The housing market made a lacklustre start to spring with sales numbers dipping slightly in September.

According to the Real Estate Institute of New Zealand (REINZ), 5439 residential properties were sold throughout Aotearoa in September, down 3.5% compared to August.

Around the country, sales declined between August and September in 10 regions : Auckland -5.2%, Waikato -6.1%, Bay of Plenty -1.8%, Gisborne -11.4%, Hawke's Bay -2.3%, Taranaki -0.7%, Wellington -1.0%, West Coast -25.6%, Canterbury -8.5% and Otago -4.9%.

Four regions went against the trend and posted higher sales in September than they did in August: Northland +19.3%, Manawatu/Whanganui +3.4%, Nelson/Marlborough/Tasman +10.4% and Southland +5.5%.

However September's sales were up 5.1% compared to September last year, although sales in September last year were extremely low.

Apart from September last year, sales in September this year were the lowest they have been for the month since 2011, suggesting the market remains extremely sluggish heading into spring.

Prices increased slightly with the national median price coming in at $785,000 in September, up 2.3% compared to August but down 3.1% compared to September last year.

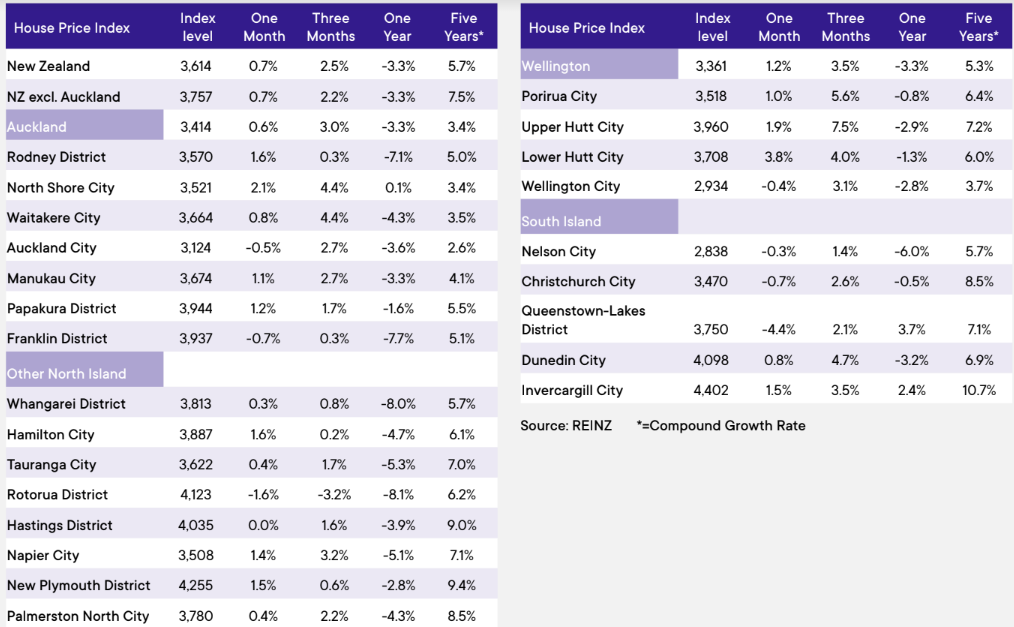

The REINZ House Price Index, which adjusts for differences in the composition of sales each month, was up 0.7% compared to August and down 3.3% compared to September last year (see table below for the full HPI figures).

It is not uncommon for there to be talk of a spring surge or of green shoots appearing in the market at this time of year.

But they also say a picture tells a thousand words.

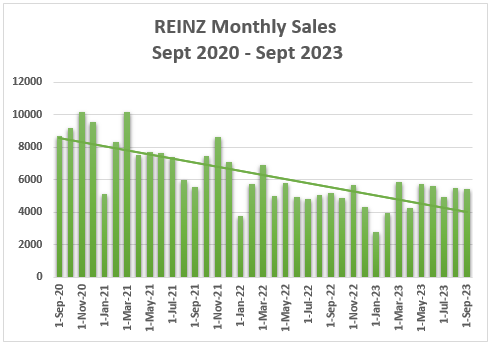

The graph below shows the REINZ's monthly sales figures from September 2020 to September 2023, with a trend line included.

Does this show green shoots, or perhaps a market that's bouncing along the bottom?

We'll let our readers make up their own minds on that one.

The comment stream on this story is now closed.

