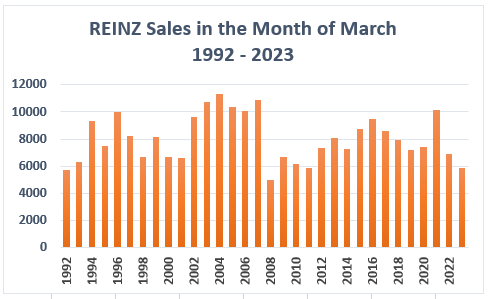

The housing market continues to bounce along the bottom, with March sales at a 12-year low.

The latest sales figures from the Real Estate Institute of NZ show that 5877 residential properties were sold throughout the country in March this year, down 15% compared to March last year and down 42% compared to March 2021.

Last month's sales were also the lowest recorded for the month of March since 2011 (see first graph below).

Selling prices also continue to be weak, with the REINZ House Price Index declining by a further 0.8% in March. It is now down by 16.8% from its November 2021 peak.

The national median selling price was $775,000 in March, down by $150,000 from its November 2021 peak, with even bigger price declines in Auckland and Wellington.

In Auckland the median selling price hovered just above $1 million in March at $1,000,600, down by $299,400 compared to its November 2021 peak of $1.3 million.

In the Wellington region the median selling price was $750,000 in March, down by $250,000 from its October 2021 peak of $1 million.

March is usually the busiest month of the year for the residential property market and while sales were up compared to January and February, they remained at a very low level compared to previous years.

"This year's summer season has been muted," REINZ Chief Executive Jen Baird said.

"Prices have eased as we can see, and properties are taking longer to sell.

"Buyers are taking their time, they are negotiating and some are waiting to see if prices ease further," she said.

The comment stream on this story is now closed.

Volumes sold - REINZ

Select chart tabs

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

169 Comments

Ouchy Ouch That puts average Auckland house down 23% from peak

And thats the ones that got sold, I know of a couple of houses that have been taken off the market as the offers are around 35% below peak and this wont let the vendors buy the next house in the chain.

Is anybody actually in the know, actually surprised?

Is anybody who reads int.co regularly not surprised?

I think there are a lot of people wanting to sell that are patiently waiting and praying for a change of government thinking it will reignite the market. Regardless of who wins I think there will be a flood of listings by year end

Haha - to 'reignite' the market now. Is political suicide - remember what happened in the UK when they played with taxes for a couple of days.

The issue is that anything, any government does to markedly pump house prices in NZ will inadvertently pump inflation..... and that will cause interest rates to stay high or rise... causing more problems.

Best thing a government can do is to cut wasted spending, maintain existing infrastructure and do stuff to encourage productive businesses here. and do what it can to help RBNZ control inflation.

Yes if National go ahead with tax cuts and the like NZ credit will be downgraded, get ready for higher interest rates for longer if they do.

If National bring back tax deductibility for rent/mortgage this will cause serious damage (loss of value) to the new build market. I feel sorry for any body who has purchased a new build (and the developers) in the last 2 years if they do.

100% correct. Mind you, new builds are not selling now either.

Wait until some of the landlords who are making damn all or even a loss see their 2023 tax reconciliation - to find that for tax they now have a profit.

The joy of having to fund the loss and now fund the tax.

Shopping time for FHB"s getting closer by the day.

.

Only anecdotal/opinion, but - a friend is an accountant who works directly with many small-time property investors. She is regularly amazed at their lack of basic financial literacy and, despite her best efforts to spell it out, believes many won't accept or understand the the implications of the tax change until they actually get the bill in their mailbox.

Most will be praying that National get in

"I'm not paying that tax bill! *scoff* What do I pay you for? You're meant to generate tax refunds not tax bills."

Agreed. I know a few true investors who understand cashflow and yield. They have all sold parts of their portfolios to significantly increase their actual equity as the focus moves off of using debt to rinse taxable income.

Yes agree - I know quite a few people who have made good money in real estate in recent years. Many I went to school with and who struggled through maths (or all subjects) and have absolutely no idea what they are doing (some work at mortgage brokers and real estate agents!) - but their recent success has fooled them into thinking they are very smart - but I know from my time with them at school that this isn't the case. They've been fortunate in their timing and their environment - and it has nothing to do with their own level of understanding or intelligence.

Fooled by randomness as Taleb would put it.

Now is when the value of having a decent education will pay off.

True for some of the people running property funds too… easy capital, rising market etc I wouldn’t trust/ have faith in some of them to run my local rugby clubs raffle ticket sales

I agree that the election outcome will decide who blinks first. I have a relative with ~50% deposit who for personal reasons will be looking to tradeup in Auckland in the second half of this year & considers that the decision should be made & deal done by the end of the year.

