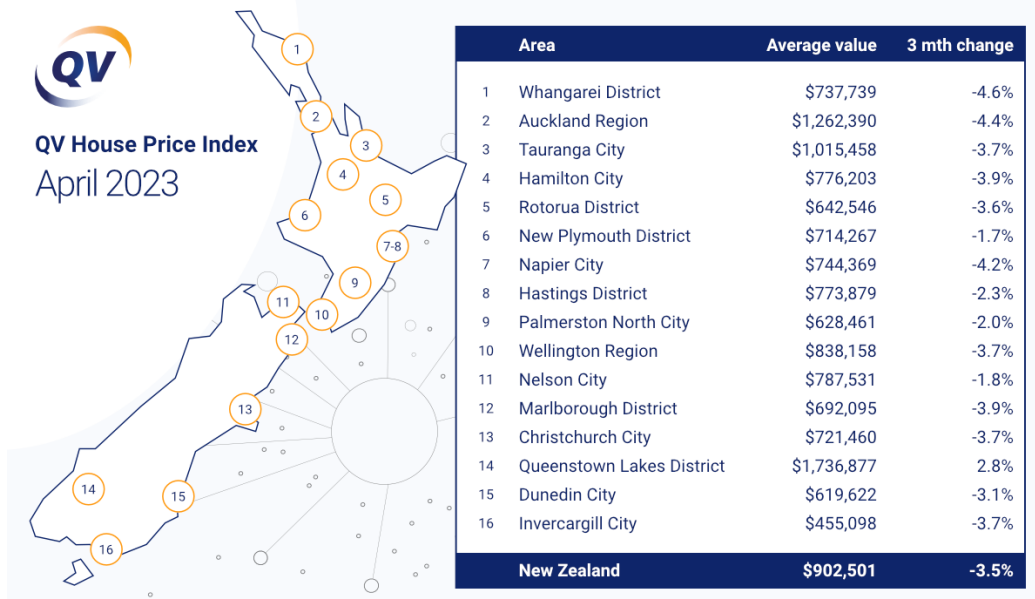

Housing values are continuing to decline around most of the country with the national average dwelling value continuing to fall by more than $1000 a week.

According to the QV House Price Index, the national average dwelling value was $902,501 at the end of April, down by $5236 compared to the end of March and down by $161,264 from the value peak at the beginning of last year.

According to QV the average dwelling value declined by 3.5% over the three months to the end April, which was a slightly slower rate of decline compared to the 3.9% decline over the three months to the of March.

Around the country, Queenstown-Lakes was the only major urban district to post an increase in average values, up 2.8% over the three months to the end of April.

However Queenstown's figures can be volatile due to the small size of the market and the April figure followed a 3.2% decline in average values over the three months to the end of March.

All other districts posted ongoing declines in average values, ranging from -1.7% in New Plymouth to -4.6% in Whangarei (see the chart below for the latest regional figures).

"The real estate industry is continuing on its steady climb back down the mountain of very significant home value growth we saw in 2020 and especially 2021," QV national spokesperson Simon Petersen said.

"It's still a long way off pre-Covid levels for the most part, but this corrective cycle isn't over yet .

"It still looks as though the market is destined for a difficult winter ahead," he said.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

213 Comments

Is it a buyers market with values steadily declining ? Wouldnt want to get the timing wrong and possibly loose 100k in the next 9 months now would we....lol

It is only a buyers market if the vendors are realistic with pricing and expectations. Things are improving slowly as sales pricing gets locked in after many elongated settlements as the chain of houses selling and waiting on others to sell as a condition finally follows through. Updated pricing forces REA's to have to lower vendor expectations or have more realistic chats with them if they are wanting to sell. Have spoken to several REA's who have had said chats with vendors over the last few weeks, some vendors seem to get it, others still thing they can get over RV by a margin. Those selling who aren't clued in on the market still seem deluded and think it is 2021 but time on the market or deadlines for getting their next house is chomping down on these expectations anecdotally from my area.

don't try to catch a falling knife...

We are talking about a house to live in and debt to service for 25 years. Completely different from the stock market - but I like your attempt to use stock market lingo for the housing market.

More evidence that our residential housing market will remain broken until homes are significantly removed as the tax free investment vehicle of choice. A simple solution would be to tax capital gains at 50% that way boomers might actually pay towards their healthcare and super costs, without bankrupting the country.

The "massive surge" NZ is experiencing in net migration is helping alleviate the country's "excess demand" for workers, BNZ economists say.

I guess some of these people will be taking part in the buyers market. Will they look back in five years time and think the price they paid was good or bad?

The commentary always seems to suggest that this is just the COVID-era froth coming off. Remember that we already had a world-leading property bubble long before anyone ever scoffed a bat in Wuhan. Prices are not just heading back to 2019.

Totally agree. They were way overpriced for the last decade. I’m amazed people don’t see this. Try comparing ordinary house prices in NZ with those in other western countries - it’s shocking. And such a waste

The instructive part is that most western property markets are also way overpriced. After 15 years of ultra-loose monetary policy, most asset classes are. The fact that NZ property still looks expensive by comparison really puts things into perspective.

Real Estate everywhere isnt cheap. In fact, in quite a few developing nations, it's even more expensive again. I've seen some fairly basic houses in places where the average wage is 12 grand a year with asking prices in the 700-800k range.

The only places it's really cheap, are where people don't want to live.

Pa1nter please give examples of countries where this is true a 12 k average wage and house price of 700 k.

Places like Sri Lanka, Bhutan, parts of India, South East Asia. And most of their interest rates have been over 10% even before covid.

They obviously didn't get your memo about how average incomes must dictate the price of housing.

Would be good to see these houses worth 700 - 800 k in area’s you are talking about. do people just rent them on 12 k a year.

Picture a 200m2 2-story cookie cutter townhouse on 300-400m2 of land. The sort of thing you see in most suburbia anywhere. Or an equivalent sized apartment in a decent area.

People on 12k usually live in something a lot more sparse, or with many more people.

Main point is there aren't too many places around the world that are popular, where you can pick up a new house like described for peanuts. There's obviously cheaper places of lesser configuration or somewhere less in demand for cheaper though. Or there's a different ownership structure, or its being subsidised with mineral or petrochemical dollars.

