Residential properties appear to be selling for around $100,000 less than their asking prices, with vendors being slow to accept how much values have fallen and buyers driving hard bargains.

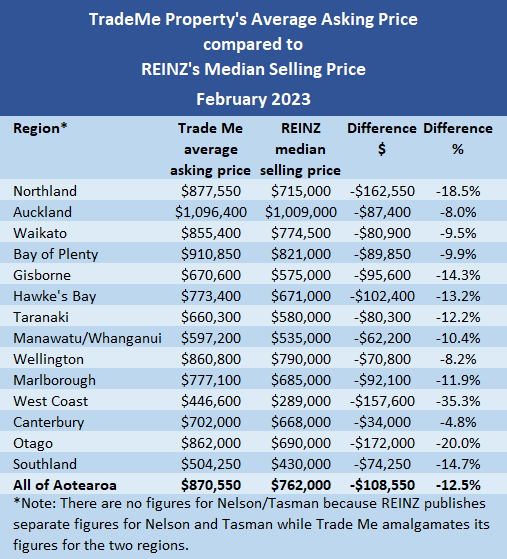

Comparing the average asking prices on Trade Me Property with the Real Estate Institute of NZ's median selling prices, shows on average there is a huge gap between the prices vendors are hoping for and the prices buyers are prepared to pay.

In February, the national average asking price of properties advertised on Trade Me was $870,550, while the national median selling price recorded by the REINZ in the same month was $762,000, a discount of $108,550 to the average asking price.

The same phenomenon was evident throughout the country, with selling prices substantially lower than asking prices in all regions.

The biggest difference between the two figures was $172,000 in Dunedin. Canterbury had the smallest difference at $34,000.

The size of the gap between asking and selling prices suggests many, if not most, vendors have not fully accepted how much the housing market has changed over the last 12 months and have unrealistic price expectations when they list their properties for sale.

Selling prices have also been falling faster than asking prices, with the REINZ's median selling price down 13.9% in the year to February, while Trade Me's average asking price was down 9.2% over the same period.

That also suggests vendors have been slower to adjust their expectations to the changing market than buyers.

That's likely to be one of the main reasons the market has been so slow, with residential sales down 31% in February compared to the same month last year, while the number of homes available for sale was up 25% compared to a year ago.

Although the Trade Me and REINZ figures are calculated differently, with Trade Me providing an average price and the REINZ a median price, the difference this creates is unlikely to be huge.

The chart below shows the difference between asking and selling prices throughout the country, and although it is not an exact measurement, it probably gives a reasonably good idea of what is happening in the market.

As the peak summer selling season is drawing to a close and economic uncertainties show no sign of abating, vendors hoping to achieve a sale over the next few months are probably going to have to bite the bullet on price in what is likely to be a painful exercise for many.

The comment stream on this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

168 Comments

I am sitting over here HW2.

Going long... Corn, butter and microwaves

Eating hash browns with baked beans and the little fake meat saussages, topped with chilli flakes... just got a big piece to rump out of the freezer for dinner.

Be great to have superimposed distribution curves of asking prices Vs selling prices at 50k increments, and see how far apart they are at the different price points

It's simpler than this comparison..

Read a NZ property's billionaire s take on it .

Bob predicted this 2 years ago

💥💥💥💥💥💥💥💥💥💥💥

https://nopunchespulled.com/2023/03/17/house-prices-collapse/

Interesting that Bob sees the market bottoming out at a value corresponding to the replacement cost of building a house as opposed to a value commensurate with what a house can be rented for, inversely scaled by the prevailing interest rate.

"Bob sees the market bottoming out at a value corresponding to the replacement cost of building a house"

Well, we're at that point already. That's why developers are struggling!

Man servant Bob. Brother of Baldrick

Developers like most speculate on land. They paid to much for theirs and with rising costs and little margin are toast

It's been established over the last couple of years dynamics that rents are determined by ability of renters to pay (ie incomes) rather than the house value (ie %ROI).

I have some sympathy for his view for new builds, they will, once bankrupt stock clears, track towards replacement.

But for older shiteboxs, its land value only and with no developers in the market, less then that....

Yeah, I think he is wrong, and the prices will drop below new build cost. Surely the new build cost defines the upper limit that someone will pay, not the lower.

Location Location Location

Agree. But Build prices will drop as they struggle for volume, as in GFC where they fell from 2.5k per SqM to 1.2k.

So bobs kinda correct 👍

Why would you pay the same price for a new car or a used one.

Building cost has nothing to do with value of an existing home. Maybe if you depreciate at 10% a year you are getting close.

Where not comparing cars bro!!!

New houses don't come with 50k of garden/ fences etc.

They compete in the sane market bro!

If newbies become to expensive in a falling market where buyers are preferring oldies then newbie's prices drop to compete brah!

They can build some really cheap houses in Detroit apparently:

The median listing home price in Detroit, MI was $79.5K in February 2023

Much lower consenting costs

Much less tight land use regulation artifically pumping up land prices

Much cheaper resources (esp. petrol)

Much more efficient, cheaper and less anti-competitive construction sector

Higher crime

Also high poverty and low incomes, $32,000 median household income...

Tts not so much the build cost it's the value of the land. How else do you explain the difference in prices of houses in California vs Michigan etc?

Yes, it's mainly in the value of the land, BUT that is determined by how easily that land is available to meet demand in developer real-time (approx. 9 months), and if the regulations are free enough for that to happen then this also means the mindset of the regulators 'get it', and thus consenting, etc. is cheaper and quicker also.

If you 'get' how to make land affordable, then everything else follows, but if the land is wrong, it is wrong all the way up the chain.

An experienced tradie in the US (10+ years) earns 15-18USD per hour.

Well maybe it depends on the State . As New York resident ( Upstate ) who has builders constantly working on renovating my house - the labor costs are considerably higher than that . $20US is the minimum wage payout for labor and skilled Tradies as you call them are much higher - like $35 US a hour or more

Or at a value commensurate with what can be afforded (to buy).

