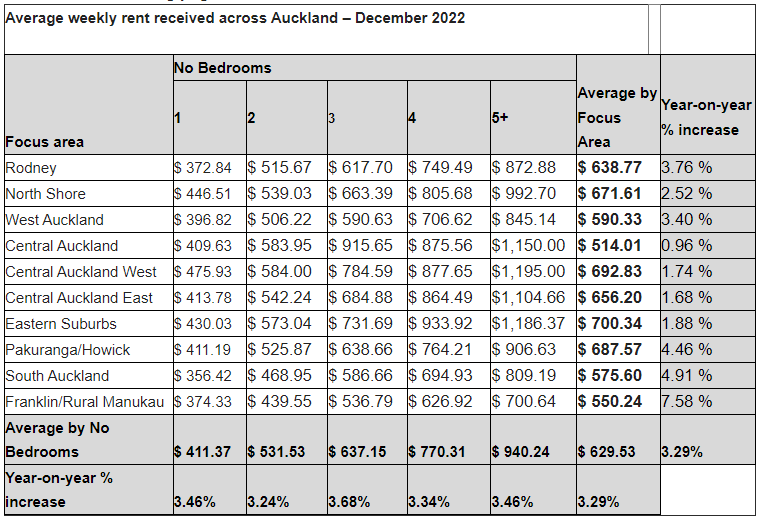

The average rent for residential properties in Auckland managed by the region's largest real estate agency, increased by just over $20 a week last year.

Barfoot & Thompson manages more than 17,000 Auckland residential rental properties on behalf of landlords and their average rent in the fourth quarter of last year was $629.53.

That was up by 3.29% ($20.04) compared to the same period of last year.

The biggest increase in rents was for three bedroom dwellings, for which the average rent was $637.15, up 3.68% for the year.

However there were substantial variations in the amount of rent increases by district.

Landlords in Auckland's central suburbs, which includes desirable areas such as Ponsonby and Grey Lynn as well as the CBD, would have had little to cheer about with annual rent increases of just 0.96%, while rents in Franklin and rural Manukau on Auckland's southern boundary increased by 7.58% (see the table below for the full rent breakdown by district and number of bedrooms).

"After being at a standstill in early 2020, the average weekly rent has made incremental steps over the past couple of years to settle into a pattern of steady but measured growth," Barfoot & Thompson director Kiri Barfoot said.

"This is despite increasing operational costs, rising interest rates and peak inflation, indicating many property owners are balancing these pressures against considerations around tenant affordability and their desire to maintain longer-term tenancies."

The comment stream on this article is now closed.

Average Rents for Properties Managed by Barfoot & Thompson

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

125 Comments

Rents have been tracking pretty much around long-term average in nominal terms but have plunged into negative territory in real terms.

Yet both parties on the right are insisting on reinstating tax breaks for landlords, saying their removal is pushing up rents. You don't need an advanced degree in economics in order to manipulate data to suit your ideological narrative.

Your a pretty weak Advisor if you call non deductibility of interest a tax break. It is standard accounting cost of business practice. All it did is punish working mum and dad investors with 1 or 2 rentals. Whist Large Property Investors and Professional Commercial and Residential housing stock owners, can simply repurpose debt (borrow against commercial and pay off residential debt) or lease housing stock to Govt backed Social Housing Providers and be 100% able to deduct all interest. It is the biggest own goal of helping the rich and punishing the poorer middle to lower class that I have ever seen from a Labour Govt whom the current crop pride themselves on being strong socialist left.

mum and dad investors with 1 or 2 rentals.

punishing the poorer middle to lower class

Yeah pull the other one mate

Yeah lets punish and hammer anyone who wants to get ahead. Tax should be flat line 20% up to 100k and then stop. So EVERYONE pays their fair share of say 20k, not only do salary earners on higher income have to pay more tax because they earn more, they have to pay it at a higher rate. What a completely unfair system. Or set a a nominal tax per citizen tax of 20k total to live here. If you earn 30k, you only get to keep10k, that is 100% fair.