What people are complaining about is a global issue.

There's reasons we don't really compare ourselves to these sorts of places though. Often they are multi generation dwellings with a few adult kids and parents all working living under the same roof. Take household incomes and its usually a different story.

Very different countires and cultures in general.

New Zealand's population density is 18 per Km2

Sri Lanka's population density 354 per Km2

India's population density is 481 per Km2

Bhutan's is actually pretty close at 20 per Km2 but I wouldn't think it's particularily comparable to any country in the world let alone NZ.

You can get houses much cheaper in NZ where it's more sparse. Prices everywhere increase when people concentrate - it's the increased competition and demand that makes them more expensive.

I used developing world examples to illustrate it's not just a first world issue. So there's also many, many cases of unaffordable housing in Western nations also.

It's a general exercise I do whenever I go anywhere, find out what people earn, what basics cost them, and what it costs them for accommodation. It's rare I'm somewhere and go "wow, that's cheap" - in recent times I'm actually getting shocked by how expensive previously cheap third world places have become.

I don't disagree that it's getting more expensive everywhere, but in comparison, New Zealand is amongst the most unaffordable, at the peak of the bubble even the regions in NZ that were previously "affordable" were getting priced out of reach for most median wage earners. Especially for locals in those areas, easy to afford a west coast house on an Auckland salary, but good luck getting an Auckland salary on the West Coast.

True but if you are on minimum wage you are a fool to live in Auckland better in alot of regions to live well on minimum, low income and still have a reasonable lifestyle

Guess it depends on your career a bit. Lots of jobs are only available in major centres but ideally, they pay over the minimum.

The main issue lately seems to be wealthy out-of-towners have pushed up land prices in basically every town in New Zealand. No place was left untouched by the speculation bubble encouraged by low-interest rates and money printing from the reserve bank. At least in Australia, USA and Canada house prices didn't go up quite as unilaterally as they did here.

Many of them might get burnt though, renters in regional places can only afford so much rent and aren't going to be willing to live like cattle in sharehouses. Not to mention a lot of investors have completely ignored rental yields lately, e.g "topping up the mortgage".

Guess it depends on your career a bit.

Or your willingness to change it.

"Must keep ....doing.... Shitty desk..... Job."

Not all desk jobs are shitty. There are plenty of fulfilling careers that can only be found in major centres, and plenty of shitty jobs out in the regions. The reverse is true as well. It all depends on what you want to get out of life.

They're not, but that's the main job type that cities offer that regional areas can't.

And if it's not providing you with the material wealth you anticipate, maybe it's not that great a career, and more of a badly paid hobby.

Well people must absolutely love those shitty jobs because they keep flooding into the cities on worldwide scale ...

Some thing become relative.

I won't disagree Auckland is a very unaffordable place to live. Just not as exceptionally unaffordable as some people need to think - so the model many nations and cities are following, clearly isn't beneficial for many of its inhabitants.

It is all relative but really we should be comparing ourselves to places that are doing better than us, just because things could be worse doesn't mean we should be content with letting it get worse.

We do that, but most of the shining examples aren't in a way that NZ can replicate, and are down more to luck and circumstance than any planned effort.

It's almost like there's an unwritten law that the great unwashed will only get a certain level of prosperity.

While it may be tempting to adopt a defeatist attitude and believe that we are limited by factors beyond our control, it is important to recognize that progress is possible when we take proactive steps towards improving our circumstances. While it is true that other countries may have unique advantages, this does not mean that we cannot learn from their successes and adapt their approaches to our own context.

It is also worth noting that achieving greater prosperity is not solely dependent on luck and circumstance. In fact, many examples of success in other countries have come about through a combination of strategic planning, effective governance, and collective action from the community. By working together towards a common goal, we can overcome the challenges that currently limit our prosperity and pave the way towards a brighter future.

It is important to avoid complacency and instead focus on identifying tangible solutions and taking action towards realizing them. By doing so, we can create a better future for ourselves and future generations, rather than resigning ourselves to a predetermined fate.

I'm talking more about causality than predeterminism.

What are these many examples of great planned success you mention and how transferable are they to the New Zealand experience? Where is this utopic, well planned civilisation with high paying jobs from non-evironmentally dependent sources, and really cheap housing and cost of living?

Switzerland, Austria, South Korea, Japan, etc. Not utopic at all but there are different ways of doing things than what we have been doing. We aren't going to be able to replicate any country's success but we can try to learn some lessons from them and implement them here. Austria for example has some excellent policies on affordable housing. Of course, talking about stuff is a lot easier than doing and a lot of countries are successful because of geography and demographic realities that made them that way.

How have these countries demonstrated what you're saying, and how did they fund it?

Like Japan has awesome public transport, but it needs that sort of population to support it.

Switzerland is Europe's bank.

How much more affordable are houses in Vienna and how many people own houses there?

Pa1nter I can't be bothered doing this again and getting dragged into a massive comment chain. How about we agree that you are right and I am wrong?

If there's a genuinely better way we can have a better society, with real world examples then I am all ears.

Are you though? Every time commenters bring up improving productivity or upping R&D spend as one potential way of improving the economy you state (without any of your own facts by the way) that they are wrong and nothing can be done and that we shouldn't do anything about it.

I can point out two examples of South Korea and Israel spending massive amounts on R&D and having corresponding gains in GDP growth and moving up the HDI but you will say these aren't comparable and there are no lessons to be learnt. I can spam a bunch of links that people smarter than me have written below showing that government R&D exepnditure has a positive effect on the economy and improving productivity but will that change your mind? You could probably find some saying the opposite but from what I have looked at everything seems to say that investing more in R&D generally has positive outcomes.

https://ifs.org.uk/sites/default/files/output_url_files/bn12.pdf

https://www.weforum.org/agenda/2023/05/government-research-development-sustainability/

https://en.wikipedia.org/wiki/List_of_sovereign_states_by_research_and_development_spending

https://www.economist.com/briefing/2021/01/16/the-case-for-more-state-spending-on-r-and-d

https://www.mcguinnessinstitute.org/strategy-nz/

Until approx. 1993, Auckland and NZ, in general, were always about 3x median income. Now it is 8 to 10xplus.

