Prime Minister Jacinda Ardern says she would like to see small increases in houses prices, acknowledging most people “expect” the value of their most valuable asset to keep rising.

Her comments come as the Salvation Army warns: “It is likely that without substantial changes in housing policy New Zealand will experience the equivalent of the intergenerational scarring, which resulted from the labour market reforms in the 1980s.”

Asked by interest.co.nz (see video below) whether “sustained moderation” of house prices was still the government’s goal, Ardern said: “Yes. We don’t want to see the significant increases; these huge jumps in house price growth.

“It means it becomes out of reach for people as their incomes or their wage growth doesn’t keep pace.”

Asked to explain why a fall in prices would be bad, Ardern said: “What we’ve simply expressed here is that the growth that we’ve seen is unsustainable. So, if anything, it is much more sustainable to have those much smaller increases. I think people expect that you see that in the market.

“What we also accept is that for most New Zealanders, their house is their most significant asset… A significant crash in the housing market - that impacts people’s most significant asset.”

Put to her that people who invest in shares, for example, don’t always expect the value of that asset to go up, so why should it be different for housing? Ardern responded: “This gets to the heart of the issue of why so many New Zealanders turn to the housing market.”

Ardern then walked off stage, having previously signalled she was taking last questions at her post-Cabinet press conference.

Negative equity concerns

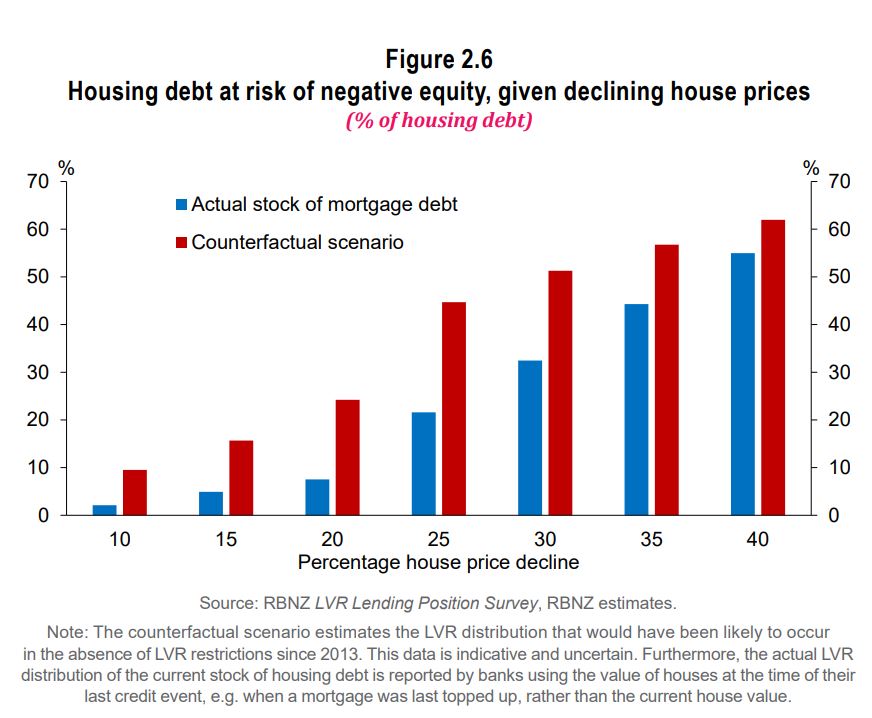

The Reserve Bank (RBNZ), in its May Financial Stability Report, said a 10% decline in house prices would put 2.1% of the country’s mortgage debt in negative equity. A 20% decline would bump this portion up to 7.5%, while a 30% decline in prices would put 32.4% of mortgage debt in negative equity.

The RBNZ, which at the time expected house prices to fall, said the introduction of loan-to-value ratio restrictions in 2013 helped make the financial system more stable.

“Household balance sheets are generally now able to absorb a greater decline in house prices without going into negative equity,” the RBNZ said.

“This leaves most borrowers in a position where they would be able to restructure debt to withstand temporary income losses. As a result, there will be fewer non-performing housing loans and fewer mortgagee sales, which reduces the chance of a negative feedback loop causing a more severe decline in house prices.”

The median house price nationally has increased by around $100,000 since the RBNZ made these comments in May.

Median price - REINZ

Select chart tabs

Finance Minister Grant Robertson last week told interest.co.nz he hadn’t considered what the net effect of a fall in house prices would be.

In other words, whether more people would benefit long-term by houses being cheaper than they are now, than those who would suffer by having to sell for less than they bought for, or those who would suffer from a potential reduction in business and consumer sentiment.

Ardern's popularity continues to soar

According to the latest 1 News-Colmar Brunton poll (conducted between November 28 and December 2), Labour is up seven percentage points since the last poll on October 15, with 53% support, while National is down six percentage points to 25%.

Ardern is also up three points in the preferred prime minister ranks to 58%.

See Ardern's comments in the RNZ video below:

242 Comments

Coward

She's broken already - 4 years. Wow...disappointing.

Despite that her popularity is increasing, she must be doing something right at least

In a post truth world that isn't necessarily a true statement (lol)

People/voters believe it so that's what counts right

Good grief. How can you possibly equate popular with right? In politics, if they are the same, it is just a fluky coincidence.

She knows the NZ economy is a one trick pony. What's more worrying is this shows the government has zero ideas to fix that.

Sounds like she is adopting the prevailing thought in Wellington, that wealth transfers from the young workers and savers must continue in order to prop up older folks' wealth.

It's basic intergenerational theft at this point. Using multitudinous policy to inflate and protect prices of a given investment. Why should young Kiwis be expected to respect the idea they shouldn't take wealth from others when they want that wealth?

Jacinda will do anything to be popular.

I heard this the other night on 'The Crown' (of all things)..and it reminded me of her:

You have no enemies, you say?

Alas! my friend, the boast is poor;

He who has mingled in the fray

Of duty, that the brave endure,

Must have made foes! If you have none,

Small is the work that you have done.

You’ve hit no traitor on the hip,

You’ve dashed no cup from perjured lip,

You’ve never turned the wrong to right,

You’ve been a coward in the fight.

- “You Have No Enemies” Charles Mackay (1814-1889)

Jacinda is quite possibly echoing the view of the masses.

Sensible enough statement from the PM.

TTP

More like a betrayal of her rhetoric and (so called) principles.

Amazing how power goes to their heads.

Yeah I was going to say its a lack of principles....she's broken under the pressure.

She's loving the power, money and status.

Phoney.

Wonder if this is going to be the new Labour party motto now on housing. If it is, its completely pathetic given what they said for years in opposition, and now with the news that is coming out from the likes of the Salvation Army around the suffering that is happening out there because of house prices/rents.