I am assuming that he must be assuming that the OCR will come down quite a bit in the next 3 years, in order to re-stimulate demand. Which I think it will, but I think 3 years is way too short for the 20% drop in prices to be regained, given that:

- the economy is likely to be very weak for the next two years

- bar a major external or internal event, and bar inflation falling much quicker than anticipated, the OCR is still likely to be at least as high as 3.5% in two years ie. not low enough to really stimulate demand

prices are likely to fall at least another 5% in the next year, even if that is regained near the end of the next two year period, I can’t see any way that the 20% fall would be regained in one year.

So maybe 5 years - not 3.

And he caveats on there not being a big migration exodus. I think that’s a scenario with at least a moderate likelihood.

I quite like and respect Bob Jones but that was a somewhat flimsy ‘I reckon’. I don’t agree with his conclusions.

He should stay out i of a market he doesn’t understand .

If value is > than cost new building will occur

If cost is > than value new building will cease .

we are now in the second cycle . Cost does not set a bottom line for value .

Well said.

Remember the car Homer Simpson designed that no one wanted and also cost a fortune to build - the value was much less than the cost. Although personally I quite liked it.

How is your suped up lada by the way? 🚗

'Cost does not set a bottom line for value.'

You are conflating issues. Yes once the asset is built and has to be sold, your statement could be true, BUT prior to it being built, through planning, the intent is that value will be more than cost, and then as a break-even value equals cost. This underwrites all valuations, otherwise, no one would build anything.

Agreed…cost matters at the margin

price is set by the producers willingness to sell and purchasers willingness to buy…producer doesn’t want to sell at a loss, buyer wants to purchase no more than the perceived value

Goes much deeper.

- Market price during "normal" times: cost + 20%

- Market price during boom times: cost + 50%

We have had a boom time, with huge credit expansion and population demand enabling higher prices to be paid. So manufacturers have enjoyed healthy margins. If not then they're morons. When things get tight, are Winstone Wallboards going to sit around with idle extrusion machines because they're still wanting 50% gross profit while borrowing power cannot support all the components that go into a new build?

Well Bob also thinks that it's thanks to Jacinda that the housing market is finally being fixed. I hope he congratulates her.

"House prices are collapsing dramatically across the nation. As there’s approximately twice as many home-owners as renters, this is unwelcome news for most folk.

Exactly two years ago on this blog I predicted this would occur as a direct result of some mind-blowingly stupid government actions at the time."

So you can blame one person in the Government for all things bad that happen in the economy, but not house price falls?

It'll be interesting to see if Council valuations are reduced? Just when they need the extra revenue - ie city rail blow out.

The budgets drive rates uplift as funding dictates, not the valuations.

The amount of rates you pay is not correlated to the RV per se, unless your house's RV goes up more or less than the average.

The covid CV hump 2019- 2022 will see values drop back to the normal curve line/ 2018 levels plus 1/2 Inflation maybe

That’s not how council revenue from rates work. The council decide on how much they need to collect, then they divide that amongst ratepayers on a proportional basis (your relative council valuation determining what proportional share of the total). The value of housing, and whether it has increased or decreased, has zero relevance to the council collecting rates revenue.

Uhhh not sure about the average vs median selling price comparison there Greg, we know that real estate values exhibit pretty strong negative skew, so the median will be less than the mean here as a matter of course. There's a very long tail of a very small number of incredibly expensive properties which pushes the average price up significantly.

While I am unsurprised to see median selling prices less than average asking prices in this market, I suspect the true gap here is probably about half what's been published.

Either that or the bottom has fallen out, which is entirely plausible given the cost of money. If so, those properties skewing the average up won't be doing so for too much longer.

I concur.

I'm not sure that this comparison is comparing like with like. For such a comparison to be accurate you'd need to match individual properties with asking and selling prices.

But don't get me wrong ... I'm tracking two segments of the market in Auckland and I am seeing people drop their original asking prices by $100k (and more) to get them sold. (Some are still making a 'profit' as they've owned them for 3 years or more.)

Yes good point, but I spend a little time checking the daily auction results, my “at a glance assessment” is that there are many properties now selling well below 2021 RV, which would have to be a hopeful expected price for any vendor. In my area there are very few asking prices attached to properties, although have noticed a few now this week, when enquiring here on vendor expectations the prices quoted back to us seem to be 12 - 18 months out of date, had one the other day was after $200,000 more than they paid for it in Feb 2022!

Ugh. I'm counting our lucky stars as the bank changed our lending amount in early 2022 thus we couldn't buy a place. Would have a been a bit of a stretch financially and a lot more stress today.

Lucky reprieve indeed - you could have been on the poison "ladder".

You mean he could've jumped onto the board on a snake square.

10/10 Cover image.

+1 (although it could well become an arm and a leg...)

Some commenters are going to cream their pants over this article!

They will be very spent from the last few months.

Yep, Jacinda's policies delivering on her election promises to bring house prices down. First government in living memory to do so.

…errrm, except that she said she didn't want to see house prices drop!

The election promise was to build 100'000 affordable homes, never to "bring down house prices"

How many houses did the private sector build in the last 5 years that are going to be 'affordable' by the time this is all over, LOL.

Government of unintended consequences unintentionally hits goal....

Ardern wants to see small increases in house prices, admitting people 'expect' this | interest.co.nz

"Prime Minister Jacinda Ardern says she would like to see small increases in houses prices, acknowledging most people “expect” the value of their most valuable asset to keep rising."

I've listened to that video several times. The headline says Jacinda wants house price growth but she never actually says that in the video at any time. She says sustained moderation - no idea what she actually means by it but I took it to mean that house prices needed to be moderated in a sustainable way to be more in line with wages. Moderation can be up or down. Sustainable I took to mean not massive increases and massive drops.