REINZ House Price Index - September 2023

Volumes sold - REINZ

Select chart tabs

116 Comments

And... let the games begin... lol

Cue multiple comments from DGMs

Cue the pointless comments - as above. They've been biting at the bit.

Let's see what happens late-October - post election.......

TTP

You'll be teleported back to year 2021?

You'll surely be missed....😜

“10% by Christmas” “FHBs are better to wait till the downturn is over” “ long way to go before increases” “50% crash” “dead cat bounce” “higher for longer”

Dreams are free.

You missed out "Suckers Market"

Like I commented below, on an inflation adjusted basis, house prices are indeed still falling.

If you were around in the eighties you will know how times such as these move very much in favour of the saving FHB - (TD's are the tool of choice) Only a fully fledged Spruiker would try and spread a FOMO mentality.

T H E R E I S N O H U R R Y!

I've heard you mention real falls in house prices several times RP, and I am struggling to see the relevance. The real amount of my mortgage DECREASES with inflation. Same as your Term deposit. That is why most mortgaged homeowners only care about changes in house prices in nominal terms - because that's what matters. Inflation is a good thing for leveraged asset owners, even if the interest rates to counter it are not.

That isn't relevant to the deposit, and deposits become cheaper in real terms if the nominal price stays the same in a time of high price/wage inflation.

Alright boomer, don’t get too triggered by my comments.

Grow up.

I actually agree that there is some ridiculously exaggerated commentary on possible downsides to the market. And that’s coming from me, a very bearish commenter.

Black and White and Frank S are still going hard on the exaggerated commentary!

House Mouse, you are sounding very reasonable today. Good on ya!

The 2008 housing market downturn lasted for about 5 years.

Median home price NZ Oct 2007 $422k

Median home price NZ Jan 2013 $430k

This market crash has a few years to go yet. OCR likely to increase before xmas. Higher for longer.

10% this year, guaranteed!

Fantastic long may it continue.

Wait for the big dip to start from Monday with unusable Government.

I am still sticking with my 20% down to go yet.

"Fantastic long may it continue"

What is fantastic and should continue BnW ?

House prices reverting to fair value?

How can house prices "revert to fair value" when they're rising? Did you bother reading the article ?

"Prices increased slightly with the national median price coming in at $785,000 in September, up 2.3%" "The REINZ House Price Index was up 0.7% compared to August"

Trend line of the graph in the article?

I believe that's the sales trend line, not the price trend. That one looks more like a rollercoaster.

Correct, but take the trendline on prices and on sales volumes over the last two years (not the last two months). That, I think, is the point of the article. And of B&W's initial comment.

Antz, the graph is about the number of sales, not the price...

Correct, but take the trendline on prices and on sales volumes over the last two years (not the last two months). That, I think, is the point of the article. And of B&W's initial comment.

I'm pretty sure that's not the point of the article but just your extrapolation of it. The article quite simply means what it says, no more, no less!

And Yvil, your quote is selective quoting par excellence. A classic case of seeing only what you want to see??

The full quote is:

Prices increased slightly with the national median price coming in at $785,000 in September, up 2.3% compared to August but down 3.1% compared to September last year.

The REINZ House Price Index, which adjusts for differences in the composition of sales each month, was up 0.7% compared to August and down 3.3% compared to September last year (see table below for the full HPI figures).

Have highlighted the bits you selectively omitted.

Antz, the REINZ report is a monthly report, so we all know, well most of us do, what has happened the previous 11 months. What's new is what happened in the September month, that's why REINZ call it "REINZ Monthly Property Report - September 2023".

Here is a link if you'd like to read it for yourself: https://www.reinz.co.nz/libraryviewer?ResourceID=612

Think and work it out Yvil.

Why would low sales volumes lead to a price drop? Ask any economics student, when the supply curve moves to the left, prices go up.

Just asked an economics student. He's doing NCEA. He said low sales volumes = lack of demand. Which means prices go down. Down means less. Both in nominal and inflation adjusted terms. That means smaller numbers. Like 1 is less than 6. 6 less than 8. And 8 less than 9.

ok no need to get facetious. Lets keep the conversation robust.

You believe that the drop in quantity sold is because of a drop in demand. I would argue that it is because of a drop in supply (listings). That is the thrust in this article. Our hypothetical economics student knows that when the supply decreases, prices increase. We are beginning to see this in the HPI over the last three months. Albeit it is negligible because demand is elastic in the short term. Ask your NCEA friend what that means ;). Peace.

