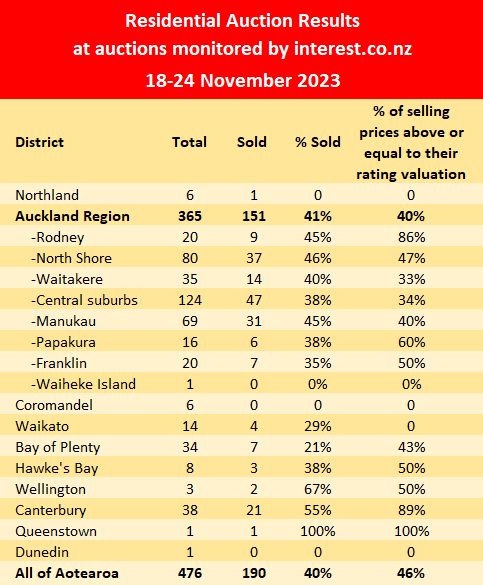

Last week (18-24 November) was the second busiest week of the year in the auction rooms, with 476 properties on offer at the residential property auctions monitored by interest.co.nz.

That was down very slightly from the previous week when 489 properties were on offer.

However it was a record week in the Auckland auction rooms, but only by a whisker, with 365 properties from around the region going under the hammer, up marginally from the previous week's 2023 record of 360.

Of the 476 properties on offer last week, 190 sold under the hammer, giving an overall sales rate of 40%, barely changed from 39% the previous week.

However the last few weeks' sales rates have drooped back to around 40%, having previously been in the mid-40% to mid-50% range since late July.

Of the properties that sold, 46% fetched prices that were equal to or greater than their rating valuations, which was about average over the last couple of months.

The table below shows the district results from the auctions around the country monitored by interest.co.nz last week.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

100 Comments

I wonder why?

Thank You NZ First.

Bit more cold water on the Ponzi

I think it was a dead cat bounce regardless of NZ First

Oh....did it actually bounce?

Well a little, right? Up 2-3% in the past few months

Okay, I concede, there was a small dead cat bounce then - LOL!

Headlines deploying words like "uninspiring", "flat", "no sign of hoped housing recovery", "sales rate dipping in recent times" and my personal favorite "anybody seeing green shoots in this housing recovery must have been smoking them" are not in keeping with a sustainable recovery though.

Mic check.. mic check.. have all the spruikers been banned or are they high at this time of the day..

Its a work day for most. Including apparently for retired poppy

....and it appears you're allowing me to live rent free in your head.

Hahaha oh well that makes two of us.

You wish.....( 🤡 )

....and it appears you're allowing me to live rent free in your head.

Good to see you acknowledging rent, Retired-Poppy......

A glimmer of hope for you.

TTP

Looks like we are in the midst of an Ireland style longterm housing crash.

"Things were looking especially weak in Wellington, where house sales were at multi-decade lows, excluding lockdown periods, and house prices dropped 2% month-on-month. Days to sell rose by five."

We won't see prices drop by 50%. But we will continue to see prices soften and stagnate, all the while inflation will merrily continue along at 4% to 6%. So for every year that prices stay flat it results in an actual fall in property value of ~5%.

Compound that reduction in buying power over 5 years and (exlcluding rates, mainteance and insurance) and it is a further crash of 27%. I wonder when savvy investors will wise up and sell up?

It's not that people don't want to buy, they do. It the disconnect between debt serviceability and the expectation of vendors price. This adds up to Greed being the winner (very low sales) with a side order of record bank profits.

Newsflash to sellers....New debt is 7-8%, not 2%.

Yep, and tested at 9 to 9.5%…

As someone who'd like to upgrade house this is the fundamental problem.

Our current mortgage payment on the townhouse we bought a few years ago is not too bad at all. Even when the second half of our mortgage kicks over to 7% in January 2024, it won't make much of an impact on our finances.

We bought for about $550k, I'd guess the house would sell for maybe $700k now but not too sure. However, if we were to buy the nice four bedder down the road for $1.25 million, it's just such a massive increase to the mortgage payment. To have to service an additional $500k of debt doesn't sound like much fun.

It goes from being a case of having little mortgage stress (and the ability to enjoy a nice holiday every so often, have a decent car each and all that sort of 'nice to have' stuff that we should really knock on the head for either strict personal finance or property ponzi participation purposes ... but life is for living right?) to far more worry about what happens if my business slows, or my wife loses her job.

