There were slightly fewer properties offered at the latest auctions monitored by interest.co.nz, but slightly more sold under the hammer.

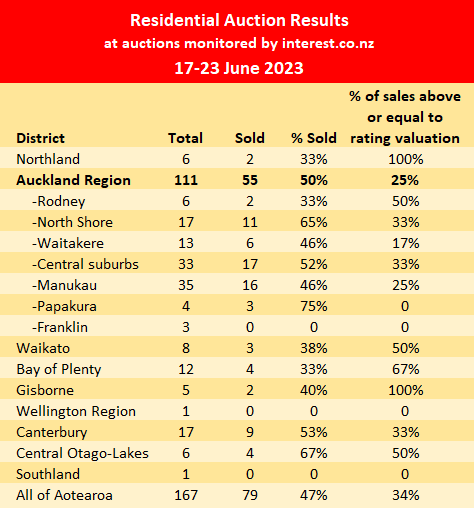

Interest.co.nz monitored 167 residential property auctions around the country during the week of 17-23 June, down from 177 the previous week.

At the latest auctions 79 properties were sold under the hammer, giving an overall sales rate of 47%,. That compares to 76 sales and a 43% sales rate the previous week.

Prices remained generally soft, with just over a third (34%) of the properties that sold at the latest auctions fetching prices above or equal to their rating valuations, although that was up from 26% the previous week.

Generally the market is subdued and appears to be bouncing along the bottom over the winter months.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices and rating valuations of those that sold, are available on our Residential Auction Results page.

The comment stream in this article is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

130 Comments

There are some screwball numbers in that list

How do you get 2/3rds (67pct) of 4 in BOP and half (50%) of 3 in waikato

You are reading the wrong column.

I think he’s right. If only 4 sold, then it’s mathematically impossible for 67% of them to have sold for above RV. It’s either 0, 25, 50, 75 or 100%.

Unless more sold after the hammer and are counted in the 4th column, but not shown in the 2nd. But then that would be a strange way of showing the data.

Dang, I think you might be right

Incredible (= Not credible) data

🤣

This sometimes happens when we are unable to match a sold property with its rating valuation. There can be several reasons for this but the most common is that the address used for the auction doesn't match the address on the rating valuation. This usually only produces a noticeable impact when the number of properties in the calculation is very small.

Hi Greg can you also explain the criteria for selecting auctions that you monitor.

There is currently approx 1400 properties across the country that are listed for upcoming auction, according to my search. So I guess would that be more than the 167-ish auctioned per week.

A few weeks back there was a comment that Northland had a handful of auctions over the week, with some selling. Compared to the single northland property in the article which did not sell.

The column on the right is interesting its the percentage SOLD at or above the RV so for say BOP, 2 out of every 3 sold is still above the latest RV, so much for the "Crash"

Yes but 8 out of 12 failed to sell so the true percentage is 2/12 put up for auction.

Irrelevant, it applies to houses that SELL, not some stat you decide to make up.

Care to provide your expert analysis on the big markets like Auckland, Wellington and Christchurch?

When were RVs set in BOP?

July 2021 for Tauranga

A better measure would be how much below peak Homes estimate.

Market is waiting for the election now.

For the overleveraged and negative geared, hoping that National will come to the rescue is easier than waiting for interest rates to halve.

National is not withdrawing the ring fencing changes meaning no income tax rinsing are they...?

My understanding is they are.

They can wait all they like. But 10% Interest Rates This Year Guaranteed, will extinguish any hopeium pipes smouldering in those mug mouths out there.

A vote for National is still a vote for Labour. Two wings to the same bird.

Blue is the new Red, netflix series.

Forget about promised tax advantages again. The banks will laugh at how you can service 10%.

Nope, not 10% this year, or next year, house prices bottoming this year, good time to buy when there's very little competition...

If that's so, I think we know what happens the very next day after the votes are counted. The Kakhovka Dam would be a good analogy.

I think it would be into the new year before vendors become realistic. Have to wonder what’s happening in the background though, there must be some banks pressuring some owners.

The banks will want to restructure the debt terms before forcing sales.

There was a comment by someone active in the commercial real estate area. Seems that there is some extend and pretend going on in that area.

