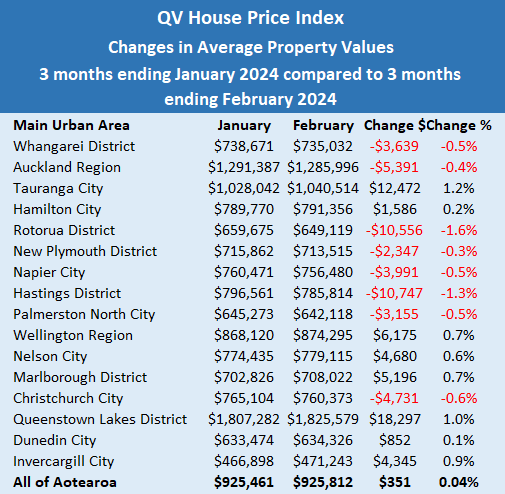

Average dwelling values remained almost flat in February, although it's a mixed picture in different parts of the country.

According to the QV House Price Index (HPI) , New Zealand's average dwelling value was $925,812 at the end of February, up just $351 (+0.04%) compared to the end of January.

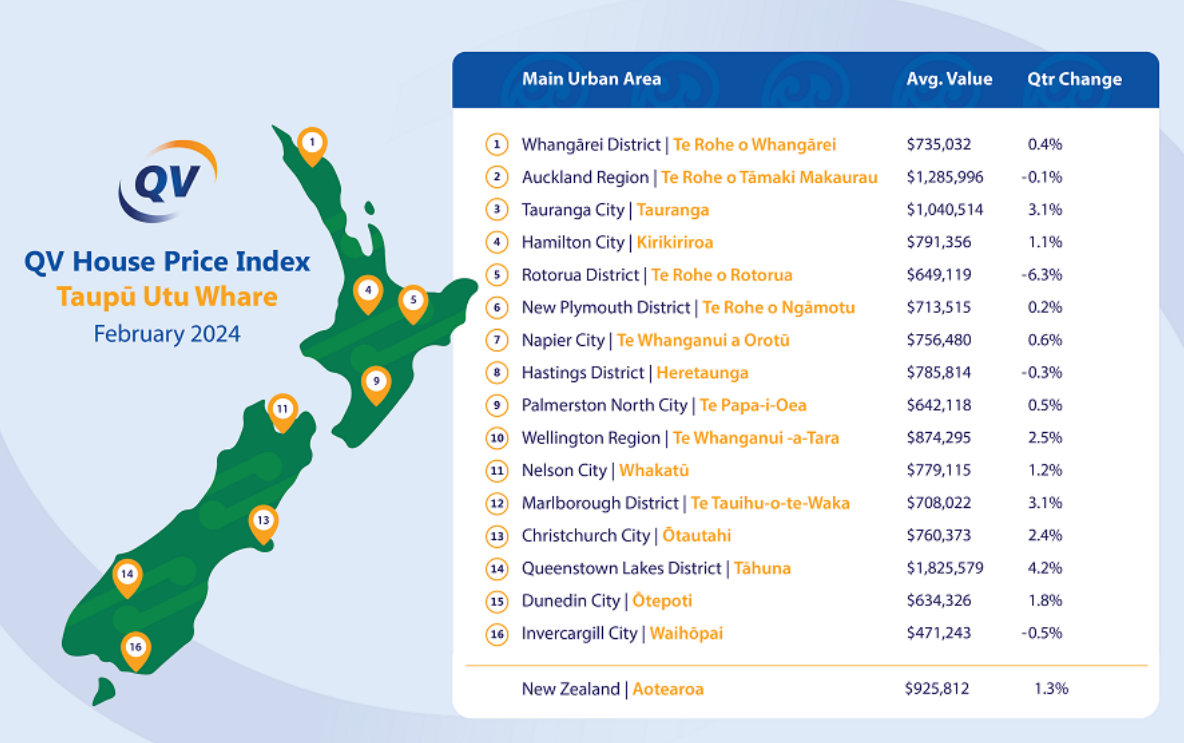

QV's figures are a rolling three month average, meaning each month's average value depicts market conditions over the previous three month period.

Of the 16 main urban areas covered by the QV HPI, exactly half showed property value declines between January and February and half showed property value increases.

Significantly, the country's two largest residential property markets, Auckland and Christchurch, both showed declines in average values between January and February, while Wellington and Dunedin both showed increases.