Well, I voted Green and may never vote Labour again.

It was so liberating to realise Labour are as vested in the status quo as National.

Yip, I've gone from National, to Labour and now Green party over the last 10 years. Me 10 years ago voting for a Green party - not even a consideration (nor did I think I ever would). But how things change - I would have voted Top if I thought they had a chance of breaking 5%. Realised a National/Labour vote would be wasted as it was going to be more of the same regardless.

Can anyone really vote for the $12million green school man?

No one said he or they are perfect, or anywhere near it...

So instead of voting for TOP because you thought it a wasted vote....you voted for the same old failed parties (a wasted vote for sure) ??!!!!

Therein lies the problem...you are part of it.

Totally agree. people who vote for labour or National and them complain about housing, should just blame themselves.

I voted for TOP.

I have thought this for 25 years (since I started voting) now choose the left or the right they are the same thing with a slightly different spin. The whole 2 party system is a farce made so people think they have a say. We need a transferable voting system, and equal public funding (no private contributions) for political campaigning. Ideas and policies should be what decide the elections not the size of the wallets of the people who fund you.

No need, just vote different (TOP). There are likely 10s of thousands of people just like IO above, caught in the same myth promoted by the major two parties that if you vote for a smaller party, they won't get in. What they fail to tell you is that if you vote for them, nothing will change. In fact if you vote for them, things will get significantly worse.

Until the idiotic voting public understand this through repeatedly voting in caretaker governments, nothing will change. So Ardern is EXACTLY right to blame people for voting her and Labour in again with policies to do absolutely nothing.

Indeed - wasted vote is voting for any party that doesn't align with your beliefs the most. Waste of democracy.

As unpopular as it might be, I firmly believe that if a party gets enough of the vote to get one seat in parliament, then they should get that seat. (Even though that would have given Advance one seat this election.) People would be much more likely to vote for the minor parties if they actually stood a decent chance of making it into parliament, and there would be much less wasted vote.

It would also give the minor parties a platform to build on and give them a tiny bit more visibility and traction with some of their policies.

This is not necessarily good even if that were the case, which in this case is the exact opposite.

Yet in a Collar Brunton Poll released yesterday 75% of people suggested that prices should drop to allow for improved affordability.

So if the majority of people don't want what Ardern says they do...whose need is being catered to?

I agree. In particular I think that last comment ('heart of the issue') was more like 'yep houses that only go up is a total farce, but I've had too much pressure put on my to say so'. Her body language and quick exit was indicating the cynicism of the whole thing.

She was not elected on a platform of "small price increases".

She should resign.

Yes she WAS! PM Ardern never said publicly she wanted house prices to decrease. Rather she said the opposite - did you not watch any of the leaders debates?

Judith Collins was the one saying house prices needed to come down 'in some areas'. I voted for TOP, but geez, this is nothing new.

Small or zero price increases would be the best/ least bad thing possible.

It is not what is happening - not least due to Lab tinkering with RBNZ charter . Lip service .

For who? Definitely not for people wanting to buy a house and waiting the next 20 years so they can reasonably afford one.

"Least bad" in that we're still transferring significant amounts of wealth from younger Kiwi workers and savers to asset holders...but they need to trust us that it's for their best interests and not object.

Soft serve in a waffle cone. Nice gleaming smile though, let's not get too serious.

Best comment I've seen in a while, cheers middleman, gave me a laugh.

Fantastic comment

She's fast heading toward becoming John Key 2.0 if she doesn't find some resolve.

Nope. I'm a home owner and I wouldn't care if prices dropped.

It is no longer a free market.

I have a feeling more people would benefit from house prices falling than the number that get hurt by that happening.

Yes I agree. I'm sure someone will probably point out that you're not obliged to sell your house for full going price, ignoring the fact that in order to buy "like for like" you must sell at market rate.

Note that very few markets are entirely free.......

Market imperfections (monopoly elements) are common/widespread and provide justification for regulatory intervention. In fact, that's a key role for government.

TTP

Fell in Ireland from 2007 (approx -50%), cleared out the dead wood, things got back to normal quicker than you’d of thought, no one starved, it allowed FHB to buy a house and scared off the investors and prospectors.

Interestingly the Govt had supported high prices in the 2000’s - similar to here.

Ireland was a odd one. They built heaps of houses and had an over supply issue. Speculation was rife. But the crash was mostly caused by a jump in interest rates as Ireland has no control over it's own rates or currency.

While houses dropped employment fell through the floor so nobody could buy them. The banks went to the wall and needed to be bailed out, terms of the bail out meant very strict lending.

Vulture funds swooped in and picked up thousands of developments for cents on the euro, now rents are through the roof and prices, proportionally, as high as here. Almost.

The speculation on housing and it's treatment as a commodity just like gold etc needs to be stopped. Ireland might not have had as bad a crash had they done something. And the Western world might not have the issue now.

At least Ireland has 42% capital gains and got lots of infrastructure out of the boom on the way up.

I think the vast majority of home owners feel the same way as you, as they see the pain and frustration this is causing in relatives and friends. Furthermore, a 20-30% drop would mean bringing prices back just a few years, and the vast majority of home owners would not even get close to negative equity, even if that happens the positive effects overweight the negatives.

I see the pain it causes my nieces and nephews and feel terrible at how exploitative we in New Zealand have been, freely living up large off the back of debt we have felt free to create and foist upon them, transferring their wealth to us. What we are doing to New Zealand's younger generations to enjoy our wealth in the moment is obscene.

As a home owner and a landlord I second that, in fact I would prefer it. I would much rather live in a society that people could own their own home.

I wish people would stop assuming what people want. I have never been asked that question by any government. If house prices went down I would still owe just as much money.

If my house went down in value by $100k, & then I sold to move somewhere else; well then logically the next house has also gone down by $100k. So for the life of my I can't why that should cause me to melt down.

It becomes a bit of a race to the bottom. Confidence drops, consumption drops, some people default and banks can't recoup the loans, then the banks stop lending to business, some businesses go bust, job losses, more drop in consumption, and so it continues until there's is a cash injection somewhere or it naturally reaches stability. When the house prices go down, banks won't lend to many but the richest few, if at all. It's a sh*t time all around.

Just f%$^ off Ardern.

Michael Joseph Savage my ass.

GOOD LUCK~!! - Labour are polling better than their result on election night.

SEE Video Below:

https://www.tvnz.co.nz/one-news/new-zealand/1-news-colmar-brunton-poll-…

Checked the homes website and was absolutely shocked at my rental valuation. Up 15% since August and 65% since purchase in 2017.

