The Government's Budget on May 18 appears to have had little if any impact one way or the other on activity at the latest residential property auctions.

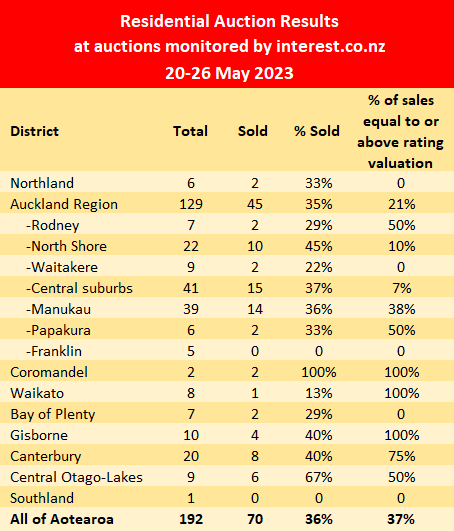

At the latest auctions monitored by interest.co.nz over the week of 20-26 May, 192 properties were offered, almost unchanged from 194 the previous week, while 70 were sold under the hammer, down slightly from 77 the previous week.

However there was no movement in the percentage of sales at prices above or equal to their rating valuations, which was unchanged at 37%, with the rest selling at prices below their rating valuations.

Queenstown-Lakes remains the most buoyant auction market in the country where several brand new homes in a development near Frankton went under the hammer at the latest auctions and the overall sales rate was 67%.

At the Auckland auctions the number of properties offered, and the number that sold, both declined by 10 at the latest auctions compared to the previous week. The percentage that sold for prices above or equal to their rating valuations dropped to 21% from 31% the previous week.

Overall, auction activity remains relatively muted, but is not changing significantly from week to week and any fluctuations tend to be small.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the prices achieved and the rating valuations of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

161 Comments

Deep freeze until the election.

So I've got to wait 5 whole months for 'real pain'?

Popcorn will be cold by then. I'm going to have to go to the park and watch kids fall off their skateboards to fill the void.

by Pa1nter | 20th May 23, 12:55pm "I wouldn't have advised anyone to take up any substantive financial responsibilities since March 2020"

Make up your mind Pa1nter - LOL!

There's a difference between showing caution in a time of upheaval

And gleefully waiting for destruction of others

Yes and there's a clear difference between drawing conclusions based on assumptions as opposed to hard facts.

What, like "no one wants to move to NZ", and "everyone's going to leave for Australia"?

Actually those are less assumptions and more hysterical exaggerations.

Pa1nter, I am more than happy to own part of your dramatized reply :) You can't deny, Australia appears attractive to many right now.

It's always been a wealthier country with more opportunities due to scale, with a relatively open border. Kiwis have been migrating there for a very long time.

'Anywhere else' seems attractive to many people now, because everyone's had 3 years of covid measures, then inflationary fatigue. There does seem to be an air of malaise out there.

You could say that...

“The complete list of Labour’s appalling record just off the top of my head.”

https://twitter.com/mikeall84403276/status/1656898457301549057?t=cktXtTu6v-ahGk4HqEdwlg&s=03

It's not labours record though. That's things that happened while X party was in government.

Otherwise you could have a list tracking things like "number of nice sunsets" or "volume of puppies born" over the last 6 years, and attribute that to them.

