from their 2020 peak.

But Zollner describes the housing market as the country’s Achilles’ heel and says there is “absolutely a risk that in trying to singe the edges of the housing market the Reserve Bank could accidently set it on fire”.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.