So we are looking instead at spending a bit of cash on doing the current place up to extend its lifespan for our family for a few more years. For example getting a nice covered outdoor area, and potentially looking at ways to convert the 'double garage' (if both your cars are Fiat Bambinas) into a home office to effectively turn a 3 bedroom into a 3 bedroom + office ... in fact if anybody has suggestions for how to achieve such an outcome I'm all ears.

change you user name to smartthoughts.

haha thanks, I appreciate it (although wait maybe until I start commenting on the political posts).

But in all seriousness, what is a young family like ours meant to do in such a situation? I'm not seeking specific financial advice, more posing that as a general question.

The choices are either stay put - which is manageable and probably $20-30k of expenditure could really transform the existing place. Or go hundreds of thousands of dollars deeper into debt and wind up potentially too stressed to enjoy the newer home.

We could sell up and move further out of town to one of the new subdivisions or a satellite town like Lincoln or Rolleston (where it's probably more like $150-200k extra to add another bedroom and living area, and a bit of grass) but then you've got higher commuting costs and time, and I feel like if property prices did go down further it's potentially those nondescript subdivisions that could particularly underperform.

I guess the sensible thing to do is the latter than then put every spare dollar into smashing out the mortgage. But then what is the opportunity cost of missing out on the memories of a nice family holiday, or being able to go out with friends for an enjoyable dinner as opposed to having to stay home and pinch pennies ... decisions, decisions I guess.

I think it depends if you have kids and what age they are. We made the move from a 2 bed townhouse to 4 bed house and it was a better in some regards (quieter mostly) and worse in some (kids missed sharing a room!).

Until the kids are knocking on their teens I don't think a house gives you anything, I would totally put my money into memories in preference to a house.

We've just got the one (two years old) and no plans for another for a couple of years, although you never know right?

Agree with your last point.

Me and my brother grew up in an ok house. It was in a nice part of town, but nothing flashy. However, we were lucky enough to go on lots of overseas and local holidays and now in my 30s I don't think I'd trade those memories for having had a bigger bedroom or a 'rumpus room'.

My wife insisted on a "play room" when the kids were that age. Now it barely gets used. I guess it will when they are older, although then the requirements change (you want young kids close to you and older kids far away)

Put the play station in the play room and you will have all the peace you want :D.

We upgraded to a 4 bedroom 2 bathroom just before our daughter turned 5 (late 2021). She has a playroom about twice the size of her bedroom, yet it's just a place to dump her toys when they're not cluttering the rest of the house.

I would stay put and get onto making baby number 2. Then when you are over the worst of preschool childcare costs maybe look at upgrading house. From my experience you don't want to wait too long to start for number two then have issues and have to fork out for IVF etc..

Yep will second this advice, if you are able of course.

We significantly increased the size of our house, but there are negatives like more cleaning, more distance to cover, etc. I doubt it improved our life much considering the cost. We have since looked at downsizing to get rid of the mortgage but the smaller options had other drawbacks.

"the sensible thing to do is the latter than then put every spare dollar into smashing out the mortgage" - only if you assume capital gain or if you think the bigger house will make you happier than the debt will make you sadder. If you exclude capital gains, then your quality of life needs to improve by more than the increase in interest costs for it to make sense. Do you think it will make you $500 a week happier for example?

Just rent a place you want to live in and rent your place out. The difference in monthly rent top up will be tiny compared to mortgage payments which is dead money to the foreign banks.

I was almost in your position like for like 6 months ago. What I did was buy a home with a granny flat. The rent from the minor dwelling was counted in my mortgage assessment. My net monthly mortgage repayment actually decreased. Not sure if it is right for your circumstances. Your idea to expand your current home sounds wise too.

Reno's might run to $100k plus so be careful not to over-capitalise. Also if you want to do a bedroom/garage conversion be worth running that by your Body Corporate to be sure you are not going to run foul of any bylaws etc.

Yes would definitely want to manage the costs.

Outdoor area isn't bad, I've priced that up doing some DIY at about $10k all-in for what I want to achieve.

The office might not be doable, but then again I could just put some carpet down and the desk and use it most of the year apart from perhaps the coldest and/or hottest days.

I’m also considering a few little adjustments to our townhouse, both to make it better for us and to also add value. Mainly the outdoor space. Ours is an ‘ok’ size by recent standards, but we aren’t making enough of it.

Covered carparking is getting rarer (we don’t have it) and really has value, so maybe think about losing that to an office space.