This decline in affordability is entirely due to 'planned effort.'

NZ is becoming more 'unwashed' entirely due to these 'written laws.'

I disagree with you on quite a few things but on this we agree 100%, we are where we are through design.

Sadly, entrenched entitlement mentality to receive free wealth from housing has screwed up NZ society.

The problem is thou that's like comparing apples to oranges example which everyone loves to do Aussie. Aus mines it's resources what does NZ do with its resources and yes we have alot. Reefton is about too open a new Gold mine looking for 1500 workers over the next couple of years closest city/town Greymouth. Look at were the highest average income in NZ was Taranaki why gas and oil. But even with these few NZ examples we still do not use our resources cause of a few people who think our 30 percent land mass which is in national parks should be kept that way never mind they then turn around and say they want higher wages free tertiary free health care and owe climate change then rush off to Aus. Look at the greens trying to stop the Aussie miner billionairs company looking for rare earth in our national parks but then turn around and say let's all drive EVs so long as we pollute and corrupt other countries who cares

But you just did compare NZ to Australia, and then described what we could do to replicate their success. Every country is unique but there is always stuff we could be doing better, of course talking about it is a lot easier than actually actioning that into real solutions.

No just showing if you want the so called wages and standard of living Aussie has that everybody loves too say is better then let's us our resources but we don't then we can't complain. You mentioned Switzerland a few comments back. How would you feel that only a few generations ago the Swiss banks took care of Hitlers etc money. And upto only a few yes ago Swiss banks were there for dictators etc. Ok to compare lifestyles wages now but let's look back over a couple of generations because as you know and zi the country takes time to develope its economy

I'm not actually disagreeing with you here, we can't compare ourselves directly with Aussie as they are both more willing and more able to extract resources to fund their lifestyles, and even if we did Australia is the oldest, lowest and flattest landmass on earth, it's a lot easier to mine than mountainous New Zealand would be in comparison.

But at the same time, we can look at what other countries are doing and try to apply it ourselves. For example we will never have the banking system and ancestral wealth of switzerland, but we can look at their education system and economy to see what could be done differently here potentially. Globally speaking we are still a very wealthy and well educated nation but none of that is a given and requires consistent work on both a governmental and personal level.

Median price in a Bhutan CBD for a home is less than $330k nzd. Where are you cherry-picking $700k from?

The cities.

Houses in the sticks aren't worth much at all.

One needs to be more specific than throwing out unsupported assertions. Tagaytay , Luzon , Philippines... A tourist town above Taal lake, elevated , cooler climate, 30 k nzd, buys a perfectly good masonry home of 4 bedrooms on 2 levels, small lot, but freestanding. Crew leader in a fast food restaurant like Jollibee can earn 8 k nzd a year,so the DTI is about 3 to 1. I know people in that situation,now. That's a specific example ,and where millions of locals ,there,would live ,if they could.

Yeah I can find examples of cheap places to live. But they're examples, usually somewhere quieter or 2nd tier. I can get a shack in a field in nowheresville Cambodia for $10k. Or provincial Italy.

Main centres most places are a lot more expensive though. There's nothing overly special about NZ.

Not " nowheresville" to middle-class locals . Luzon has 10 million people, Tagaytay nearly 100 thousand, and highly preferred location. Auckland is equally " nowheresville",pa1nter, if you want to be parochial, just continue, painting yourself into a corner fairly quickly.

I'm sure its nice, and people live there, but it's not Manila, is it? And Manila, is not an affordable place for the average Filipino - it's one of the world's least affordable cities.

I'm not trying to make personal jabs mate, just pointing out for people who think Auckland is uniquely unaffordable. Property follows fairly similar rules anywhere you go.

If we want to have a discussion about "places with cheaper housing", I can find examples all day long. They're unlikely going to be palable for most though, they usually want to live where everywhere else does also - and get surprised why they can't compete on pricing.

No, Auckland is one of the most unaffordable places in the world to live using actual metrics not anecdata like you're peddling. Stop digging.

"After 15 years of ultra-loose monetary policy..." + Baby Boomers retiring + AI making more (memory-intensive) skills redundant...

Black Swan, anyone?

....+ Brightline + removal of mortgage interest deductability + ringfence investor property losses...+ ?

The black swan is here..and few have noticed. GPT etc. The job losses have hardly started, the educated middle classes will be smashed.

I cannot understand the lack of commentary - I'm wondering if this is going to be so terrifyingly bad that it's not too be talked about.

UBI will have to be on the table soon.

Can you provide a list of jobs that would be made redundant by GPT? Curious to know.

Not software development or architect.. yet.

I use it daily, it makes me much more productive. However, you need to watch it very carefully. It makes mistakes, very confidently - this is not something we're used to when working with a computer.

I think it will cut into call centres hard over the next few years. It'll deal with mundane tasks.

Yes agree...you need decent knowledge of what to query to pick up errors - at the moment. I disagree re timing of years. This tech is learning lightningly fast - I follow a few geeks on twitter who are right into it. The deployments, add on etc are extraordinary.

I experiment with it mostly - though have used it to summarise multiple page reports into a couple of paragraphs. Done in seconds.

I agree that it will be capable very soon. It's just a case of integrating the right technology, voice-to-text:GPT API:text-to-voice. Then providing the appropriate pre-prompts to stop it from being abused.

As always, the challenge is deployment. Most businesses, especially in NZ, are slow to adopt.

It'll have an interesting effect on the legal industry. The tasks of legal research and documentation could be simplified a lot, which leaves oratory and...what else?

I use chatgpt (and copilot daily), actually my entire household uses chatgpt now. I encourage my team of developers to use it as well. However, it can make you lazy and you can rely on answers without really understanding the underlying changes. If you don't understand something it is easy to actually waste time, especially on edge cases.

I don't think anyone really knows what their industry will look like in the future, but I don't see any significant job losses on the horizon in my industry (software development) because of ai. Worst case, I will just start a new career as a prompt engineer!

Maybe people that don't adapt to this new technology will drop out of their industry but we've seen that many times before, but it feels like we are going at a breakneck speed at the moment. Anyway, I think we will become vastly more productive though, and that is a great thing.

The easier question will be not will not be made redundant..