Facetious? Me? Never. Sarcastic? Me? Yes.

According to the most fervent of property speculators - Spring is the season to be jolly. When unsuspecting property wannabees take heed of 'green shoots' and offer up their hundred year old dilapidated villas slapsticked with a lick of paint and staged with rinky dink furniture from the latest Nood sale. And so supply goes up, as we emerge like property bears from the hibernation of winter - this time funding salmon of a different type - the salmon shaded shirts of slimy RE agents across the country, feverishly tapping up Chat GPT to come up with a new catch line for their latest TradeMe advert.

And yet, even with the spring air in our nostrils, listings (supply) is down around the country.

Vendors waiting on the election to 'save' them so they can rent instead of selling. Just wait until they realise they had their expectations too high and should have sold earlier, that is when we'll see the listings come hard and fast.

supply decreases, prices increase

Only if demand is static/rising.

Agree. And I think it is. High immigration. high mortgage approval rates etc. The drop in quantity sold is because of a drop in listings (supply) rather than demand. I think this is going to continue for the next year or so with housing stock not increasing in line with immigration. Time will tell if I'm right or not. happy to admit if i get my predictions wrong.

Supply has decreased BECAUSE demand has decreased. The majority of home buyers already own a home. When they decide they want a new house they sell the old one. So if they decide they dont want a new house (or rather the bank says no we wont give you a new mortgage) they are then neither a buyer or seller. Unlike most products, the supply of housing is tied to the demand for housing by vitue of the buyer also being a seller in the same market.

Its a drop in listings. A huge number of people are waiting for the election result, that should be pretty obvious. I'm expecting a huge up tick in listings post election regardless of the results as people have waited months. If Labour had won the election there would have been even more listings. DGM's will be jumping with joy thinking its yet another market crash because everyone is trying to sell.

Also many failed listings and the vendors have decided to rent instead off carrying the cost of the mortgage for an empty house trying to sell it.

Chubbs - thank you, makes sense to me (I studied cambridge).

We can also consider the upcoming BVPC (boomer vacuum price crash) - a phenomena where boomers will stop giving handouts to other useless generations (and rightfully so!) - the instant cutting of the embilical cord will crash prices, sending Gen Zers and their rabble back to renting my one of my second homes.

-SMG.

low supply and low sales are not the same thing

Agree. However in this case, the low sales volume (quantity sold) is a direct result from the drop in listings (decrease in supply) - not because of a decrease in demand.

oh really? seems there's been a significant decrease in realizable demand - it's no good saying there are X amount of people who want to buy a house, when interest rates etc. mean only Y amount of people can buy a house.

only demand that can actually pay for the goods matters.

I totally agree that for demand to be real there needs to be willingness AND ability. What I am not seeing is any tangible evidence that demand has decreased. It is listings, or supply, that has visibly decreased since the beginning of the year. Hence my assertion that this is putting upwards pressure on prices. Happy to admit if I get this wrong.

Good points from both of you.

One would think that realisable demand has decreased, due to rising interest rates, but perhaps the high levels of immigration have meant demand is roughly static. Hence, with falling supply, slightly higher prices.

While many of the recent immigrants won’t be able to afford to buy, even if 5-10% of them can then that is enough to have some impact (when the number of immigrants is so high)

Wouldn't a house's median days on market to sell give an indication if the slowdown is supply or demand driven.

A lot of stock came onto the market this week in Wellington - listings on trade me have been hovering around the 1800 mark for the last couple of months - suddenly shot up to 1920 listings on Wed.

I think that is just seasonal noise. Listings always increase in spring. The charts show that listings have been decreasing since the start of this year.

I actually wonder why the number of sales is talked about so much ? Sure, if you're a RE agent, it's most important as fewer sales mean less commission. But for mr & mrs average buyer and seller, it has little relevance. Also there is no clear evidence, that fewer or more sales lead to higher or lower prices.

It may signal to prospective first home buyers currently sitting on the sidelines that the market is quiet and they may have a better chance of securing a home.

What you're talking about is stock levels Dan, but that's not the same as sales volume, I think many people don't understand the difference. Sure more stock for sale = more choice = better chance to get a deal, but that's different from number of sales.

I read something about prices being related to supply and demand.

Of course it does XS, but I was clearly talking about the volume - price relationship. So put your thinking cap on, and write a proper argument which connects supply and demand to low sales and then low prices, and which cannot be turned around. (i.e. low volume could be because of less buyers, but it could also be because of less vendors, or it could be a combination of both).