Got a valuation by CoreLogic which was 2% higher than homes. Went straight to another bank, drew it down to 20% equity and threw it all on the family home. Happy days.

We're up 80% over that same timeframe, $12k in the last 2 weeks according to Core Logic. I've just handed in my resignation at work.

What, no boat or Tesla?

Think tank

Up 65% since 2017. Well done - proved to be the right choice not only financially but also for family security.

Nzdan you are another who bought when many were scoffing as to the future of the market.

Mmm . . . so while the most common rhetoric on this site was “bubble burst”, “bubble burst” you both choose differently and now reaping the benefit.

Those who claimed bubble burst made a choice based on that and chose to continue to rent. A number who did so are now not in a position to moan; sorry not much sympathy as it was your decision so you need to live with it.

We all make choices that don’t work out; however one accepts it, wears it, and don’t going around griping and blame shifting but get on with it.

I note a few in that camp have since disappeared. I think it was Foreign Buyer claiming six months ago anyone considering buying was “officially stoopied” - couldn’t have told him otherwise and scoffed at those who did. Court Jester has continually posted for most of the year about being able to buy but waiting for falling prices.

To those who are now working towards being a FHB - yes things are very tough. I really do hope prices do flatten next year (current rates not sustainable), interest rates fall a little more, and affordability improves.

You cannot deduct the interest as an expense doing it this way - your intent is wrong as as you'reclearly doing this for tax purposes. If IRD find out (and they've been putting a lot of effort into this area recently), you'll have some very unpleasant explaining to do. You should get some accounting advice. My 2c.

I’m not bothered about maximising my interest deductibility, I was more happy to pay my personal mortgage off 22 years early. Why would IRD come after me for pulling equity from my rental? I’m not claiming that portion of interest as an expense, the rent just covers it.

And there ladies and gentlemen is why investing in property is a winner for the foreseeable future. No politician wants to touch the problem because in reality, most of us are loving it.

Jacinda has a house in Auckland, she's 'lovin it' - top it off with a cheeseburger love.

Yep.

Including Jacinda. Her Auckland home will be soaring in value. And as a phoney 'chardonnay socialist', its right up her alley

Phoney.

Housing is such a safe bet now.

- The economy needs it (no matter how flawed that model may be)

- The people need it (to feel "confident" and keep up the spending)

- The politicians need it for the votes

- The media needs it to keep the newspaper sales up by writing about housing.

Yes, upsize that combo!

lol :)

How long before it gets beyond even the ability of the Reverse Bank of New Zealand to sustain and inflate, though? Assuming they cannot print money / transfer wealth in unlimited amounts.

No politician wants to touch the problem because in reality, most of us are loving it.

Not most - ~ two thirds of households have no mortgage according to the RBNZ - higher present values of future liability costs associated with rising asset prices do little to enhance the buying power of savings and wages as bank deposit interest rates fall.

Come on, that's overly technical.

Mortgage or no mortgage, most owners love to see their house values increasing.

Not me - maintenance costs, council rates and insurance rates rise without any commensurate cash flow increase from my owner occupied home. In fact no income at all, in my case.

And I have to double my capital deposit amount every time the RBNZ cuts interest rates in half (five times since 2008) to generate the same income to meet those mentioned rising present value liability cash flows. Don't get me started on rising every day costs. Supermarket product package weights are reducing while the prices remain the same at best.

How long do you think this is sustainable for?

I think most home owners without mortgages and not in high paying jobs are running on empty and just getting by with state subsidies, if at all.

It's telling that banks extend ~60 % of their lending to the already wealthy one third of households to speculate in the residential property market.

Right - I guess that falls within what I'm seeing with the people I interact with. Makes me wonder, how those same people would ever afford their homes now if they were 20-30 years younger.

Indeed - wages have not kept up due to the pressures of "free trade" to level global labour costs - but the FIRE industry seems above government regulation due to oppressive corporate protection clauses written into trade agreements, hence the majority are financialised into serfdom as are elderly savers without recourse other than to down size to an out of area neighbourhood absent family ties.

I've had a conversation with people and they say 'well perhaps house prices just rise at the same rate (%) as wages now'. And I say, that's impossible because house prices are 10x the average wage in NZ.

2% rise on average $70,000 wage = $1,400 p/a

2% rise on a average NZ $750,000 house = $15,000 p/a

That difference needs to be covered by falling interest rates and a future debt obligation. Question becomes then, how long can we sustain this/that before something gives? When people invest based on capital gains only - I look at those numbers above and think at some point this has to come undone.

End up with a Stalemate as we run out of people who can afford the asking prices, investors included. Capital gains become uncertain, so there's a focus on yield. If rents need to exceed people's ability to pay to generate a yield then uh oh. Landlords could remove maximum occupancy clauses from their tenancy agreements to bring in more income earners, but as the average rental occupancy rate rises there's a smaller pool of renters for other properties.

Oh we can sustain it for a bit more. Average standalone house prices in Vancouver are 1.5mil CAD. When I was living there 10 years ago they were 800K and people were making exactly this same comment as you...

I.O.. agree that it does have to come undone in the end but with the powers that be so determined to throw the kitchen sink at propping it all up it may well be a number of years. With Adern's mindset and the extreme likelihood that mass migration resumes next year, demand for housing will massively outstrip supply all but assuring house prices and rents remain extortionately high for a while yet.

By far the best thing Adern could have done to assist the poor and address racial inequality would have been to take steps to cool property inflation and rental prices but she has done the exact opposite. Maybe she thinks inconsequential acts like wearing traditional earrings and giving Neve a Maori middle name shows she really cares. I just hope the victims of her crimes now understand how negatively she is affecting their future and how what she says she stands for is so disjointed from where she is leading us. Guess I will need to buy another house so both my kids are on the right side of the great social divide she seems so intent on creating.

It's possible even with current settings.

For a start there are normally two wage earners buying a house. And secondly it's the deposit that's the main problem for most FHB.

Taking that into account here's a different set of numbers:

2% rise on average $70,000 = $1,400 p/a. x2 = $2,800 p/a

2% rise on average $750,000 house = $15,000. @ 20% = $3,000 p/a. or @ 10% = $1,500 p/a

Thirdly, the market is not only made up of average income earners buying average houses.

Are you able to explain your numbers?

That's based on your number above but modified for 2 incomes and looking at the increase in house deposit required rather than total house price.

First wage rises are more than eaten up by cost of living increases. Second applying the LVR nicely reduces amount saved but does nothing to reduce the amount you actually repay, if LVR is 0 then obviously every body could just go out and buy billion dollar homes.

