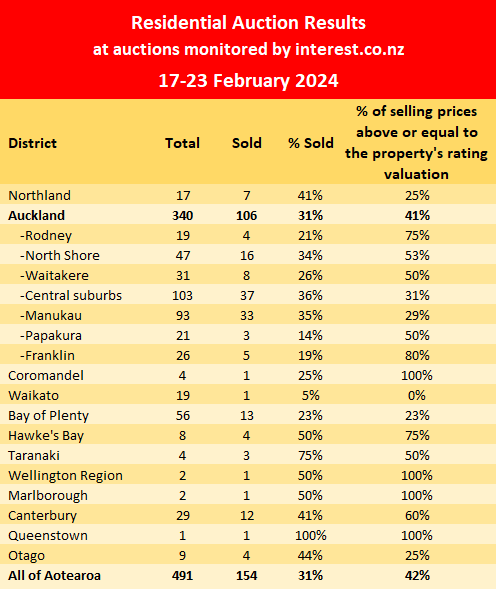

More properties are being offered at auction but the sales rate is declining as market activity moves into top gear.

Interest.co.nz monitored the auctions of 491 residential properties over the week of 17-23 February, up from 449 the previous week.

But less than a third (31%) of the properties offered at auction sold under the hammer, suggesting the market remains soft as it heads into the busiest time of the year.

Prices also appear soft, with just 42% of the properties that sold achieving prices equal to or above their rating valuations.

The market appeared especially soft in the Waikato. There, just 5% of the properties offered at the auctions monitored by interest.co.nz were sold under the hammer. And of those that were sold, none reached prices equal to or above their rating valuations.

The latest results suggest there are plenty of properties on the market for buyers to choose from, but they are playing hardball on price.

That means vendors will need to be particularly well informed about price trends in their area and realistic in their price expectations if they want to achieve a sale.

Details of the individual properties offered at all of the auctions monitored by interest.co.nz, including the selling prices of the properties that sold, are available on our Residential Auction Results page.

The table below shows the latest results by district.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

80 Comments

1/19 in the Waikato! Reserve prices need some serious adjustment.

Housing market in limbo - awaiting clearer signal re interest rates.

RBNZ's mandate re inflation means it will seize the opportunity to keep the brakes on. After all, Governor Adrian Orr is keen to keep his job and, in my opinion, he deserves to do so.

TTP

The current RBNZ excuse is non-tradeable is still high. Will spin that for months/years

And....if we don't sort the supermarket duopoly, building materials market and insurance companies out, non-tradeable will remain high and even increase!

This new govt has more determination. Despite losing some parliamentary days this week they have still committed to reaching the 100 day target on time.

You mightn't agree with their agenda but at least they are committed to making it happen. Happy days

It's a lot faster to knock a house down than it is to build one.

Is this a joke? Didn’t they lose an afternoon or parliament?

Committing to reach an arbitrary target they made up for no purpose other than spin shouldn’t really be applauded.

@ Pete M

well said . And let’s not forget local authority rates increases lThey are all broke... Interest rates are just one factor . Toss in global events on top 😊

If you watched the auctions I have no doubt that many didn't even get a bid so reserve price wasn't that relevant unless it was super low and advertised as such. Also the reserve price at an auction is not set in stone as many, many, auctions have vendors lowering their reserve on the fly as the auction unfolds.

I am often surprised by the one vendor that does get a good offer, turning it down after every other property passed in with no bids. Some were even advertised as "must sell", "urgent sale!" and so on. I like to watch these and see what eventuates.

There’s still a lot of greed in the market, and I suspect some denial that prices are going to drop.

Good intel cheers

This will weigh heavily on the RBNZ's OCR decision... the property market must go on 📈

Yes I saw Orr at an auction room this week, shaking his head and writing in big numerals on his notepad, “0.25!!!”

We all know what Orr did in 2020 when he thought the propery market was going to collapse...

We all also know house prices are way over valued compared to income.the people who did manage to off load a property recently Will be very happy as the next phase of crash is not the way, I expect another 20% of over next 18 month and it could be a lot more if a recession sets in.

More will be selling with conditional agreements after auction, lets not sweat

Coming up to March madness month which is traditionally the busiest real estate month of the year

March-mirage might be on the cards...

A message for those patient FHB's who have temporarily put their lives on hold while watching their savings grow, "the evidence is obvious and time is on your side"....

Good morning saar

‘Transitory’ inflation is still a concern and is chipping away at savings. If they don’t get on top of it then the waiting game may not work out too well. Thoughts?