A start - IT, accounting, finance, journalism, social media, Law, Medicine, consulting, advisory, education, music, video......

If you haven't started using you are already getting left behind

In that scenario, it won't be just job losses but entire industries going out of business. If people could attain all those services without having to buy them, businesses won't be able to sell anything that AI can't offer on the cheap.

That means the global economy will hit a deep recession and would succumb to widespread job losses. Sounds dystopian, but not impossible.

It'll be like what happened to Western Manufacturing. The value of many people's time will be eroded, but for a smaller subset, increase greatly.

Seems funny if you are into dark humour - we spent all these years de-industrialising our economy on the promise of high-paying service jobs that never arrived in the expected numbers and could now vanish into thin air.

It's like your aspiration of sweet productivity gains - the lion's share of additional wealth generated will go to the owner of the capital, not the worker (except a diminishing handful of workers).

Don't worry though, we will enable all sort of financial and legislative measures to retain full employment. Just mostly doing stuff of really dubious value.

That's why I called it a black swan. Its landed, flapping around on the pond and we are still searching the sky for ducks!

I wish I were a geek so I could really get on top of it. The smart ones will be and those are the ones who will keep their jobs - while the office shrinks.

The way I see it, this tech advancement will once again put talented/experienced STEM workers in the driving seat. Think about all those wasted years and billions of dollars on public university funding for pumping out grads with degrees in international relations, literature and commerce.

I think it will be the STEM careers that are more at risk. These jobs require people to learn specific information and rules and apply them, very easy for AI to replicate.

The other degrees you mention rely on an understanding of human nature, something AI is yet to master.

Moral philosophy education wasn't wasted, though. STEM is tool-oriented, but the challenges of AI are far beyond the tools. Interesting discussion had in books such as What We Owe the Future.

Teachers. AI makes homeschooling a breeze. And with the racist, revisionist, socialist rubbish that is currently being taught in schools, I expect it will become an increasingly popular option.

Kahn Academy has been around for years and is amazing (and free). Tried talking to kids teacher about it years ago….no interest at all.

It's because teachers are not in the business of just passing on information anymore (learn by rote) as lots of the old timers are used to.

Kahn Academy is amazing but can only replace a very narrow part of what teachers do.

Like you say it's been around for years and yet people still pay mega fees to send their kids to private schools. Why do they do this? We'll because of the high quality teaching by ... drumroll ... teachers ... not AI.

Well the real intelligence is pretty shocking, perhaps AI will improve things.

Your job is (probably) safe from artificial intelligence | The Economist (registration gives 3 free articles/week)

I've been using these AI products as a software engineer. Based on the number of tickets I'm completing I would guess its boosted my productivity by maybe 20% and I'm just pocketing the extra billable hours.

Having used it pretty heavily I think people are underestimating how long its going to take to actually replace peoples jobs other than bullshit paper shuffling type makework.

I mean, a car first drove itself across america in the 70s. 50 years later I don't trust my tesla to stop itself at a stop sign reliably.

I've had the same experience with AI tools at work. GPT or otherwise can provide generic advice but not cater to project-specific needs, especially the more complex ones.

In fact, these tools have the potential to supplement the skills of workers instead of replacing them altogether. The ones caught in the crossfire will likely be grads across the board who normally learn on-the-job by handling the mundane paperwork and reporting for their experienced team members.

This will only aggravate skill shortages as is already the case: businesses in the West experiencing high labour costs will automate entry-level roles. However, without the training pipeline, experienced will have to be imported from elsewhere, while under-skilling and underutilisation will grow in the local economy.

Property prices are composed of 2 components-Land & Improvements. Now that the tide has gone out what is now in full view is the different value of the buildings. Modern double glazed buildings are performing outsized compared to old unimproved houses as the market understands the astronomical cost in 2023 to put up a new building, and if the building being purchased is near new in style and appointments the market understands. Thus in this market great houses are rising in value, and poor quality houses falling much faster-far greater declines versus rises-which may explain the Queenstown difference with all its new construction. But the Building is only one component. When one views sales of bare land the rest of the story is told. It is Land that is falling most in price.

And regards NZ Housing Prices versus other Western Countries that difference in cost to put up a building is what really looms large. Double the cost or more to construct a building in NZ is a component of our House Prices that cannot be solved due to small population's inability to provide benefits of mass production combined with a high GST component-nearly $150,000 on a million dollar build.

Yes it is dearer to build in NZ but the largest % increase is the cost of buying raw land and bringing it to build stage.

Compare a 4brm dble garage house on its own section in Auckland with a London bedsit and yeah prices are high but find the same 4brm house in London and compare also try Singapore wereby you buy the apartment but only for 99 years don't compare apples to oranges

Not the most up to date figures, using 3 month rolling average of settled sales. Note they give a market peak in early '22, and a 15 percent drop since. I dont think that adds up to 2019 prices.

Did not sleep well under the pressure of housing price drop? Good news is I found the diving speed has slowed to some extent this year

It represents what's happening in the market.. prices slowing declining..

Another day, another dollar poorer, eh?

Where are the green shoots? What you think seems to count for little HW2 you have been wrong from the top thats 256k wrong in Auckland plus!

Where is the collapsed economy, crashing sharemarkets and deep unemployment. Isn't that what you predicted.

Real pain is coming HW2. It must, for I have bought all these cases of popcorn.

Hi Pa1nter,

You’ll get fat/fatter (not wealthy) if you feed your face with popcorn. 🍿

TTP

Bank default provisions at historical HIGHS you fool. Open your one eye!

Triggered?

With the exception of housing, none of the predictions you've made since last year have held water.

Housing and property is your true love so its only a matter of time before you will get back together. It may be difficult though, since you have cleared your mortgages, invested in a large block with no return, and the test rates being what they are

I mentioned in another post the massive sales slow down in my leisure based import business, we are seeing sales back where they were 4 years ago (covid was a boom for us), roughly 35% down on last year.

HW2 house price’s are falling this crash is closer to beginning than the end and has a couple more years to play out and when it finally hits bottom it will stay stuck there until wage growth and inflation enables average wages earners to purchase a home at 4 x DTI. Anyone who is over leveraged and purchased property in last few years will unfortunately see huge financial losses accelerating housing market’s decline.