Have read some anecdotal stories of banks assisting retail borrowers in their hardship department - such as interest only terms for a period of time, term out the mortgages.

Those borrowers who took out high levels of debt in 2020 - 2021 are likely to have a higher probability of default.

A growing number are getting behind through such reasons as job loss, sickness, exploding overheads or all of the above. If the equity has evaporated so has the options of loan restructure.

Option - Sell.

All 5 of these townhouses have been fully completed and for sale since November last year. And yet not a single Townhouse sold yet. The one under contract as the advert says has fallen through, a long time ago, strange how that has not been amended .

The other 5 still to be completed in September this year are also for sale now, but NO bites yet.

The company tells me it's OK because the Property Market will be firing again in December.

Sometimes it's just easier to Smile !

https://www.trademe.co.nz/a/property/residential/sale/hawkes-bay/napier…

"A bank is a place where they lend you an umbrella in fair weather and ask for it back when it begins to rain" ~ Robert Frost

And raining it is Reverend Poppy. In Australia for their Landlords.

"Up to HALF of the states Landlords are considering selling up their Investment Properties ! "

In NZ its probably more than half

They know when there backs are against it. The reverend should announce Last Rites

🤣🤣🤣🤣

As many people said last year, smart ones sold in 2020 or 2021 at the very latest. Pity Printer8 didn’t advise his sons to do that. Or did he? He commented May 2022 that two of his sons held investment properties. Last week he said his family members sold out in 2020/2021. He’s either lying or going senile. Ironic when in the same thread he had a go at someone for dishonesty.

Sorry for having a dig, but you open yourself to that when you have unfair digs at others.

😂#Hypocrite

The smart ones also sold out in 1929.... those who didn't, thought it would be a passing phase. How could everything turn to crap after such a wonderful 1920s decade?

Blue skies smiling at me, nothing but blue skies do I see.

Gee HouseMouse pretty desperate stuff to twist things. Clearly I really cut you up - and not unexpected from someone who blatantly lies stating I said properties were going to increase by 15 to 20% in 2022. :)

On this, I am happy to be accountable.

Clearly you do not understand what my comment the other day about "getting out of property investment" means. Being active in property investment means seeking out potential properties, upgrading and/or developing them, in some instances subdividing, and then either renting them out or selling for capital gains (subject more recently to the bright-line test).

I got out in 2016/7 when I did sell the last of my rentals and in 2020/21 my two sons who had been active as I stated "got out" - that is not being active in seeking properties including one selling four properties 2020/21 (and another in 2022). Subsequent to that they each did hold a rental property as a passive investment as they have very positive yields .

So yes my comment the other day as I said about "getting out" of property investment is consistent with my comment of May 22 and earlier:

As to their homes (and two with a rental each) their mortgages are 2.99% until 2026, and yes, one millennial sold four rentals late 2020 and is now mortgage free in a very nice home. All done on their own resources without financial support from me.

Now, you be accountable for your blatant lie when you stated I said properties were going to increase by 15 to 20% when in 2021 and 2022 I said that I thought then prices were unsustainable . . and I'm happy again to show your blatant lie.

Cheers :)

Financially stretched authorities in search of a cash cow are more likely to turn their attention to owners of multiple properties as a revenue source. One would be of foolish mindset to think it will never happen here. Would it be less likely to cause rioting than the cutting of welfare benefits?

ah yes 7 news the epitome of good journalism, second only to nz herald

"Thu, 6 Oct

Ahuriri Townhouses

21 Battery Road, Ahuriri, Napier, Hawke's Bay

Enquiries over $1,450,000

2 bedrooms"

Remove the "1" then you'll have buyers

Oh but they have assured me that $1,450,000 price tag was from a reputable Registered Valuation company. Done recently.

Just don't compare it to the Homes.co.nz estimate provided in the same advert. Because Homes.co.nz is very accurate, lol.

If you buy now it will be worth way more by December.

How would you like to pay ?

I wonder how much it would cost to build those houses?

2 bedroom terrace in Napier should be way south of $1m.

If they cannot build for that on relatively cheap land we have gone massively wrong

How many distinctive architectural features would you like?

Dunno, how many should there be

Agree here!