he complete list of Labour's appalling record just off the top of my head. * Number of Kiwis living in cars has more than quadrupled since 2017. • Gross debt figure is now $722.62 Billion, up 47% from 5 years ago. • Under Labour, tax take has gone from $86 billion per year when they took power to $118 billion – up 38%. • Retail crime has doubled since Labour came to power in 2017, and 70% of the crimes are not even being reported. • Since 2017, when Labour took power, gang membership in Auckland has gone up 51%. • Labour has taken away all healthcare targets. Every single healthcare metric has gone backwards in the last five years. • Average weekly rent in 2017: $400, in 2023 up 50% to $600. • 37,000 more kids are in benefit dependant homes than when Labour’s government took power 5 years ago. • Labours fast track immigration processing: Only 20% processed with the 10 day timeframe promised by the minister. Setup to process 3500, only got through 169 with only 1 approved within the 4 weeks it has been open. • Labour government has increased consultant spending from $900 million the previous year to $1.24 billion this year – a massive 33% increase, even after Labour increased public service employees by 50,000 since Labour took office. • NZTA has increased staff by 60% in last 4 years (1000 extra bureaucrats). • More than 100,000 students were chronically absent from school. • Government refuses COVID-19 inquiry, despite cross-party support. • 70% of NZ businesses have no confidence in this government to steer them through the economic down turn. • Stats NZ data showed a deficit of $10.5 billion between export earnings and import costs for the year ended June, the highest annual deficit since current records began in 1960. • Ram-raids on retailers have soared under Labour, with a more than 500 per cent increase within the first six months of 2022 compared to the same period in 2018. • Emergency Department wait times are now the worst in at least a decade, with more than one in five people waiting at least six hours for treatment. • Domestic inflation is up 6.3% and has a higher weighting than trade based inflation. • In a multi nation survey involving 12000 people, NZ is now ranked 51st out of 52 countries for best place to live, no.52 was Kuwait. • This was a Government elected to make housing affordable, help those less well off, reduce child poverty, and give us a kinder, more united society. On every front, it could not have failed more profoundly. • 316 foreign entertainers, including 64 DJs, were fast-tracked through MIQ in 2021. Taxpayers have spent $1.2 billion on MIQ – $660 for every household in the country. • Stating that we will be front of the vaccine queue versus being the slowest in the OECD to roll it out. • Patients waiting for specialists for over a year has gone up 17 fold since 2019. • 25% drop in prisoners, just ‘let out’ doing community sentences, while there has been an increase in offending against prisoner officers. Violent crime has increased 21%, gang membership increased 56%, record low number of offences resulting in prison sentences in last year representing an overall decrease of 44% under Labour. • Savings report from Finders that looks at savings data across all the OECD says NZ will record the second to lowest savings in the world at -0.2% (only Poland is lower) compared to the average of +7%, showing how bad the cost of living crisis is. • For more than three decades, the Swiss Institute for Management and Development (IMD) has compiled annual rankings of competitiveness for 63 of the world’s most important countries. Back in 2017 when Labour took power, New Zealand ranked #16 - ahead of Australia at #21. Five years on, New Zealand has fallen to #31, while Australia is now ranked #19. Over the past few years, we have plunged in economic performance, falling from 22nd to 47th place. Government efficiency has also deteriorated markedly from 7th to 17th place. Consumer confidence in New Zealand now stands at the lowest level since Westpac’s Consumer Confidence survey began in 1988. And, perhaps most damningly, for the first time, a majority has a negative 5-year outlook on the economy. • Jamie Ngatata Love – 3rd strike law removed by Labour resulting in his sentence for armed robbery reduced from 10 years to 18 months, with 138 previous convictions. • Sixty-four percent of Kiwis, across all ages, believe New Zealanders are more divided than ever. • Day Jacinda resigns, news pushed aside of food price inflation data released showing the highest rate of increase in more than 30 years. • Doctor GP waiting times are now 5th to bottom of OECD countries (38 countries). Access to GP’s is the first thing to go in a failing health system. • The government collected $78 million more tax than forecast for the five months ended November 2022 while its expenses were up $742m on forecast. • After 6 years of a Labour government, emissions have increased and the importing and burning of coal has more than doubled - all after Jacinda declared climate change is her 'Nuclear free moment'. • Farm conversions into forestry in 2013 = 1, under Labour: 2022 = 31 due to carbon credits incentives, 2017 = 695 Hectares, under Labour 2022 = 18,000 Hectares. At the same time Labour calling foul on amount of slash washing away bridges etc & killing a child in East Cape. • Govt car fleet grown 16% for past 3 years and 1000 of them are petrol or Diesel, their stated ambition on being EV by 2025 is a joke. • New Zealand is now bottom of the OECD for access to modern medicines • Retail crime increased 40% in 2022, with most police districts reporting twice as much as 4 years ago. There were 292 incidents a day last year, compared to 140 a day in 2018. • Ramping hours (Ambulances sitting outside ER waiting to get patients in) went from 3000 hours in 2019 per quarter to 9756 hours per quarter in 2023. Targets of 90% of patients should receive MRIs within 42 days – currently it is 36%, 95% for CT scans within 42 days – currently it is 57%. • Crime: 46% increase in victimisations, 140% increase in serious assaults, 551% increase in ram raids, number of people in prison for that has dropped 45%. • Public sector managers have been growing at nearly twice the rate of frontline workers since the current Government came to power. • Nearly 5000 New Zealand nurses have registered to work in Australia since August. As of March 4th 2022, only 1 nurse has arrived from overseas to NZ. • Burglaries crime stats: 49% under 18 years old, 51% of those did not face court action. 112 between 0-17 arrested received a family group conference - that’s it. Most was just a formal or informal warning. 94 didn't receive any consequence whatsoever. • Much of the bad luck is the result of Government’s own actions. The Reserve Bank only agreed to the inflationary $100 billion money printing programme after the Labour Government gave a taxpayer guarantee. Labour is recklessly running a deficit at a time of over-full employment. Borrow and spend always results in bust. The bank has no doubt that Labour’s borrowing to spend is inflationary. • IMFs 2023 outlook forecasts New Zealand will have one of the lowest GDP growth rates and one of the highest inflation rates in the Asia Pacific region in the coming years. In their projections for GDP, NZ's current account balance is reported as -8.6 percent of GDP, worse than Greece's at -8.0 percent, in 2023. NZ was one of the best GDP performing countries in the world, now we are bottom half of advanced countries in the world with the worst current account deficit of all of them. • Frontline police told to ‘consider necessity’ of bail arrests as NZ’s largest prison nears capacity • 2023: 19,000 nurses have left the profession in the last 5 years under this Labour government. In 2017 it was under 3000 leaving compared to 5000 leaving in last year – a 60% increase in nurses leaving.

Wow

Hopefully enough of the electorate realize this appealing list is true

Very un"appealing"

Appalling😄

Did i mention Co governance, 3 waters, . Treaty payouts, youth suicides? Ute tax, that big waste called Rotorua hotel accommodation,...

These are all driven by labour's idealistic leadership who collectively have little real world commercial or practical experience. Thus the reason why they have so many advisers working out how to manipulate the masses.

youth suicides

It's not really the government to blame for this, it's everyone.

Wow - thay have been bizi bees!

Wow!

Very comprehensive list of the many failures of this Government.

Jacinda will be remembered as the worst PM in NZ history - by a large margin.

Care to make a similar list about Nationals last term? House price increases, rent increases, low growth, government debt increases, south Canterbury bailouts, poor earthquake response, very low infrastructure investment, tax bracket creep, high immigration without infrastructure, constant threat of deflation, wasted flag referendum, people living in cars and motels, no attempt to curtail supermarket, bank or petrol cartels - that’s off the top of my head. Oh yeah also bad handshakes and pony tails pulled.