The good thing is that its possible to make any claim about the longterm and never be proven wrong.

Right now, there are a lot of factors weighing in favour of property values

Facts are if you purchased a property 18 months ago that property is now worth around 20% less the next 18 month will probably be the same.

by HW2 | 9th May 23, 8:48am - "Right now, there are a lot of factors weighing in favour of property values"

Rhetorical question time; Would these factors be based on the same guesswork that you applied in Nov-21? BTW, is your money still on Grant Robertson backflipping on the removal of the fuel subsidy? Have you had some more thought about the intention behind possible implementation of DTI and its effect on property prices? Some debt junkies need protection from themselves! You really need to take some of this stuff more seriously.

I know you would have had me sell out as you told other 'specuvestors'. Then I could be like IT GUY and gloated about creaming all the gains while some other poor sod got dunked.

Yeah good plan RP, I suggest you stick with TDs

by HW2 | 9th May 23, 11:22am - "I suggest you stick with TDs"

Thanks - I will. Given the times, its a no-brainer.

No work today Mr Not-Retired-Poppy. You've reduced yourself to making snipey remarks at people you don't know, is that something for you to be proud of

Yawn...get a hobby.

Does that upset you while you wait for customers. Go get a hobby yourself, no one is forcing you to read my comments. The sooner we have less snivelling remarks like this the better imo.

You literally flood the comments sections with snivelling remarks ...

Dear boy, it can't be easy for you. Where's your hanky.

Best time to sell was yesterday next best time is today.

Notice desperation starting to show up in RE ads..

Vendors realizing with every passing day, their house is worth less..

We may not get snow this winter, but the housing market is sure to feel the chill

sounds like spoken word poetry:

I'd rather have a house worth less than a house worthless

I’ve been looking for the past 6 months in central Auckland suburbs but I feel vendors are still delusional with their expectations as 1.2M still barely buys a 3bed polished turd it appears.

I have a 600k deposit (!!) and will be borrowing about the same. However a 600k loan repayments at 6.5% plus rates/ins gets me to just shy of 1k/week!?

I don’t want that hanging over my head.

So I’ve put the 600k into TDs and now booked to go have a look if there’s anywhere better to live overseas.

Suggestions welcome!

Adelaide or Perth

Hahaha lol

I’ve been looking across Queensland, there is a real mix of properties at affordable prices. In comparison to Auckland it’s dirt cheap. And while I like Auckland it’s a small city in a the back arse of nowhere

That's because Queensland is an expansive state, with sections worth nothing, and Auckland is a relatively small piece of dirt wedged between two harbours and a bunch of hills.

True but incomes for my role are significantly higher, therefore offering a better standard of living. I used to love flying into Auckland when I was based overseas, unfortunately it’s just a rat race now

Well, it's potentially a higher level of disposable income. "Standard of living" becomes a more subjective proposition. The places I'd rather live, generally poorer, because I enjoy less stuff around, not more.

You do know there are other parts of NZ best financial move I ever did was shifting from Auckland to Taupo.

Pa1nter although you say Auckland is a small piece of dirt, most of it is suitable to build on - only about 500km2 of the 5000km2 is urban area. Its the urban containment policies that has boosted prices into the stratosphere and driven young people to cheaper regions

Auckland drives NZ prices - so should the restrictive policies be reversed - and house prices return to normal long term averages which are well under a half - then the internal migration would also reverse and people will leave the regions and move to Auckland.

This makes any debate about NZ houses price rises/falls almost meaningless unless you have an insight into which way a Govt or the AC will go on Auckland zoning policies.

Adelaide is a great city, lived there for 3 years.

I’ve heard nothing but good things about Adelaide, it’s on my list of possibilities

It’s really good, pretty affordable compared to Auckland. Easy to get around.

Great place if you love food, wine, culture and sports… have I covered all bases?

Have you been to Wanganui. Another great place

Are Whanganui building a new AFL stadium seating 60k?

No but they are replacing the rotten wooden velodrome at Cooks Gardens (which was not that old) that had no roof (so it rotted) with a new one that has no roof.

Ratepayers are not so happy.

A bit of kiln dried laserframe will have it sorted in no time.

For 600k you could live somewhere way cheaper, not work, and rent for about 20 years.

I think you will find the plan for most is to escape the endless rent enslavement of bank debt and their proxys, the speculord.

"freedom" is a very attractive proposition for many people.

It's rarely free though, theres always a cost to be here.

Indeed. The single biggest cost is a roof. Why is that. Time to vote is approaching.

Land and or CGT approaches...

It's the largest cost because it's one of the only substantive things we still make in NZ, and most of your other stuff is made by indentured servants.

You've built dozens of houses and own 4-5 still, no? You should know this.

Disagree. Our business related exports and IP development is where it's at.

It may be that many lack the creativity to build a real business. They fall back on lazy investing in "it always goes up maaaaate", all built of exploiting their fellow man via endless rent, with a side of tax avoidance.

Example. Look at the blokes in the SI that made a blow up artificial surf wave on the News last night, Rocketlabs, Xero (typo), Ōtepoti Games, Ziwipeak and on and on and on.

LOL, you used tax avoidance and Xerox in the same post.

I'm not sure what any of that has to do with the fact doing stuff in NZ is pretty expensive and building a house involves a lot of doing stuff in NZ.

It's good to have cutting edge businesses. I've had technology businesses and I'm always looking for how to deploy or develop new technology in what I do. But most businesses don't need to be a primarily innovative entity. In fact, I think some businesses try to be cutting edge, to their detriment - they lose sight of the fundamentals. Case in point; it's better to have automated customer service, unless you're a customer.

Left renting behind, bought a yacht for less than half of what a house would cost me. Live and work on the sea now. Currently working from the mid South Pacific.

Dont miss the traffic...

That's the best strategy for now. If prices drop significantly then NZ can be a great place to live again. if they don't somewhere overseas is a better option. Think wider than Aussie, their central bank is a total disgrace in terms of protecting property prices and immigration beyond reckless.

Agreed - Kiwis probably need to look beyond the English-speaking countries for their OE, so as to bring back a work culture that doesn't breed the same speculation, migration and/or bulk resource-based economic mindset that we have here.