Why should the 15% of high income earners pay 85% of the tax for the rest of the people in NZ, pretty corrupt system isnt it.

Because the rest do the actual work rather than pretend stuff, you know essential workers.

I've always said I'd rather be in a position to whinge and moan about how much tax I have to pay, than be a position I rely on someone else paying tax to provide my necessities of life. And I pay a lot of tax.

A motherhood statement in the wild. Brilliant.

Bluekiwi Property Consulting ....with a name like that, you were obviously on the now "defunct" property gravy train.

You would of been one of those that was squawking "borrow to the max" ... "property only goes up" ...."doubles every 10 years" ...and the classic "low interest rates are here to stay" !

Well times have changed buddy and your bleating on about a "fair tax system" , when landlords have their hand firmly in the taxpayers pocket, with the accommodation supplement, is just XXX ! ..... Why should any business at all, have to be subsidised by the taxpayer, as the amount needed to run that business, under normal market forces is not enough.

If your tenants can't afford the rent on that sh*tty, damp box in Manurewa (yes, I have seen them) they can't afford to live there....full stop.

True market forces should be applied to residential property, as this would of kept the price of the property down, while the rents then wouldn't have to have been "topped up" by the taxpayer.

You always rave on your doing "good for the community" and supplying someone with a house, when really if there was no money in to for you, you wouldn't of gone near it with a barge pole.

While the government (up until the no claiming on interest payments) has not helped in any way, to slow down the increase in property prices - while NZ is the only country without a capital gains tax - why would that be ? I know, can't upset the voters - ridiculous, as who/what is going to pay for all the added and needed infrastructure etc

Then you have the banks and the "ticket clippers" who have been creaming it all the way - up to now at least.

Anyway the tide has now turned and hopefully house prices and rents will return to match average kiwi incomes, while those days of "capital gains making more per week than someone's salary" have now gone.....in fact it has turned 180 degrees and your capital gains are now becoming capital losses.

I think the lesson you property investors have to learn is that "nothing stays the same forever" - including interest rates and what can go up quickly, can come down just as fast.

I just feel for some of those FHB's competing against property investors, who had to take on more debt than was necessary, just to get themselves into one (1) home.

Do you actually know anyone paying 39% tax who needs or wants the tax cut?

Do you think the wealthy need a break more than the poor?

I know dozens of people paying a bunch at top tax dollar, the only ones who want a tax cut are the outwardly selfish.

I know of a couple of people in the $180k+ bracket. They have little issue with it for a couple of reasons:

- They're grateful to have a skillset and qualifications that demand such a pay,

- If they went to Australia, the rate would be 45%.

Property remains the best bet for Mum and Dad investors. 🤠

TTP

I have to disagree with your turn of phrase TTP... there is little or no gambling involved with well managed rentals. 🐎

TTP ....your little emoticon at the end says it all to me ....."cowboy" , as you should be saying "Property remains the best bet for my cashflow and business" while I am one of the "ticket clippers" , and have been now for many years.

That's why I don't take took much notice of your one line "factual" statements, as I said in my post, things do change and nothing stays the same forever.

In saying that, MOST of the time property is the "best bet for Mum and Dad investors" - but not all the time ie right now.

Have a great weekend there in Palmy TTP

Mum and Dad investors… I love these sayings as it makes the government seem evil and the investors as poor folk . Buying property comes with risk!!! It goes up but can go down!!! These people have had best case scenario for decades now… it’s time to sink or swim

I love these sayings as it makes the government seem evil and the investors as poor folk . Buying property comes with risk!!! It goes up but can go down!!! These people have had best case scenario for decades now… it’s time to sink or swim

Yes, but let's also rememeber that the govt is not some agnostic bystander. The NZ govt-central bank-commercial bank cartel has laid out all the incentives and nudges for the ma and pa family unit to play landlord in the pursuit to "secure their future." So while I agree with your sentiment that people need to accept risk, the cartel also needs to understand that their money making model is not as antifragile as they would like to believe it is.