My thinking is that, in a downtrend, higher volumes lead to lower prices. I would interpret this as vendors not being able to hold on anymorre, which has not happened yet, but it could happen in the future.

Perhaps the relevance of small numbers of sales is that little can be told from them, because such a small sample size can give wrong impressions one way or other.

The number of properties sold in a housing market reflects market activity, supply and demand dynamics, and price trends. A higher number of sales indicates a strong, competitive market with potential price increases. It can also signify consumer confidence. However, it should be analyzed alongside other factors like prices, inventory, and economic conditions for a complete market assessment.

- ChatGPT

I think chat GPT is wrong here. An decrease in quantity sold only means a decrease in price if demand drops (the demand curve moves to the left). In the case of NZ it is a situation where supply is dropping, leading to a decrease in quantity sold and (if demand is inelastic), an INCREASE in price.

If you check the house price index chart vs the volumes sold chart the low sales volumes match up with the low periods of price growth pretty well.

There is a saying in the stock and bond markets "all market crashes are liquidity events". Liquidity is required for an efficient market, because illiquidity creates an inefficient market where price distortions occur. In other words, a market should have a sufficient number of transactions so that all buyers/sellers can easily enter or exit the market without creating a price issue.

Anyone who has had the misfortune of trading on the NZX will understand the problem of illiquidity. Trying to get in or out of a stock on the NZX sets up huge price fluctuations.

Also there is no clear evidence, that fewer or more sales lead to higher or lower prices.

Would it not be reasonable to say that statistically the chances of having prices change [up or down] would be increased by means of volume, in that when one house sells at a higher or lower price than expected, this will influence prices in the same area etc therefore the higher the volume of sales, the more responsive the market in that area.

Like it or not, when adjusted for inflation, house prices are still falling.

Facts mate Facts..it's something people detest..

Let's not forget interest rates starting rising over the last month.. so that will show up in the next couple of months results

Like it or not, when adjusted for inflation, house prices are still falling

So is your term deposit...

I hope you're not telling hard saving FHB's this BS because this might well suggest you don't give a toss about the finances of the next generation of buyers and you're rallying against cash saving. Your mind seems way more pre-occupied about my TD's than it needs to be - it's not healthy. I'm already financially established.

Lets not teach the next generation of buyers to be fools.

Hi RP, not trying to be argumentative or sell a generation up the creek. Wisdom in found in the counsel of many elders so I am offering my advice, as you are.

Depending on an aspiring homebuyer's situation, I would be more circumspect about recommending a term deposit as the way forward. The current rates are about 6.25% at best. Lets say 5% after tax. That is a real loss when adjusted with inflation. Also, they would need to take into account the $40k p.a. they would continue to lose in rent. This opportunity cost is often overlooked in the comment threads.

Owning rental properties is another debate entirely, but owning your own home as opposed to renting seems like a no brainer economically. I shifted from renting to living in my own place this year. In my case, the interest payments are about a 1/4 of what I was paying rent. that is only going to decrease each month as well.

When an aspiring homeowner faces paying a net 8% in interest plus rates, insurance and maintenance costs, the bigger up front chunk of equity the first time buyer can obtain the better off they are.

This current FOMO is a race trumped up by fools with the sole purpose of drawing in more fools to keep a yesteryear dream alive. At the moment, its way cheaper to rent than own. At a net 8% PA, interest, that's a lot more dead money than temporary renting, the bank is your Landlord and you are merely a caretaker of the banks security.

Renting vs Owning - BNZ chief economist estimates the average annual expense associated with buying the median NZ home currently exceeds the cost of renting by just over $38,000 a year"

https://www.interest.co.nz/personal-finance/124362/bnz-chief-economist-…

Even I didn't know it was that much!

For me the sum of interest, rates, insurance, and general household maintenance is significantly less than the $40k in rent I was paying. Even when offsetting the interest i was earning by having my deposit sit in the bank. I am not sure how this BNZ economist came to his 38k figure. But I would encourage a prospective Homebuyer to do their own sums. They might not be the "average buyer" that he is referring to. I certainly don't fit his profile.

If I, as a FTB, were to buy the house I currently rent, I'd be paying 190% (10% dep.) or 170% (20% dep.) of my rent on the mortgage alone, let alone rates, maintenance and insurances on top of that.