Except wage rises are taxed, and 70k is the top tax bracket - so that's actually $1848 a year. So even two earners, both in the top tax bracket, will be going backwards when trying to save for a 20% deposit if both houses and wages go up at 2% a year. If they are renting, then it's a pretty sure bet that rent increases will gobble up enough of the extra that they'll even be going backwards in terms of saving for a 10% deposit.

al123... and it gets so much worse if a young couple feel they can take liberties such as starting a family while still renting.

The use of equity to buy more houses just make me think of a ponzi scheme - then once your in it, you become an advocate for it, trying to drag more people in. i.e. like what you see with a real life ponzi!

"...maintenance costs, rates and insurance rates rise..."

It's land values that are increasing. Why would that affect maintenance or insurance costs? It shouldn't affect rates either unless your place is increasing faster than other properties.

My residential property has seen the Land Value rise from $210,000, as of Sep 2001 to $495,000, as of Sep 2019.

The Value of Improvements has risen from $165,000 to $375,000 over the same time frame.

My council assesses my current $4,128.00 annual rates bill on total capital value - the sum of land an improvement values.

My house insurance is estimated on a much greater value than the house improvements level, hence these costs have risen from $145 back in 1999 to near $1,500.00 today.

$ 8000,00 to paint the roof last summer, painted the whole house, including the roof and garage for $6.000 in 1999.

I could go on.

"$ 8000,00 to paint the roof last summer, painted the whole house, including the roof and garage for $6.000 in 1999."

Yes but that's due to general inflation of goods and services, not the price of your house.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax.

https://www.grantspub.com/files/presentations/FISHERGRANTSREMARKS15MAR1…

{kind=link}

"$8,000 to paint the roof" ? What do you own = Forsyth Barr Stadium?

Returned to NZ this year. Couldn't believe how expensive insurance and rates had become. My rates alone are almost $100 per week (already increased $100PA in first 6 months). NZ has become a country that is a great place to live...as long as you have plenty of money. Aotearoa 2020 = The land of the K shaped economy.

Rates will only go up.

Exactly. How is it academics don't understand this? Or do they understand it, but refuse to admit and address it.

I have never experienced a market/financial/monetary policy failure of this magnitude for which it appears an academic taboo to mention regulatory options/fixes.

Talk about cloistered.

Why rock the boat? You get paid no matter what. Lockdown poverty is for other people.

The narrative isn't driven by academics. It's driven by bank economists, Bindi and Ashley, and the front pages of the Herald.

You are right there, but academia - where alternative ideas and arguments ought to come from - is sitting (at best) sniping platitudes from the sidelines about poverty and intergenerational inequity - but not going so far as to propose a paradigm shift. The best analysis and voice I see on this subject comes from the Salvation Army, e.g.,

https://www.rnz.co.nz/news/national/432256/salvation-army-warns-of-soci…

Wow, well done Jenee!

No need to waste time lobbying for CGT or LVR's this is generational war, all plausible deniability has been removed.

So Jacinda and Labour are fine with 30 year to intergeneration mortgages and spending our entire working lives paying of the loan, and that's for the well off. As long as the retiring boomers can get cashed out.

Pretty sure PM Ardern isn't saying anything new here. The above video is actually from last week. Everybody is acting as if this is a new revelation.

I think a lot of people are hypnotized by the waffle PM Ardern's speaks. Jenee seems to be bravely breaking the spell for many.

We all "knew" this was government policy. I don't think it has ever been stated this explicitly by a PM, have I missed it? All the stuff about the RMA, Kiwi Build and CGT was just for show. Along with any plan to tackle child poverty and any number of her other welfare promises.

The last comment really gets me, (I could be reading way to much into this but listen to it in the video): “This gets to the heart of the issue of why so many New Zealanders turn to the housing market.”

She is absolutely sure of this as a long-standing fact and the only way she could be this sure is if it was non-partisan policy agreed to with all parties with an open secret. No worries about investment in the productive economy either.

Everyone under 30 should be out in the streets setting stuff on fire.

Thats a stoopid thing to say... get arrested for arson and ruin all prospects

If a single person burns down a building they're a criminal, if 10,000 people burn it down, they're revolutionaries.

Does interest have 10,000 DGMs though? According to the article above, the population at large appear to be happy with the status quo.

Yep, the youth of NZ are soft as a pillow

Honestly though, once you feel like the system and your government have betrayed you, social cooperation and etiquette no longer feel important. This is a disaster.

Well, I would not blame them if they started with pilfering or vandalising real estate hoardings with slogans. Folk do it creatively at election time, they could do it creatively to commentate New Zealand's biggest welfare wealth transfer scheme.

tim

Pathetic.

Blame it all on boomers - unfortunately it isn’t boomers who have purchased homes in the past decade; they bought 30 years or so ago.

If you read the comments FHB like thinktank and Nzdan have done very well (as they post above) in the past three years.

Time you got off your chuff. Record numbers of FHB since RBNZ data published in 2014 - currently over twice the rate back then.

Start wearing your big boy pants.

The boomers are about to retire and be sellers. The high prices benefit them the most. Where's the blame they are just the privileged voting block that get to be the centre.

While I have got you here: what do you think mortgage rates will be in 5, 10 and 15 years time? higher and lower that what they are now? FHB might feel good as prices go up now but they won't be selling and they will have to pay the tax on all things the government does to try to keep this afloat. Do you seriously believe our house buyer sentiment is going to allow Japanification without the house price crash?

Yes generational war is gross over simplification but for sake of comment length I though it was appropriate.

tim

"The boomers are about to retire and be sellers."

Rubbish; most who retire keep the house they are in until they look to heading for the rest home - only 7% apparently - whereas 93% head directly for the funeral palour and aren't too concerned about the sale of the property.

Mortgage rates in 5, 10 years time - well anybody who says so is guessing.

It is for this reason I always advocate (sadly having to be repetitive) that FHB need to be prudent and pay down the debt as quickly as possible. The other day I had to really spell out to somebody (Nifty I think) what this meant and he really couldn't grasp the concept.

As to the risk of increasing mortgage rates, be prudent and pay that debt down but be aware that is only one potential risk. Other risk factors of equal importance are related to jobs (e.g. redundancy, pay cut, down graded), family (e.g. marital issues), personal (e.g. accident), other (e.g. extreme natural event, problem with house such as leaky home) and give me another couple of minutes and I will come up with more.

Personally I am of the view RBNZ (as much as they are the whipping boy ahead of boomers) can not afford interest rates to go that high and suddenly to create widespread mortgagee sales. Something I thought you would have learnt in the past decade - and certainly in the past six months - is that RBNZ (and now Jacinda) see stable house prices are a basis of a stable economy.

So I would be prudent and be worrying about some of those other factors rather than mortgage rates.

Mortgage rates are the least of your problems.