Can we make all Mum and Dads tax free regardless of whether they are investors? Or are investors special?

Can we make all Mum and Dads tax free regardless of whether they are investors? Or are investors special?

I don't necessarily have a problem with investments being tax free. The first natural reaction to my comment should be why should one asset class receive tax exemption over another. The answer will be something along the lines of 'well owning rental properties is a business'. And that's fair enough. But defining what a business is can be somewhat grey as it relates to investments.

Also why "Mum & Dad" investors as most couples I know have no kids ...either by choice or market forces left it too late.

It is a very valid comment to my mind. Decision to do that needs to be reversed but I'm proposing to do so in concert with regulation of the rental market. Wrote an article on it which should be published here over the weekend.

It is definitely a tax break because a "Mum and Dad" investor can make crap loads of money from property while paying zero tax. Its even worse when it is an existing property that goes from being a tax paying "business" to a loss making "business" just because it was sold to someone else with a mortgage.

Saying its fine because it is "standard accounting best practise" is just like saying its fine that Apple pays no tax in NZ because it is "standard accounting best practise". Obviously "standard accounting best practise" is not fit for purpose.

I am a "working dad", I have debt, do you mind if I offset it against my PAYE?

Blue Kiwi is correct, it's an inconsistent and dumbrule to disallow deductibility. Arbitrarily changing basic income/expense accounting principles to compensate for the Govt's own incompetence. Restore interest deductibility but introduce stamp duty and capital gains tax on investment properties.

Yes, agree it is inconsistent. But my solution is to regulate the market as opposed to introduce new taxes. New taxes do nothing for the renters who can't afford to rent in this market.

Should we make it consistent and remove it everywhere? Surely you agree it is odd that the debt used to buy a business is considered a business expense, when really it is an expense of the person who bought the business. Businesses can go from "highly profitable" to "not profitable" overnight just be being sold, isn't that weird?

No, I don't find that odd. I think it a sensible business/accounting practice/rule. Not sure I get the meaning of your last sentence/comment.

"Businesses can go from "highly profitable" to "not profitable" overnight just be being sold, isn't that weird?"

If I buy a business with no debt that makes a good profit and pays tax, I can load it up with the debt I used to buy it with (debt that enriches me not the business), and all of a sudden it is a loss making business that pays no tax. Same business, same revenue, same real expenses, but now it makes a massive loss.

Right, thanks, I now get it. But isn't there a three-year grace period for those type of accounting losses to be claimed?

If you buy a house? Pretty sure interest is counted as a loss on day one isn't it? I have never owned an investment property so not sure TBH.

My understanding being any start-up has three-years 'grace' - meaning an ability to run the company at a loss in the start-up phase - and after that it needs to show profitability/a ROI. But perhaps that was grace from the bank, not from the IRD? It's a long time ago I needed to understand business accounting rules :-)!

Kate, how is it possible or credible to regulate private rents without negative unintended consequences? I know some European countries do this but that is more high density purpose built and not houses.

That short answer is - I don't know - but I have put a proposal together that I believe avoids some of the unintended consequences of the overseas experience. Article on it to be published here over the weekend - I look forward to your thoughts!

For sure!

Was it supposed to be published last weekend. You know, before we found out that rents increased a measly 3 percent.

That was an average increase, HW. Averages mean nothing when you are the person paying OTT rent.

It always red flags something for me when the Govt. gives themselves break, but not others. For example, if you provide your rental to them for their clients, you can claim interest deduction, but if for the private market you can't.

Same with healthy home upgrades.

What is the logic, besides self-interest, an unfair competitive advantage, and social engineering, that they would do this?

I wouldn't say interest deduction for investors providing their rental as "giving them a break". The investor will still likely charge market rent AND not pay tax on the deductions AND likely have the Government pay for any repairs. Meanwhile the Government only charge 25% of the tenant's income, leaving a shortfall.