Yep just as bad for different reasons.

How lucky we are to have such great political parties and political personnel.

Rate Labour worse and Nats bad

Do national have any plans you think will fix any of this? They seem to be the same as labour but with extra perks for property investors. Remember national claimed all through covid that they would have done the same.

I’d happily vote National if they had some decent policies.

Come on be KIND it's only your tax money. I mean they are so transparent and oh let's have a hug. Tounge in cheek

Looks like the list from inside Maga Mike's head.

Not a hinged conservative.

No matter where prices go from now, there will be some people who will feel pain

You're acknowledging the ones who've taken high mortgages and especially the uninspired speculators who bought at market peak

If prices stay up inequality is amplified to unreasonable levels, a lot of responsible families put off having children, smart people are more drawn to leave, and generally speaking a whole generation is living the pain of renting with all its drawbacks

Are you capable of acknowledging even for a second he might be gleefully celebrating the glimmer of hope of seeing this anomaly reverse and a generation having a chance to worry about other things than a basic need?

Many of the commenters on the site are more interested in schadenfreude than correctly framing and addressing issues. Not that that's something specific to here, people have a natural tendency to need to get lost in blame apportioning than objectively dealing to root causes.

The system won't automatically self correct by specuvestors falling by the wayside and things getting more affordable, that's in the realm of wishful thinking. I can't see anything changing significantly without a very large effort into the supply side of things, that appears universal in most housing markets.

The system won't automatically self correct by specuvestors falling by the wayside and things getting more affordable, that's in the realm of wishful thinking. I can't see anything changing significantly without a very large effort into the supply side of things, that appears universal in most housing markets.

Hmmm. So on the one hand you think people are not "correctly framing and addressing issues" and that can be trumped by a "I reckon"?

You can discount something without having a 100% foolproof alternative.

Like food costs. The knee-jerk is "supermarkets are to blame, they're creaming it", but the reality is the cost to produce food is really high. So even if comcom clamps down on supermarkets, there won't be a significant reduction in food prices, because the underlying issue is still there. I can only offer reckons as to how to resolve that in a meaningful way.

Why are the underlying costs so much higher in NZ though? The supermarket duopoly can’t be innocent.

Are they that much higher? Walk into a supermarket in most countries that aren't 3rd world, and it's a similar story. Food inflations pretty high most places.

Our supermarkets net 1% more than larger markets. So even if you pulled that in line, at best you'll save yourself a couple bucks on your weekly food shop.

Duopoly’s don’t just take extra profit, they are also significantly less efficient and less demanding on suppliers.

To be fair a lot of the time when we compare food prices to other countries we forget about GST which is often lower in other countries or excluded on healthy food. And also labour costs are higher here compared to the US, UK, etc due to our very high minimum wage.

Also we seem to focus on food prices when really it’s rent and mortgage taking most of our money. Even worse those “businesses” are mostly tax free (or were).

Really just an example of misappropriated causation.

So with housing, the biggest problem is an inability to supply affordable housing. But peoples need to find a baddy to vanquish has it reduced to greedy boomers, or whatever. Remove the greedy boomers, and it's still really expensive to produce new units of housing.

Until recently you could build a basic house for $300k. If you could find any land you were allowed to build on.

About 6-7 years ago you could get it done at $1650 or so a square metre (build only). Today it's closer to 3 grand. There's a decent list of why that is, post covid work environment, high material costs, rather massive labour and experience deficit, improved building standards and oversight, etc. The freehold nature of most property also adds around 100k in council costs just out the gate.

Even if the land was free, hard getting change out of 500k to produce something fairly basic.

3 grand a metre still let’s you build a cheap 3 bed 1 bath 100 meter house! The land price is the problem.

Only if you're picky about the location.

Can’t speak for supermarkets but if you at look at building materials then the following situation has occurred.

The two diy chains , Bunnings and mitre 10, have a “can’t beat our price” promise. But in essence this means suppliers only supply one or the other….so a brand or product is only in one chain and can’t be compared.. In the case of a product like Simple Green or wd40 then the supplier has to stock and supply two different pack sizes to each merchant. It all adds cost and when marked up means extra high retail price points. There is a court case/com com going on about this but it’s all swept under the carpet.

the gross margins are typically 20% higher than Australian stores because of the massive overheads and low volumes here.so we pay significantly more for many products.

Fletchers and Bunnings cut a deal to not compete when Bunnings entered the market so it just means the volumes get divided by another player….but the overheads increase.

a similar cosy position occurs in the trade area with fletchers and carters. One produces and the gib and the the other the timber. The difference with the Australian market is that large investments have been made to automate frame production. But here the market has 90 or so small frame and truss makers. It’s kind of like an organised cartel because they only sell into their local area, and never have the volume to justify a bigger plant because of this issue. I’m a lot of cases the actual businesses have different shareholders but in work in unison.in many cases .anyone breaking ranks gets pulled up by the frame and truss association.imagine if we had 90 small plants making baked beans…what would a can cost?

Thats one massive generalisation of a whole industry in a few paragraphs.The comer e commission report just really whitewashed the whole lot.the public would probably be appalled if they know what really goes on.

bur hey what would I know.