Shhh... dont say that or he will be grumpy all day

Not necessarily the case, depending on what happens from here with house prices.

At the end of the day, inflation is a rise in the general prices of goods and services. However, this increase is not uniform across all goods and services. As we don't all consume the exact same bundle of goods and services, the impact of inflation is different for everyone, depending on what you're buying.

So, if you have savings that are earmarked for a house deposit, which is the only thing you intend to spend them on, does it matter if these savings can now buy less TVs / blocks of cheese / petrol etc? No. All that matters is what happens to house prices.

"All that matters is what happens to house prices."

A reminder for owner occupier buyers - choose your scenario and act accordingly.

Which will the owner occupier regret most:

1) missing out on future potential gains in equity?

2) potential actual loss of their invested equity or even potential negative equity?

For owner occupiers, a reminder of the impact of leverage (it amplifies property price changes both on the up and down):

Scenarios of impact of leverage on equity, assuming an 80% LVR for owner occupier, for a recent $1,000,000 property purchase, $200,000 initial deposit, mortgage $800,000.

A) Scenario - property price rise:

1) property price rises 5% to 1,050,000, mortgage 800,000, equity 250,000, so 25% gain in equity value from 200,000.

2) property price rises 10% to 1,100,000, mortgage 800,000, equity 300,000, so 50% gain in equity value from 200,000.

3) property price rises 15% to 1,150,000, mortgage 800,000, equity 350,000, so 75% gain in equity value from 200,000.

4) property price rises 20% to 1,200,000, mortgage 800,000, equity 400,000, so 100% gain in equity value from 200,000.

5) property price rises 25% to 1,250,000, mortgage 800,000, equity 450,000, so 125% gain in equity value from 200,000.

6) property price rises 30% to 1,300,000, mortgage 800,000, equity 500,000, so 150% gain in equity value from 200,000.

7) property price rises 35% to 1,350,000, mortgage 800,000, equity 550,000, so 175% gain in equity value from 200,000.

property price rises 40% to 1,400,000, mortgage 800,000, equity 600,000, so 200% gain in equity value from 200,000.

9) property price rises 50% to 1,500,000, mortgage 800,000, equity 700,000, so 250% gain in equity value from 200,000.

10) property price rises 100% to 2,000,000, mortgage 800,000, equity 1,200,000, so 500% gain in equity value from 200,000. (i.e property price doubles every 10 years)

Remember, the owner occupier must be able to hold on under ALL economic environments (including any potential significant reduction in household income, higher mortgage interest rates).

B) Scenario - Property price falls:

1) property price falls 5% to 950,000, mortgage 800,000, equity 150,000, so 25% loss in equity value from 200,000.

2) property price falls 10% to 900,000, mortgage 800,000, equity 100,000, so 50% loss in equity value from 200,000.

3) property price falls 15% to 850,000, mortgage 800,000, equity 50,000, so 75% loss in equity value from 200,000.

4) property price falls 20% to 800,000, mortgage 800,000, equity is ZERO, so 100% loss in equity value from 200,000.

5) property price falls 25% to 750,000, mortgage 800,000, equity is NEGATIVE 50,000, so 125% loss in equity value from 200,000.

6) property price falls 30% to 700,000, mortgage 800,000, equity is NEGATIVE 100,000, so 150% loss in equity value from 200,000.

7) property price falls 35% to 650,000, mortgage 800,000, equity is NEGATIVE 150,000, so 175% loss in equity value from 200,000.

8) property price falls 40% to 600,000, mortgage 800,000, equity is NEGATIVE 200,000, so 200% loss in equity value from 200,000.

Inflation has been about 7% p.a. since Nov 2021. Did leveraged property keep up with inflation?

Here is what the property promoters with their vested financial self interests don't tell you and don't want people to know.

Here is an example of how a potential buyer was saved by their lender. This guy didn't realise it then, but being rejected excessive credit from the bank was actually a blessing in disguise. Being declined for a large mortgage was better than getting approved to buy a house when house price risks are extremely elevated.

Nov 2021 - https://www.newshub.co.nz/home/money/2021/11/first-home-buyer-not-very-…

So what would have happened if this guy bought in Nov 2021? Let's take a look at what could have happened.