What break is the Government getting again? As for healthy homes, well there's not enough tradespeople to complete all upgrades. We know the private sector will drag their heels and leave until the last minute, so why not have the private sector go first?

If you want fair deductibility it should only apply to interest minus inflation. This should also apply to tax on savings. The inflation component of interest is not a cost as the asset backing it goes up with inflation.

I understand that point and it is a fair comment.

The tax system is full of inconsistent things and limitations, like Thin Cap or the Entertainment regime or god forbid, FBT. Then there's the biggest one of them all, the deductions available to contractors that employees doing the exact same jobs don't get to claim. Investors should just sit down, this argument sucks and is bad, and anyone with a basic undergraduate-level understanding of tax will be able to point out why.

The fact that aspiring FHBs could be outbid by investors who would have a third of their interest cost underwritten by the same First Home Buyers they outbid was never a question of taxation, it was a question of morals. And we failed that test, and loaded more and more debt onto FHBs who wanted to break through.

The solution is showing a basic degree of moral fortitude not demanding consistency from a tax system that clearly doesn't place much value on it anyway. The fact that something you think was so fundamental had to be broken to give others a look-in should give you some idea what a rort it was.

Relatives will sell their herd this year and cop capital gains tax just as we did 20 odd years ago. Totally inconsistent.

Moral dilemna's really have have no place in tax law, it should only be about consistency. Deductibility is being used to "fix" a broken sytem and it is not working. How do we know it isn't working? This very week Interest announced that our housing has never been less affordable.

There are far superior ways to better tax investment property.

Very good comment GV.

"Mum and Dad" investor can make crap loads of money from property

yep all risk free.... Wait a minute.

Tax deductions are everywhere and always a tax break, regardless of your line of business.

The real question is first, why we should, as a society, give this tax break to businesses; and secondly, to which businesses should they be given.

I’ll have a go at answering my own questions:

1) because lubricating the use of debt and opex of productive businesses contributes to wider society, particularly through increasing growth and therefore employment

2) businesses who operate on a ‘rent-seeking’ model do not qualify according to (1)

We should be looking seriously at all rent-seeking businesses and seeing whether they too should have this tax break removed. Not just so called mum and dad property investors

It's not a 'tax break' when the fundamental nexus between revenue and expenses say it's a legitimate deduction. That's the wrong way to look at it.

It just needs to be considered in the same vein as any other deduction which is limited or not allowed. Property investors should be well-used to this as plenty of things are limited or have different treatments when it comes to residential property; like depreciation, capital vs revenue, and so on. There's no over-riding principle that all tax rules need to be the same for every class of investment.

It's just another limitation. Except this one stops them from clawing back the financing cost for a 'business' that realistically has a single cash-generating asset, and then ceases to exist when that one asset is sold, for a convenient tax-free gain after years of posting a loss driven by deductible financing costs.

Nailed it again!

.

Fair comment but society does need accommodation for rent. Renting is good for its flexibility/mobility - and for many other reasons it is the most appropriate accommodation choice for many people. So, as a type of business goes - it is to my mind a necessary industry/business.

Hence, we need to find a way that the environment surrounding investment in residential real estate is fair and equitable for both buy-to-let investors and tenants.

Those unclaimed interests technically still deductible if an investment property sold before bright-line-test date when a capital gain tax is imposed. It will still be calculated as deductible.

And, whoever saying NZ doesn't have CGT is wrong, we do have CGT here.

I fully appreciate your point, however I stand by my point that, the removal of interest deductibility adds on rental expenses significantly to landlords. For a typical rental, it's equivalent of adding 1%~1.5% on top of their normal interest rates.

By the way, have you noticed the share market since new year? it started rally again.