Like food costs. The knee-jerk is "supermarkets are to blame, they're creaming it", but the reality is the cost to produce food is really high. So even if comcom clamps down on supermarkets, there won't be a significant reduction in food prices, because the underlying issue is still there. I can only offer reckons as to how to resolve that in a meaningful way.

OK. NZ is known as a food producer. Yet the cost of food is relatively higher in NZ than Japan, which is not known as a food producer.

Anyway, I think there's some very smart commentators who give their views on interest dot co. Don't agree that it's just a hodgepodge of schadenfreude.

Japan has market efficiencies being a market 20x the size.

Our minimum wage is 3x what a Japanese supermarket worker gets paid.

"Many of the commenters on the site are more interested in schadenfreude than correctly framing and addressing issues."

That's unfortunately spot on. The reason is simple, they believe that putting others down or hoping for their downfall, will make themselves feel less miserable.

Lol - like belittling people as ‘doom gloom merchants’ because they can see the damage that house prices being so detached from incomes was causing (financial and social).

Haha the hypocrisy always makes me laugh as it’s almost unbelievable

Agreed. That the leverage monkeys are so detached from this reality underlines their psyche, me me me me me.

Narcissistic Sosiopathy.

It's not really any different to demanding someone else does something about productivity so that I can earn more money.

You just underlined my point without realizing it. Well done.

You used a big word back there, but not in a way someone who's really danced with the devil would.

You can want affordable housing without being part of the pitchfork brigade. People baying for blood rarely make great choices.

Wow... You just highlighted the "big words" again without realizing. Keep going. Let's see if you can publicly punch yourself in the face for a third time.

#priceless.

You're using words like "narcissistic sociopathy" to gaslight others.

Could be worth having a think about. Are you secretly Meghan Markle? Do you tell people you have a big heart?

by Pa1nter | 27th May 23, 12:22pm 1685146972

It's not really any different to demanding someone else does something about productivity so that I can earn more money.

Like property investors expecting somebody else to pay their mortgage debt (tenants) by being productive in the real economy and earning wages?

Maybe, if property investors were making out they weren't self interested.

How could they be self interested when they are all providing below market rents and giving shelter to the poor so that they don’t have to live in their cars! (sarc)

Starting to think that some are actually pathological

Yes as has been pointed out before, I've found there to be a high correlation between hardcore property investment enthusiasts and narcissistic personality disorder. Their own financial gain is more important than the overall financial and social wellbeing of the community/nation as a whole.

Note that they will claim that others are 'envious' of their success. How many times have we heard that one!

https://th.bing.com/th/id/OIP.G-kmZZPGI4onJo-pKM91NAAAAA?pid=ImgDet&rs=1

‘Narcissistic personality disorder’ sounds about right.

I've often found it links back to childhood and a poor relationship with their fathers (i.e. they felt inadequate and not loved so they view things like property and wealth as a way to feel more powerful/strong/dominant and to show their Dads how successful they are - in hope they will be loved). Often not their fault, just the painful dynamic of families and pain/trauma that gets passed down between generations.

So often when I'm dealing with those types of personalities (including on this website) then this is what I'm thinking.

On the theme of the scrolls today, the wisdom of the bible suggests:

https://th.bing.com/th/id/OIP.DRESeOn8HKVG5gfmzp8KNwHaFi?pid=ImgDet&rs=1

Don't really agree, what you are describing is just the new normal of today. People just look at their friends and they are all trying to do the same so its just normal. Its just incredibly competitive out there today and although I'm really out of the loop work wise I still see it transfer into every aspect of peoples lives like even down to sports where people can no longer have a "Social game" or do activities just for fun, everything is turned into a competition these days and you have to strive to be the winner. Obtaining wealth is just top of the tree as far as status goes.

There is a difference between a competitive game of sport where you shake hands at the end and go and have a beer vs using leveraged debt and previous capital gains/equity to outbid FHBs who just want a house to live in for their own financial and social security.

One is predatory type behaviour (exploiting a position of power for one’s own gain without questioning the ethics of the actions), the other is not.

Getting into this conversation is like inviting daggers

I think you're using guilt against people for having an investment property to provide for their families and retirement

The govt can't supply all rentals for those who need them

Capitalism's just fine.

Except when it's housing then it's literally worse than Hitler.

"like belittling people as ‘doom gloom merchants"

Yes, of course, it applies to all types of "belittling", not good at all !

Does anyone here have data on house buyer's status.

I presume since Labour killed off foreign investment buyer's have to be kiwis, Aussies and Singaporeans.

But what percentage are nèw immigrants ?

What % are FHBs

What % are investors.

What % are ...

What percentage are property developers?

What percentage are landbankers / land speculators?

https://www.oneroof.co.nz/news/43641

For the same house on a subdividable piece of land, property developers will outbid owner occupier buyers.

That’s a relatively new phenomenon, developers always use to pay less for development land than someone wanting a home. Perhaps that’s an Auckland high density thing.

The stock level is this morning below 12100.

Others here also monitor the levels and will be aware that is the lowest it's been for sometime and has not stopped falling

Please elaborate Houseworks on what you believe this implies.

You're an old boar 🐖🐗 and one of the ones cheering on rising stock levels of 13500. So ask yourself the question

Me being here incites you, what will you do if I come back as HW3

Even when asking a reasonable question about your statement you become this defensive angry little man.

Also, don't think of yourself too highly champ - I give zero f's about a selfish, small-minded little troll like you.

Tofa oe trolling weasel ia manuia le aso.