Yeah the garage to office conversion would only be a thing if we stayed in the house long enough for another kid. Agree that having covered carparking, let alone a garage, is increasingly a luxury.

It's the outdoors space in ours as well that really needs some work.

I hear you. We have about 28 sq m of courtyard, but 40% of it is covered by worthless, scrappy shrubs that came with the property that reduces the usable area alot. There is a nice specimen tree that we want to keep, but apart from that we want to do decking for the whole courtyard.

Some sort of pergola would be good too as the courtyard is open to all the elements.

Ours is totally barren, so there's nothing much good to loose.

We are looking at one of those pergolas (with the ability to add side shades etc). Pricing varies so much but I think me and a friend will just put a morning aside to DIY one of the Trade Tested/Mitre 10 ones and I'll add some lighting to it myself.

I reached out to several 'custom' providers and none of them even bothered to come back with pricing or next steps.

re ... "Ours is totally barren ..."

Yup - definitely! You should get your money back if you control costs, do a good design that meets the needs of the next owner, and do most of the work yourself (turn your time into cash). Coverings for those less perfect days is like adding another room. Nice patios help sell the place. Barren ones are blockers. If it is south facing, absolute minimum spend.

My advice on townhouses (in general) is that money spent on the house itself is seldom recouped - unless what's there is seriously old/decrepit/broken and then just replace like with like.

You said you need (want?) something bigger. Best bet is to rent/buy something bigger. But spend lots of time investigating where. (3 rules of property.) If capital appreciation is a requirement, look for a bigger section with a smaller house (and don't forget to check the zoning!)

Annualized capital return: Bought: $550k. Could sell $700k, less all costs, say $650k. Owned for few years? Lets say 4 years. -> about 4.3% (tax free) per year. Not too shabby given where the market is.

Well Luxon sataed this morning that he fears recession is looming..

Just more icy water tipped on already cooled housing market.

..didn't I hear from Nicola the old 'we opened the books and it worse than we thought' this morning?

History will show we are in a recession now.

We're being softened up, to get far less, as the NACT knew they could never deliver on their promises.

No surprise sales rate has drooped given the still lofty price point and 8% money! From here, indications are that, at best, the market will remain flat price wise up till Feb, then come Autumn a nasty reality check will again ensue for the besotted speculator and most importantly a more viable entry point for the patient FHB.

Houses are for living in not speculating on.

Isn’t this one of the most buoyant times of the year usually for the market? What happened to the much hyped’green shoots’?

Yes, it's certainly a fizzer. TTP may be along shortly to diligently remind all and sundry of yesteryears performance, price movements rarely go in straight lines and DGM's are all losers who will never own homes...😂

At current interest rates house prices are still way too high. The number one reason house prices got to such high levels is because they were still affordable to average people due to very low interest rates. That is no longer the case.

Better just wait for the new government to get into gear and the RBNZ to start to signal rate decreases or at least this is the peak for this cycle. Will not take much petrol on the fire this time to kick it off, first mention of rate decreases and away it goes again.

Seems consistent with the water cooler reckoning and all the usual themes. Central planning, the mythical cycles, and the infallibility of the Nu Zillun wealth prosperity model.

It won't. Water cooler people are generally ignorant of the wider themes. Supply will increase and prices will go nowhere... NPS-UD, MDRS, Unitary plans ... blah, blah, blah (I really can't be bothered writing it all again.)

It will be at least 2025 before there are any truly meaningful lifts in the market.

My pick is flattish / small increases in 2024, and the same in 2025 until things get hotter in Spring of that year.

My pick is flattish / small increases in 2024, and the same in 2025 until things get hotter in Spring of that year.

OK. I don't play or pay attention to predictions unless I understand the model and / or rationale behind those predictions.

In short:

- no more interest rate increases, but no significant decreases in 2024. Without the latter, the market won’t truly heat up

- decreases will start accumulating through late 2024 to late 2025. OCR could be 3.5-4% by spring 2025, and retail rates circa 5 to 5.5%. Enough of a decrease to start breathing a little life in to the market. Restoration of interest deductibility might have started to have some impact by then, too

Cost of finance is the key variable in what happens to the market in my view, hence my prediction

Note - I think there could be some significant regional variations. For example, I think Wellington could be very weak for many years with the pending cut in headcount which will suck quite a bit of demand out of the market there.

That's not a model though.

Models are extremely overrated.

You asked for a model and/or rationale. I provided some rationale. Disagree with that rationale?