I lived in central Europe (Graz, Austria) for a work secondment. The biggest difference I noticed in their economy compared to ours is the uptake of advanced technologies among small businesses and their high levels of participation in hi-tech exports.

Much of the advanced manufacturers we have heard of (BMW, KTM, ABB, Bosch, etc.) procure their parts, feedstock, software and tools from several small but very hi-tech suppliers scattered across Austria, France, Germany, Switzerland and even Liechtenstein.

They say about half of hi-tech exports going out of Austria are produced by businesses with less than 30 employees.

That's because those countries you named have traditionally had low interest rates and high labour costs, so it was more profitable to borrow for cheap and invest in high tech solutions that reduce reliance on labour.

27k per year in TD's, you could easily live off that in SE Asia and not even touch the deposit. Take a year off and hang out in Thailand/Bali and rent a cheap place. If you can remote even better. Just keep an eye on the market here and be ready to jump back if you find a place you like the look of at a decent price.

Don't buy in Auckland and you'll have a 30% mortgage.

There is less choice for buyers as stock is reduced

BS there is plenty of brand new stock they cannot sell......

Not really "cheap" though, is it. You're paying a premium for new.

but HW2 says new cannot fall as building materials are going up? is he wrong can new prices fall?

New prices can definitely fall in the short term, because they have an imperative to be exchanged for money (whereas someone can just stay put in their existing house).

What does happen though, is if prices fall future new houses don't get built.

This is not my first Rodeo... The issue is how long the prices will stay low for, RBNZ has inflation headwinds, global economy has a new multi polar cold war, and our banks have to be kind to keep their social license.... So this will play out over many years. But its clear to even Blind Freddy that with our lack of workers (willing to work) we are short a lot of houses. It's the only lever they have to pull on, they always have and they will do it again, You want land that can be subdivided not replicatable shiteboxes. In the meantime we will keep losing 1k a week across NZ, last month in Auckland it was 1k a day !

Auckland is going to bleed lots of people in the coming years. People want more opportunities, and boomers are fleeing to the provinces. It'll also bring in more than it loses.

As for the duration of price decreases or lower values, well that's a multi million dollar question now isn't it.

Thats why I always say with the 6 month moving average turns positive prices have bottomed..... market never runs away from there, perversely credit is harder to get at the bottom then the top. Perhaps because banks are licking there wounds at the bottom, vs drinking their bonuses at the top.

Withdrawn from sale while prices fall. Waiting a year or two will make reality disapear back into the lala land of 2% rates and covid panic...

Yeah nah.

More wear, tear and desperation from sellers as time passes by

by HW2 | 9th May 23, 6:47am 1683571660

There is less choice for buyers as stock is reduced

That's hilarious. There are 00's of new houses coming to market weekly. And the developers are cutting deal to move them. Deals that ordinary homeowners simply can't.

Winter is going to be excruciating if you're a seller.

Especially a distressed seller. (And there'll be plenty of those as the RBNZ's actions guarantee it.)

NZ RE market is still very very expensive and no one should be buying at these levels. Anyone with half a brain cell would know that it's stupid to buy a house at these valuations in NZ.

There are some gullible who fall for the lying tactic of RE agents and get sucked into it.

Newly made shiny shoe boxes are being sold at crazy prices. It takes a village to earn a million dollars, they do not grow on trees in the back yard.

Agreed.

Remeber when petrol/diesiel prices went thru the roof and everybody running around saying OMG we can't live we can't do this we can't do that. Look at fuel prices now they have come back. And it dosnt get mentioned but they haven't come back as far as as they were just before the big rise, yet barrel prices have, yet nobody cares now. And it could drop a bit more but over time it will creep up a few cents here a few cents there but we carry on. And before you know it

Had a look at oil prices and it hasn't really been going steadily up. Historically its current price is pretty average. The price is kind of all over the place when adjusted for inflation who knows what it will do in the future? My gut feeling is that it will trend more upward as the easily accessible reserves get depleted but maybe we will find more alternative energy options by then.

The most important thing I ever woke up to regarding real estate, is that you are not buying an indexed fund of the entire housing market. You are buying a particular property, in a particular location, that has its very own unique characteristics.

Any advice given referencing “the market “ needs to be taken with a very large grain of salt.

If anyone reading this is actually thinking of purchasing, make sure you talk to someone with a decent amount of real world property experience.

Yep I agree, like a "Unique" location that doesn't flood like Auckland is experiencing AGAIN right now.

Of the two property markets, Australia and NZ, which one is better for the first home buyer right now.

That’s like asking if you want the firing squad or the electric chair.

As the choice is binary, buy or rent then you are somewhat right.

The irony is that DGM say dont buy. While also saying landlords should be outlawed.

Not all DGM say don’t buy.

I have said several times that I think there are good opportunities for FHBs over the next 6 months.

Did I miss out the word 'yet". Here it is, DGM say dont buy yet. But in the meantime they dont have much choice but to rent from private landlords they despise.

I remember when I myself got back into the market I had to go a long way down market from the rental to ownership. It was the still the best unforgettable feeling. It helped that I was leaving a landlord who was a complete fickwit

And who is responsible for such a broken rental market. The government policies for last 40 years and the public voting for those governments. The government policy was so bent to favour the mum and dad land lords and this has created those fukwit landlords who own one or two properties and they think they are the lords who should be worshipped by the tenant.

Only if any government had supported better planning for building societies which make better land lords and have tenant well being in their motto as their existence rests on rent paid by tenants.

But but but, look our dumbness have created for the current and next generations. Short sighted political gains of poor leaders we elected.

It’s worth pointing out that the vast majority of landlords and tenants are completely normal reasonable people. We only read about the bad 3%.

It’s very important in life not to read into extreme examples and develop prejudice.

I’m not suggesting you are prejudice nguturoa. Just wanting to make the point as sometimes in nz we all get a bit carried away 🙂

Not at all. LLs play a role. It's the overuse of debt for speculation stack to rinse tax that's the problem. Must say I like TOPs residential rental property. Deposit required is the purchase price.

Aka 100% equity.

Were any of your rentals bought using the method you now denounce

So what is they were?

So after rates, insurance and maintenance its got to clear the risk free rate... that would mean rents are about 10% yield...... no one would buy and the few that had would be able to hold rental auctions.... Not a smart policy or is it just more leftie ideology.