Should read inquiry range 350 to 450k......

WILL NOT SELL anywhere near 1 mill, with 7 to 10% mortgage rates in the Napier hicktown.

What are these developers smoking?? One things for sure, they will be downgrading to rollyourowns .....when this crashing market dust settles, by 2027.

One Woof this avo Gecko. They should rename it Saturday Spin Show

Absolutely ridiculous !!! ......meanwhile for the same price in NZD (USD $891,000) you can purchase this fine property ......

https://www.zillow.com/homedetails/9533-Loma-Vista-Dr-Dallas-TX-75243/2…

Yee haa says the "Crazy Horse" !!

These townhouses are *really* pricey for Napier. You can get a beautiful, new-build, good spec 220+ sqm house on 600+ sqm just 5 minutes drive away in Parklands for 1.2 M (which is already over-priced, but that's another story) so why would you choose a smaller townhouse with little land? Makes little sense to me. These townhouses strike me as very seriously over-priced!

"All 5 of these townhouses have been fully completed and for sale since November last year. And yet not a single Townhouse sold yet. The one under contract as the advert says has fallen through, a long time ago, strange how that has not been amended .

The other 5 still to be completed in September this year are also for sale now, but NO bites yet."

Where is the housing shortage that economists are talking about?

These 10 newbuilds are listed for sale (5 listed for sale for 7 months now) but where are the buyers?

Where are those immigrant buyers the property promoters keep talking about?

"Have read some anecdotal stories of banks assisting retail borrowers in their hardship department - such as interest only terms for a period of time, term out the mortgages."

They aren't helping the borrowers, they know that they are going to default, they are protecting themselves by trying to stagger the defaults. Banks do not want a surge of defaults it hurts their book valuation.

"They aren't helping the borrowers, they know that they are going to default, they are protecting themselves by trying to stagger the defaults. Banks do not want a surge of defaults it hurts their book valuation. "

It would be very interesting to know how much forebearance the banks in NZ are willing to give.

In the UK, the UK government had a meeting with the CEO's of the large lenders to discuss some type of temporary forebearance for those house owners under cashflow stress due to rising mortgage interest rates.

Here are some of the measures:

https://youtu.be/8ZKJA9fnnjY?t=65

Again, that discussion the UK government is having with banks isn't about helping house owners, it's about minimizing criticism of the Tory Government.

If similar is happening here (and why wouldn't it be?) then we might see an increasing number of AirBnB type places hit the market. If there's no income, it makes it hard to service the mortgage as % rate continue rising ever upwards.

"Like somebody turned the tap off". Demand for holiday rentals slumps. Demand for holiday rental homes in some of the most popular regions has dried up in the past three months as households slash their discretionary spending to cope with the pressure of rising interest rates and cost of living, owners say. (AFR)

I mean, it's winter, and spending on travel is up in general, and banks don't lend for Airbnb's usually, but ok.

Could be. But in the grand scheme of a fish rotting from the head, today we get:

Three years ago businessman John Changjin Li seemed to have it all: a happy marriage...and enough money to buy a new trophy home on the Point Piper waterfront for $95 million...Li went on a buying spree, adding a waterfront estate in Lake Macquarie, an investment house in Vaucluse and a Bayview mansion to his already well-endowed property portfolio. But things seem to have gone awry since 2020.....Three years later, and after tens of millions of dollars have been paid toward the cost of the house, it remains unknown if the company will settle on it..... companies were placed into administration last year with debts itemised on the companies’ own corporate filings that included a tax debt totalling $7.5 million, $16,000 in council rates and charges, $800,000 in outstanding land tax, almost $1 million owed to construction company Forbair and $100 million in outstanding loans.

As with all failures, the damage spreads out, and out, and out...

Brown shoots aplenty!

Can someone provide how many properties have been withdrawn in the last 6 months?

And may be drill down to a bit more to look at unrealistic expectations of vendors as the asking price.

The market is totally broken. These days even a million is a lot of money if you got to borrow it. But if you have cash, then you are king but only if not tempted to buy tulip mania and invest in something stupid.