You asked for a model and/or rationale. I provided some rationale. Disagree with that rationale?

It's not whether or not I disagree. Your thinking sounds logical, even if the outcomes may be different.

My thought basis is built around:

1. Refute the null hypothesis

2. Karl Popper. Theory should make predictions that can be tested and the theory should be rejected if these predictions are shown not to be correct.

So no disrespect, but a rationale really needs some kind of confirmation if built into prediction.

My pick is flattish / small increases in 2024, and the same in 2025 until things get hotter in Spring of that year.

Noted, thanks very much

That’s my best guess, probably should be ignored 😂

Up 10% in 2024...

Sticking with my 4 to 5% prediction. 10% is possible but rates would have to take a big dive mid 2024 and I'm only thinking a 25 to 50bps drop in 2024.

"Better just wait for the new government to get into gear and the RBNZ to start to signal rate decreases or at least this is the peak for this cycle"

My bet is 2026 and election will be just around the corner!

Probably nothing. But just a little peek at the the U.S. housing market

Home Sales Collapse, Prices Drop Further, Supply Jumps. People Are Finally on Buyers’ Strike

Sales of previously owned houses, condos, and co-ops, at a seasonally adjusted annual rate of 3.79 million homes in October, have collapsed to levels not seen since the worst three months of the housing bust: The post-Lehman-bankruptcy November in 2008 (matched it) and July and August 2010.

https://wolfstreet.com/2023/11/21/home-sales-collapse-prices-drop-furth…

It's not nothing, but the market there is very different from the one here. The mortgage construct, the supply line, the infrastructure approach, all different.

It's not nothing, but the market there is very different from the one here. The mortgage construct, the supply line, the infrastructure approach, all different.

Yes yes. I know we're different. Aussie is different too.

And our banks are the best in the world apparently.

Seems to be a lot of conflicting stats in there. Form example median days on the market looks low by historical standards.

The negative knuckle-draggers will see what they want to see.

Meanwhile Auckland is already up 6% in the last quarter.

The negative knuckle-draggers will see what they want to see.

Or have it interpreted for them by the media. That's typically how most people consume data. Most lack the time, chops, and accessibility to do it themselves.

Knuckles all fine here mate .... have a look at my post here for the last 12 months

Get out there Cotey and purchase a few houses if things are that rosey :) ....put ya munny where your mouth is !

Oh wait !! ..... you want OTHERS to get out there and buy, because your own livelihood depends on it !

Typical ....VESTED INTEREST at play !

That's a solid horse kick..

niiiieeeeegggggggghhhhhh ..... yells the Crazy Horse !!

The "spruikers" very quiet today ???

Oh well, they "know" what they are doing, so we will leave them all to it :)

Here's a bit of anecdotal evidence - heard a work colleague (young couple with 2 children) are now paying $6,000 a month in mortgage payments... truly marvellous.

Meanwhile in granny herald ..... Price change last 12 months according to property analysts CoreLogic:

Auckland - 8%

Sydney + 9%

Wellington - 7%

Melbourne +2%

Christchurch -2%

Brisbane +8%

Don't worry folks, our resident "Spruiker" , Taking the Proverbial et al will no doubt have a positive spin on the above .....to polish the turd.

Looking at Australian rental situation, it goes to show the grass isn't always greener on the other side when the farmer lets in all the neighbours herd to graze and scarcity for resources starts to bite faster.

$6000/month? They obviously (and luckily) got much better than average incomes.

That might not be down to luck. Imagine doing everything right in life, having a real good job that pays well, and then having to live very cheaply so you can pay a mortgage on an average house.

An excellent example of how the Great Unwashed consistently miss the boat.

The bottom of the market in Auckland was May 2023 - this cannot be seen with Annualised figures.

Cotey ...as a part of what you call the "Great Unwashed", do you ever look at what is happening to property markets overseas ie US, UK, Canada and Australia ?

All countries with a higher GDP per capita and stronger currencies than NZ .....so how can property prices keep on the "upward trajectory" you spruikers all attest to ? (this does not include price increases due to inflation ONLY)

My father who grew up in hard years used to drum it in to myself and siblings "get your first house debt free as fast as possible never borrow against it ,that way no matter what happens in the economy you can always have somewhere to sleep at night'

That's good advice!

Good advise. But we have let society be engineered into the endless bank profit model instead.

Looks pretty steady out there... not bad when you consider we're operating under record high interest rates & property prices. Now we actually know how the Government's formed will it bring any more action, property investors be keen again?

by Nifty1 | 27th Nov 23, 1:48pm - "record high interest rates & property prices"

?