I give zillion f's about a selfish, small-minded little troll like you

There fixed it for you

Amokk you and I both know you are not interested in my answers. OTY

by HW2 | 27th May 23, 6:58am 1685127493 "lowest it's been for sometime and has not stopped falling"

Yes, its winter and prices are still falling. What will you be spinning come spring when listings once again bloat? Why not measure something useful like "days to sell" to measure market health?

Did they all sell ?

One on my watchlist did

Anyone noticed how, Since selling prices are falling, the sly dogs at RAY WHITE longer list the sale prices.

Also some embarrassing sales are being removed from Homes,con.

The RE industry has to rate below usd car salesmen and politicians for integrity.

Um? I thought stock levels always fell moving into winter?

Now there's a plausible explanation 👍

That's far better than DH amokk having a paddy in front of everyone

by HW2 | 27th May 23, 5:40pm - Now there's a plausible explanation 👍

I would have thought you'd have already known the basics. A lesson for a rookie....

There's certainly still life in the market. If you bought a property in the last two years and want to sell now you are probably out of luck. Back in the old days it was expected that you would lose out if you had to sell within a year or two.

It has only been in recent times that people expected they would be able to make a profit as well as pay the commission after only a short time. People who bought a $4M Central Auckland house on a full section a year or two ago are likely to lose a million. However, they likely made profits in the past and will just have to wear it if they insist on selling now.

Bargain hunters are now active in the market going by the increased number of low bids on many properties.

by Zachary Smith | 27th May 23, 8:32am "There's certainly still life in the market"

Even on this downhill ride there will be life but peoples unrealistic and naive expectations are going through an timely reset. Post the likely introduction of DTI measures, even ones like HW3 will emerge more the wiser😂

How long will it be until you have egg all over yourself. Yes I have been optimistic right through but I notice more and more who are joining the ranks including the reserve bank and the trading banks. This week the rbnz pared back their negative price forecasts. Still, you don't need me to point that out do you.

How long will it be until you have egg all over yourself. Yes I have been optimistic right through but I notice more and more who are joining the ranks including the reserve bank and the trading banks. This week the rbnz pared back their negative price forecasts. Still, you don't need me to point that out do you.

If you think it will help HW, I'll sit in your camp. People will assume that when all is stacked against the bubble, that it will somehow cave in on itself. But what if it doesn't? These are historically unparalleled times. You can't even compare it to the period leading up to the Great Depression (touch wood). So anything can happen and it's very hard to fit a narrative. Just make sure you have insurance.

Insurance like a cash buffer JC and a mortgage free spread to grow own food. If youre a tenant whats your insurance JC, and don't say old ratty, that will go bust

Insurance like a cash buffer JC and a mortgage free spread to grow own food. If youre a tenant whats your insurance JC, and don't say old ratty, that will go bust

There's the expression 'cash is trash' HW. But I 'reckon' at least 24 months of living expenses at hand is useful.

1. Jury is out on ol' ratty as an inflation hedge. Y'day I did a simple calculation to work out how long it would take to 10x in dirty fiat. At today's prices, approx 6 years.

If the kids are smart (and they are), they will allocate part of their winnings on the dogsh*t coins to BTC. And this appears to be a reality. All power to them.

2. Now, if you want to look at gold in Kiwi pesos, going back to 2007, it has been appreciating at a CAGR of 8.4%. That fits within your beloved 7-10 year theory. Arguably, gold is an inflation hedge based on these back of the envelopes.

3. Silver has a CAGR of 5.4% over the same time period as gold. Much less convincing than gold on the inflation hedge narrative. But I couldn't help myself and started accumulating in 2019. Why not? Nothing to lose. And healthy returns of 50-60%.

If things get really out of control, the sheeple are thinking they will be able to borrow against their house for purchasing power. And I think this is potentially a likely scenario. But trust me. They will get reamed on fees. I have no doubt. The banks have them by the short and curlies.

You do a lot of pontificating and analytics, but this does not seem to result in good net positive outcomes.

The energy you spend on this would give better returns working a supermarket checkout and putting the earnings in a standard bank savings account.

You do a lot of pontificating and analytics, but this does not seem to result in good net positive outcomes.

What do you mean "not result in net positive outcomes"? Is there something "negative" about the outcomes of what I just outlined?

I don't think so.

If you think that curiosity and the ability to build your own positions don't come without time and effort, I think you're mistaken. Even better if you actually have an interest in and enjoy what you do.

What do you mean "not result in net positive outcomes"?

I'm saying the return you've achieved for whatever monies you've put in, and the hundreds of thousands of dollars you've spent researching and analysing things might as well had you working in an Asian sweatshop. I.e, not a viable commercial pursuit, more of an expensive hobby.

All relative my friend. And I don't think anyone will sniff at 10x returns on assets such as ETH over the past few years. We might just be getting started too. You're not going to learn these things crowing about house prices at the neighborhood BBQ. Life is for learning.

It's not a subjective thing. You want to maximise the value of your time, if returns are the name of the game.

Otherwise I'll get better returns taking a walk on the beach

You want to maximise the value of your time, if returns are the name of the game.

Sure. But back to the original point: what is 'insurance'? It's a personal thing. And I don't look at ETH as 'insurance' by any means. It's more like owning a programmable internet money.

I'm doubling down on fruit trees.

Sweeeeet 👍

How much does it cost to create a crypto. If promotional cost is large, then start one and call it Interest-Coin.

There's at least a couple of DGM drongoes that would lap it up.

"and don't say old ratty, that will go bust"

There we have it a new Carlos in town..HW2!