I agree the market is broken. Just chatting to my husband about properties we know here. Good quality homes $1.5 million to $2.5 million with large section/ lifestyle. We think there are equal numbers of properties pulled and properties languishing (6-8 months) on listings, about ten properties in each group. Bar one these properties have all been priced at 2021 levels. We think an additional 4 have sold in the last 6 months.

I agree one million dollars is a lot of money, some people ( and agents) don’t haven’t yet adjusted to this.

The average NZ household can borrow just under 500k now and this (+ the 100k deposit) is where a lot of "average properties" must fall to, its slow motion crash, as happens in every multiyear, property crash, such as we are now and just 1/3 into it.

Sure the special featured lifestyler types will go for more, but they are on the edge of a mighty cliff, they are indeed poised to fall off - and its a shear face with unforgiving rocks beneath!

I'm not sure why people keep guessing what house prices should be based on what the average can afford. That's not what's been determining the market for quite some time.

Ok then. What can the average afford at 8%??

Sorry- same result. A massive price reset - as we are all WITNESSING NOW.

I don't think the average has been able to afford much at all for a good decade or more.

The market is just a lot more diverse than thinking about what the average can and can't afford.

The point is that the OCR dropping to nearly zero % enabled a whole lot of people - ‘the average’ - the potential to buy when it would not have existed in ‘normal’ times. It was a fake opportunity.

Now that normality has resumed, we will pay the piper.

Prices are still at least 5-7% too high for ‘well above average’ people to buy. Drop another 5-7%, and interest rates start their drop, and we may have hit the bottom. This time next year?

The point is that the OCR dropping to nearly zero % enabled a whole lot of people - ‘the average’ - the potential to buy when it would not have existed in ‘normal’ times. It was a fake opportunity.

It didn't though really. Lending terms in the last decade have gotten a lot more stringent than in years gone by. It's allowed for servicing of larger volumes of debt for those eligible, but the 'average' buyer has been increasingly marginalised.

House price’s are falling fast the people who purchased last week will see property purchased worth 20% less this time next year, the same as people who purchased this time last year are now down 20%. It’s a bit silly to buy in a falling market especially when bottom is no where to be seen.

Your onto it- market confidence of a bottom is nowhere in sight- I have warned all potential FHBs that I know, to only offer around 2014 valuation prices or prepare for big losses in 2024-2027.

Ive looked in deeper and dropped a big rock this time..... still no sound.

- The bottom is very deep. Not even a hemorrhoid bump to be seen, by telescope!

Sales rate picking up in Auckland, there's definitely more interest in the auction rooms... clearly some must think we're at 'the bottom'.

Or perhaps near the bottom and worth a bid.

Or, the Vendors realise The Bottom is still quite a way below today's prices and have decided to try to sell-up whilst they can (they are right)

those (that benfited) the most have the most to lose should the facade crumble. Those at the top of the heap are thus fanatically devoted to propping up the illusion of stability and "growth," regardless of the damage being done behind....There is no master-plan in the desperate machinations to keep the facade intact. There is only the day-to-day plugging of holes, that reality is leaking through.

"clearly some must think we're at 'the bottom'."

There seems to be a big co-ordinated push of this narrative by those with vested self serving financial interests in mainstream media to boost confidence in potential buyers?

A relative who wishes to be a first time owner occupier buyer and relatively uninformed about the residential real estate market sent me the recent article from the NZ Herald pushing this narrative.

Also saw a segment on prime time mainstream free to air TV.

All on the basis of sales picking up slightly in May (from rock bottom levels) and a slight increase in median value (but HPI still falling).

Alot of the market is driven by sentiment... people are sheep and follow the herd.

Yep, that's why spruikers are morally corrupt and deserve as much contempt as possible.

Reminder

There will ALWAYS be someone telling people that now is the best time to buy.

Why?

Because these people need to earn income to put food on the table to feed their families, pay for the roof over their heads (either rent or mortgage). More property transaction volume and transaction values financially benefit the following groups of people:

1) real estate agents

2) mortgage brokers

3) property mentors

4) property developers

There are others.

Positive spin leads to increased confidence to persuade people to buy.

Always remember the vested financial self serving interests involved

Ok then, let's call a spade a spade. I think we should from now on call this whole property spruiker business a Cult. There are the high priests; for instance Tony "Greenshoots" Alexander. Mortgage brokers constitute a lower level priestly caste. Landlords are the next level down in the hierarchy.