Sleep tight.

Cheers

If your not going to speculate on interest rates don't speculate on house prices.

You missed the point, interest rates determine almost all of what wage multiple you get when selling your house when they are this expensive. Sure you can bring up all the transient deviations from this you want.

Unless you want to predict a deep negative OCR in 10 years there be no significant house price gains outside of inflation from sometime next year.

If no ones selling no one cares about the price. What's the source for your retirement living stats, I don't believe them. And with savings so low some won't have a choice but to downsize or carry on working.

I beg to differ.. And due to your childish emotional outburst I can only assume that you identify as a boomer. We sold our family home last week. 9 offers- 8 of those unconditional. Only one from a family looking to buy a home for themselves. The rest were from 'boomer' investors not getting any interest on their savings. And being prepared to buy at 70% over valuation.. desperate times out there, and people are being irrational with their purchases. We are moving areas and buying in the same market, so despite realising a high price for our home we will be paying highly for our next. But I feel sorry for the young trying to secure a home for themselves. It's alarming to witness how selfish housing investors (specuvestors) are. I refuse to buy housing as an investment because I care about the country we live in, and the future of current and future generations. There are many innovative businesses to support and invest in in NZ if you do your research- and a lot of them being run by these 'lazy, entitled millennials' everyone complains about. Their emerging world is the result of what has been created before them, so have some compassion. It seems the 'give each other a hand up' New Zealand that I grew up in has turned into has turned into an 'all for one and all for me' scenario. Best of luck to all of you reading this who just want to buy a home to live in, and may this unsustainable market shift in your favour.

That is why the RB's policy on interest rates is foolish. It is not encouraging businesses to start up - it is just painting boomers into a corner of having to buy another house to get any meaningful return on their money.

The value of my Onehunga townhouse might have gone up 10% in the last year, but the amount of homeless on the streets and in your face aggro is also increasing.

I would happily trade in less property value gain for a more equal and happier society.

Indeed - did you see the botched "money scramble" in Aotea Square. A sad indictment of a society fraying at the edges. I saw desperate people becoming disappointed then angry. NZ is turning into a powder keg thanks to Labours failed policies. It'll blow back on asset owners in one form or another. NZ tends to do nothing then overreact.

Yeah, disgrace. We are really degenerating.

I was sitting in Carl's Jr beside Aotea Square, having a burger about to go to the RBNZ Ballet and group after group of folk came in with huge handfuls of fake five-dollar notes trying to spend it. It looked counterfeit, they looked a bit bewildered but you could see it was a recipe for disaster.. Red band guards had to come out because there were 2,500 people and it almost turned into a full-blown riot. People had travelled up from Levin, Palmerston North and all over to try and get free cash... It was actually sad to see people sitting on steps at surrounding buildings with coy smiles as they counted out their fake $5 notes like they either couldn't tell they fake or were in still hoping they could spend it..... however, the ballet was great.

Bravo, great comment! There is an imbalance.

Mine has gone up too and it's weird that a 1960s batch is worth 660k now.

Are Nats voters finding it hard to hate Jacinda now? Is this the new Key?

Definitely the new Key. Who was the new Helen (she did very little about housing and hugely pumped immigration when in power).

Red or Blue they all have their snouts in the food!!!

Nifty... she needs to replace that Savage photo in her office with one of John Key.

The REINZ index is looking more and more like the Mt Everest elevation profile by the month! Anyone else getting hypoxia yet?

It's this crap that increasing the fomo for FHB and accentuates the problem. I have been good at resisting it however now she's come out with this shallow shit I am definitely reconsidering. Thanks Jenee for asking the questions MSM continually fail to do. Too bad I've never seen her answer a question directly in my life.

'she would like to see small increases in houses prices,'

er um, ok then, When? she is the PM after all.

Just watched the video. Can't believe Jacinda's dismissive body language at the end. In her mind, nothing to see here folks. Great questions Jenee. Thank you for asking.

After spending years bemoaning neoliberalism and how it screwed over a generation (apparently), Ardern is presiding, like Lange, over changes to New Zealand that will resound for decades to come. Whereas Lange did what was needed, with bad results for many, Ardern is doing nothing, with bad results for many. Lange 2.0, not Micky Savage 2.0

I think she has many similarities with another Labour phoney and one of her idols, Tony Blair

hahahahahahahahhahaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaaahahahah

hahahahah

Democracy?

Politician is a job not leader of any sorts.

Hahaha

Oh zingmo, you really come across as quite the fool in this comments section.

Can’t you see the PM is being openly criticised here because we are freely able to do so?

I dare you to criticise your beloved leader....and who will come to your aid when you’ve “disappeared”?

Yeah, try sending Emperor Xi a Pooh Bear toy and see how fast you land up strapped to a Tiger Chair in a windlowless room.....

Ardern and Robertson need to realise that wishing for something don't make it happen. Clueless.

Have you observed how the network news on 1 and 3 have dropped their sharemarket and exchange rates reports a while ago. They still have plenty of housing updates and reports from open homes and auctions. What does that say??

Our tv gave up the ghost 3 weeks ago. Soooooo not missing it or the 'news' which I only watched sporadically.

Got Spark Sport and can watch my beloved cricket and English football on the laptop.

Not missing much... we been enjoying Freeview on demand through smart TV... and sky sport go

She stands to openly profit personally from making these statements as speculators feed on it. This stinks of corruption.

Audaxes, do you think owning gold/miners is a good defence against the risk of falling real prices over the next several years?

Think of gold as a currency. What are central banks doing to their currencies?

What a stupid woman.

Thanks for asking these important questions, Jenée. The PM's answers made the government's stand very clear. Keep up the good job.

Classic. Ask her a few questions about government policy and she walks off. She is so lucky with the opposition she has. They could have a field day with this, but have probably not even noticed the opportunity to show her for what she is.

U know very well National MP's own lots of homes too.

Indeed. National supported this very problem as long as they could including through denying the existence of a housing crisis they campaigned on. They are the fire to Labour's frying pan. Everyone knows they cannot be trusted on housing and will only actively make things worse.

What the actual f*** did I just watch?

Wouldn't surprise me if she thinks cryptocurrency is a scam and wants the price to crash (because most people expect it).

Are wages going to rise in New Zealand? Peak worker productivity was 2012.

Remember Jacinda said no pay rises in the public sector because of COVID so..

No, you now have to work a full time job and a part time job in the weekend to keep up. You get 10 sick days though...

Many government departments have unlimited sick leave but they’ll probably need it..

Every time she performs her schtick on camera the more it's apparent that she has fundamental problems with numeracy and the country is being irreparably harmed by it.

Totally clueless and out of her depth. Her body language speaks volumes.