I think people heard what they wanted to hear and the reporter who I actually rate put words in her mouth.

If she had wanted to say she wanted house prices to go up she would have said it.

Hre is another report which says that she was OK with house prices falling.

"Speaking to RNZ for an extended end-of-year interview, Ardern said she hoped 2022 would halt the recent "runaway increases in house price growth".

Asked directly whether she wanted prices to come back, Ardern said: "Yes"."

https://www.rnz.co.nz/news/political/457683/ardern-wants-runaway-increa…

Yvil

"…errrm, except that she said she didn't want to see house prices drop!"

Yes she did.

"Speaking to RNZ for an extended end-of-year interview, Ardern said she hoped 2022 would halt the recent "runaway increases in house price growth".

Asked directly whether she wanted prices to come back, Ardern said: "Yes"."

Indeed - she said both things. She never met a sentence she did not like .

Nope, she never said she wanted house prices to go up. They were the reporter's words not hers.

She said: "...it is much more sustainable to have those much smaller increases. I think people expect that you see that in the market."

Let it go agnostium, you're digging yourself a hole. Your original statement "Jacinda's policies delivering on her election promises to bring house prices down. First government in living memory to do so" was just plain wrong!

It was Judith Collins that promised to do something about the prices. Jacinda said she had no intention of stopping house price inflation

Chlöe Swarbrick ran for Auckland Mayor in 2015 with her main policy being that she wanted house prices to fall. I think she was the first to get it.

Offensive comment deleted. Ed

Please leave lazy your Maori bashing comments at the door when you enter this (mostly) non racist debating chamber. Nga mihi nui.

Thanks editor.

Truth hurts !?

I see you are unrepentant. The editors are sending you a message if you care to take it on board.

Some commenters are going to cream their pants over this article!

You mean just like specuvestors were creaming their pants when the country was awash with cheap cash and house prices rose 30% in 12 months a few years back???

Flat household consumption in Q4-22 despite a tourism bounce back and net positive migration. The reverse wealth effect from recent buyers sitting on negative equity must be at play here.

That picture got a good chuckle from me.

Is that Napolean's surgeon who could amputate a leg in 17 seconds, I wonder? If I recall aright, all the patients died afterwards...

Yes Gregg, once again a great pictorial representation.

The statistics are likely not revealing much of value yet. As price falls accelerate, there is no reason to buy into negative equity until price falls slow.

The few that are selling and settling at the agreed price are the few fools willing to pay those prices either by necessity or whatever circumstance drives them to it. Everyone else is waiting their time.

The time to buy is when people say that realestate as an investment is dead forever.... Then you know that all the weak hands are out of the building.

I've been saying that for 3 or four months.

Fill ya boots son.

When you go to an auction and the only ones there are investors that have done their sums and have a set price where the house stacks up based on yield, that should be the bottom. Of course that assumes the speculation switch hasn’t been reengaged by the RBNZ or the National party.

By this theory prices need to drop another 50% or so (or interest rates drop which is probably more likely).

More if the tax stays same ie bright line and int deductions..... Investors will need to see cash flow positive, I think you may be waiting a bit.

You gotta be fast. Earned 250k in 2 months back in 2021 by buying and selling a new build.

If investors are smart enough they should've gotten out by now.

Many are real smart having learnt their skills through property investment classes advertised on Newstalk ZB....

Those who decided to keep their properties during the boom and expecting even more profit were simply greedy and now paying the price for it.

My profit looks pretty good in my bank account earning interest.

No tenants to worry about either.

That is a gamble though and luck. I know people that failed at that and are now holding a house that they couldn't sell 100k less than they purchased it for. Many that purchased in 2021-22 will have to sell at a loss. The only good thing is the house they are buying will also be worth less. But they could lose all their equity and deposit for the new house. I wonder if that is part of the current problem at teh moment.

Is that before or after tax?

I lack sympathy for these sellers because they willingly engaged in speculation. What's happening is a natural and expected consequence

Yeah. At least in gambling (and sharemarket) you only lose the money you chose to bet.

In many cases the losses here are going to be many times the deposit and repayments made to date.

It should have come with a warning.

:)

Buying with a mortgage is like speculating on margin. It makes you look smart on the way up, and broke on the way down!

Given that all NZ mortgages are full recourse, the banks don't really care how much you lose. In fact, due to the remaining debt being unsecured, they make out even better because they can charge you 12-15% instead of 7%.

It was clearly in the mortgage docs you signed..... you borrowed money , you pay it back.... are you 18

That’s a sweeping generalisation. Plenty have to sell due to changed financial circumstances. Not everyone is a speculator.

Plenty don't.too

Totes bro?

Timing is everything?

The best TIME to buy is just when the market is just on the up. Don't!!! Guess the bottom you will get it wrong in this fiscal climate clusterfock!

The market has another 15- 30 % to fall. Just depending on the panic sellers who are now FOMO 😁👍

REMEMBER THE CLOSER TO THE BOTTOM YOU BUY THE QUICKER YOU get back any loss and make a gain.

It's just common sense...

Ignore RE A's.experts with their noses to close to the data/ money/ srats trough...

With so many PBN how does trademe have any idea what the asking is?

They still need to enter a hidden price (might be a range?) so that when buyers search for 3 bedrooms in Ranui in a price range of $X to $Y Trademe knows whether to show the listing or not.

I hope TradeMe changes this to get ChatGPT to decide the value range - that would have the potential to be much funnier.

Lol yeah an AI would be way better and actually decide the value on a range of logical factors. Not the emotive fomo nonsense in nz... if it worked out value for the buyer prices would fall tenfold.

One of those logical factors is how much an equivalent house sold for. At the end of the day it would need to be trained on the outcome of factors, ie a real price for a sold sticker on an equivalent home. So in no way void of FOMO.

Great idea though, you could turn it into a website where people could go to view the machine learnt price of a home they're looking at! Give it a catchy name like "homes.co.nz" and travel 8 years back in time to release it!