Would you say your friend knows they are digging deeper into a country with a big and persistent balance of payments deficit, and what that means for them?

Good point.

My relative is also registered to teach 2ndry in Queensland which was the plan just before Covid - during which time they met their current partner who is more tied to NZ. So, it may well depend if that relationship continues.

We have also had that emigration conversation again this year because of extended family in Oz (one has just entered Aged care there) & I myself lost my wife 18 months ago so am more open minded about a move & have said I will make my own decision after the election.

I am sorry for your loss, I cannot even imagine how hard that must be.

Thank you very much for your condolence.

"That puts average Auckland house down 23% from peak"

Still standby my theme (for many years on this site) that NZ houses have the potential to drop 40-50% in real (inflation/income adjusted) terms.

A 23% drop, adjusted by a few years of 7% income/CPI inflation is a significant move towards this outcome. But I've been told (by biased/vested interest parties) that this outcome is 'impossible' so of course it can't happen here.

But do note that when a housing market starts falling like this, the rate of price drops often accelerate as the economy deteriorates and unemployment rises and credit extended to the market drops (as banks get fearful of borrowers in negative equity/ debt defaults and they can't find any/enough credit worthy entities to lend to, in order to continue debt expansion - which is what the bubble was fueled by).

Agree. As business start to fail, que the very at risk construction sector getting short squeezed currently. It employs a lot of people directly and indirectly. If things really start to unwind will the banks start to make some margin calls. The banks are acting scared when approached for non housing lending, and are reducing overhead left and right via closing branches or sinking head counts as staff leave but are not replaced.

What do they think is coming...?

There is too much debt relative to income generating assets* across the economy and when this happens, at some point, always ends in financial chaos.

Timing is the difficult part to determine.

*many people think they are wealthy because the hold a lot of debt against an asset that has inflated in price, but never considered the consequences of servicing that debt in the long term and whether that asset can produce more income over the long term relative to the cost of servicing the associated debt.

In the past 40 years, on average/ the trend has been, that each year the debt serviving costs of income producing assets reduced. That 40 year cycle may now be in reverse and could have huge consequences on asset prices (when discounting future cash flows).

So Auckland is already down about 33% from peak in real terms

Yes and no meaningful rise in unemployment or mortgagee sales yet. A 'soft landing' for the Auckland market could mean a 40-50% drop in real terms! - given the way it is unfolding at present i.e. we're seeing US GFC size drops in major city property market like Auckland and Wellington (30-40% in real terms) and yet we are yet to see any real damage within the economy.

It is a little scary to think what a 'hard landing' means now....what could happen if unemployment really takes off and it takes 12-24 months for inflation to get back into a safe space for the RBNZ to start dropping rates again and for falling mortgages to soften the blow. We are already down a long way and no significant signs of recession, debt defaults, mortgagee sales.

If the RBNZ and Government intervene too heavily like they did in 2020 to stop unemployment rising too much, all it is going to do is push inflation higher again, and if inflation is high, mortgage rates are going to remain high, and if mortgage rates remain high house prices are going to keep falling.

My maths running the discounted cash flows last year indicated a 40% fall in nominal terms is quite possible for the lending that was done in 2020-2021 with 2-3% rates at initial lending vs 7% average rates over the life of a loan (which will be determined by how much money/inflation the US creates to avoid default on its treasuries). I'm not sure how we avoid this but I'm sure central bankers will come up with something that will distort 'free markets' even further!

Could easily see a further 5% fall in nominal prices in Auckland, and if we assume inflation averages around 5% from now till late 2024 then that will be a real fall in values of over 45%.

Yes I'm not sure which is going to happen:

1. Rising unemployment and deflation which pushes nominal prices lower (limited/no drop in prices if adjusted for wage/price inflation/deflation).

2. Stable employment and higher inflation which limits the fall or flat lines price falls in nominal terms but causes prices to fall further in real inflation adjusted terms.

Could go either way at this point.

With the scale of the property market and its interdependence across so many industries, unemployment has to rise as the market collapses.

How can it not?

There is no alternative prop.

The unemployment could correct pretty quickly though. NZers who can build , drive, nurse, or anything else except sell houses can earn more in Oz, and once they go they are not unemployed anymore.

HM many taking houses off the market because bids are considerably lower then just 5% more.... we will see further falls but then the market will start to function again, at the moment to many holding out so the chain stops.....

Nice to see you back on these boards. I think there would be very little chance that the govt or especially the RB, are going to intervene to stop employment falling further.

This inflation is now in deep and some of the reasons are directly related to interest rates being a blunter tool than they were in the past.