I have said it before, she has above average intelligence, but not much above. And clearly lacking in numeracy.

Absolutely fantastic final question and appalling answer from PM. What she is saying is that her Govt will continue to incentivise people to put all their eggs in the housing basket and thereby discourage productive investment making us all poorer for it. I thought John Key was useless; now we have a PM who is doing her damnedest to outdo him. Haere atu kotiro! He koretake koe!

I will say this, at least Key didn't pretend to care deeply about the have nots.

You have got my upvote on this comment. Very true.

Ae e hoa. Better to have an honest villian than a mendacious saint.

C S Lewis' classic quote seems apropos here:

Of all tyrannies, a tyranny sincerely exercised for the good of its victim may be the most oppressive. It may be better to live under robber barons than under omnipotent moral busybodies. The robber baron’s cruelty may sometimes sleep, his cupidity may at some point be satiated, but those who torment us for our own good will torment us without end for they do so with the approval of their own conscience.

For Pete's sake ardern you came in on the back of containing immigration and house prices you are a waste of a political leader when now you just speak from your own self interested and self satisfied position.

Let them eat cake!

vegan cake

Gosh, she needs some serious help on this one.

My suggestion for the PM:

"We are not as concerned about house price rises as we are about rent prices increases, and rent costs more generally. Owner-occupiers of housing are benefitting from the low interest rate environment of today - in many cases lowering the cost of their home ownership. Non-asset owners, or renters are not receiving any of the benefit of today's low mortgage interest rate environment. If rents are regulated to ensure they are affordable, we could solve both issues by addressing only the buy-to-let end of the housing market".

Every single time she's repeated this mantra with not wanting prices to go down she's sending a very clear message that they won't let that happen under any circumstances effectively pushing the bubble even further and throwing under the bus the same young and poor families that brought them into power in the first place. The utter lack of empathy Mrs. Arden shows with the millions that are suffering due to the housing hyperinflation caused by both Labour and National governments is totally unacceptable for a leader that built a reputation out of the exact opposite. Wages won't catch up unless we immediately BAN investment in housing, period, must be done and must be done now.

Wages won't catch up unless we immediately BAN investment in housing

Real wages have been falling for a long time because of monetary debasement.

One slowing car can overtake another one slowing down slightly faster.

Thanks Jenee for asking the hard questions and keep our government accountable. I think your last question really got her and showed me that she is just a politician and not a leader.

I'm not angry, just disappointed........

..... and angry...

This year 20%, hopefully it's steady, modest every 20% for 2021-2025 - our country debt is still as not as large as other big countries, so clearly more provision to grow here, more stimulus & permanent subsidy are needed. As this year we can see the result of large corporation profit/dividend to share holders, Govt surplus. Which means? the more of QE/LSAP from RBNZ, the quick implementation of negative OCR, keep the LVR lid, more opening of FLPs into building society, credit union & toward supply of 'housing development' are the key here. Steadfast NZ

Kiwis jealous sentiment said, if they move to OZ is to bring up the IQ level for both countries. yea, about that my question is why OZ supplying the banks here, the grocery too.. and why for more specialisation of healthcare training is also in OZ? - no wonder why Rutherford have to leave and many other for generations, one cannot expect too much from IQ and EQ from picky sided moderation vested interest.. ala Kiwi. K/dragger jungle bunch

New Zealanders exhibit the Dunning–Kruger effect a lot imo — a cognitive bias in which people with low ability at a task overestimate their ability.

Two points, the market is always right. Can't be adjusted like a big Govt thermostat.

And the more our currency gets debased, the greater the value will show in real assets. Like property etc.

"Ardern then walked off stage, having previously signalled she was taking last questions at her post-Cabinet press conference." Hmm! What does the body language say?

I can’t keep blaming nine years of National’s neglect, now that we are into year four of our Government. Kiwibuild was a disaster but the people love me anyway. I don’t want my house value to decrease so the first homebuyers can shift for themselves. This is way too complex for my caucus to solve. I know... let’s declare a climate emergency and focus attention there.

it says she does'nt have a clue. But some of us knew that before the election. So good luck to those FHB's looks like you need borrow just a little bit more..and a little bit more...etc etc etc

Woah. Good leaders are supposed to build consensus, not just take consensus.

This in a nutshell is why house prices will continue to rise. The government will continue to ensure they never fall, negative gearing will mean any increase in prices will mean profit can be multiplied out, Capital Gains Tax will do nothing since it will only ever tax profit. The government does not guarantee share prices, however they do house prices, I don't know if it is to protect banks or property owners or both, but time to invest in some more property. Interest rates cannot go up since that will cause too much damage to banks, and people with mortgages.

It is time that the government realized that in order to fix this problem somebody some where is going to have to experience some pain, and I think it should be property owners (I am a property owner) and banks since they are the ones who benefited most from the gains in property prices. To me that is the problem with this government, its to nice, and unwilling to make the hard choices.

"it's too nice and unwilling to make hard choices".

Just unwilling to make hard choices. Being nice would be fixing this shambles but the power feels too good. To make hard choices, in the best interests of the country and future generations, you have to risk becoming unpopular with certain groups and possibly losing power. Jacinda is a career politician and she has no intention of going anywhere.

This may result in larger and faster price increases in property markets as investors perceive the government support for the asset class is growing.

Less risk because the government has your back -> higher risk-adjusted return -> higher prices

Feel like she should resign tbh.

How can she possibly solve housing affordability or child poverty without real house prices falling? We have the most expensive housing vs income in the world...

Yup tend to agree - that was her waving the white flag. Who’s next?

"You have passed legislation that you say is going to lift 88,000 children out of child poverty. That's great but the National Party pledged to lift 100,000 out in the same time period - are you being ambitious enough?" asked Ms Owen.

"Their plan to lift those kids out was tax cuts, which only took 50,000 kids out of child poverty," said Ms Ardern.

"What they're going to do about getting those extra 50? We don't know, but if they share our ambition on child poverty, that is fantastic.

"One of the things we're really wanting to do is commit future parliaments and future parties to setting targets around this issue."

National won't join child poverty conversation unless Govt 'shows it's serious' - Bill English

The Prime Minister emphasised that 88,000 was just a starting point to rolling out a wider plan, which will be conducted through robust research and transparency with the public.

https://www.newshub.co.nz/home/politics/2017/12/jacinda-ardern-wants-to…

3 years later, number of children in poverty = 150k and housing wait lists exploding.

Well done Labour...

At the risk of stating the bleeding obvious, child poverty is inextricably linked to house price inflation and high rents.