That is also how buyers can find out what price the agent expects it to sell for, by ordering all houses by price and then finding that house you are interested is in the list in relation to all the other houses.

Yes but my experience is that this is the most optimistic, hopeful price. They don’t usually get it.

Good point ITGUY, shows how meaningless these figures are... working out an asking price on an average price bracket is pretty misleading...

Easy to price most houses...

💥Look at CV. If it's a new CV set during Covid then ignore it and go to last pre covid CV and start from there.💥

💥In other words ignore the covid hump!

IGNORE Homes and One roof!!!

To eas

Like it. The Covid Hump of cheap debt stupidity.

I prefer to stick to the facts and work on actual price at the point of sale....... they use this stat in the UK a lot but in the UK properties have asking prices.

You'll pay to much .

similarly beo implies the least they will take - so the expectations could be higher

similarly beo implies the least they will take - so the expectations could be higher

Doesn't the agent have to tell the seller what they expect it is worth? So guessing they use that figure.

FFS bro. You have to give trademe a price expectation number when you list.

That's why searching by highest or lowest give properties a pricing order even though you see no price.

TM 101 bro

The lister has to list a price so it can be categorized in TM so when you search highest or lowest price they are ordered

The cracks in the housing Ponzi are getting more and more visible by the week.

With Auckland central down 400k and Papakura down 31% its no longer a ponsi... it "WAS A PONSI"

We are well out of Denial now, even mainstream media know its a crash... and crashing way way faster then Ireland did.

Agreed - looks like a larger portion of the market is entering the panic phase. It is still amazing to see data that suggests that over half of the regular population still doesn't grasp how deep this property crash is going to be.

Winter is coming, and the great NZ property bust along with it.

Housing bubble crash stages:

1. Rising prices

2. FOMO

3. Euphoria

4. Denial

5. Disbelief

6. Panic

7. Bust

I think a ‘partial bust’ is needed between 4 and 5, and , ‘complete bust’ or ‘complete capitulation’ is needed at the end.

Because I agree we are reaching the panic phase, but things have pretty much busted already.

8. Sell

9. Sell for many months

10. Offer a low low price

11. Me buy!

Banks folding, printing money exercises are folding, bonds folding.

House prices starting to fold. Good times coming.

The ‘Everything Bubble’ has moved into the ‘Everything Crash’

Nah. There is money being spent. Just not in the crazy manner of the lasy 8+ years.

We are in software - automatìon . People are spending big again to drive business costs down, to deskill roles and simultaneously spend up on smart marketing. Most businesses already prepping to lose staff and how to drive fmore business for those that will remain.

Game changed. Didnt stop.

Well I am talking about investments really, when I am talking about ‘everything’.

And of course, obviously, there will always be some pockets of success and strength. Even in the Great Depression there was.

Wouldn’t demographics have been a pretty good indicator of what you are saying? We knew there was a bulge of Boomers born, it’s obvious that they would invest before retirement and gradually pull it out again afterwards. It’s quite possible that asset prices decline for a good 20 years isn’t it?

Ultimately deflationary. Bring on the robots!

"Good times".

your job may be at risk of folding too.

No one ever seems to think about that. They seem to think everything will be cheaper, they'll live like Kings amongst men and everyone else will cop all the fallout. But not them.

Meanwhile, in the Acorns & Other Various Winter Stores/Provisions Department', squirrelling continues unabated. Plan for the worst, hope for the best. Although the French generally weren't afraid to give a few an ambitious haircut if the mood struck them. I note they have recently rioted because they can no longer retire before they've finished high school on a full state pension. I wonder what it would take to see the same sort of thing here.

"I wonder what it would take to see the same sort of thing here."

TOP & the Greens in Govt

A vaccine mandate and forced shutdown of the economy for a virus - we got pretty close.

The sooner we get this recalibration out of the way, the better.

Given that many FHBers are now well into their 30s, they don't have the luxury of time to hang about and wait for the market to have a gentle landing if they have any intentions of family formation.

It's like the OCR. We knew what was coming, and still is, so getting it out of the way allows us all to move on in the new environment.

Wishful thinking, all of that, of course.

The best time to not buy a house is now.

I had kids in my 50s and we are still renting in my 60s.

I think I will skip paying 3 times too much for a house and leave that hard work to those braver and more committed than me.

For anyone in the 30s or whatever wanting to buy a house for emotive or fomo reasons is a mistake.

Life is for living and spending time with family doing what u enjoy. A house is a place to sleep and play or to generate money and facilitate more time for what they love..

So a smart person or couple will wait as long as it takes to buy SMART : at a low price - a house that can be affordably extended as the family grows and one that in probablility will increase in value or offers addition revenue streams.

If a couple are on a mean salary of say 150k and value their wellbeing and family time and budget ok then buying smart will potentially cut off 25 to 50 % of their lifetime of working hours. Time available for what they choose and less stress.

So why rush for any reason...best advice foŕ them is to wait and wait again and find the best possible property at the lowest possible cost. The market will be low for a few years so mo rush. Think about aus opportunities too as its way better life than hete in their 30s.

Best plan... wait for a lot of the people who bought from 2015 to 2021 to start to struggle from job losses and mounting pressure..they will be forced to sell and noone will be buying. Then hunt and hunt for the right place and put in low ball high time pressure offers. Whilst it seems hard .. its a life lesson for all and most on all sides will learn from it and end up better off.

Whilst it seems hard .. its a life lesson for all and most on all sides will learn from it and end up better off.

Funny, we only got into this mess because one group of people seems to think that they should be immune from life lessons and have whatever they want when they want.

Meanwhile, young people should always be patient, or work harder, or be prepared to move to another country to buy a house in this one. There's always something they're doing wrong or a lesson they need to taught.