R-P .....it's like shooting ducks in a barrel !! ....the lengths they will go to !

More like the depths they will plumb......😂

Really curious on what your position is. You have both spruikerish and anti-spruikerish views. Quite curious - not necessarily incompatible.

My best guess is:

You bought recently but are worried about negative equity. It’s not in your interests for the market to fall further. Yet as a recent FHB, at the same time you have some empathy for FHBs.

OR

You bought maybe 4-5 years ago, you have some sympathy for FHBs as a fairly recent buyer, but think that now is as good time as ever to buy for FHBs if they can, hence your viewpoints opposed to ‘DGM’ posts. Ie. That some FHBs might miss out all together if they listen to the ‘DGMs’ and hold off

If I may posit something, just from the perspective of a prospective FHB in Auckland, that despite these price drops over the last year or two, houses are still prohibitively expensive. I'm sure I'm relitigating what's already been said multiple times in comments on this site, but even when accounting for the price drops, the current financing rates actually make house ownership MORE expensive for us than during the boom, where rates were in the 3% range. The real issue is that people selling houses think that they're selling into the same market or context as when they purchased it, which just isn't the case. But this is keeping prices frustratingly high despite the actual market conditions.

Added to this. It's really exhausting having to dance the dance with real estate agents, when they're being anything but 'real', constantly misleading us with price indications, and frankly wasting our time giving us hope that houses are within our range, only for them to sell 200-300k above their 'indications'.

I don't blame any of my fellow Kiwis in their 20s and 30s who are packing up and moving to Australia. In reality, if you want to do any of the traditional 'life goals', buy a house, start a family, even have a modest wedding, they are next to impossible in New Zealand now.

To make things even more grim for people of my generation, this latest government is looking to reward some of the very people that got our housing market into its current state, by reducing the brightline test and reintroducing interest deductibility. But hey, thank God the 'war on landlords' is at an end, and let the war on the rest of the country resume at pace.

Housing is a basic human need, and the more money Kiwis have to put into keeping a roof over their head, the less they can pay for food, heating, healthcare, savings, even putting back into our economy and investing in enterprise. At the root of our low productivity, stagnant growth, and reducing living standards is expensive housing which drains so much productive capital out of our wallets, and sends it to Australian banks, and the pockets of landlords only to help buy more property and perpetuate the problem.

Sorry for my rant, but this country has lost its vision, and it's frankly depressing.

Well put.

Yes it’s tragic.

Most honest piece I have read today ..... thank you FHBtears

Yes, you are so right ....the more these clowns drive house prices up (with interest rates more than tripled !!) the more they will drive the NZ economy down.

The banks are hell bent on getting as much cash flow from your pocket as possible (I hate those "family friendly" ads. where they are really driving younger families to the financial brink !) and that is their ultimate "modus operandi" ....profit at all "Costs" from their so called "customers" - they really should call them "cash cows" ! .....moooooooo !!

If house prices keep going up, more than the "brightest and best" will leave and even these "cash rich" immigrants BS the media feed us, already can't afford to buy a house, let alone paying these rents (in AKL) ....and for all you greedy landlords out there salivating at the rising rents, they will only cram more people in to your damp, cold, south facing Mt Roskill sh*t box !

Yes, we are only going to go downhill at this rate ....and National are not helping either !

Too many VESTED INTERESTS in the pot !

Sorry, I can't be more positive, but I totally understand your frustrations.

The banks are hell bent on getting as much cash flow from your pocket as possible

Naturally. Their "product" basically comes out of thin air and the taxpayer picks up the pieces if it all goes to seed.

They live a charmed existence.

FHBtears, this is indeed a sad state of affairs our country finds itself in. It sickens me reading the various posts from the vested arguing how property is currently a great investment yet, for those who, like yourself, want to purchase a home to live in, it's prohibitive, not only price wise but interest rate wise.

I am a one home owner of 26-years and would very much like to see house prices free fall to a point where it increases our home ownership rate significantly. Houses are for living in and not speculating on. There is really only a need to own one home not multiple. Anything beyond that is purely greed driven.

I wish you all the very best going forward :)

Thank you for your kind words, RP.

And to be honest, I count my partner and I as lucky. We’re both on okay incomes and have no dependants.