We have reduced home ownership, have a larger proportion of owners with no mortgages, no movement in unemployment numbers and rents static. We also have two generations that have basically given up on ever getting a house and thus not saving.

Couple that with climate change damage that increases demand for repairs and maintenance and you get very sticky inflation.

It seems what is more likely is that govt needs to engineer unemployment or increase taxes to quell demand, which isn't happening in an election year. This is a new kind of paradigm and we possibly don't have the tools yet to combat it.

No idea where this ends up? Something has to give and it does feel like it means a longer recession and more instability for the foreseeable future.

I never understand the use inflation adjusted performance for property, this is irrelevant. Because, property is typically bought with borrowed money (partially offset by rent received, or avoiding paying rent if it is your home). NZ property prices underperformed inflation during the 1970s, But, anyone who bought multiple properties in the early 1970s was wealthy by 1980. They did not go the houses I bought for 10K are now worth 30K, but inflation has 4x ed the last 10 years so I'm underwater. They would have gone the house I bought for 10K with a 8K mortgage, is now worth 30K, so my 2K equity is now 22K, I have 11x my deposit, and the rent for the property has kept up with inflation and is now 4x what is was in 1970, so is throwing off tons of cash as my mortgage is still only 8K.

This does not mean I think property is going to go up. I don't think 2021 prices will be exceeded until 2030 to 2035 at the earliest. I just think, comparison to inflation is pretty irrelevant with leveraged investments, and just muddies the waters. It sounds like you are grasping at straws with a bearish narrative , "so you think you have done well, but have you adjusted for inflation".

I just think, comparison to inflation is pretty irrelevant with leveraged investments, and just muddies the waters

I'm on the same page. If wage and income growth is outstripping general CPI grown, then there is an argument for its relevance. Wage inflation growth has substantially lagged CPI and house price growth for 30 years. That is not going to change. In fact, it's likely to get worse.

The ruling elite tolerated this because lack of meaningful income growth for the boomers was substituted by asset price growth. The con is becoming more clear but the sheeple can't really see it yet.

The average punter in a $1 million house, with inflation at 7%. Would be happy if the house only appreciated 5%, and went up $50 K in value, even if you told them it went up less than inflation. As the principal of their mortgage is not inflation adjusted, this is where the inflation adjustment for leveraged assets argument falls flat and becomes irrelevant.

Looking forward to the same comments from the same people on this one!

If you take out us old agitants, I wonder how many comments would be left

The pot calling the kettle black I think.

Not at all. Its a good forum that draws in smart people to comment. You can check out anytime but never leave

I presume you think the only ones who are smart are those who agree with your views.

Gee childish

Honestly the only reason I come to this site is the comments section.

There are other bits?

That is what attracted me when I first started a few years ago too. There were usually more interesting discussions to be found than the article itself.

Def gone down hill a little bit but still great in general.

Real estate agents are going to need to find a new job pretty soon

Some employ smart marketing getting them national newspaper headlines by taking a cutesy alpaca to open homes and client meetings. Whatever next... an agent with a House mouse?

Almost 6000 homes sold during the month. Not a bad tally in tough times

See my comment re 31st of March.

and most real estate agents are also qualified to...

In most cases I really hope they managed to save enough to go back to uni.

OSE

6000 sales at the median is a lot of commission dollars. Lets call it 100 million at a little over 15k each

Yeah - BUT i would wager the 80-20 rule applies. (20% of RE agents sold lots, are loaded and will continue to do well even in the downturn but the other 80% probably wont fare so well if they didnt in the boom)/

Then - we have to see how many of those that DID make money believed their own pitch and invested in property and are now regretful.

Lets not forget the other agents who sell lifestyle, commercial, rural etc. This is a billion plus dollar industry and to you its about to fall on its head

Real Estate falls on its head every few years. last time was the GFC, now is the next. good agents will survive... esp those that have been around and know how to manage downturns. some older ones will simply retire now. its the same in sales in most industries...

Spoke to one on sunday who claimed in Nelson/Tasman they sold between two of them, 10 houses Jan,Feb,March on a portfolio of 40 or so houses so around 25% successful sales. The bloke was doing 9 open homes this sunday been so they're obviously having to do some work.

"This is great news for the housing market" - Tony the Comb, probably

"FHBers intentions to visit open homes are up 1%"

Lots of green shoots as people cannot afford to mow the lawn as often?

Oneroof helping the REA's out there by putting a positive spin on it... "NZ house sales jump 42% after wash-out summer" https://www.oneroof.co.nz/news/43432

They have no shame, make no mistake they have no interest in the financial outcome for the buyers, they simply need transactions to stay alive as an industry. We are still moving faster than Ireland did, during their crash.