A) buying a house

Nov 2021

REINZ median house price in Auckland: 1,300,000

Mortgage at 80% LVR: 1,040,000

Equity: 260,000

Jan 2024

REINZ median house price in Auckland: 975,000 (-25.0%)

Mortgage: 1,040,000 (assumed to be interest only to illustrate impact on equity) - note that the LVR is now over 100%

Equity: NEGATIVE 65,000 (-125% of initial equity, negative equity position)

B) keeping money in bank, and continue saving for a house

Nov 2021

Time deposit: 260,000 (same as house purchase)

Jan 2024

Time deposit with interest (after tax of 33%): 271,000

Now that deposit can be used to buy a house at the current price. This results in a smaller mortgage (704,000 vs 1,040,000 if purchased in Nov 2021), reduced total interest payments over 30 years.

REINZ median house price in Auckland: 975,000

Equity 271,000

Mortgage : 704,000 (LVR of 72.2%)

So from an equity perspective, keeping money on time deposit at the bank was a far better outcome than buying a house in November 2021.

Remember back in November 2021 when most property commentators were saying that house prices in NZ couldn't drop by more than 10%? Well they've dropped more than that.

What do people not know that they don't know?

Here is something that most people don't know, and don't see. (And the property promoters with their vested financial self interests won't tell you).

On an inflation adjusted basis, price change from the peak REINZ median house price in the following areas:

1) South Waikato: -40.6%

2) Porirua: -43.0%

3) Kawerau: -43.8%

4) Central suburbs of Auckland: -45.0%

4) Buller: -47.0%

6) South Wairarapa: -48.8%

Remember, this is before the impact of leverage.

This is something most people do not realise. The property promoters with their vested financial self interests won't tell you this.

Peaker vs Buyer Today

How does this compare with a Peaker and a Buyer Today (BT) in NZ?

1) Peaker

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

2) Buyer Today ("BT")

The current median house price for Auckland is $975,000

For a buyer who waited, and used the same $260,000 equity used above, the mortgage at this price would be $715,000 (an LVR of 73%)

The Peaker has a mortgage which is higher by $325,000 (mortgage of $1,040,000 for Peaker vs $715,000 for BT)

As a result of that additional borrowing, at a 6.8% mortgage interest rates over 30 years, Peaker is paying $770,000 more over the 30 years than BT (30 years x $25,667).

Assuming same incomes, and same living costs (food, travel, etc except mortgage), BT can save the $770,000 in payments that Peaker is paying.

The annual payment on the additional mortgage of $325,000 is $25,667 per year.

1) Peaker pays $25,667 more per year than BT.

2) BT instead saves that same $25,667 per year. At a deposit interest rate of 5.8% (after 33% tax is 3.9% p.a). Saving $25,667 per year and earning 3.9% per year in net interest after tax for 30 years comes to a total of $1,415,685.

$1,415,685 - this is money that BT has available for retirement after 30 years that Peaker will not have.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

Yup. Lets also highlight agentsand other vested interests don't care about this sort of thing. They just want the ticket clip $$$.

"‘Transitory’ inflation is still a concern and is chipping away at savings. If they don’t get on top of it then the waiting game may not work out too well. Thoughts?"

Do your own calculations for your circumstances to make an informed choice / decision. Refer my examples of calculations to consider.

An outstanding thread of comments CN. In 2021 I thought the market was nuts based on a little bit of amateur history lessons but I never broke it down into calculations like you took the time to do so above.

Cheers

Not so 'financially viable' at present for many and how sustainable would it be if lower rates returned because eventually it just climbs to the same levels whereby it becomes not financially viable. There is an unseen limit which is likely why sale by auction was popularised and property seminars will forecast the sky is the limit...but reality has boundaries . Plenty burned in China and values here are out of kilter with the average punters pocket. Making the record highs stick is the hope of all that have vested interests but it looks like the price being sought is presently still too much for those aspiring to RE. Some folk have good memories and remember when values were more reflective of social factors particular to different locales and regions , now everyone wants top dollar for very basic . 'The multiplier' has bottomed out (prices doubling every 5-7 years) because when 1 million turns into 2 million.... and 2million to 4 million....? Where does that leave the majority of young aspiring and how does that look on the risk sheet ?

The multiplier has happened through a combination of wage inflation, increase from 1 to 2 worker households and the lowering of interest rates.

Dropping rates to 2.5% again would in theory reverse the falls, but you'd need interest rates to continue to fall for the multiplier to continue. Or, wages could always double over the next 10 years. That would be a nice way to inflate away today's debt, like what happened in the 70's/80's.

Yes and if you read some central bankers publications over the last couple years, interest rates that level do not provide enough buffer for them to have freedom to move either way. I believe the uk wrote exactly of this last year, treadlightly posted a link which I don’t have on hand.