ROTFLMAO

Lets say an annualised house grown rate of 4%, incomes never rose that fast, but even if they did, your average income of $53,040 will go up by $2121 while your required 20% deposit on a median house worth $760,000 of $152,000 will go up by $6,080 and therefore becoming increasingly unaffordable. The price level is too high for incomes to ever keep up with the deposit increases if the goal is for incomes and houses to rises at the same rate.

Lower interest rates have softened the blow but that can't continue for much longer and once rates stop falling, affordability will drop significantly. I've only just thought this through so let me know if I'm missing something.

You can buy smaller (apartments) or further out from the city centre. That's what happens with a growing population. I'm willing to bet that the average income of inner-suburb residents is higher than the average of the city as a whole, at least if you exclude city centre students.

Or not if they’re NIMBY boomers living off rental income and super.

Who needs a deposit when you just use equity in other homes? Hence why people who have home/s can buy more and more while FHBs (who don’t have rich parents) are going to struggle to put together a deposit

Yes I think you're onto something here Jesse1...

Low interest rates as now push up prices. As does more buyers chasing stock than sellers provide.

Interest rates go up... sellers wont want to sell for less unless they're also buying in the same market, so unlikely to list houses unless they really need to and that could be based on having taken on a massive amount of debt at previously low interest rates.

Shortage of supply despite increased rates still puts price floor under sales. The lock-in effect.

So I think barring people moving within the same market, unlikely sellers are going to accept a huge discounted price compared to what we've seen lately. Hence, after another year of increases in my analysis (2021), likely to perhaps go flat for a long time. Maybe that is the time to buy.

Then again, perhaps I'd be better off polishing up that crystal ball.

You've got to the heart of the issue. So many New Zealanders turn to the housing market because they don't have to worry about prices going up and down like they do with shares. They only go up. (And of course no mention of debt leverage and tax advantage).

How can this be a mentality expressed by our Prime Minister?

Well because it’s true. I’ll give her that.

"Put to her that people who invest in shares, for example, don’t always expect the value of that asset to go up, so why should it be different for housing? Ardern responded: “This gets to the heart of the issue of why so many New Zealanders turn to the housing market.”"

What on earth is this nonsense. Housing is an asset with risk associated with it like any other. For the government to attempt to 'derisk it' or pretend that it is 'risk-free' will only result in very very fast price rises as investors risk-adjusted returns increase. Sustained moderation my ass. What on earth...

But that is what happened this year - they made property a zero risk investment with 20% returns. What a deal! Everyone should buy 5 each

Investors in shares don't expect their shares to go down for very long. I think the calculation is one year in five or something like that. In the long term share investors expect them to go up hence the saying, "it's not timing the market it is time in the market". They would soon give up in shares if losses were to be expected much more than that.

Property buyers expect to lose in the first year or two as well.

I guess she *is* the new Helen Clark. Good at 'gravitas', a 'steady hand', but totally relaxed about poverty and inequality.

I'm starting to think she *is* a little bit intellectually lacking, in the specific sense of being unable to distinguish between gestures and policy that changes observable reality.

You're not wrong.... super empathetic, and great communicator - but lacking in policy effectiveness

There is a big difference between those skills and understanding cause-effect relationships + designing good policies that drive behaviours you envision

She won the popularity vote - that's really it.... (largely due to crisis management and having empathy), but did not deliver policy promises or improving everybodies standards or living

Popularity makes you feel good in the short term, but driving better policies actually drives a larger benefit overall and is far more important

Most of the comments are so tiresome and whacky. For your mental (and financial) health try and stay away from interest.co comment streams. Ardern is shaping up to be a fine Prime minister.

Zach. How are you defining fine?

Are you comparing her to

1. Promises and delivered outcomes, calibre of team she selects and structure she devises for them to work within.

2. Past NZ governments in different circumstance

3. Other countries governments with different circumstances.

4. Feelings.

5. Ideology.

How?

Because she is now promoting house price increases - that is why...

Your measuring stick for a prime minister must be pretty low then

zachary... but it is a little ironic that, financially speaking, she is great for most people who did not vote for her while doing extreme harm to a good percentage of those who voted for her.

Pathetic

Well, want to put the brakes on? put restrictions on borrowing capacity and foreign cash investing in property

Implement a max debt to income, where rental income is calculated at 30-50% of actual

Clearly Labour has no incentive or desire to tackle this housing mess, its simply a hot potato that gets thrown around, talked to, blamed on, avoided or kicked down the road

Inept government

This article sounds like lip service to me.

- Housing is a basic human need... enter the mortgage lending industry by the banks

- Education is a basic human need... enter the student loans.

- Money should be sound.... enter currency devaluation due to printing at such a ridiculous amount, so much that nobody cares about the printing anymore.

- Free nations being allies is a basic working mechanism for peace... enter the swap lines.

- The reserve currency of the world has printed 40cents for every dollar that has existed, in March.

https://remarkboard.com/m/the-government-has-printed-40-cents-for-every…

Things are entering chaos time.. you must invest otherwise you'll wonder what happened.

Simply put - she has no idea of the problem, how bad it is, what it means, how it happened, or how to fix it.

So many anti-Jacinda comments on this thread (over 50 thumbs up on the 1st comment) Obviously this does not represent the majority of people's opinions since her popularity has risen to an amazingly high level. I've always wondered why the majority of commenters on Interest are so far left leaning, positively hating National and now very much disliking Labour too. This is not a reflection of the majority since Labour's support is up 7% to 53%

Indeed, Yvil, the comments here are very much a minority viewpoint.

Zachary...intelligent, thoughtful viewpoints will always be in the minority.

Interest is definitely an outlier. As an example it's the best place to discuss Bitcoin in the context of economics with wide ranging and generally intelligent robust discussion. Worldwide ownership of BTC is somewhere around 2% right now - not even out of the innovator stage. The fact you can find quite a few people here who understand it, how it works, and the opportunity as well as the long term risks says more about this community to me than anything.

If you're looking for blind no brain support of politicians - maybe jump over to Facebook or Twitter. On those platforms when it comes to matters of finance, they're thick as proverbial pig shite.

Indeed ks, just look at the over 70 thumbs up on the 1st post of this tread.

Most people on this website visit it because they are concerned about economic and social issues and probably have a much better understanding of them than the majority you are referring to, this makes it is perfectly normal for them to understand what Labour is doing is hurting us as a country.

I am hopeful more people are opening their eyes even if the polls still don't show, it is not a matter of being pro of anti Jacinda, but against the policies they do or better said they avoid to do.

Oh it's anti Jacinda. Because she LIED about fixing these issues to get herself into power.

Let me know when the big media outlets report that Ardern wants house prices to keep rising. Then you might see how popular she actually is. At the moment she has the Grey Lynn set running interference for her and actual reporting like we see here being ignored. In the words of Francis Urquhart, "nothing lasts forever."