Auckland and Wellington leading it down, there is carnage to come in the regions.

Agreed - I had a chuckle yesterday when a friend of mine proudly told me Queenstown is immune to the crash

'crash'... is a bit steep hey.

Perhaps 'Most NZ citizens and next generation of Kiwis finally to benefit from rapid shift to affordable housing'... or if you are leveraged maybe... 'A few NZ citizens get wiped out after years of greedy selfish gambling on house prices'

We may not see it as a crash and for sure OneRoof and MSM are not using the C word yet, but internationally thats the word being used re NZ Housing market

I like the "I" word. Immigration.

Every person is here because of it and now many many many more are calling NZ home

FBB means it can't stoke house sales much, so you're still ok to use the C word

"It is evident from the statistics that prices have stopped unrising at quite the same pace in some regions of the country, presenting a golden opportunity for the astute, savvy, intelligent, and good-looking investor..."

"unrising" I like it. Even when prices stop unrising, they will grow sideways for a while.

I do not think the sellers have woken up to the reality and their handlers RE agents are not giving the right advice.

I know of examples where RE agents provide high expectations for the price and when the house doesn't sell, they tell them to take it off and wait up to cause a shortage of houses on the market. They are reaching prospective buyers without even listing the house so that it creates a false sense of not enough houses on the market.

RE agents are a cartel system and they are certainly not honest. The whole system is totally corrupt and main reason why house prices went so high and still remain high when interest rates have gone from 2% to 8%.

I had one ( from Ray White) flat out lie to me on Sunday at an open home, said “ prices haven’t decreased at all, they have just stopped rising” , I couldn’t stand this so told them I follow the REINZ HPI and prices certainly are dropping, but they were fairly unrelenting in their argument.

Was it Steve?

Mr K?

oh gawd

No a woman, but the way she talked and how I’ve heard it before sounds like a company thing “Well what WE see is prices flattening a bit, then the market taking off again in the New Year, back to where we were “ ( last years RE advice), both times sounded like it was coming from RW training days.

Ray white spinning the same lies up north too.

Its an obvious nationwide guidence from HO to avoid the bleeding obvious.

Just confirms what I see: houses listed between 95% and 110% of CV (Sept 2021 here = ~peak) and buyers having a purchase power of ~80% of CV. The latter are borrowing to the max with no possibility to increase their budget, the former won't move on their price. No wonder sales aren't happening. Either wages and inflation catch up with sellers expectations, or asking prices have to go down. How much longer can the status quo linger?

Or the standoff continues a lot longer. Depends how many people need to sell, vs how many need to buy, and at the moment there aren't a lot of either.

We are not at the bottom yet wait to June to October then the market will really undo.

This is only good for all young Kiwi.

Let the correction begin.

Not so good for young Kiwis who own homes, is it?

The lower the prices the easier it is to upgrade as you have kids etc.... lately a decent upgrade has been like 500k in AKL, who in their late 40;s early 50's wants to take on another 500k of debt, most do not even have that saved for retirement. Some will have taken the debt on with the idea they where renting that debt and would downsize later.. now they are stuck with the debt, so goes it in a falling market.

The big impact on NZers is they hold a disproportionately high amount of wealth in housing, this crash will make many peoples retirement more bread and butter then honey and jam.

Only if they need to sell, which is not many of them.

GV

Currently, the more significant issue for young home owners is mortgage interest rates rates. This is especially important for those who mortgage terms are due to roll this year, and as RBNZ have indicated that there is likely to be further OCR rises, this is likely to include those due to roll over in the coming year.

For young home owners, the value of the house is very much secondary to interest rates. As long as borrowers are meeting their mortgage repayments, the bank is unlikely to be overly concerned about the current values. In their own interest, banks protect themselves and their deposit requirements and stress testing means that while some borrowers will be struggling - especially if there is changes such as loss of job or separation - most will not be causing banks alarm.

Yes, for most young home owners who purchased in the last year the current situation is not "a good feely-one"; however, rather than short term, home ownership is long term. As I have posted before, I purchased an investment property in late 2006 to see its CV value during the GFC go below purchase price but I sold in 2016 with a tidy capital gain. Its a bit like the KiwiSaver growth fund - one shouldn't panic in a downturn.

Yes Printer, I think the pace of this unwinding is very much down to the banks, if they are happy with the risk held on their books - which must be changing for the worse daily - then things will go slowly. Seems the very high employment rate may be stopping forced sales, but there have been some very low prices achieved at Auckland auctions and some sizeable drops in HPI this last month (March).