Property Investment isn't a business. Even the IRD defines someone receiving rental income as an Individual. It's an investment, not a business. Even the IRS consider it an investment:

If you have a property that you rent to a tenant and you use the income to pay bills relating to that property, you may find that you, in fact, have an investment, not a business, according to the IRS.

https://rentprep.com/blog/property-maintenance/is-a-rental-property-con…

Rental properties should be left to professionals, not a bunch of debt stacking mugs and the various leeching consultancy firms that tag along looking to screw the next generation for retirement gains.

oh, great, if it's an investment, the top tax rate would be 28% on gains. not 30%, 33% or 39%.

I'd like that.

No, it's Individual Income. If property investment is a business as you say, then why are they not paying 28% like other businesses? Like I said....Individual, not Business.

All part of the plan, destroy the middle classes by targeted tax and other policies. The small players will be forced to sell out to the large players. Rents will rise as the big players have larger overheads and need to turn a good profit. Watch for banks becoming landlords as per plans already unveiled in the UK.

the interests is expense won't magically vanished, and must be paid, it can be paid by landlord, or by the renters, or someone else. You are saying there is no consequences by removing the interests deductability because rents only rose $20, I'd say you are rather naiive and over simplifying the math.

again, the expense must be paid, if you force landlords take the loss, they will leave, and renters will pay in other forms, either by rental shortage, or rent rise later on, or simply property market crash. Renter won't be magically able to purchase properties because landlords take losses.

Renter won't be magically able to purchase properties because landlords take losses.

You just said the market would crash, implying houses would be more affordable. Which is it? If houses get cheaper because investors aren't mopping them up with the rest of the country underwriting a portion of their finance costs, then we all win.

Houses don't cease to exist if an investor sells them. In reality this should have been addressed a long time ago and blackmail is not a good reason to keep tax rules that generate crappy and unjust outcome. If you want to finance a rental at a loss that you sell for a tax-free gain, then don't expect me other other taxpayers to help you cover the cost.

market crash doesn't mean people will buy or can buy, look back on 2008, did most people lose their homes became renters, or did most renters become home owners?

and the tax rule is currently meddling basic business rule, as interests are their expenses. Like it or not, rentals are business not charity. Unless the demands for rentals disappears, then the rental as business will stay.

another point you need to rethink carefully that, is the current house price a result of investors buying properties? hence should investors take the blame for 'high property prices'?

Without investors inject capital into the housing market, who and how do the general public fund their building / maintaining / exchanging properties?

Yes, I'd blame the sheer number of investors crowding out the market for high house prices. RBNZ C31, 2014 to 2017.

Total Lending per month

- FHB $656m

- Investor $1.6b

Total Number Borrowers per month

- FHB 1800

- Investor 4700

Imagine if we had a very limited supply of food and "mum and dad investors" were buying up 3/4 of it knowing that prices would only go up as people got more and more desperate.

the supermarkets is doing exactly what you are saying, taking a good cut of profits between farmers and consumers, which I didn't see too many people make fuss about.

Your comments also reminded me a different but of the same logic narrative, the "foreign buyer buying all properties and causing high house prices". Did you remember how that narrative worked? did house prices stopped increasing after they banned foreign buyers 2018?

Supermarkets may be uncompetitive due to the duopoly, but they aren't speculating.

Did foreign buyers ever make up ~75% of new sales? It was probably a scapegoat by the mum and dads.

are you implying 'ma and pa investors' bought 75% of all properties?

this is the figure of the past 3 years of all mortgage lending figure from RBNZ https://www.rbnz.govt.nz/statistics/series/lending-and-monetary/new-res… .

Total Lending [$Mil] | Nov 2020 | Nov 2021 | Nov 2022 |

All borrower types | 9,289 | 9,121 | 6,055 |

First home buyers | 1,605 | 1,739 | 1,357 |

Other owner-occupiers | 5,384 | 5,760 | 3,656 |

Investors | 2,226 | 1,527 | 957 |

Business purposes | 73 | 95 | 84 |

Looks like it according to those figures above. There are three main categories: FHBs, investors and existing owners. Existing owners are the biggest category but they normally sell when they buy so they don't really count.