The other consideration is yield. Interest rates being so low pushes values up in relation to yield. This is why we see values with a 3-4% rental yield, because rates of yesterday could allow for it. For a leveraged rental, where do you go from 3% yield?? Immediately negatively geared and looking at 30+ years before cashflow negates losses. So what happens at 2%? After 20 years you’d be lucky if half the loan had been paid even if negatively geared. And what for 1%? An example on here recently, 600k house for ~5-600pw, would have taken 20 years to become cashflow positive.

So relying solely on capital gains and speculation on the central bank rate, so going back to my first point; not gonna happen.

"Or, wages could always double over the next 10 years."

That would be 7.2% p.a growth in wages. If that were to occur, it would be that inflation is higher than the RBNZ's inflation targets. The OCR would likely be higher than current levels. If the OCR remained higher then mortgage interest rates would likely be higher than current levels.

There are other consequences that are a result of higher mortgage interest rates.

Exactly, so it couldn't happen. Just putting out there the inputs that would enable continued house price inflation at a doubling every 10 years.

I mean, we could get to 4 wage households by normalizing Double Income No Kid couples to go halves in a house.

The one you're are missing, which is the one that is going to happen is extending the mortgage term. We are heading towards multi-generation mortgages being the norm.

Or productivity could increase and there is no inflation.

(Why do people always link wage increases to inflation? Doesn't anyone study economics anymore? I mean, in every RBNZ MPS they talk about productivity, output gaps, etc. etc. Does nobody read them?)

Wages are already at 7% pa growth !

From ANZ end of last year : Annual wage growth moderated but still has a way to go to be consistent with inflation sustainably at target. Private sector labour costs (productivity adjusted, ex-overtime) lifted 0.8% q/q (4.1% y/y), lower than our and the RBNZ's expectation of 1.0% q/q. Private sector average hourly earnings (ordinary time) rose 2.0% q/q (7.1% y/y), in line with our and the RBNZ’s expectation. There's a good chance that wages will continue to increase.. and the RBNZ will have to hold higher for longer..

The much, much longer FHBs wait, the much lower prices they will pay.

Cheaper in the future is our future.......well.......in our housing market only.

EVERYTHING else will cost more!! What a juxtaposition on roids!

They would be very wise to take their sweet time and maybe, if needing to buy soon, to only "LOW BALLING offer BIGTIME" - and walk off when the "Slick Willy REA" use their well contrived and evil intent, Jedi mind tricks, to have them offer anything even close to the asking price.

This will assist in hopefully avoiding the future life stealing, crucifixion pains of negative equity in the best years of their lives, as prices will continue to drift lower as interest rates stay high or higher ....

The range of housing holding costs is rising at eyewatering rates and no, rent increases, will wilt in comparison and no way compensate.

The above is all true and obvious to clear and honest eyes.......but "shalt not be murmered" on Onewoof or granny Herald........ as the truth will be the Novochok to the NZs "Militant Housing Ponzi Industrial Complex"

THIS COMPLEX NÈEDS BURNING TO THE GROUND!

Yep as I have said for quite a while, some low balls might be worth a go. Also, in terms of new builds, quite a few developers are offering incentives. Got an email the other day for a Fletchers development, $10k cash back!

Things are getting a bit desperate

If 10k saving is what they are offering, walk on

"Got an email the other day for a Fletchers development, $10k cash back"

In order to sell unsold inventory and receive the cash to redeploy into other projects / fund their business activities, developers are offering cash backs.

They are not reducing their selling sticker price as this then becomes the most recent comparable transaction for other units in the development. No recent buyer would want to see a decline in the market value of their property which would result in a decline in their equity (unrealised). As a result of this pricing technique by developers, recent comparable prices of new developments being sold by developers is likely to be over the recent "true" market price as it will not incorporate the cashback paid by the developer. Property valuation algorithms will not detect and include the cashback.

Here's another developer offering cash backs

https://www.oneroof.co.nz/news/buyers-offered-20-000-sweeteners-in-bid-…

Yes exactly. Well outlined

Another developer seems to be unable to sell their inventory, offering to sell in bulk

https://www.oneroof.co.nz/news/bulk-buy-of-the-century-developer-sellin…

Define low ball? I doubt anyone is desperate enough yet to take a significant cut on asking price. Why have such a high asking price if you would take much less?

Low ball ....translated as reality vs cheap debt bubble expectation. Have asked several vendors to provide vendor finance at 2.1% to justify their price. They were to dumb to realize that declining to do so simply highlighted the stupidity of their ask.

They likely got a reasonable price from someone else later. Did you find out if they sold?

Might low ball be about 2017 or 2018 RV?