Agreed. Try borrowing to do something constructive within a non ponzi related business. The very first question is "how much is your house worth". Overdrafts are north of 10% already, even with multiple securities.

Overdrafts are 15-21% if unsecured by real estate.

That's bollocks. I have a 300k od not secured by property, 10.3%.

"Seems the very high employment rate may be stopping forced sales"

I think the very high employment rate (globally) is the one remaining thing supporting the entire everything bubble, like a giant late-game Jenga wobbling precariously on that one high-employment block. When that block goes, it all comes down.

Happy Tuesday everybody. ;)

True. Unfortunately they are victims of the Ponzi. Doesn't mean that the Ponzi shouldn't be brought down.

only if they are so overstretched they are forced to sell -- and TBH if young kiwis have got on the market in the last 2 or 3 years -- they probably have either the means or the Family/whanau support to hang on to them through the next couple of years anyway. Great for the 95%+ who have had no chance up to now though!

Yes if you made a bad decision in the last 4 years not good at all.

You can thank the bankers for this they feed the biggest Ponzi this country's ever seen.

Be very carefully of them for the rest of your life.

Hang in there you will be fine in the end.

Time fixes most things in the property game.

June to October? Sounds about right.

That would be about the time the tax bill for many landlords actually sinks in ... Together with the realisation that interest deductibility is only at 50% ... and next year it will be 75% and the year after 100%.

Property prices won't see all time highs again until the mid 2040's. The deflationary bust is only just starting.

Nah - unfortunately we humans arent logical - look at Ireland. We forget bad periods much faster than that.

We will likely have a massive crash, might event wipe 80% of values by 2026 and in 2027 they will start to recover and anyone with a shirt left on their back will be buying houses again.

(course the retirees in the next few years will still be working in 2040)

Land owned by households as a % of GDP at the end of 2021.

-Japan 130% (peaked at 325% in 1990)

-Australia 330%

-New Zealand 520%

Could be later than 2040 - much later.

I've posted before about the effect that the intensification changes that came out in Auckland's Unitary Plan of 2016. It caused a flatlines of house prices from 2016 to 2020. Now thanks to the NPS/UD and the MDRS every major city must do something slightly bigger than what Auckland did in 2016. That's a huge increase in the supply of 'land' that can be built on.

Inflation up. Rates up. Sellers still in denial. Buyers are increasingly being pushed backwards buy the cost of lending. Agents caught as the proverbial meat in the middle.

Lets face it, a lot of cheap debt has not expired so, sellers are happy to continue in denial waiting for cashed up desperate buyers that were around in lockdown. News flash... the cashed up Awklander is all but a thing of the past. No sales no cashed up buyer. Awkland wore the worst of the lock down so people were panic buying to exit the region. This was fueled by overseas based buyers paying anything to return to NZ, all underpinned by debt at 2.5%. This created a very artificial high. All those dynamics have stopped.

All coming to a head. Popcorn.

So you aren't a fan of Awkland, I'd never have guessed. Something else I would not have guessed is you owning 4 homes.

Yes, I was also quite surprised Avergeman saying he owns 4 properties.

Not an average man. Sold 5 others and sitting on a cash pile

Stay on topic lads. Sales are the lowest in over ten years. Why is that...hint, its not because of something I did or did not do.

I don't own any llamas or use them as a marketing gimic.

These REINZ reports have become a lot less user friendly for the public. You can’t download reports on a device, so I have to biff the iPad and drag out my laptop, then graphs have all lost their time labels - hard to judge the start of the pandemic other than the shape of the graph.

Hard to not view this as intentionally obfuscating.

Yikes.

Some of these monthly HPI drops would be very concerning as annual drops:

North Shore -3.4%

Franklin District -4.1%

Rotorua -3.9%

Wellington City -3.6%

Genuine question: when should a RE declare that a property for sale is cross-lease not fee simple?

Should that be in the advert?

Should it be in the written material handed out at an open home?

Or is it OK to only verbally advise that a house is cross-lease once people get to the open home, even though neither the advert nor open home brochure contain that info?

No hard and fast rule in the Code of Conduct when things should be disclosed, but I certainly think that would be in the advert.

You can normally tell quite easily because a cross lease property won't advertise the sqm land size.

At most they will say 1/2 or 1/3 share of xx sqm.

If it was in the advertising, would you have gone to the Open Home?

There's your answer.

Did you notice how antz has his terminology muddled up

??

Educate me.

The only time I ever noticed an agent adding any value was them providing a quick vacuum before an open home. I mean the floors.