Not all investors are ma and pa, personally I don't really care what their parenting status is.

a reminder that, about 25% - 30% percent of people rent in NZ, and the percentage of lending for investors are on par with that percentage. look at the figure of Nov, 2022, it's significantly lower than what the rental market shares.

investors represent renters in this chart. and the investor share dropped from 1/4 to 1/6, this is not a good sign to renters if you ask me as this will translate short supply of rentals down the track.

It's clear you don't understand statistics. Why does the figure of November 2022 for Investors need to be 30%? Just because 30% of people rent, it doesn't mean we need to have 30% of all sales/lending going to investors.

What happens if the number of FHB increases by 30%, resulting in the total number of tenants shrinking by let's say 10%? How would 30% of all forward lending going to investors make any sense????

obviously a rise share of FHB and dropping share of investors means some properties transfer from investors to FHB, as you said, it's normal and justified.

There will always be people renting, and not all renters in a place to buy, a drop in investors share means a drop of rental share, which is not good news to renters, especially the lower-end renters who are most vulnerable of all.

Another point that's to your favor is that, this lending chart doesn't seem include lending to new build (I might be wrong here), as some of those lending would fall into business lending. this means there might be more new builds to the house market and relieve the rental shortage. how that would fit in the picture, I don't know.

My whole point of all this is that, investors to housing market is not devil, they deserve a place in it, and deserve profits like all other persons. demonize investors won't solve the housing shortage problems as they are not the root cause, they are just player in it.

and the tax duction saga only means some monies transferred from investors pocket to government pocket. Will government be better guardian of that money? this the most important question to ask.

There will always be people renting, but we did not need investors outbidding first home buyers by 3x from 2010 to 2017.

Investors still have their place in the market. We just don't want investors borrowing a shit tonne of money to outbid FHB on existing stock. There's nothing stopping you from buying existing houses with cash, or you can buy a new house if you want to deduct mortgage. But the taxpayer is sick of deducting tax for people who have not put a single cent of their own money into it.

Yes, those numbers are terrific to see. Because up until 2017, investors outnumbered first home buyers 3 to 1. So Jimbo is correct when he says 75% of new sales. A new sale being either a first time buyer, or a new property added to rental stock, both transactions changing the number of properties available by -1.

This is where government programmes such as shared equity purchase comes in.

You have any example of shared equity successfully working anywhere Kate?

The same place where you'll find a property bubble that hasn't burst.

Don't know how successful but the programmes exist;

https://www.westpac.co.nz/home-loans-mortgages/options/shared-equity/

It’s a complete disaster

In what way a disaster?

Uptake has been poor and that comes back to the pathetically ill informed way the government’s bureaucrats conceived it.

Of course it’s no surprise, at least to me. Over the past week I have come across two ‘Principal advisors’ in government ministries with less than 5 years experience. And policy generalists lacking both academic training and practical experience in the policy areas they are working on.

The central government bureaucracy in Wellington under this government has gone from mediocre to a complete debacle.

Has the poor uptake been reported on? Any links would be helpful.

$20/week - that will cover the extra tax and mortgage costs. You can't lose with property.

Are you taking a pun or this is a serious well researched comment?

😳

Do you own research - I did mine at a property investment seminar and a Facebook investors group. The only way is up.

Lol

Brilliant joke.

Up into the stratosphere.

The rents are like a helium Balloon i guess?

😁😁😁😁🤔🤔🤔

Its also one of the Church's 10 commandments.

When I hear that phrase "The only way is up" .....https://www.youtube.com/watch?v=vjD3EVC1-zU

NZ house prices ....to the moon AND BEYOND !

Pretty low rate of inflation. I am confident that the overall rate of rental inflation will be lower, as Barfoots seem to manage few of the new build townhouses hitting the market, which will be bringing the average down.