[edit: removed snarky comment, i've felt bad about it all day, so my apologies]

Does that include principal repayments? As that is not an expense it should be counted. Even so though, it sounds like your situation is quite different from my own so I will withhold giving specific advice. I had a 40% deposit so that might account for the difference in the cashflow calc. Just purchased so not looking to sell thanks.

Yes, that is including principal. Which could be argued as forced savings, but the budget doesn't see it that way.

I'd say our situations could be very different - we will only buy if it makes financial sense for us, as our long-term (almost medium now!) plan is to emigrate to give our kids access to better universities, should they wish - so we're prioritizing liquidity.

That's a good chunk of equity on your purchase, nicely done. Yes, if we had 40% deposit it'd be only a 20% increase over our current rent - but on the other hand, that would buy a property elsewhere outright, so we'd still be unlikely to purchase the house we rent, and the mortgage comparison would be with the rent on those houses, which still wouldn't add up. (We're fully aware our current rental is a lifestyle choice).

House next door just sold for $1.6M, rented at $620 a week. Some real life figures from the last month.

Wow. The cost to own that house, with 20% down, is roughly per month $8,252 mortgage + $416 rates + $330 insurance + $330 maintenance. Total cost to own per month $9,328.00. ($111,936 annually).

The cost to rent per month $2,686.67. (32,240.04 annually). Once you factor in the interest income of $17,280, after tax, from the same deposit amount ($320k). The cost to rent is actually $14,960 per year.

Almost $100k per year that the renter can put towards a deposit.

Just do it

Yep. The numbers just don't stack up with a 20% deposit. My rough calculations tell me that the crossover point where buying is better than renting is about 45% deposit for this house. This of course assumes that there is no income potential with the house. If you work from home part of the mortgage is a tax writeoff, boarders at $300pw per room etc.

It's a two bed unit. Second bedroom is box room, can barely fit double bed. My partner has just corrected me, rent is $640. Apologies.

You bought well. In Auckland the interest payments for the same house still dwarf the rental payments in many areas, even with a 20% deposit

It's fallacious to think housing investment is limited to capital price movements......

Equally, if not more important for many investors, is the return on investment derived from rental income. When rental return is factored into an assessment (as it should be) houses stack up pretty damned well - as the record over many years/decades illustrates.

This largely explains why houses have become a preferred form of investment. (Term deposits aren't in the same league, especially after tax considerations are factored in.)

TTP

Total BS TTP, the numbers do not stack up at ALL at the moment, in fact current leveraged owners must be shitting bricks......

It stacks up for those that already own more than one house outright and hence can use the equity towards another. They already have sufficient equity to capitalise, and the rich get richer. Not all are leveraged to the gills, there;ll be plenty out there who got a couple pre-2020 at lower mortgages who won't be as impacted by interest rates and will be cranking the rents as far as the market can bare, then others with 2 or more houses owned outright and shifting the after-tax profit from that into paying other houses off, thus lowering the impact of interest rate increases. 2020 was only 3 years ago, people have been in property investment for a long time before this. Sadly it is more likely those that took on large mortgages at the peak, be it FHB or those trading up that will face the biggest strain.

Wrong. It all depends only on your personal financial situation. If the price of food and everything else is going up and your pay is not increasing then the house prices are going up for you. Its pure math and you don't seem to get it. Hell I was totally useless at accounting, couldn't even get the numbers in the right column (and there were only two) at school but its simply income vs expenses or outgoings and the bank very quickly does the math for you even if you are stupid.

Zwifter, sorry to hear that your pay has not increased.....

Its increased through the roof, I'm like you I have a big TD. It went from paying 1% to paying 6% in 2 years. I got a 6 fold pay rise.

I guess when you put it that way, you indeed got a six-fold rise :)

Median weekly and hourly pay increased by 7.1 and 6.6 per cent respectively in the year to the June 2023 quarter.

https://www.nzherald.co.nz/business/wage-growth-earnings-up-above-cost-…

If you are buying or selling ignore the election and get on with it.

The outcome will make little difference, likely none.

"Just do it" This simple Nike slogan is gold, we too often fret and talk about things so much that we don't end up doing anything at all. "Just do it"

Just put your money in a term deposit rather than buy a house? Just do it?

The shittiest investment TDs. People forget that you pay tax on the return which ultimately is a very poor return.

TDs don't have council rates, need to be insured and maintained. Every ten to fifteen years need to be completely renovated.