E: OK this was a little bit tetchy, but if I'd sat on the sidelines for as long as I've been told 'houses are overvalued, wait for a correction' I'd be 12 years older and still no closer to owning, with zero chance of catching up to insane deposit requirements. These things come at a cost for other parts of your life, endless 'just hold tight' doesn't stop life from marching on around you, and you only have a certain number of working years in you to pay off mortgages (or even qualify for them).

I hear that a lot The flaw in that arguement is the flawed belief that owning ones oown home asap for some reason trumps ones medium to long term happiness.

The marketers caught onto that belief being part of the NZ culture and have used it to drive up house prices in boom times to make more money. Smart marketing professionals get paid to do that.

Also and this is key to remember... there is no right for anyone in nz to own their own home or land at any price. Anymore than i or anyone else will have a right to have any sort of pension in 15 to 30 years (the probability gets less and less). Change accelerates and its up to individuals to think, plan and adapt... its actually always been like that.

Great post OSE, I find myself concurring with a lot of your "lifestyle" thinking.

I hang with a lot of middle aged surfers and lifestylers... i dont know of any that are unhappy. Quite the opposite

I also know a lot of middle aged business people who work hard and play 'keep up with the joneses'.. they try to avoid talking about my surfing/whatever most days (its hard to work and struggle when you think that others are playing) and try to convince me i should do that.

But i still make plenty of money.

I heard this once... tis good advice . 'The god(s) made the world to play in. It is just because humans take it so seriously that they struggle' (or somthing like that).

Comparing median with averages could be misleading. Throw in how Trademe calculate the asking price into the equation and it could be even more skewed up or down. People getting carried away with the excitement of the slow motion train crash. Wonder who the forced sellers are in this environment.

* trademe calculates the asking price into the equation"! WTF!?

- the lister inputs the list price into TM. TM calculate the avarages

- what equation

Stick to being the woke police bro!

Sellers remain delusional, and Agents have been supporting those delusion just to maintain listings. Well....the Ponzi nature of prices is well out of the bag for all to see now unless you are deaf, blind and dumb. Most cannot buy under new lending rules, and those that can are just waiting to save themselves 20-40% from printed stupidity.

More and more lenders will be rolling weekly from 2% to 7%, which will fuel the transition from fear to capitulation.

The kaaaaark moment is approaching.

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⣤⣶⣶⡿⠿⠿⠿⣶⣦⣀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣀⣤⣤⣤⣤⣀⣀⣠⣴⣾⣿⣿⣿⣿⣿⣿⣿⣤⣄⠀⠀⠀⠀⠈⠛⢷⣄⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⢀⡴⠋⠉⠉⠉⠙⠛⢿⣿⣿⣟⠿⣿⣿⣿⣿⣿⢿⡿⢿⣿⣿⣦⡀⠀⠀⠀⠀⠙⣧⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⢠⡞⠀⠀⠀⠀⠀⠀⠀⠀⠈⠛⢿⣿⣮⡛⢯⠛⢿⠢⡙⢦⣽⣭⣮⣿⣆⠀⠀⠀⣄⠸⡇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⢀⡟⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠈⠛⢿⣦⣥⡶⠗⠲⠿⣿⠁⠀⠈⠙⢧⠀⠀⢹⠀⣿⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⣾⠇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣹⣟⣀⣀⣀⡀⠀⠀⠀⠀⠀⠸⠷⣦⡀⠀⢻⠀⠀⠀⡄⠀⠀⡀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⢠⣿⠀⠀⠀⡆⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣴⠟⠋⠁⠀⠀⠈⠃⠀⠀⠀⣆⠀⠀⢹⣧⠠⣈⠀⠀⠐⡇⠀⢸⠁⠀⢀⠤⠒⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⢸⡇⡀⠀⠀⣇⠀⠀⡇⠀⠀⠀⠀⠀⠀⠀⣸⠃⠀⠀⠀⠀⢤⣤⡀⠀⠀⢀⣿⡆⠀⠸⢿⡀⠙⣷⡔⣾⡇⠿⠟⢰⡶⢁⡴⠖⠂⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⣾⡇⢳⠀⠀⢹⡄⠀⣷⠀⠀⢸⣧⠀⠀⠀⢻⡀⠀⠀⠀⠀⠀⠙⣿⣶⣶⡿⣿⠀⡀⠀⣸⡇⣰⡟⠳⠀⠀⠀⠀⠀⠀⠀⠘⠻⣥⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⢸⡇⢸⡇⠀⠀⣷⠴⠉⠙⠀⡀⠉⠀⠀⢸⡄⣷⠄⠀⠀⠀⠀⢀⡟⠀⠸⡇⢻⡟⢁⣴⢟⢠⣿⠃⡄⠆⠀⠀⠀⠀⠀⠰⠄⣀⠈⢳⡄⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⢸⣧⢸⡇⠀⠀⣧⠀⢠⠀⣀⠻⠆⠠⡄⠈⣷⡟⠀⠠⣄⣠⣤⣾⠁⠀⠀⢷⠈⣿⣿⣿⣸⣾⣿⠀⠰⠀⠀⢀⡤⣤⣀⠀⠖⠈⠁⠀⠹⣄⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⢸⣿⣾⣿⣸⣷⣿⣴⣼⣴⣿⡆⢲⣦⢳⢠⠀⢧⡀⠀⠉⠉⢉⣿⣇⠀⠀⠘⡆⢹⣿⡏⣿⢿⣿⠀⠀⠀⠰⠁⠀⠀⠈⢷⡀⠀⠀⠀⠀⢿⣦⣄⠀⠀

⠀⠀⠀⠀⠀⠀⢸⣿⣿⣿⣧⣸⣛⣯⢁⣷⣻⣿⣸⣿⡞⡎⣧⠀⣿⠀⠐⠒⠛⠋⢻⡄⠀⠀⠀⠀⢻⣇⣿⣦⢻⡄⠀⠀⠁⡾⠻⣷⣄⠀⠳⡄⠀⠀⠀⢸⡇⢹⡆⠀

⠀⠀⠀⠀⠀⠀⢸⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣷⣽⣧⠁⣿⠀⠘⠷⣤⣀⣠⣴⣯⣿⡄⠀⠀⠀⠀⠻⣿⣿⠀⢿⡀⠀⠀⢀⡴⠟⠛⢷⡀⠹⡄⠀⠀⠀⠇⢸⡇⠀