I would call this cult "The Spruiker's Cult" or similar.

The victims, of course, are the FHBs who were sucked in by the ingeniously successful concept of FOMO, dream't up by the Cult's propaganda department, One Spoof, which, as I understand, had studied the methods of Goebbels the infamous Nazi propagandist.

These are just a few basics but other commentators could surely elaborate by filling in, or improving upon, the many gaps in my, as yet, inadequate knowledge of this cult.

You see it with clarity SW.

Yes the Onespoof spin doctoring team, have studied the exponents in Propaganda for the masses, of the Germans and Russians for sure!

The prices requested atm are simply: "NOT possible to achieve for most buyers, at interest rates above 4.5%"

- So we have the now long obvious collapse in volume, this can only be solved by buyer capitulation.......or 4.4% mortgages ( 4.4% not happening this side of many years - barring a worse still - economic calamity!)

For the Spruiker cult army, the truest statement that fits this bill is: "When its this bad, They just have to lie"

Media like Granny Herald also need real estate advertising revenue to survive.

While I don’t rate him, at least Liam Dann is usually fairly balanced. Even he has been having a spruik in the past few weeks.

They are getting DESPERATE.

Anti spruikers don't do anyone any favours either... there's been people on here for years preaching that you shouldn't buy/invest - safer to hold your money in a savings account or TD. I would imagine there's a been few that have missed out on prime opportunities given the scare mongering...

Nifty - don't you think it's always about individual circumstances and the dynamics of timing and their level of debt? - I think you simply shouldn't buy unless you can afford to payback debt fast - not leverage yourself into 30 years of debt servicing paying twice as much as you would to rent.

Sadly most people are making massive life decisions without any experience or proper guidance - so they look to media and the opinion of property experts - who always tell them "now is the time to buy"

Some have held onto huge levels of debt priced at under 3% as they were told by these ‘experts’ with vested interests on national telly etc to not panic when rates got above 5% as inflation was transitory and rates would be coming down at the end of 2022 or start of 2023

https://twitter.com/TheProject_NZ/status/1526825567663935489

Interviewer: "What are the chances you’re wrong?”

Bernard Hickey: “I’ve actually been right for the last 10 years”

Looks like the facts have changed for ol’ Bernie

All I can add is the people in their late 50s and 60s I know who didn't want to burden themselves with decades of debt securing a home are facing pretty sad futures.

So maybe if someone was one of a very small minority of people who don't buy a property and are diligent lifelong investors/savers, they'll probably do ok. Most people seem to be more hand to mouth.

Buying a house is a form of compulsory savings so you do not get a chance to "Blow" all your money. You would have to be an extremely controlled individual to put that money elsewhere and come out in the end at 65 with say $2 million. Pretty much that never happens in the real world so most of the people that never bought a house are screwed.

Yip, also it generally forces you into a longer-term investment thinking, which also helps.

People who haven’t owned property often miss these very important points.

You're beholden to something for life regardless of whether you think you can opt in or out.

So it's smarter to consider that than how unfair the system is.

Painter - yep, it's always about smart choices in life, and working hard to save along the journey.

I know people in their 60s now facing bankruptcy or a very significant loss (unless rates go back below 4% in the next 12 months) because they bought the wrong investment properties in their 50s for 'retirement' income.

Ok but if we averaged it out, people with one or more properties at 65 will have a better quality of life than someone with no properties at 65.

If they're bankrupt having to sell an additional property they've held for 10 years they likely are bad with money period.

I agree Painter as an average thanks to 40 years of falling interest rates and rising property values - but still only if you understand what you are doing which is hard when you start out at any age with no experience and are taking guidance from the wrong people/media/spruikers/.