I really feel for those who are single income, lower income and/or have one or more dependents. I can’t imagine the hardship they’re enduring to keep afloat, whilst in all likelihood, renting substandard housing. I can’t help but feel that things are going to get worse, before they get better in the coming years. I just hope that we don’t have to hit rock bottom before we realise this.

Even luckier - you are just a prospective buyer and not someone who "climbed the ladder" 2 years ago, they got even more shafted.

TTP will be here soon to perk you up!

Seriously, we were very lucky to buy a house in Wellington's northern suburb in the mid 90s when average price was around 250k and our combined income was 52K. it was so doable back then.

250k is the deposit these days

Sad indeed and this is why so many are piling out of Auckland to the regions also. If you have to move to achieve your goals for such a key milestone then it appears that many are willing to do so and start fresh somewhere else, be it in NZ or overseas.

It's not just NZ, it's the whole world that "lost its mind". You can't just escape to another western country for more affordable housing. Aus might have lower mortgage interest rates, but they will slap you with tens of thousands of $$$ in Stamp Duty tax to buy an average priced house in the capital cities (Thinking Melbourne/Sydney mainly). So you have to save even more for the upfront costs to buy a house in Aus, and to make it worse their deposit interest rates are lower too so it'll take you a bit longer to save the same amount of money there. ( matching equal $ for $ deposit).

An average house in Melbourne costs roughly 950k. Upfront Stamp Duty tax on that is 52k. That's before even the deposit or any other fees that one has to pay upfront. In Sydney the average house price is well above 1mil, I don't even want to calculate stamp duty costs on those prices, it's too depressing.

Good luck to those who move to "greener" AUS pastures to escape NZ's high housing costs.

I think it might be best to figure out a way to move/live to/in a smaller town in NZ.

True, although Adelaide and Perth are much more affordable than Auckland, and both quite nice cities.

That's true. But there are also some other things to potentially consider such as the fact that Perth/Adelaide are further away from NZ (Family/friends) than Sydney/Melbourne. But then Hobart/Brisbane might not be, so ultimately it's about weighing out options. Also if you find a cheap house in the capital cities (below the set thresholds for each state) then there are some Stamp Duty concessions for FHBers. Either way, the point of my post was to respond to something I saw in the comments above and stress that Aus is not the housing dream that some NZers might believe.

I lived in Adelaide for three years, more than ten years ago. Really nice city, very liveable. Horribly hot for 3-4 weeks of summer, but apart from that it has a really nice climate. The flight to Auckland isn’t bad.

The only reason I came back was my mother’s ill health. She lived in Wellington, if she had been in Auckland I might have stayed in Adelaide (the extra flight to Wellington was inconvenient and costly)

House price is quite correlated to job opportunity

Yes, having watched some UK house programs, they don't seem much cheaper there either, unless you buy a tiny little unit with very little land. At least they have that option I guess, we don't really have many 1 bed basement flats, hence our average house price is higher.

Amongst everything, AirBnB is back in force over there which is making things harder again sadly.

Just wanted to say - we're moving to Aus. My wife is still in shock - took her less than a week to find a job, and when she got the contract, they'd offered her double what she is on here (accounting for exchange rate). At the same time as halving our rent.

Sounds like you guys found a way to get ahead. Good on you. You might be able to make/save enough money there to come back to NZ and buy a house here!:)

People moving overseas to make/save money in foreign currency and then coming back to NZ to buy a house here has been a way for some to get ahead, for as long as I remember. I know people who went to live in England or Aus, etc. and came back with savings converted to NZD from GBP or AUD.

Thanks for sharing FHB tears. It's the elephant in the room that the government don't talk about. Affordability IS the answer to the problems they are trying to fix. Unfortunately there are people more powerful than you or I that dictate what happens in NZ. John Key in his current role, Christopher Luxon, the boomer generation... mate, the deck is stacked in favour of the house. The country is built on over priced houses. It's just the reality of it and nothing changes until people rise up. It's corrupt, it's the only word for it.

I suspect you are speaking for the many disillusioned youth across NZ. I have 2 Young ones working and living in London and have worked hard to gain further education and qualification with a constant view of returning home and settle down, which was planned for next year. unfortunately, they are now telling me they are heading to AU. They feel it’s the right long term position for them. This I’m sure is very similar to many kiwi families. I do hope that someone involved in government can work policy towards making this country great again and stop this pure speculative financial gain of property. The impact across our country is entering a very depressing position. Do property speculators actually believe they are contributing in any way towards the health of New Zealand or is everything driven by pure greed and accumulated wealth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.