Hi HW2,

Nobody ever accused the DGM of being intelligent or rational.

TTP

Hi TTP

Now thanks to Penny you can be very proud of being Tim Morduant. I have no idea whether you are but those dimwitted DGM like to accuse you and rib you about it.

Nah, TTP has already made it clear he would never want to be associated with Tim Mordaunt. There is quite a few undesirable footprints in Google.

See my comment above "You've reduced yourself to making snipey remarks at people you don't know"

You literally just said "dimwitted DGMs".

What's your point agnost. Anyway my work is done and my forecasts seem to be taking place. Even David Hargreaves is surprised at the results. Am just waiting for house prices to show a change

Yip yip

Both overpriced but the wages and cost of living is a better compensating package in Aussie. 700k kiwis agree.

Obviously you're not keeping up with what's happening in that aust real wages are falling

Main cities in Aus you can't find a rental. Rents gone up by 350 dollars a week. If so good in Aus why homelessness people living in cars why unemployment if the wages are so high.

In Australia you can buy a home, live in it for 6 months, collect your First Home Buyer grants and stamp duty discounts, then rent it out for 6 years without incurring capital gains tax.

Dare I say it...... the prophecy is coming true. Someone get the prophet another login and let's see what the future has in stall for us next!

Careful now, he may say everything is heading to the moon. Get in quick!

What strikes me about Auckland is not just the cost of housing, but the cost relative to quality.

I did Yellow Pages deliveries in the weekend with my daughter as a fundraiser, through St Johns/Meadowbank in the eastern suburbs. I always knew the quality of housing was mixed, but seriously I reckon 60-70% of the properties that I saw were slum-like or leaky. Really instructive, you just don’t notice when you drive.

Pretty eye opening.

And before anyone says, it was mostly not in the leasehold area of St Johns/Meadowbank.

Yeah they are big but leaky. There is a reason why Glendowie and St Helliors cost so much. In general the build quality is way way higher. On the north shore areas like Browns Bay are also a cluster of 70's homes that are past their use date, but built on bad slopes etc. This is why I say that 50% of the Auckland market is really only land value.

Yep, and it’s land value that has really plummeted. Values of full sectioned properties have generally dropped more than townhouses on small sections.

HouseMouse- I wonder if the recent plan changes, allowing more intensive development on many more developable sections in the main cities has also played a role in reducing the crazy prices paid by developers. From memory, you can now build up to 3 houses of up to 3 storeys without needing to get resource consent, as long as the development meets the new site coverage and other rules.

At last! Someone else has cottoned on to this! I've been saying this for months on this forum and for years on others. !!!

Kiwiana02 - Go here: https://www.interest.co.nz/charts/real-estate/median-price-reinz

Select Auckland, and note the flat-line between 2016 and the RBNZ inspired covid madness that started 2020. That's the effect of of the new Unitary Plan of 2016. Compare it to Wellington. And the national average.

But now ... all major centres in NZ must do what Akl did in 2016. And even better, the NPS-UD has forced all major territory authorities to support / enable 6-8 storey apartment building in metro areas. At long last!

Its not just that. Developers are no longer in the market looking to buy crappy old houses on full sections, and overpaying for them. Crappy houses on sections are now just worth what someone will pay to live in a crappy house on a section. Not what some developer with plans to put 6 townhouses on that section can afford to pay. Most professional developers are not buying sections to put 3 townhouses on them, but 6-8 so the ability to build 3 without resource consent won't impact what they buy, as they will always need consent to build more than 3.

It’s usually not commercially feasible to build only three, apart from perhaps in high value locations. You usually need to build 5-6+ to get it to stack up. Although even that’s very very hard now.

The property market is clearly still in decline. One of the issues is that the media raise awareness several months after changes happen. We saw the first month of month drop in Auckland in January 2022 but due to their affinity with Core Logic the mainstream news outlets were still reporting price rises due to the lag at that time.

The seriousness of the correction is now in the mainstream news although many here due to the HPI data have been seeing things much earlier. Vendors are now acutely aware of the situation and I see some sustained drops now as vendor expectation changes fast and there is a degree of panic to minimise losses when a sale is unavoidable.

Yes and buyers can smell the fear....which is why the bid/ask spread is so high

The bulls are fearful hence their incessant comments. It’s dropping beyond their expectations and there is more to come in differing degrees throughout NZ.

Does anyone have any market observations about what is happening for those off the plan sales coming up for settlement?

Especially those where the market price is currently below the off the plan buyer's original purchase price? And there may be difficulty in financing the transaction due to a lower allowable mortgage amount.

Big trouble brewing, but I can’t be more specific.

A few developers that I either do work for or know are really in panic stations right now. Not pretty.

Does anyone know why new immigrants and non residents are not buying these properties?

Non residents can buy new build apartments I believe.

New immigrants, citizens of Singapore and Australia can buy both new build and existing properties I believe.

Statistically speaking, the average person they let into NZ is smarter than the average resident.

Spat my tea out!

The foreign buyer exemption is only for "apartments within a multi-storey development of 20 or more apartments which are purchased ‘off the plan’ (provided the developer has themselves applied for and obtained an exemption)."

From the couple of people I know there is alot of people running around trying to find the money and people are losing their deposits. But also these developers who brought development sites 18 months ago with long settlement and paid a 10 percent deposit are running around. Watch to see what happens to the like of Williams Corp Wolfbrooke etc

A family member sold their North Shore home to someone who withdrew from an off the plan purchase in Beach Haven. However this was a development that had stalled for many many months, not sure why.

In the same general area, same family member has been looking to buy a 2 bedroom house so I’ve been checking out the market for these. Still lots of interest in well presented stand alone houses. Lots of new terrace type 2 bedrooms on market. Most were advertised from $799,000. Not much interest in them at auction. However saw one advertised recently from $669,000.

I've been monitoring about 250 new builds that could be bought off the plans in Auckland around Oct 2021. Some that were selling for $2.5m are now being re-advertised at $1.6m. Many that were "sold out" in weeks are now back on the market. Wording in the ads indicates desperation. (Talking to the agents - if they'll divulge the information - gives a better picture of each situation.)