These guys were relatively affluent and successful career wise, just all the classic property investment mistakes - mainly negatively exposed to higher rates and no liquidity because never understood or run the numbers properly - holding costs etc

“it’s all about leverage and capital gain, prices only ever go one way"

“portfolio is interest only mortgages because a mate who’s done well in property said that is the best thing to do”

"Tony Alexander said values wouldn’t fall more than 10% as that’s what happened in the GFC and this won’t be as bad”

“Rates won’t go above 5-6%”

Lots of delayed maintenance, now trying to do repairs themselves as can’t afford tradesman etc

Basic plan was to sell all one day when they retired and bank the capital gain

Rolling off sub 4% rates next year

Now realise they need to sell now but multiple agents have told them to sell in this market they need to be empty and staged… but can’t afford to list without tenants paying their holding costs - and can't re-let without bringing up to healthy home standard if they don't sell.

"just all the classic property investment mistakes - mainly negatively exposed to higher rates and no liquidity because never understood or run the numbers properly - holding costs etc"

Key question is: How many residential property owners will be unable to hold on?

multiple agents have told them to sell in this market they need to be empty and staged

Or they could list with the tenants for a sensible price and let the purchaser decide if vacant possession or not.

Reality is, properties probably not gonna sell without a fire sale. If they're over-leveraged, they're cooked.

Listed as ‘Renovators dream’…

"empty and staged… but can’t afford to list without tenants paying their holding costs - and can't re-let without bringing up to healthy home standard if they don't sell."

Catch 2022 🥺

Not to mention staging costs THOUSANDS for only a few SHORT weeks.

“Sadly most people are making massive life decisions without any experience or proper guidance - so they look to the interest.co.nz comment section - who always tell them "never is the time to buy"

Some very dangerous advice given on here. You have to access your own financial position and future and make your own decision. If you can afford to buy a house and make the required lifestyle compromises then its always a good time to buy.

https://www.interest.co.nz/users/zwifter

by Zwifter | 24th Jun 23, 7:17pm

Some very dangerous advice given on here. You have to access your own financial position and future and make your own decision. If you can afford to buy a house and make the required lifestyle compromises then its always a good time to buy.

----------------------------------------------------------------------------

SPRUIKER cultist Snapped in the headlights! Ding!

Very dangerous advice?

A few hundred dollars extra per week (paying $1300 rather than $1000) will halve your mortgage term from 30 to 15 years

And if rates go down in the future, keep paying the same amount and thus be reducing your mortgage even faster.

Run the numbers

https://www.interest.co.nz/calculators/full-function-mortgage-calculator

Saw an interview with a property trader specialising in South Auckland.

It seems that confidence has improved with property traders in the housing market. There are property trading joint ventures that are buying up houses on media reports / high profile market commentators saying that prices have bottomed out, causing some of these property traders to develop a fear of missing out.

These property traders typically only buy older houses in need of some work, not apartments or units, or newer stand alone townhouses.

Note that there are also a few property investment joint ventures that have been buying in the past - combining their borrowing capacity to buy investment properties (and outbidding owner occupier buyers). Don't know if they're active in the current environment.

Depends what they're paying. If it's 50% below peak it means the bottom for everyone else still has a way to fall yet.

Sales picked up slightly, Fantastic.

For the first time that I can remember, there are 40 mortgagee listings on Trademe. After hovering in the range of mid 20's to 30ish, for a month, and up from around a dozen at the beginning of the year.

I'm not seeing any bottom yet.

40 mortgagee sales across the country, wow!

I can see these increasing 10 fold by October as the manic rates / prices of 2021 roll over with their 2 year fixed rates.

I feel for these young families who because of what ever reason jumped into this craziness at its height. Some I know were lied to buy their RE agents and now they are stuck buying at the high.

So how many mortgage sales signal a serious problem in the market ? 100 ? 400? 1000?

It's the rate of change Nifty. Rates are still rising in the Eurozone and USofA. At some point even the true believers will have to realise, that there is no point in any longer keeping a finger in the leaky dyke, as the flood becomes undeniable.

As our good friend DDD would say, it's all about the debt baby.

Article from 2009, to put it into perspective...

Figures released exclusively to the Sunday Star-Times show there were 150 forced sales in January a whopping five-fold increase from January 2007's 28 sales, when the property market was robust and the economy stable.

https://i.stuff.co.nz/the-press/2299788/More-Kiwis-lose-homes-as-recess…

Put what into perspective? You're sounding as desperate as HW2 clutching at cherry picked anecdata

HW = Human Womble

I think nifty is saying we are diffrunt this time

🤣

The simplistic nature of property investment has Nifty1 believing that China, interest rates halving and National will come to the rescue.