👍

A new crypto can be created for a few thousand bucks. Its not something tangible so why pay someone millions for it. Funny how people talk about property pnzi and dont want to pay for a roof over, yet prepared to invest their hard earned in crypto

Old ratty (its not worth me looking up how that nickname has come about) bitcoin and ethereum are simply two of the best known

JC I get 25 percent rental return cash, I wouldn't even glance at 5 or 8. That's before making squillions of capital gains where I put in a few hundred k

Sorry mate that won't tempt me but thanks for the info

As for borrowing against the equity, whatever you do dont take a reverse mortgage.

Sure you do.

Easy JC, bought on a yield over ten percent and grown the income since.

The problem is I don't share one cent directly with Amokk and he is really really angry about it. I give big chunks to the govt but Amokk thinks that's not enough, he wants his cut

Hahaha way to edit housework’s. The classic thing is you bang on all day long spruiking rental property and here I am renting space in your head for free 😂😂

Fa'afetai

Who was the one yesterday who waited all day for my reply, then responded in a flash 🐖🐗

Kia kaha bra

Orr introduced some more optimism in the market this week... OCR peak & reducing LVR requirments. On top of this CCCFA has just been eased up & the immigration flood gates are open. You can hear murmurs around the office & family gatherings that this could now be a good time to get back in... will they act on it?

Lol - the Barfoot and Thompson annual awards were last night Nifty!

You’ll need to wait another 12 months if you’re looking for the ‘RE spruiker of the year’ award.

Was there anything I said there that wasn't correct? It's ironic that you know when the Barfoot & Thompsom awards are... as they say, the haters are the biggest fans.

RBNZ are just looking to merely slow the most spectacular housing market crash in history, that we have here in little old NZ. NZ is always world beating!!

Its far too little and will be ineffective at softening this Boeing 777 into mountainside collision!

A crash course chart for the Times!!

Imgur: The magic of the Internet

Nice graph.

My guess is (unless there is a global black swan in our future) we'll be more 'Merica than Eire. Mainly because the economy is seriously out of kilter (but we could come close given the RBNZ's overreaction).

Onewoof was on yesterday with one of your favourite guests ... spruiker Ashley

No talk of "crashes"

You will only see the truth you want to see there Nifty. I could bullet point the assumptions and guesses that you are making (e.g. OCR has peaked), but in the end I'm likely wasting my time because your bias is that you want to see house prices go back up again for your own benefit. You might be right in all of your assumptions, but equally you could be wrong. We won't know until after events have unfolded and that we can view them in retrospect.

BTW - my friend works at Barfoots and today shared their photos with me (is that okay with you or does that make me a 'hater'?). As an organisation I neither hate nor love them. If they were an 'enemy', the wisdom of the bible (where the scrolls came from) told me I should love thy enemy so my thoughts and prayers are with them in these difficult and challenging times. But then again, given the amount of money they appeared to spend on their awards night and with the performers they paid to be there, business can't be all that bad for them! So perhaps they don't need any sympathy at all?

The truth hurts IO... please observe more closely what is happening out there & stop dismissing anything you dont like. There's clearly been positive news this week for the property market. Being open minded may benefit you more... it can be easy getting stuck in an echo chamber of gloom whilst missing out on opportunities...

‘this week’

Haha ok so your view is based off one weeks data and mine is not (it’s off all the data) but I’m being closed minded?

Nice one Nifty - I thought you were being serious for a moment 😂

The intention of your original post was to try and trigger FOMO - why would you want to create fear for people? For personal gain because you are afraid prices may fall further and hurt your own financial position.

Well said, IO.

All I've been hearing at work and family gatherings is people worried about their rising mortgage costs. Savings dwindling and revolving debt rising, afraid to think what will happen when they start missing mortgage payments.

"revolving debt rising"

So these owners are taking on debt to meet debt service payments?

If the owner's cashflow position remains unchanged, using debt to pay for cashflow shortages in household budgets can only go on for so long.

Can these owner's hold on until mortgage interest rates fall to more manageable levels? or will they run out of money before that happens?

"afraid to think what will happen when they start missing mortgage payments."

It does depend on what the bank will do with borrowers under cashflow stress. The most vulnerable owners will likely be those who took out high debt to income mortgages in the 2020 / 2021 period.

The murmurs in the office are colleagues with 1-4 rentals surprised by, or stresing out, about their tax bill.

Are they not stressing out about mortgage payment increases?

For highly leveraged property investors, the cashflow impact of mortgage payment increases (due to rising mortgage interest rates) is far higher than the increase in tax payments due to phasing out of interest deductibility.

Perhaps it is the unexpected tax bill, the sticker shock of the tax bill and the unplanned cashflow associated with it?

Boomer and Speculator paper become vapor...equity that is.

The stand off continues, and the ticket clippers, agents and brokers etc, are all calling ever louder boo hoo's. Every interest rate rise, and inflation labour rise pressures land downwards. Ticket clippers go and look up the bubble curve. The sooner you transition sellers from the delusional phase to the capitulation phase the sooner you can clip and pay for some advo on toast.

Popcorn and butter, melting.

The stand off continues, and the ticket clippers, agents and brokers etc, are all calling ever louder boo hoo's.

IMO, it's a good time to be an agent even if you don't rely on the job as a meal ticket - for ex, you need to sell one property per week to put food on the table. I think it's a good time because there's less competition in the market and it's possible to position yourself as an agent with a different disposition to the rest. Most seem still trapped in the 'ascending bubble' hype. It's a little different now and you need to be more sensitive to loss aversion on the seller side.