If you are small minded enough to think that TDs outperform property, good luck. But if I need to spell it out - TDs don’t return you 50-100% in 15 years too. TDs don’t give you leverage to borrow to invest in another property, business etc. Wake up.

facepalm.

While that is true once you have a mortgage free home that you live in and you are not trying to build an empire or are greedy, a TD is a great investment because its a regular return and it takes zero of your time to manage it and comes with very little risk so you can sleep at night and not even think about it. Once you are looking at 60, everything changes in your life and you stop thinking you are going to live forever so the priorities in your life flip upside down.

"If you are not greedy, Term Deposits are a great investment." Zwifter, isn't that another way of saying they are a bad investment!?

"it's wise for investors to be fearful when others are greedy and to be greedy only when others are fearful" - Warren Buffet

We've witnessed plenty of greed, hard saved money (Todays TD's) will go a lot further when the fear of others sets in.

Timely resets are a good thing. With fixed interest rollovers still in progress, we are only part way through the reset of peoples lofty expectations of house price appreciation over time.

I'm not making an assessment on whether term deposits are a good investment just that the logo "just do it" could apply to any investment. Not sure why Yvil picks out housing?

The green shoots could be weeds .....Higher rates will sort them...lol . I understand the fierce and strong move to normalize the last few years high values but looking at some locations , can they stand.?

Very slow for this time of the year and more supply coming, with rates staying around this level not many will be jumping into the market soon, price’s are still way above average wage couples affordability and a investor would be crazy to buy at this level.

House price in Gold Coat is having a massive jump, mass migration from Auckland, Tauranga and Wellington. There will be few basement bargains coming up.

Some truth in this

I'll tell you what's wrong with it, my lad. It's dead, that's what's wrong with it.

It's not dead its pinin for the fjords!

It's just tired following a prolonged sqwark

Just been watching the start of Eves Auctions today (live stream started at 1pm). Simply, cannot believe the ridiculous vendor bidding by the auctioneer and people are bidding against him...good grief.

In what situations would bidding against the vendor be a useful tactic?

Because that's what I did. Basically you have a "Value" in your head as to what you will pay and the vendor simply is moving it to the reserve price. If you want it and don't want to dick about and prepared to pay that then bid until its sold. I will be honest here however in that Trade Me property had a major flaw that's since been fixed so I actually knew the reserve price going into the auction. All the other buyers pulled out with $50K to go but I was prepared to pay the asking price.

What a shocking glitch. I. Surprised there hasn't been legal action against TM or the agencies for allowing it to happen.

I went to an auction a few months back and the vendor only gave the reserve price verbally to the auctioneer 10min before the auction. I thought it was strange at the time. But having heard your story it sounds wise.

Thanks for explanation. So vendor bids in auction provide price certainty for seller and potentially exclusivity from the unconditional requirement for auctions for the bidder so they won't have to compete against conditional offers if the auction passes in.

Seems like quite a narrow set of circumstances for when this tactic would be sensible

what it says is that, the buyers have been pushed to their bottom line, and the buyers find it even harder to buy due to lending limitation. Other words, buyers f**ed, sellers f**ed too.

I disagree, when the buyers can't buy no more and the sellers can't hold on anymore, prices drop hard. This may still happen in the future, but it's not happening now.

assumes people in a position must sell, and move to a cave after sold.

or they could move to a cheaper house, which, if done on a large scale, leads to the potential price drops I talked about.

Yvil, out of interest, would you consider to buy an investment property over the next few years? And what would lead you to doing so?

only 2-3 years ago you were a bit of a property spruiker, but you have become pretty bearish

I wouldn't consider buying an IP now, it doesn't make sense cashflow wise, in a few years if things change and I can find a bargain I can add value to, maybe. Yes, I've become bearish about 2 years ago because interest rates started rising, supply started to catch up with demand, the brightline test was extended to 10 years, interest was no longer deductible from income for taxes, cost of renos went through the roof, healthy homes standards required more expenses... These are a lot of headwinds happening at the same time, enough to change my view from investing in propery is lucrative, to not being a good investment anymore. Cheers.

Thanks, good response.

Interesting that there’s many who still see it as a good investment, right now

Oh Dear, How Sad, Never Mind......

As a FHB I find all of these reports really difficult to get a read on, and often conflicting.

For example, whilst this piece on Interest ran, RNZ also posted this: https://www.rnz.co.nz/news/business/499973/house-prices-stabilising-increased-sales-in-september-reinz-says

What's the best/most trustworthy source that should be used in your opinion(s)?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.