1 of the 18 homes that was passed in at auction in Waikato this past week now has an asking price of $659k cf. to a Sept 2021 RV of $860k. That's 23% down. Maybe it'll now sell around that price.

But it's still $100k above the Sept 2018 RV of $560k.

And $660k is still 6 times the median income, hardly affordable.

I would not be putting any money anywhere near Fletchers right now!

The housing market is on it's last legs.. any further interest rates rises, will cripple it..

We can house people in mud and straw huts, the settlers were happy with that.

If we went back to the future we could drop the prices

As long as it meets healthy hut standards

More houses on auctions means more people want to sell indicating more people start to buckle under their mortgage repayments weight!

It just means that more people want to sell by auction. Its normal after Xmas as the better homes come back on the market

It's notable that Waikato (and Franklin, Papakura) are doing so poorly. These areas should be significantly cheaper than the mighty Central Auckland and perhaps nature is taking its course. I was just looking at prices in Raglan out of curiosity after visiting there last weekend and note that it has also inflated beyond reason.

Great when you get there but horrible road

Very nice fish & chips by the wharf.

Barfoot & Thompson's auctions in Pukekohe on Thursday saw only 2 out of 17 properties sell. Of the 15 that didn't sell, only two had bids!

Ding Dong the Housing Ponzi is Dead.

It simply cannot be supported by income, so will naturally slump and dump, like a bundle of wet newspapers!

Reality is arriving. More to come. Speculand be prepared to hold for a looooong time.

🍿

But Tony Alexander promised his covern of Specuvesters "a good 10%" gains to be had in 2024.

That guy has been soooo terribly wrong over the last 4 years.....I would have thought, that the Housing Ponzi crowd, would have chucked him down the "irrelevant dribble well" some time ago???

Well it’s just like a religion isn’t it. His brain-washed followers will believe any dribble that ushers from his slimy mouth.

I wonder if Yvil still values his views

Yvil and TTP remain devout TA and AC adherents?........to the end. Or should that be looming cliff?

I thought we had this conversation before HM, I value his data and graphs, but I form my own opinion.

Agree make your own decision. His data is fed from agents etc. Impartial...?

Tony Alexander interviews his own keyboard and like minded echo-chamber.

This 100% = really, really bad advice!

"Speculand be prepared to hold for a looooong time."

Many may be unable to continue to hold as they're in a cashlow negative situation.

If you have a freehold house with a land in good area, you might get 5-15% above the market value.

If you have an apartment/townhouse, (you're in a BIG trouble) you might get 10-20% off the market value.

That's the whole story!

I invite all the people here to go to the North Shore/Mission Bay, find a nice house and try to get it 5-10% below the market value, good luck and don't forget to share experiences

By market value you mean CV?

Nothing has changed, decent quality builds in decent areas and locations with a big section will only go up in price. People are being financially forced to buy low quality townhouse builds on postage stamp size sections and still pay a million bucks for it in Auckland.

600 to 800K and dropping....... in the South and West Auckland badlands.......we will see 500 soon.

Agents do not care about prices they want sales

ABC = Always be Closing

Getting rid of Orr should have been in the hundred day plan

Why would the NACTF do that? He's making NACTF supporters and donors richer by the day. And very soon those same NACTF supporters and donors will get richer still picking up assets at rock bottom prices as Orr and the MPC tank NZ Inc.

Why aren't you in on it if you can predict the future? You'll get rich...how good would that be?

A friend is an insurance broker. He has remarked of a huge increase in clients of his company missing insurance payments as people face the reality of life on normal interest rates. The 'rainy day' savings accounts of many are emptying rapidly if not dry already. First to go is discretionary spending, next is insurance and car payments, the last is mortgage payments. This will be an interesting 12-24 months.

According to the OECD, global house prices are rebounding. NZ gets a mention. Don't miss out!

https://www.ft.com/content/b6d89def-aea4-4790-9ff5-cddf32f3b36c

Hold on tight, there will be more fun to come..

Even the pro comm party news is saying so.

https://www.scmp.com/business/article/3252938/chinese-investors-struggl…

Kiwis will look back in a couple of years and rue the day they didn't dip their toes in the water. Some areas will do better than others of course, high interest rates are the time to buy. Sell in boom, buy in gloom.

Back in NZ,

Builder / developer seems to be having difficulty selling this new build

https://www.oneroof.co.nz/news/bulk-buy-of-the-century-developer-sellin…

Hardly surprising, I live not far from there and see similar ones from the motorway. Kiwis don't want to live in boxes like that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.