⠀⠀⠀⠀⠀⠀⠈⣿⡿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⡄⣿⠀⠀⠀⠀⠀⠀⠀⠉⠙⢷⡀⠀⠀⠀⠀⠙⠿⣄⣸⡇⠀⢠⡟⠀⣠⣶⣾⣷⣄⠈⠀⠀⠀⠀⣾⣷⡀

⠀⠀⠀⠀⠀⠀⠀⠘⣷⣿⣿⣿⣿⣿⣿⣟⣿⣿⣿⣿⣿⡇⣿⠀⠀⡀⠀⠀⠀⠀⠀⢀⠘⢿⡄⠀⠀⠀⠀⠶⠬⠿⠃⠀⣿⠀⠀⣿⣧⣼⣿⠻⣆⠀⠐⣄⠀⣿⠈⣧

⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣿⣏⡿⣿⠻⣿⠟⣿⣿⣿⣿⣷⢻⠀⠀⢻⡀⢢⠀⢰⡀⢸⣧⠈⠻⣆⠀⠀⠀⠀⠀⠀⢸⡄⣏⠀⠀⠈⠙⠋⠁⠀⠙⣆⠀⣿⠀⣿⣠⣿

⠀⠀⠀⠀⠀⠀⠀⢸⣿⣿⣿⣿⣿⣿⣿⣷⣆⣿⣿⣽⣿⣿⢸⡇⣧⢸⡇⢸⡀⠈⣧⠀⣿⡄⠀⢹⣷⣄⡀⠀⢀⣠⣾⣧⢻⡀⠀⠀⠀⠀⠀⠀⠀⢸⣷⣿⡼⠋⢩⡟

⠀⠀⠀⠀⠀⠀⠀⢸⣿⣿⣿⣿⣿⣿⣷⣿⣿⣿⣿⣿⣿⣿⢸⠁⣿⢸⡇⢸⡇⠀⣿⠀⣿⡇⢰⢸⣿⣿⣿⠳⠿⠿⠛⠙⢧⣿⣤⡀⠤⠤⢄⣠⡴⠟⠁⠸⣧⣠⡾⠁

⠀⠀⠀⠀⠀⠀⠀⠀⢿⣿⣿⣿⣿⣿⣿⣿⣿⣿⢿⣿⣿⣿⣼⠀⣿⢸⣇⢸⡇⢀⣿⠀⣿⡇⣸⢸⣿⣿⣿⠀⠀⠀⠀⠀⢸⡏⠈⠉⠛⠛⠋⠁⠀⣄⠀⠀⢻⡟⠁⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣹⣿⣿⣿⣏⣹⣿⣿⣻⣷⣿⢻⣶⣿⢸⣿⢸⡇⢸⣿⢰⣿⡇⡟⣸⣿⣿⣿⠀⠀⠀⠀⠀⠘⢧⣞⢻⣿⣶⡄⠀⠀⢹⡇⠀⢰⣿⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣷⣿⣿⣿⣷⣿⣿⣿⣿⣿⣿⢸⣿⣿⣸⣿⣸⡇⣾⣿⣼⣿⣿⡇⣿⣿⣿⠟⠀⠀⠀⠀⠀⠀⢀⣙⣿⡇⠀⠀⠀⠀⠀⠃⠀⢸⡏⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣿⣿⣿⣿⣇⣿⣿⣿⣿⣿⣿⢸⣿⣿⣿⣿⣿⣷⣿⣿⣿⣿⣿⢰⣿⣿⣿⠀⠀⠀⠀⠀⣠⡾⠛⢻⣿⡇⠀⠀⠀⠀⠀⠀⠀⢸⡇⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠹⢿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⡿⢸⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⡏⣾⣿⣿⡟⠀⠀⠀⠀⠀⡏⠠⠐⠋⣿⡇⠀⠀⠀⠀⠀⠀⠀⣾⠁⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⣿⡿⣿⣿⣿⡏⣥⣌⢛⡈⣶⢸⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⢱⣿⣿⣿⠃⠀⠀⠀⠀⠀⠳⣤⣤⠾⢿⡇⠀⠀⠀⠀⠀⠀⢀⡿⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⣿⣧⣿⣿⣿⣧⣿⣿⢸⣿⡟⣸⣿⣿⣿⣿⣿⣿⣿⣿⣿⡏⣼⣿⣿⡇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⡇⠀⠀⠀⠀⠀⠀⣼⠁⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⣿⣿⢿⣿⣿⣿⣿⣿⢸⣿⠇⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⢷⣿⣿⣿⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⣧⠀⠀⠀⠀⣠⡾⠁⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣾⣿⣿⣿⣟⣿⣻⡟⣸⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣼⣿⣿⡟⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⡟⠀⢀⣠⡾⠋⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠘⣿⣿⣿⣿⢻⣿⣿⣿⣇⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢸⣧⠶⠋⠁⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣿⣿⣏⣿⣼⣿⣿⣿⡿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⡏⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠈⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢹⣿⣿⣿⣿⣿⣿⣿⠇⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⠇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⣠⣴⣶⠿⠟⠛⠂⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠘⢿⣿⣿⣿⣿⣿⣿⢰⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢠⣾⡿⠋⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢠⣿⣾⣿⣿⣙⣿⡇⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣧⣿⣿⣄⣀⣤⣀⣤⣤⣤⣤⣤⡀⠀⠀⠀⠀⠀⢠⣿⡟⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠘⣿⣿⣩⣭⣿⣿⡷⣿⣿⣿⣿⣿⠟⠛⢿⣟⠁⠈⢻⡆⠈⢿⡍⠙⣿⡍⠻⣯⠉⢻⣦⠀⠀⠀⠀⣸⡿⠀⠀⠀⠀⠀⣠⣴⡶⠆

⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⢿⣿⣿⣿⣿⣯⡓⣿⣿⣿⣿⢃⠆⠀⠈⣿⡆⠀⠈⣿⠀⢸⣷⠀⢸⣇⠀⢿⡇⠀⣿⣆⣀⣀⣀⣻⡇⠀⠀⠀⢀⣾⡟⠁⠀⠀

⢀⣀⣀⣀⣀⡀⠀⠀⠀⠀⠀⠀⠀⠀⠘⢿⣿⣿⣧⣽⠏⣿⣿⣿⡇⣾⡔⠀⠀⢸⣷⠀⠀⣿⠄⢸⣿⠀⢸⡟⠀⢸⡇⠀⣿⡟⠛⠛⠛⠛⠇⠀⠀⠀⣼⡿⠀⠀⠀⠀

⢠⣮⠿⢿⣭⡙⣦⠀⠀⠀⠀⠀⠀⠀⠀⠸⣿⣿⣿⣿⣾⠿⠛⠛⠉⣹⠁⠀⠀⢸⡿⠀⢰⣿⠀⣼⡇⠀⣼⠇⠀⣾⠃⠀⣿⡇⠀⢀⣀⡀⠀⠀⠀⠀⣿⡇⠀⠀⠀⠀

⠸⠁⠀⣠⡾⠷⠘⢧⣄⣀⣀⡀⠀⣀⣤⡶⠟⠛⠉⣁⣀⣀⣀⣀⣀⣿⠀⠀⠀⣸⡇⠀⣼⡏⢠⡿⠁⢠⡿⠀⣰⡟⠀⣼⡿⠿⠿⠿⠿⠿⠿⠷⢶⣦⣿⡇⠀⠀⠀⠀

⠀⠀⠞⢁⣤⡶⠀⠀⠀⠈⠉⠻⠾⠋⢁⣤⣴⣾⣿⣿⣿⣿⣿⣿⣿⣿⠀⠀⢠⣿⠃⣴⡿⢠⣿⣇⣤⣿⢁⣰⣟⣠⣾⠟⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠉⠁⠀⠀⠀⠀

⠀⠀⡰⠁⣸⠁⡴⠛⠛⢿⣦⡄⣠⣾⠟⢩⣾⣿⣿⣿⣿⣿⣿⣿⣿⣏⠀⢀⣿⣯⣾⣿⣷⠟⠉⠛⠛⠿⠟⠋⠛⠋⠁⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠰⣇⠰⣇⠀⠀⠀⠙⠿⠛⠁⣰⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣶⣿⣿⣿⠉⠉⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠈⠆⣸⡿⠀⠀⠀⠀⠀⠀⣿⡿⢸⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣿⣇⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⣀⣠⣄⣰⣋⣀⡀⠀⠀⠀⠀⠀⣿⠃⢸⣿⡿⣿⣿⣿⣿⢿⣿⣿⣿⣿⣏⢿⣿⡆⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠁⠉⠉⣿⠷⠤⢬⣷⣄⠀⠀⠀⠀⠀⢾⣿⠃⢿⣿⣿⣿⡾⣿⣿⠘⠿⠿⠄⠈⠉⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

⠀⠀⠀⠀⠀⠛⠒⠒⠚⠉⠁⠀⠀⠀⠀⠀⠈⠙⠀⠈⠻⠇⢿⡧⠈⠙⠃⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀⠀

Brilliant

Until you realise that most people browse on mobile, and it just looks like a mess.

ChatGPT ?

In this case no, just a good old fashioned "vulture emoji" google search and a copy paste.

It's cool Rob.

But what does the birdie say?

And the answer, of course, is kaaaaark

Good time to buy during the depths of this winter. Prices will be lower and it's an opportune time to grab a bargain.

You talking gummy bears there champ ?

If you don't get it then you will never become wealthy.

You always buy during the bottom of a downturn when no one wants a bar of anything.

By the time prices rise and people realise and look to buy a bargain they are too late.

Investment 101 champ.

Wrong! How do you know the bottom? You don't until it rises!

You buy as quickly into the rise as possible ...

The rise is obvious, the fall is obvious. The bottom is the transition!

I agree with him that this winter *could* be a good time to buy. But only with low ball offers. There’s no rush but if you can get success with a low ball offer (at least 30% below peak value), why not?

30% below peak is about the price from 2019. But at that time we thought houses were way overpriced and that was with interest rates around 4%.

Yip about august September could be near bottom.. unless the govt feck with the economy to much to save the bums

How dare you suggest anyone should consider buying this year... that sort of talk is blasphemy around here.

Sometimes you just have to get on with things eh.

But you can make life easier for yourself by being realistic about what you're selling and not going gangbusters on what you decide to buy next.

If you can do that and it still stacks up and you can back yourself to make it through a downturn (which is coming) then it's a case of doing your best to put your head down.

Well said GV 27.

It's not as simple as "oh don't buy". It's about strategy and planning.

No so. Buying this year is fine, just buy at a price you wont regret, and can actully afford.

That's the crux that sellers and speculators don't grasp. The debt affordability goal posts have moved and continue to erode with each OCR increase and overseas bank failure. Most simply cannot afford the ponzi like speculation of the last ten years. Those that have to sell will do so only into a market that buyers can actually afford. There will be a few extreme examples that avoid reality with a high price as trumped by Vested Interest funded Onreoof etc, but they will be the exception.

Note: the reason these banks are falling is because they cannot sell assets at their marked value to create funds to pay back depositors. Simply their loan books are marked at a overinflated valued, and a value unachievable in today's market. Sound familiar....?

Which NZ bank will wake up to this, and be the first one to start gassing its speculators....