I'm not anti-Jacinda... I think she's been a great leader, though I definitely support Australia. I lived and worked over there and it's a wonderful place, people happy, friendly no worries attitude.. the news had a lot to celebrate in Australia.. when I came back here I couldn't watch the news for a long time.. it focuses on all the crime and suffering. Not a lot to celebrate, except sports of course.. I think we could learn a lot from our cousins across the ditch, It's not a good idea to not support them. They haven't got any chips on their shoulder about westerners like that other country that we won't mention, who is giving them strife atm. When you are a popular leader, money can still buy you if you have no guts.

I don't hear or see such a rosy picture of our friends BL, either personally or from friends/colleagues. They do some things better I agree, but they are as corrupt as it's possible for a Western nation to be. The influence of mineral, super fund and union lobby groups is extraordinary. This is the nation that exports 40% of the worlds coal (not including their own use) despite having devastating bush fires last year. Yes they have great infrastructure, but it will cost you $30 to drive from North Sydney to the airport on toll roads - would you sign up to that? They have a terrible human rights record, soldiers slitting unarmed 14y old boys throats and a toxic corporate culture. We aren't perfect, but I think we are a far more harmonious and sustainable nation.

National ran a sham of an economy based off selling land/assets, high immigration and promoting housing speculation. Labour are now seemingly doing exactly the same thing (minus immigration temporarily due to COVID), hence the outrage from commentators.

I'd hazard a guess that most people who read interest have a better awareness around these issues than the general population (a good chunk of which are statistically not very intelligent).

Yeah in my experience there tends to be a correlation between education level and tendency to be more left leaning.

So the Greens supporters are the smartest in our land, huh IO

Who is a Green supporter?

I wonder if there is a correlation between level of education and voting preference. Universities in the US are heavily left leaning then you wonder what influence they would have on the minds that go through those institutions. Equally you may see a left leaning tendency here in NZ for those with higher education.

I.O.. never went to varsity myself but strongly suspect NZ universities are seriously left leaning in every possible way.

They are left leaning because they are ideological, theoretical entities. Teachers don't own businesses which need to be profitable to survive, teachers don't employ people and pay them wages

Generally the haves are happy to see house prices rise while the have-nots would like to see them fall. In actuality there are many homeowners who would prefer a fairer society who would be quite happy to see house prices come back 20-30%

Completely agree.

The immigration free for all would have to be indefinitely suspended for that to be remotely possible.

I'm confused. Almost everyone tries to pretend house prices and rent increases have nothing to do with adding 300K every five years to the demand side of the equation.

Very high net immigration is the root cause of the problem. The problem is that both Labour and National support this policy and are afraid of upsetting the increasing number of recent immigrants to wind it down.

True, in fact a Collmar Brunton poll revealed 75% of people believe house prices need to fall to improve afforadability

Interesting that jacinda has gone the same way as john key.

In 2007 , john key was talking about housing affordability and seemed to have a reasonable understanding.

Im guessing the both of them realized that the nz economy relies on credit growth and immigration.

( Which are related to house prices )

They both realize a recession, which is what would happen with a contraction in credit growth, is not good for politics.

( Debt capitalism requires continuing credit growth ).

Im guessing people want cheap house prices ,without a recession ...

SO... Thks to our version of capitalism and John and Jacinda , who have been passed the parcel, we are where we are .

She has this wrong. It looks like they are now "National lite". The people that voted for her expect her to actually do something about housing. People are prepared to suffer their leftist agenda, but only if the current housing stupidity is actually addressed in a meaningful way. Planning to have employers simply pay lots more in wages will only lead to Hyperinflation which will do far more damage.

For her to Kowtow to the global banking agenda of "debt forever" is nothing but a total sell out.

Interest free 20% deposit from government for first home buyer I heard?

Hot off the press - NZ's home ownership level lowest in 70 years. (Note: only to 2018 - likely even worse now)

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

So question to all the commentators who say that house are still affordable - why don't more people own them?

I was prompted to run some numbers to look at the idea of “smaller increases” in house prices being the solution to reconnecting house prices to incomes.

In 2000 the ratio of median income (individual) to house prices (HPI) was 15 times.

In 2020 this same ratio is 29 times.

If we assume 4% wage growth each year, the number of years it will take to get back to the 2000 ratio (x15) under different “smaller increases” scenarios is:

Annual house growth @ 1% = 22.5 years

Annual house growth @ 2% = 33.9 years

Annual house growth @ 3% = 68.0 years

If there is just a single year when house growth outstrips wage growth prior to these “smaller increases” happening (e.g. in 2021 10% house growth vs 4% wage growth), you need to add another 4, 6 and 10 years to the above totals respectively.

How can this realistically be the government's strategy?

This is why Im calling out Ardern as either totally innumerate or an outright liar.

Perhaps both.

You forgot the politically acceptable scenario.

Wage inflation at 0%

House price inflation at >4%

Houses more affordable = never.

For our global banking owners, the preferred option. Endless loop of forever debt.

B-b-b-b-b-but we started working on household income to house price ratios back in the 90's because that disguised the ugly truth, kept the "ratios" somewhat in check.

I can't believe what I just watched. Ardern is in deep water and struggling.

House is not an asset. House is not an asset. House is not an asset.

An owner-occupied house isn't for sure, something many people don't understand.

"Put to her that people who invest in shares, for example, don’t always expect the value of that asset to go up, so why should it be different for housing?" Don't they? That's surprising to me. Who invests to see their asset go down? The volatility of shares can be tracked more precisely by observing daily price movements, making dips more obvious, whereas the daily market fluctuations of property is invisible, but investing in shares to make va loss? Pleeeeze!

Um, dividends.....

Dividends will never match a falling share price and when share prices do fall, dividends disappear along with asset value!

Given house prices have been meteoric for some while, there is plenty of room for them to fall quite a lot without doing too much harm, then they can make small increases.

It is probably cheaper to compensate all owner/occupiers who bought this year, in a fall, than it is to continually have to subsidize rents/mortgages via top ups.

Well she is right as always , small increases allow people to invest and upgrade their properties .

In other words. I'll look after the 'Middle Class' serfs whilst the peasants can toil for crumbs.

Why does every home have to be an "asset". Most people simply want somewhere to live they can call their own. She is perpetuating the problem by stating people want their assets to rise and viewing housing as an investment even if you only own the family home.

Can't wait for the reactions from our PM when the new REINZ stats are released in a few days.

Spent the last few months in wellington region areas looking at homes and if they thought October was bad, just wait until November's stats are released.. the flames are about to get much higher

I hate this women. [second part of comment removed by Editor]

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.