Cross Lease or Fee simple is part of the legal description of the property, it most certainly should be declared early. Our experience is where they can agents will try to withhold information. Flooding is the most recent example where we live, it is never declared and when we ask ( knowing the answer), the agents say they don’t know. We always check the council interactive maps (just google with the name of your council with the words interactive map) it will show you the legal package of land …. If there’s a second house on the back that’s a giveaway, plus they have overlays for hazard areas such as flooding or coastal inundation.

Did you mean leasehold (i.e. usually with ground rent payable and subject to review)? Cross-lease properties are common, especially in Auckland.

The legal description of the property is on the first page of the contract so everyone can see it before going to auction or putting pen to paper.

No, I meant cross-lease, not leasehold.

Greg, why do you compare March 2023 sale prices with November 2021 figures? Surely March 2023 figures would be best compared with the same month a year ago, as is common practice.

It's a bit like stating "The median price rose by 1.3% in March compared to February in NZ". Well it did, but it's cherry picking to try to make a biased point.

The comparison in the article is with November 2021, not 2022. And that is because that was the peak. It makes sense to compare current prices with peak prices.

Or am I missing something?

Well, comparing to a peak over a year ago, instead of common practice of comparing year-on-year, is a biaised attempt to say: "Wow, look how much values have dropped by"

It's like comparing prices to the last trough in 2008 and say: "Wow, look how much prices have appreciated by" It's biaised to make a point.

Both are relevant and useful, ie. Fall from peak, and YOY.

Agree - it was one of the things I was looking for in REINZ report. Then I couldn't see what the dates were on the x-axis so the data became very hard to interpret.

And I find it odd how they suddenly changed the timeframe of the charts they used when house prices started falling. They used to use a far longer history on the x-axis to show how far and fast prices were going up, but have recently moved to a much shorter time frame so you can no longer see that data. Are they trying to hide the risk of just how far house prices could fall - given how far they went up during the boom?

Best option is to go here on interest.co.nz and drag the timeline out to full scale so you can see where we are at, how much and how quickly prices went up in the past few decades, and how quickly they appear to be falling now, and the risk that they could continue to fall further and realising that now asset price cannot grow exponentially (or more exponentially over the long term) when it is based upon cash flows (incomes) that are targeted to grow steadily at 2% p.a.

Unfortunately, you can't do this on the HPI report (view historic data on a graph) - you can't even see dates on their charts anymore (it is like a child's math project that would fail for incorrectly labelling, or not labelling at all, its x axis).

Isn't the 31st of March the big settlement day for new builds?

Looking at the graph above the 31st of March is often the highpoint of the year. This year's highpoint is noticeably below just about every other 31st March date for year! Including even 31 March 2009!

And yet the spruikers, e.g. OneRoof, are claiming the increase in volumes point to the fact we're near or at the bottom? (And they can't spell munted right either.)

https://www.oneroof.co.nz/news/43432

Good grief! And you can't read, you'd better go to specsavers

I don’t see any desperation in house price. No House is for sale in St Lukes and New Market. A house in Rolleston purchased in Aug 2020 for 558k still asking for 889k although it has been on the market since beginning of March. I remember how thick the Propery Magazine were back in 2009-2010 most of them were mortage sale. I haven’t seen it happening this time. Owners are holding very well

The thinner the Property Magazines are, the worse it is getting.

As each day passes, more 'owners' will be imprisoned with their existing holdings as they can't sell at a price sufficient to discharge the Debt.

And we haven't started to see the full force of that arrive yet. It will, as the short Fixed Terms advised by Mortgage Brokers mature and the reality of a new set of mortgage rates reveal themselves to the indebted.

Wait until the tax bill for many landlords actually sinks in ... Together with the realisation that interest deductibility is only at 50% ... and next year it will be 75% and the year after 100%. ... It'll come.

Early days mate.

In OTP there have been 7 price drops in the last 2 weeks.

They have ranged from 10% to 33%

One was 1,300,000.00 now offer over 850k. 2018 CV was 765k, 2021 cv is 1,200,000.00. ... 2024 CV is going to be 800k??

A lot of building in OTP

Canal frontage will cost you big just for the section

Hey Greg, another great photo. It’s a little idyllic though ….. looks like it could possibly be a peaceful retreat from the ensuing economic woes. Some glass, some batts and a large vege garden?

There is no doubt many here are more knowledgeable, thru asessing a broader range of data points and market influences, than the myopic experts still believing the data they get from the real estate industry and other biased sources.

Theres an old saying " 10,000 soldiers cant be wrong" and in this scenario the RB, finance munster🫠, añd the PM are guilty ( as they were in covid) of seeking to few, to narrow and to biased a view point from a few ill informed generals at the expense of the obvious " mood of the soldiers" ( the public)

Examples are..