I think it's difficult to 'buy at a price you won't regret' because that largely depends on what happens in future. If prices drop by a lot, you'll regret having overpaid. If they go up by a lot, you won't regret having bought at the price you did. I know heaps of people who bought late 2019/early 2020 who regretted it deeply for about 6 months when everyone was saying prices would fall by 15%, and then were very relieved. My two rules of thumb were: can I pay the mortgage reasonably comfortably assuming rates of 8% and a 25 year term (shorter than that if that will take you past retirement age). Can I afford rates of 10% on the actual term (30 years)? I am very pleased now that I set those limits rather than borrowing as much of the banks will let me, because it simply means that interest rate rises are just annoying instead of disastrous.

I remember 2015 November December the market dropped. Then went up again in 2016 before dropping off again and remaining stagnant. Until this covid frenzy buying. 30% + in some areas. See prices retreating 20% - 30% putting us approximately where we were with perhaps a slight increase of 2% - 5% . People who bought in 2020 breaking even.

As this Ponzi death-spiral accelerates, spare a thought for those with no means of escape, who will be suffering horribly....

.... I am of course referring to CWBW's basement boys...

a huge gap between the prices vendors are hoping for and the prices buyers are prepared to pay.

And there you have it....hope. I think saying many vendors are slow to see how much the market has changed and how big the falls are is a massive understatement and goes to show how brainwashed we have become to believe that "property is different".

For those not willing to accept reality the pain will be potentially severe, but they only have themselves to blame.

Yes, have a number of properties in a number of locations watchlisted on realesta.co.nz. They have a 'Notes' function and I've been recording the changes to method of sale and price over the past 3 months. Generally most properties are either tender or negotiation initially - changed to fixed-price/BEO marketing - asking prices gets lowered one or two times in small increments ($20K-$50K) - and then sellers revert to negotiation again.

Lots of withdrawals after no sale - sometimes re-listed as for rent.

It's not a good time to be a vendor.

It's not a good time to be a vendor.

Some would say it's a good time to be a buyer...

I notice that the media isn't really covering this at all like they did when when house prices were rising, causing FOMO. There are houses selling now under the RVs. I remember real estate agents saying that the RV has no reflection on the value of the house, but there are now more being sold where they are pointing out that it is selling under RV', like they have reversed their opinion and that the RV is a reflection of it's true value.

Not a good time at all. There seem to be quite a few vendors who are determined to get rid of their stock - many appear to be the ones who can afford to take a "hit" by accepting offers way below CV (most would've still made some gains assuming they purchased before COVID).

in general before xmas when I was reporting auctions each day, yes people who had owned for 10 years just taking market... now we starting to see actual losses go through, lower prices await

Indeed not a good time to be a "greedy" vendor. The whole price by speculation dangle is a waste of time in a falling market, and just delays sale and reduces what the vendor may actually get.

Witnessed RE Agent say to a room at an open home. 'Gotta - have a million bucks'. Everyone walked out, house withdrawn a few months later.

Same agent listed another property Sep 2022 for $1.059m. Later changed to $1.039, then $959 and finally landing on $899 before being removed from market Mar 23'.

At 3.5 x DTI average wage couples can probably only borrow 450k plus if they have managed to save 90k deposit 540k would be top of the range of purchase options so looks like bigger falls will be coming over next year in most places.

Average wage isn't the right benchmark for as long as there's deferred pent-up demand. It's the average wage of potential buyers.

Given your example infers a combined income of $130K which is under even the old FHB subsidy levels, I'd say that $700K as a FHB is probably optimal - but given how expensive new builds and supplies in NZ are, the question then becomes "What sort of home are you really likely to get for $700K?".

You'll have a small cohort of owners who need to sell at any given time, but an increasing amount of vendors will just sit on the sidelines if prices dip below a sustainable level. Once the total number of sales slows down, charting a direction becomes much harder.

This is true, but as the top earners of the potential buyers purchase, they are removed from the pool, and the average income of potential buyers drops... leaving the average income of all potential buyers (not just the high earners) the value to watch.

You will see an increasing number of vendors sitting on the sidelines (those who owe nothing or little), but if these are outnumbered by those who need to sell (those who owe a lot/have not held for long) then their presence is largely meaningless - and as time drags on and more need to sell than want to sell, more of those who want to sell become need to sell.

Indeed. As those that need to sell take ever lower prices, and the banks and valuation community will start noting that trend. Any marginal seller on the sidelines starts making paper capital losses as prices erode. This mirrors capital gains, in that any loss/gain is speculative based on market.

Most of the population have no chance of purchasing a property from scratch in most of the main areas. You would have to be in top 5% of earners to by a average home in Auckland the market is crashing because people are starting to understand the million dollar mortgage has climbed up to 1600 per week leaving them very little to pay other bill and food. The shit has hit the fan for many selling at a reduced rate is only option this is going to take a number of years as negative equity becomes the norm for anyone who purchased from 2015 onwards

They could move to Rotorua. Prices are affordable in the provinces.

There will be any number of vendors; an increasing number each day as variable continue to go against them, that have no choice but to ask 'optimistic' prices to quit their holdings.

Many will reach the point where a sale will not discharge the debt owed, and so the lender will not allow them to sell unless they top up the missing money.

Only those will positive equity; many from decades past, will be able to lower their prices to sell. And as time passes, they will, compounding the problem for those trapped with their properties and associated debt.

It's times like those coming where it will at least a consolation to look at the rooms that surround you and say "Ah, well. At least I like living here!"

typically a lot of good family homes come off the market here, they will pay mortgage keep jobs....... Sure some may be forced sellers but until that starts sit and wait

Vendors will not wish to immediately discount their offering in the market, the hope being that their offering is something that a buyer might fall in love with and pay premium, or over value. Not all buyers need bank finance, so while interest rates cool the market their influence on price is not absolute. Attractive property in high demand areas should hold price while property in areas of lower demand ones with issues or unattractive are where one might find bargains.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.