It's a mess. A total and complete cluster f##k. Winter is going to be horrible.

Yep, carnage coming. All completely foreseeable a couple of years back.

I would rather lose money buying property and renting out than giving my money to some broker to invest in some company wereby the CEO still gets his/her big salary and golden handshake while the company either goes broke or shares drop in value. For the then CEO to ride off somewhere to show up on a different board of directors on a nice paycheck. Meanwhile the broker/advisor still clips the ticket on my money no matter what happens. With property if I f. .up I pay but still beats being in a job as Robert Jones says I would rather be earning 5 dollars an hour self employed than earning big bucks but working for the man.

Colin I think you should be diversified. I know several people who only worked for modest wages yet over the years they bought NZ and International equities on a monthly basis through Craigs and now they have a 5 to 10 million portfolio giving them a fantastic retirement income. Some of them retired relatively young for their age. I acknowledge that they had great timing over the post crash to now years and that it is not so easy to do that now. I for one only have commercial property and equities and a home. I also had the benefit of timing and a bit of luck.

Thing is you are at the mercy of big traders example brought Macquarie Bank at 72 dollars Aus sold at 17 Aus first a broker told me to buy second the short sellers drove price down And finally when Aus govt stepped in and stopped short sellers to late this is 2008ish. The difference with property I can add value myself example brought one property in Christchurch an as is for 140k FHB couldn't do that as can't get a mortgage and or insurance. Right opposite the tannery. Over 6 months brought it upto code and reroofed replied dble glazed etc spent 75k on it engineers etc did it all myself 4 yrs ago lived in it with no windows cold showers etc etc. Valued at 400k after it got signed off not bad return for 6 month work plus now earns 445 a week rent mortgage free. Can give you several more examples of that I have done. And I will never ever put my money wereby I can't control it. Am just starting a new build this week I have enough money sitting there to build it if for some reason I don't then I lock up and carry on living in my caravan and if worst case scenario is I have to go back and swing a hammer for someone else so be it.

Colin we can all find examples of property or equity disasters. You have the problem in that you have tenants to deal with and local authority and government decisions that affect your property investments. The clients of Craigs have two problems. Too much income and not enough to spend it on especially during periods of lockdown. No tenants and minimal costs. They are highly diversified in a number of countries. There will be downtimes for individual stocks which are always offset by stocks that are outperforming. As I said we should all be diversified in terms of investments. I can only think of an amazing amount of capital you have missed out on because you dwelt on an investment that occurred way back.

End of covid lockdown when the economists were picking houses prices to fall. I brought a 3brm house on a quarter acre for 325k in Christchurch spent 235k on subdividing and built a 4brm house last yr so all up 560k rented first house out for 400 aweek the new house out at 550 a week value at 1.2 mill so that was my earning on one property I own plus lived on site rent free. So good profit on one property 34 and 34a Ottawa Rd if you want too look it up for facts. And since 2010 I have only brought property and all my properties even in the last year have gone up as I brought well and I added value can't do that with shares and I won't touch Craig's as they cost me alot of money when they were doing Warrents

You are not listening Colin. The people I talk about put in a million or so max. Now that portfolio is worth close to 10 million. That is hard to beat even with your average at best rentals. You could have done the same but you need to have courage and financial nous.

Oh I am all well and good with advice went ain't your money. You create that like I have done and doing and show me your bank balance like I will show you then I might listen.

Colin I don’t think you would listen to Warren Buffett even.

Since Jan 2003 (20 years) the national average property value has risen from $263,562 to $1,027,121 (Market peak) – an increase of $763,559, or a cumulative 290%.

Over the same period the NZX increased 658%. (No rates, no maintenance, no interest and no insurance premiums to pay - which over 20 years would be hundreds of thousands of dollars)

Colin so the four CEO’s of the big four Aussie banks earning $10-$15m each are mugs are they. They might just disagree with you!

"It's still a long way off pre-Covid levels for the most part, but this corrective cycle isn't over yet.

For me pre-Covid is still the most useful benchmark because it was the last time we ran vaguely sensible monetary and fiscal policy.

Pre-2008 (or even dotcom bubble) might be a more suitable benchmark. Since then its been about dropping discount rates to stimulate asset prices, while importing deflation by using cheap foreign labour (a result of peak globalisation).

Those factors now appear to be reversing.

I can't see why the banks would lend to anyone who's payments would be less than the house prices are dropping.

Which means certain areas (Auckland in particular) are going to see greatly reduced lending, leading to further contraction of prices.

$1000/week pays for a $660k mortgage - so with a 20% deposit, that might be a $825k property. But that property only has to drop another 3% over the year, and they've made zero headway - and if it drops more, they [and the bank] are in a worsening position.

Wow this rain in Auckland is crazy, and way way worse than forecast. Hard to believe how the forecast can be that far out. I guess it’s still far from a perfect science.

Take care out there.

What do you mean way worse ? I heard that the civil defence warning went out to mobile phones hours ago.

Hourly levels of rainfall between 11am-2pm were 6-8 times greater than forecasted this morning. Rainfall was only forecasted to be light-moderate until late afternoon

No trains or buses the CBD was a cluster

the national average dwelling value continuing to fall by more than $1000 a week

In the past I used to often comment that the seller of a particular property made 1,000, 2,000, maybe even 3,000 a week for 12 years straight or something like that. So I guess this rate of fall is not necessarily particularly impressive.

"Stability leads to instability. The more stable things become and the longer things are stable, the more unstable they will be when the crisis hits"

~ Hyman Minsky

Have look at the last few days of Auckland City auction results - those that sold are in free fall!

https://www.interest.co.nz/property/residential-auction-results?region=…-

Just looked at my suburb over the last year from that page:

33 auctions, 21 passed in, 1 withdrawn, 11 sold.

Of those sold, 8 were under RV by an average of 126k (or 12%); 3 were for essentially RV, and 1 (far and away the cheapest with less than half the average asking price) was sold over RV by 275k.

We're now seeing neighbours with mortgagee sales, and the house we live in has dropped below its 2017 purchase price.

6/105 Tamaki Drive, Mission Bay not bad for a mil is it freehold plus body corp ... HW2 at 35% off .... is it a crash yet you spruiker fool?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.