Just to clarify - most of the new townhouses are 2 bedrooms, it will be increasing the proportion of the market that is 2 bedrooms, reducing the proportion of the market that is 3 or 4 bedrooms, hence reducing the average.

Conversely, it might increase the average rent of 2 bedroom properties, as it is improving the quality (or at least the age) of two bedroom rentals

I would say so, those rents look cheap. $630 a week in Auckland is going to get you a dump, its like $650 to $700 a week even down here for a 3 or 4 bed house you would actually want to live in.

Yes, sounded on the low side to me as well.

2 bedroom is accommodation for 13 in the utopia of NZ. Add another 5 if it has a garage.

The answer, of course, is a lower capital cost for new landlords - ones who will replace the current owners as costs (% rates) rise further and prices fall, and make them reconsider their holdings. Tenants can only pay what they can pay, then they leave the place empty and make alternative arrangements (the dwelling ratio is about to increase?)

If it takes $X rent to justify a new rental purchase for $1,000,000, then it takes half $X at $500,000 to make those same numbers work. That doesn't guarantee rents will fall, but it neuters the argument that rent = costs +. Costs (% rates) can then follow prices back down as long as restriction are put in place (LVR's, DTI's etc) to discourage malinvestment.

It's not how much we earn in dollar terms, but what that will buy.

Great analysis, thanks. Aligns with my anecdotal observations that the lowest income neighbourhoods are being hit the hardest by increasing inflation in rental accommodation costs.

Of course in the low-income neighbourhoods the landlords know that they can increase rents and the state will cover it.

ASUP is a largely a welfare payment to property owners - inflationary and of no benefit to those at the bottom.

Yep, it's my concern as well. Government needs to find a way to unwind that subsidy/supplement (i.e., restore housing affordability).

The govt raised the ASUP when they got in, they are not on your wavelength

That's why I put in a petition to Parliament. To my mind the taxpayer just cannot continue to subsidise this cost-of-living expense, however neither do we want tent cities popping up everywhere. It's a complex problem.

Dont waste your time Kate. Haven't you heard that today's petition is tomorrow's 'chippie' wrapper. But if you want to do that I will put together my own questions to parliament and the housing minister

I tend to agree it’s a waste of time and energy, based on my own experience. The government bureaucracy is ultra arrogant and they believe their own BS.

:-) In the tradition of Blackadder, I have a cunning plan :-).

It could also be that the lower end cause more damage and the cost of getting that fixed is astronomical right now.

The reality is that being a residential landlord in NZ makes absolutely no sense right now unless you still think house prices will double again soon.

Agree with the last comment - it makes no investment sense to me - but still a lot of people would rather invest in bricks and mortar than stocks, etc. And many rental investors have owned the properties they rent for so many years that profitability (as opposed to yield) is a fantastic earner.

True but why not sell and transfer that capital to something higher yielding, rather then just see it fall.......

Personal choice. My husband grows vegetables as more of a hobby than a cost-savings - same goes for his interest in pottering around with redecoration and minor home improvements. He likes having projects on, regardless of their ROI. There might be some of that in providing rental accommodation as a hobby too? Just a guess.

Paul Henry likes to grow vegetables as well, while getting an all over tan. Its nuts

So real rents have fallen I guess? Not going to help those dealing with the rises though

I guess, but the average person hasn't had a 7.4% pay increase as well, so we're all losers.

Yes they have

Wages increased a lot from mid 2021 to mid 2022. Don’t know if they have increased that much since mid 2022? Maybe I am wrong.

one of the reasons I think inflation will have moderated significantly by mid 2023 is wage inflation moderation

Salary earning Mum and dad investors have, just not the tenants.

This is not a tax debate, it's a story of the constant failure of our govt.

A) The NZ govt failed to build enough social housing for more than 40 years, this after underwriting a taxpayer sponsored lower decile breeding programme for the said time & longer. Two points to note here, 1; they knew they were coming & 2; they did nothing about it.