1. There is no issue with gang organised theft post the napier floods said the police commisionerl!... ( INFO RELAYED from his commander)

The reality.. the public were ignored and proven correct!

2. Ardern relied on to few people / hand puppets for poor lockdown advise etc? Which is a major contributer to our economic woes... " she ignored the majority and paid the price"

3. Health, education, roading... all the same!.., pick a few favoured experts, ignore the masses, and spin a excuse when it goes belly up.

The experts are stuck in a mind set of "same same " optics that donr give a fulĺ picture. The banks are slightly better equipped than the RB and government, but they all miss the real fèel of the WHOLE markets many influences on the property market.

They would be better of reading thie comments here!!!

And what is worse... the government is working against the RB based on bad advice from a few generals, who inturn ignore the 2.5 million soldiers ( who have been either been suppressed or opressed)

Winston Churchill , when faced with his biggest internal conflict ignored his experts, evaded his security, and mingled with the people and asked the hard questions of the common folk.!...

It was a step change / reality check in his govrnance, that improved his profile and Great Britian.

Ardern, Hipkins etal, need/ed to get away from the "organised" public shows of kindness and front the real 10,000 soldiers. They should also be brave and..

-Stop pussy footing around hard questions

- IGNORE THE RADICAL MINORITIES

- Take back NZ from the wokesters

- define the sexes

- unite kiwis by ending the racial maori wonderfulness propoganda/ grievance process

- put the UN demands on hold until the rain stops

- remove mmp or adjust it so all parties declare aļl policies and all alliances prior to voting and not after.

- have ful 100% disclosure of every non mandated deal done up front .

Won't happen. National and ACT would never agree to such terms. ;-)

Sounds like you are half between denial and anger stages there shaft!

Don't Trigger Hemi... i mean shaft

You'll have to try better than that IT

How would you do it Nifty?

You have only put 14 comments on this topic so far. That is quiet for you. Have you something else to do today other than come on here and put people down who don’t agree with your views.

Are you annoyed that I pulled you up for your childish remarks ?

If you think I am here to put people down then please report my comments. But if you just want to be a troll towards me then I will do the same to you sir. Good day to you.

Virtually every comment you make puts people down. We can see it but you cannot for whatever reason. Personally I don’t care if my properties go down in value. I can still afford to eat and go for a ride on my e bike if I so wish. I am a very lucky boomer who retired early and who has helped my children into housing as giving money to them before I kick the bucket seems the right thing to do.

A greedy bored boomer I suspect who likes to target me and shout me down. You sound rather pompous going on about your ebike and comfortable lifestyle. If you dont like that description you can report me or better still stop with your infantile comments like the ones earlier.

I am definitely sick of you repeatedly trolling me and getting in my face for literally no reason and not having a valid point to share about the thread.

You're welcome to have the last word.

The pot calling the kettle black.

I am not pompous. I am a lucky boomer simply by my date of birth. I would love to see those born after me having the same luck but us boomers put the drawbridge up. Put simply housing should be cheaper. Especially the older badly maintained crap that is so prevalent in NZ.

Ebikes are about to qualify for a FBT exemption.

Probably also a rise in acc levies for those employees.

Politicians should realize that this decade is different with internet - heaps of social media option for people to express / exchange views and not be fooled by sound and media byte / paid propgoanda / lobbying.

I big part of the prior FOMO was scarcity of housing. In Wellington prices peaked when people could not find a home to rent. With net migration rising rapidly, how long before we are back to housing scarcity?

Im also interested in our inflation trend versus the US. They seem well on top of theirs, whereas ours seems very sticky. Which is strange given our interest rates are higher. Likely because of the number of monopolies or effective monopolies in New Zealand.

if inflation doesn’t drop it will be higher interest rates for longer and property prices will really suffer.

Yeah, its worse than that. Quarterly sales are at their lowest point since 1991 and its only 1991 because thats as far back as I could get numbers. I took the sales data from the Reserve bank website and normalized it with population data from statistics NZ.

{kind=link}

Great work on the chart CDub. It would appear our chickens are coming home to roost.

If we are lucky we may get some free eggs

Wow. Lower than the late-90's, Dot-com, GFC, and Pandemic. Scary Graph indeed.

Great work on the chart. Thanks for sharing.

Great work thanks for sharing! I would love to see median prices overlaid on this. My gut tells me the median price may follow the same trend albeit with a few months lag - but I am not savvy enough to chart this myself!

I had house price index handy so thats what you get.

{kind=link}

Thanks again! Looks like my gut was wrong!

Your gut isn't wrong. Look at the slope of HPI changes relative to sales numbers. At points of low sales, price is usually flat or falling. Good call asking for this, and great work by the grapher generating it.