Flying high, you are HW2 - LOL!

Says retired "poppycock". What other innuendo do you have in the arsenal

Why the charade HW2?

The rate of change that your link implies just reinforces my point of view NIfty. But thanks, good link.

Should I post a link for you with the change in the debt between then and now? Love your work.

Looked alot worse in 2009. We're looking pretty good so far after a pandemic, a recession and what some would describe here a housing market crash...

Something to watch but it's good to look back at history for some context.

I’m not sure it was a lot worse in 2009. My husband was a senior manager in a large Aust/NZ company. He spent the majority of his time in Aust making redundancies, we were not effected the same with job losses here - in fact I didn’t know one person in NZ who lost their job back then. Likewise with property - the falls weren’t on the scales we have now….. it all just seemed to happen faster then.

Now think about the size of mortgages. We had a $400,000 mortgage back then that was considered big, that’s a small mortgage today. Interest rates were adjusted down to protect borrowers and the economy. So I think overall it’s much worse now, just slower….. perhaps because the banks are slower to react to stressed borrowers.

Likewise I worked for a multi-national corporate. Plenty of redundancies in Australia, including closing down factories and offshoring production. Meanwhile NZ, being the pimple on the asshole of a blowfly, we were unscathed. The scale of NZ operations in comparison to globally, unless it's an exercise in cashflow survival rather than maintaining a desired cashflow, really would have made bugger all difference to let what? A couple of people go?

The economy was starting to do ‘slightly’ better in 2009. All that that quote shows is that it takes time for the damage to really show in terms of mortgagee sales.

If 2023 is 2008, then 2024 is 2009.

Nifty Grifty Grifter......

How about your current crop of poor sop, property bag holders, numbering now what would be in excess of TWENTY THOUSAND PLUS!!! That is 20,000 mortgage holders who are sadly behind on payments ???

This is the True and Nationally Destructively Dangerous NZ Karkova Dam the spruikers do not have enough fingers to plug.....yet they furiously try with their nefarious vested interest acolyte goons to reanimate.

Vested/Read as........ OWNWOLF, Banker economists, and the one and only "Independent Economic clowns". Yes Listen to ZB today for more Ownwolf drivel and twisting the crash narrative.....to "green shoots"

Its near financial criminality sucking in the newby FHBs to the ponzi-like wealth destruction of buying property, at todays ludicrous prices.

They believed your spriuker stories of: Buy Now, Buy Today, You just cannot lose on Propeeerrteee!

- You fed them into the Bankers shredding blades like cannon fodder.

Yet you shamelessly still encourage and seek to encourage and feed in new FHB meat??? Shameless on roids!

They believed your spriuker stories of: Buy Now, Buy Today, You just cannot lose on Propeeerrteee!

- You fed them into the Bankers shredding blades like cannon fodder.

Yet you shamelessly still encourage and seek to encourage and feed in new FHB meat??? Shameless on roids!

Lol wtf, you've lost the plot mate...

Ok so I have lumped you in with the worst of the worst from Onewolf and their Constant leading on of the buying crowd. They fed the mania of the mindless buying masses for years. Were you party to this?

Soz if it was too rough an assessment.

The spruiker cheered on house price boom, will lead to thousands of extremely stressed households, many, many will lose it all. So very dangerous for our country.

I believe anyone can truly be redeemed, So you now disown the Onewolf fellow travelers TA, AC, BH and the rest of the coven?

Get a grip mate. For the vast majority of Kiwi's life goes on as normal.

So you are saying? Who gives two fxxxs for the 21,000+ homeowners, who are facing financially existential crisis?

Most are just fine??? WTF! Are you living in the subantarctic islands??

These buyers from the last 5 years, have been used as cannon fodder to prop up the NZ housing ponzi, now it is all splitting apart, on a scale we have never seen in NZ.

These poor new homeowners are the spruikers usefull idiots. They should take a class action on the Media aligned spruikers Cult. Perhaps it will come when the pain gets real media attention.

It's like you've never been through an economic downturn.