B) Due to the gap in the market becoming so obvious over the above timeframe, many ordinary people with their hard earned savings [seeing the gap in the market] decided to buy mainly older type dwellings & rent them out, after having seen the above govt sponsored breeding programme going on for decades & also their failure to provide for them.

C) NZ govt feels guilty about not building enough social housing for so many newcomer lower decile folk, so decide to to top up their benefits with an accommodation supplement, so they can afford a roof over their heads, as at the same time property prices rise across the western world, not only just here in NZ.

D) More hard working kiwis see what's happening & go out & buy more rental properties as they now see that they will get a govt subsidy [one step removed] for their rentals, as those who are bereft of any other options at the now booming bottom end of our [now very visible] crumbling culture, have no choice.

E) NZ 6th Labour Govt removes interest rate deductions for rental properties for many M&D rental providers as they cannot stand others not only filling the gaps, but making money, a true admission of their own failures, as witnessed in the recent Kiwibuild debacle [of both the urgent need of new social housing, & then once again, the failure to deliver, thereof].

Govt is the problem. Not the solution.

as at the same time property prices rise across the western world, not only just here in NZ.

Disagree. If you said the Anglosphere, sure. It's an extension of bubble economics.

This doesn't make sense. $20 per week is $1,040. And the average rent is $629.53. Hard to figure out what the message actually is trying to say.

It's hard to figure out what you're saying. If the average rent is $629.53 after a 3.29% increase, then the rent prior was $608.82.

$629.53 - $608.82 = $20.71 difference.

Here’s an easy way to stop rising rent.

Tax rates for landlords are set dependent on the number of rentals they own. The more you own the lower the tax rate.

This incentive for everyone to own more rentals, thus more housing available for rent. Possibly drive rent down.

Result- Renters happy, Landlords happy, Trades people happy as there will be more work, Government happy as there will be no housing crisis.

NZdan NOT be happy

I'm just speaking for the majority of hard working net taxpayers in this country who are tired of seeing slum providers not paying their fair share, that's all. Removal of interest deductibility is a great move. If it increases rents then so bet it!

Next we need to remove the Accommodation Supplement.

slum providers

I take offense at that comment, although you probably think of all landlords as homogeneous

If it increases rents then so bet [be] it!

Until it does, then I bet you won't be so chirpy.

While it's hard to measure, I'd say there's probably a 50/50 mix of slum providers and landlords that were fortunate to buy a property that's not yet in need of maintenance. The taxpayer shouldn't enable landlords to accumulate properties by pushing up prices out of reach of FHB while giving them a tax break because they borrowed too much. It was a RORT.

I'd be happy for tax deductions to be reinstated IF homeowners get the same tax treatment, otherwise it's skewed.

You're a cost estimator or qs for commercial buildings right. I guess you think you know all things property and qualified to give your unqualified opinions.

It's pretty simple.

If you're buying something older, it's a hidden gem with potential.

If you're renting the same property, a slumlord is profiting from you.

The 'same property' that then had a thorough going over before being rented 🔨 from builder and painter to AC man

NZdan probably says auckland 'slumlords' are to blame for auckland floods tonight. Not a nice experience for those flooded

Just because you say it happens, it doesn't mean it does. Well, I suppose it probably happens more frequently thanks to Healthy Homes legislation but you cannot give landlords the credit. I mean, the mere fact the legislation had to be drawn up is extremely telling.

As for the floods. Well I wouldn't go THAT far, even if it's tempting. There's probably a few landlords that have ignored requests to have the stormwater fixed on their properties, which has worsened things.

Just remember everyone, the price of the asset dictates the income (only applies to property)

and farms, businesses etc.

except farms and businesses have productive use for selling goods and services which actually fun fact are included in their value (it is not solely the value of property asset). The only time when they are not is when they are literally not farms and businesses but rather kept empty doing nothing in the case of land banking or renting to a separate entity (for which that separate entities value is not counted in the value to the main party; you cannot claim the productivity/productive value and assets inside of the tenants as a landlord).

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.