I'd add, "But the prices are sticky so the falls in prices aren't as big as the drop in sales.

Yes but I think there might be a variable or two missing to further explain the graph. My thought is that prices have not responded to sales volume in the same way prior GFC and post the GFC because post GFC:

1. Looser monetary policy ( interest rates)

2. Investors overpaying during this period in the hopes of capital gains ( as distinct from rental yield)

3. Possibly immigration pressures?

Thanks for the graph CDub :)

Awesome graph CDub. It looks like it's missing the last 4 plots on the HPI though...

Highlights just how far there is still to fall. Was sensible till about 2012….

Think worse is yet to come.

Someone who bought an investment house to subdivide and rebuild in future in Papakura is struggling as has a loan of million dollar and earlier was able to cover the mortage (Interest only) against the rent that 3 Bedroom/1 Bathroom house was generating but today have to top it up by appox $1000 a week as now paying appox 8% compare to 3% earlier.

Can feel the pinch but is still able to survive for now but if the market does not turn positive soon, may not survive and in dire sutuation, if have to sell at a loss - will lose 25% to30% if not more being lucky.

Many mum and dad used their existing equity to be top bidder in auction and also many small to medium business people had diverted funds into speculation for fast money and are now stuck.......so is Wait and Watch.

23% in fall in Auckland is Crash.

Definitely seeing a trend of increasing numbers of people on investors FB pages and reddit pages asking for advice on their 'tough' situations. Also the mood tends to be to 'hold out' for the election and hope.

Question re investing further here are being met by some strong negitive answers sort of suggesting the naievity of the person asking the question.... Not sure many are cash flow modellers.

Slightly off topic, but this is exactly why planners should have no say on aesthetics.

Not brilliant architecture, but brutal? Pretty harmless and low impact I would have thought:

https://i.stuff.co.nz/life-style/homed/houses/131787058/are-blenheims-b…

Very similar to how my Uncle Malcolm would build. Solid, not showy, practical.

I agree. If built well they will be good homes.

And far from ‘brutal’ looking. Will probably stand the test of time better than some developments showing more ‘design flair’.

Yep, I hear so many people complain about red tape and burdensome regulations then turn around and praise council's that stop development on aesthetic grounds. It's a big part of the problem.

Cities that grew and become powerhouses like New York and London were allowed to grow organically. Artificially crippling growth through stupid council restrictions is a good way to hamstring your economy and keep a nation poor.

We won't be at the bottom till there are almost no articles or comments on house prices on interest, except for historical articles reminiscing on long past price behavior - we'll have to stay there for a good long time (multiple years) before you can call the recent madness over.

The one thing you can rely on more than death and taxes, is there will always be articles and comments on interest.co.nz about housing.

People are obsessed. Especially those who seem to constantly complain about housing.

Accurate comment

at the bottom HW2 will become correct after a gd 4-5 years being wrong

And there is a good reason for the obsession, beyond any self interest (noting I and many other ‘complainers about housing’ actually own homes). Ponzi housing markets are a social and economic disaster. Just look at the aftermath of the Irish bubble and property crash. Or Japan.

September 2023. First 0.25% cut by reserve bank. First Home Buyer Grant will be increased 50% 7500 per person for existing home 15000 per person for new build. Income cap increased to 200000 for a couple.

Existing 875k price cap should be about right by then.

Maybe a government backed mortgage via Kiwibank at discount rate fixed for 2 years.

To coax the last of the viable buyers into the market and bail out the developers in Auckland who will be in serious poop by then.

National will come out with their own competing policy. Hopefully they read the room and don't relax the measures against investors.

I am sure National have clearly stated their policy is to reintroduce ability to deduct interest from profits.

I do not think this will encourage many to suddenly jump in, but at the limit it may allow Ma and Pa to cling onto their one rental.

As an investor you would continually worry that Labour may get back in and reintroduce this.

I think that will leave brightline where it is, not much capital gains nowdays anyway.

Even those things wouldn’t turn this crash around. Unless the FHB has a really decent deposit, they are still faced with a mortgage of 650-700k. Even with a household income of 200k that’s borderline in terms of serviceability at 6-7%, certainly extremely borderline when stress tested at 8-9%.

It would require something really silly like California’s recent approach to have a chance at salvaging this sinking ship. I don’t think even NZ’s government is dumb enough to do that.

how does this square with the headline that a record number of homes are being completed ? Once completed they presumably change hands from developer to new owner. Are these sales counted when bought off the plan or when settled ?

I thought they counted as sold when the title transfered, so would depend if you purchased the land then contracted the build vs you buy land/house at the same time .. after the build.

Defintely not off plan as titles often not even issued at that stage.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.