Like your positive attitude. It's definitely tougher vs the last couple of years. Agents would post a listing and the phone would run red hot with people throwing money like crazy people. All you had to do was run a Dutch auction and bang...sold in days.

That was not selling, it was order taking. Agents picking the winner if they wanted, as always a que of loosing bidders.

The young REA's who jumped onboard 2019-2021 to ride the wave are lazy as hell and will be leaving the market in droves soon if they don't learn to put in the work. The veterans know that in tough times they have to put in the time, the calls, the tailored service in order to attract and retain clients - with word of mouth being key for further referrals.

HPI data trumps all. Until that stops falling I'll just believe the numbers.

House prices are recovering in Toronto, Montreal, Vancouver and Sydney. The bottom has likely been reached in the lower tier global cities too. Auckland will follow this trend.

The schadenfreuders will need to wait a little longer before they see the much anticipated return to dystopian medievalism.

House prices are recovering in Toronto, Montreal, Vancouver and Sydney. The bottom has likely been reached in the lower tier global cities too. Auckland will follow this trend.

That's the spirit ZS. Remember, we're part of the Anglosphere and we are special. We refuse to be spooked by credit-driven everything bubbles.

Well, duh.

LOL! The vested will always have others believe we follow major cities on the way up but never so on the way down. Such shallow assumptions are pure entertainment.

Ireland didn’t follow other major cities when they had their crash, who’s to say we won’t be the same!

I still see it being pretty flat here in NZ until post election. The election timing is nice, just before summer so I expect to see a bounce off the bottom, especially if the OCR is still set in stone. Recovery will take a while, maybe 1% house price increases next year.

Yes, recovery will take a while. With the expected introduction of DTI, it will be many years before we once again witness a time where house price increases exceed the prevailing rate of inflation. I know the vested are turning blue waiting for this benchmark of portfolio performance to justify all the interest they're having to cough up 🥶

Regarding dti: next year the rbnz will have the power to introduce these. However I’m not sure they will until they see signs of a recovery.

There's been nothing stopping them putting in a reducing DTI except for one thing - their currently proposed implementation of it is a joke.

It's too hard to simply give a ratio, they have to carve out exceptions for certain market actors.

I've only been half joking when I suggest to people that this RBNZ will relax the DTI rules for Maori borrowers...

Maori bank with special interest rates, an RBNZ "Tane Mahuta for Lending" programme?

They could make it simple: all borrowing must be stress tested at a minimum of 10%, or 5% above the interest rate of the loan they are applying for (whichever is higher). No need for a DTI, as the stress test would effectively restrict the amount everyone can borrow.

Next we could ban "investors" from buying existing housing stock (except in special zones and only if they are demolishing and building high density). New property Investors should be given the tax perks back, but they will only be able to buy land and build or buy new off the plan from builders.

I can't believe that the political parties are not running on a slogan like "Housing is for people, not investment returns"

"Next we could ban "investors" from buying existing housing stock (except in special zones and only if they are demolishing and building high density)."

FYI, how Singapore government housing policies work:

https://twitter.com/GRomePow/status/1643083095376285698?s=20

Only if national win. In fact if it looks like they will win I might buy an investment property pre election, may as well get on the gravy train if that’s what the democracy have decided upon.

OCR is never set in stone. Even if OCR doesn't go higher (which I doubt will happen) prices will fall further. There is denial, delay and lagg to account for

The election timing is nice, just before summer so I expect to see a bounce off the bottom, especially if the OCR is still set in stone.

I'm more expecting a flood of properties to come on the market in spring for those who want to move location, sell a rental from mortgage stress, divorce sales, O/O simply wanting to move location. Plenty of pent up sales waiting through the winter to list, we'll see what happens.

You are comparing lemons to squash. The Canadian govt allowed the bankers to extend mortgage terms, from the previous limit of 30 years, as far as they wanted. The longest term I'm aware of is 95 years. This, combined with the lowest inventory in 26 years and 1 million new immigrants in 2022, is why the Canadian housing market has not continued its death spiral. Canadian housing still dropped between 25% and 30% to this point.

Add to this inflation ticking up again and Canada is bracing for further OCR increases. This may be a short lived deadcat bounce for the Canada market. It all hinges on the Govt response, as they have taken over command of the housing market and will likely continue to tinker, with the intent of preserving all the boomers wealth (as Baby Boomers make up the deciding cohort of voters).

Listed down. Sold down. Seems like the trailer of things to come this winter.

And agents with foreign origins and offshore links still selling property at ever higher prices that do not make financial sense. Is there some investigation needed? Or no one cares since money is coming in but but but What about long term consequences???

If this does turn out to be one of the biggest financial bubbles in history (thinking shares and property and globally- not just NZ) then we’re a showing all of the signs of the ‘return to normal’ phase.

‘Everyone should but now as prices are going back up again’

It’s a dangerous time - can also be known as the suckers rally.

On the bubble diagram there is always a "bull trap" before the return to mean. See what happens.

It feels like a complete reversal doesn’t it! We were pumping up assets and deflating consumer prices, now it’s the opposite. But now all of a sudden increasing prices are considered a problem not a positive, think of the poor, etc.

If this does turn out to be one of the biggest financial bubbles in history (thinking shares and property and globally- not just NZ) then we’re a showing all of the signs of the ‘return to normal’ phase.