Many will be economically stressed

Some will lose their shirts

Most will be fine

I bought a house within the last 5 years, I'm hardly shitting my pants. I suggest you put on a clean pair of panties and get on with it. Some people will always make bad decisions in life. five jumped into a sub the other day that clearly had not been getting the required maintenance or inspection.

"I bought a house within the last 5 years"

Your spruiking makes more sense now, thanks for giving context.

Zwifter, much like TTP and others your efforts of trying to talk up another "one hit wonder" is very telling.

edit

The problem is on this site you can get labelled a spruiker if you've seen a house in the last 5 years, let alone bought one.

'hey, this guy's not blindly joining our club. It's a spruiker everyone, burn him before he mutates into his true form!'

Yes, depending on where we are in the economic cycle, we all seem to get labelled something here once and a while - LOL!

Many people are confusing 'how you'd like things to be' with 'what will probably be'.

Commercially it's more beneficial to deal with the latter, no matter how grim.

I presume you’re meaning:

'how you'd like things to be' - rates below 4%

‘what will probably be’ - rates above 8%

Listed 1 year fixed rates today

Kiwi 7.89

ASB 7.05

ANZ 7.59

BNZ 6.99

Westpac 7.59

https://www.interest.co.nz/borrowing

A 5 year fix at around 5% last year would have been a good trade

No, not at all.

I'm talking about the reckoning that the house market is going to correct and all of a sudden make home ownership more affordable. I think home ownership rates will further decline without some sort of massive external intervention.

Mortgagee listings have now doubled from a few months ago. Wow.

How long until they double again? Wow!

and again Wow!

and again - OUCH!

Interesting times for sure. I look at the interest.co weekly auction results overall & don't get too deep into the region by region stuff. It's weekly, it's the trend I'm looking for. Sales have stabilised somewhat, which in peak winter is no bad thing. The NZ market is down between 15-25% depending on where you are. That's a good correction & we needed it. The plus 40% covid stupidity is finally settling down. It needed to. There are some outlier results but 95% of the market is within thus. This winter was always going to be the crunch period. Winter 23 was in trouble 12 months ago & is so it is proving to be. No surprises here.

Globally things are starting to level out. Inflation will continue to be tough to tame & interest rates will settle in the mid-to-high single digits, so I'm picking this might probably be the new normal. I can live with this & I think we will all just have to get used to it. It is not the end of the world.

There are some real risks on the table with most of them outside our control. I'm talking about a hot war here. This would not be ideal, however, for the most part it has already begun so once again, get used to it. Will we lose? I hope not. We're the goodies remember.

But remember the baddies are not the Chinese people per se, or the Russian people per se. It is their autocratic leaders that are the stirrers, with both leaderships more scarred of their own people rising up against them than they are about us. And if you look really closely you will see that they have troubles at home already & in more places than they would have you believe. That's one of the possible upsides of the Ukraine situation - is that the Russian people see their opportunity for some real freedom & just go for it. Who'd blame them. They've been treated like shit for 100 years & longer. It's a similar tale in China. So far all the descent has been crushed. The police state kicks into gear & wham you're dead or worse, jailed & tortured. But it is leaking out. The wonders of technology. All power to the ordinary people of China & Russia I say.

Coming to a town and city near us all.

Tauranga Commissioners agreed to a median increase (of) 18 per cent for commercial rates, excluding water rates. For residential ratepayers, the median increase, excluding water rates, is 9.4 per cent.

Confusingly, the report also notes "... a median increase to residential rates of 7.2 per cent, including water rates, and 18 per cent for commercial rates, excluding water rates. It’s important to note that these actually lose us ground in terms of our inflation rates running well above that 7 per cent, particularly for infrastructure,” Selwood said. “We can’t afford to keep these rates low” So who knows, except it will be more.

Meanwhile, another abysmal failure of a housing policy from Liebour.

https://www.nzherald.co.nz/business/home-ownership-labour-governments-4…

Wood has gone. Woods should also go. Hopeless and hapless minister.

New Zealand has one of the highest rates of people aged 65-plus still working, at 24%. In the UK it’s 10%, US 19% and Australia 12%.

https://www.stuff.co.nz/national/300912995/when-youre--65-and-still-wor…

Speaks volumes......

Yep to be worse than the US is a particularly poor indictment..!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.