‘Everyone should but now as prices are going back up again’

It’s a dangerous time - can also be known as the suckers rally.

120%.

Here's a bit of fun for you. I need to buy an apartment to work out of in the medical mile Auckland. It's complex but I have waited as long as I can and now need to buy. I zeroed in on a short list. After inspections etc I have floated an offer based on peak price adjusted down 22.9% as per HPI. CV June 2021 1.65m, I offered 1.34 based on best data. REA reported back they want offers over 1.6m. I have asked them to address the data rather than reply with a number they would like - plan to walk unless reason prevails of course. I'll report back....

The price is the price no point throwing data at it. The seller will become more realistic only based on time listed or urgency in the sale, many places simply get withdrawn as vendors wait for the market to improve. Best to have a few different options on the go, sooner or later you will get lucky in the current market. The REA pretty much never tell the truth as to the genuine reason it is for sale, so you just need to find the one that really really wants to sell.

Sounds like a reasonable offer and a classic case of vendors dreaming that it's still 2021.

There's a lot of nice apartments coming on stream around there in the next few years, you should be able to wait and pounce on a good bargain.

Gets to the point you cannot wait any longer. There are people on here still waiting for the property bus to arrive, its decades overdue.

Is that 22.9% as per HPI in the medical mile of apartments that were valued at 1.65m in June? I.e. fall of that much, in that area and price range is more than I'd expect at first glance. I'm guessing 3 bed between 95 and 135sqm? If so, that's more akin to a house in the area. In any event, stick to your guns and keep looking around - things are popping up all the time as mortgages role over.

The existing landlords should all sell up and crash the house market as per the DGM world view.

Where might existing tenants stay after that, they will end up in cars.

Good plan

Once a rented house is sold does it disappear altogether? So, hypothetically speaking, are you saying that a tenant can never own a home even after all the exiting Landlords have crashed the market?

You certainly think like a Landlord......

A fair chunk of tenants don't aspire to (or have the means to) be homeowners.

Agreed. However, for the large chunk of tenants that do, HW2 would have them believe exiting Landlords would render them homeless too. Its unduly precious. Besides, even if the market crashed outright, many investors would remain reluctant Landlords as they couldn't exit. There will always be Landlords. A higher home ownership rate (something we should all be proud of) would be the result of such a deep reset.

If it crashes more people will be able to buy including first home buyers, people who have separated and lost equity and landlords wanting to increase the size of their portfolios.

Nope, the existing tenant can just sign up with new landlord - who no doubt will be better capitalised - having bought recently from one of the many emotionally distressed landlords threatening to throw their house out of the cot.

.

Note the tenants won't be homeless until the house actually sells - and who's to say the new owner isn't a landlord wannabe?

If everyone sells, and no one is buying, tenants can just sit pretty. Maybe they can even wait till it hits mortgagee sale, and take if off their poor struggling landlords hands?

Yep the Juxtaposition of that, would have the country in a much happy place indeed!

A deeply indebted, highly leveraged and poorly struggling landlord "saved by their tenant"......who buys the house at a much reduced 2012 price level, yet saves the LL the 20k RE Agent fees. Both winning!:)

Meanwhile the Landlord will still have leveraged (property never goes down reminder) bank debts to pay off. Kind of Funny.

by HW2 | 27th May 23, 1:17pm 1685150258

The existing landlords should all sell up and crash the house market as per the DGM world view.

Where might existing tenants stay after that, they will end up in cars.

Good plan

I find it funny because you say 'good plan' sarcastically and yet it actually is a good plan.

If all the landlords try to sell at once, supply of houses for sale would go to the moon, and the supply demand balance would favour buyers dramatically and the prices paid would be dramatically lower than where they are now - meaning FHB's would need to take on far less debt, mortgage stress would be much lower, and it would bring about financial and social stability for our society. Houses would sell because they would be at a price point that FHB could afford at current interest rate levels. They would be on the ladder as opposed to renting. Heck more young people might get married and have children and be less depressed and anxious.

It is a great idea HW2 - genius really. Are you going to get the ball rolling and sell up your portfolio or is your personal net worth more important than the well-being of society as a whole?

The scrolls have some wisdom on this topic:

https://th.bing.com/th/id/OIP.12tkB-6Nk-fwPbrvws14YgHaFj?pid=ImgDet&rs=1

IO, you've become the new prophet with this scroll stuff.

I don't think we ever got to see the Third Scroll - would have liked to have seen that, before The End.

How many tenants do you know, that have significant savings.

Very few other than those who are aspiring future homeowners?

Most know that if they have dollars in de bank they can't claim some benefits. Its better spending everything, like buying a flash car on HP and living like kings. The smart people do the opposite and live like paupers

If Auckland homes fell to 500k buyers still need 20 percent deposit or $100,000 so low low house prices aren't going to help much.

And remember LL are despised ridiculed and have been run out of town under the DGM world view. There won't be cheap rent, just hundreds of thousands of homes sitting empty and waiting for a buyer

HW2, straight from the carton or "sunny side up" ?

I hope your day is well but comments like this is why I give you a wide berth R-P

Actually that's a great plan.

A few people here need to cut out the noise and stay topic focused

Sean Foo made an interesting point a day or two ago. Because of the protracted US debt ceiling standoff, the US Treasury has chewed through their reserves. Assuming a deal comes through, they will need to go to market and borrow up a storm.

I don't like the sound of that - if rates keep going up we'll never get to that hilarious $2m mark for an AKL shit box. What am I going to do with all this popcorn then?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.