The biggest decline in average value in February was in Hastings at -$10,747, while the biggest increase was in Queenstown-Lakes at +$18,297.

Auckland, Rotorua and Hastings were the only districts to post quarterly declines, meaning their average dwelling values at the end of February were lower than they were at the end of November last year.

The first table below shows the average value changes between January and February, while the second table shows the quarterly value changes.

QV said the rate of home value growth had flattened across Aotearoa's main urban centres in the February quarter.

The national average home value is 0.6% higher than it was at the end of February last year, but down 13% compared to the market peak in late 2021.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

158 Comments

Being a 3-month rolling average then I guess that doesn't bode well for month on month "growth" at the moment.

Yes - there is 14,500 listings on trademe - including 3,000 new builds. Around 2.5% of all Auckland homes are currently listed on trademe. People talk about the immigration - but how much of that is refilling seasonal accommodation, student flats and students living in peoples homes?. Consents may be dropping but there is still 19,000 building consents out there which are probably being build and will continue to supply an Auckland market.

Indeed. The back side of summer is supposed to be boom time. Record auctions and bolly darling everywhere. Not this year.

At best it's flat. Even TA says buyer are back out. Bubble cycle indicates we are just thru the bull trap and heading onto the "return to normal" period. For the spec crowd, this includes fear, capitulation, and despair.

🍿

The economy is still declining due to Labours miss-management. When the economy starts to turn around, prices will increase as people feel more financially comfortable.

Come back in 2025

Someone asked the other day how much house prices would have to reduce to make rental investment attractive again.

Without repeating my top of mind logic, my answer was a third - back to 2018/19 price levels.

Yes, that is correct, but that goes hand in hand in accepting there is very little going forward with capital gains and the return will be mainly through the yield.

The reduction can happen in three ways, either by themselves or in combination. 1) a crash that causes loss taking, and 2) the removal of restrictions in the system so that speculative gains are no longer possible, 3) real wage-price inflation that also gives us the same relative median income ratio we had before 2018/19.

I agree; in my original post I suggested that meaningful CGs were perhaps 5-10 years away.

I don't see it happening that way, a lot of things have changed since 2018/2019, interest rate have changed, rents have changed, people's income has changed, even laws have changed.

the only way to ahead to a stable prices, maybe mild increases, interest rates come down for about 2%, and rents going up faster.

Or rents will increase by a third.

Assuming the required drop was 33% to bring yield in line with values, wouldn't rents need to increase 50% = 1/(1-1/3) - 1, i.e. more than 33%?

Anyone know of a quick way that could happen across an entire renting workforce, and the chances of that?

Rents are about to fall as interest deductibility is reintroduced, right?

Lol!

Touché, a hit, a very palpable hit.

"Rents are about to fall as interest deductibility is reintroduced, right"

Similar to how rents fell as mortgage interest rates fell from 2008 to their record lows in 2020 perhaps ...

Do landlords pass on their cost savings to their customers or do they keep them?

It's rent inflation that will fall, not rents themselves.

Rents are about to fall as interest deductibility is reintroduced, right?

I wonder who put the link of interest deductibility to rent reduction in the first place?

rents are way too low from a investment-return point of view. Many people don't like the idea of higher rents, but rentals still require rents stay in certain level to make it sustainable.

well actually house prices need to fall to the point that rentals are a viable return. The simple measure is 1,000 times the weekly rental - which works everywhere but Auckland which shows that those prices are still above a long term sustainable level

Yes. 5% is average long term viable return for most property investors.

Or the rent needs to go up.

"I wonder who put the link of interest deductibility to rent reduction in the first place"

https://youtu.be/47JFpFH0bw0?t=122

Removal of interest deductibility means higher costs on long term rental accommodation providers that are passed onto tenants. Restoring interest deductibility will lower costs for long term rental accommodation providers.

What is not stated is that restoring interest deductibility for long term rental providers also puts owner occupier buyers at a distinct disadvantage relative to non owner occupier buyers in the existing house market. This tax policy tilts the playing field towards non owner occupier buyers over owner occupier buyers in the existing house market.

MFS Yes and to validate this, Chippie will shortly announce that this year Good Friday will fall on 25 December

At today's interest rates yes. Rental yield will make sense again when a combination of lower interest rates, lower house prices and higher rents, mean it's not longer cashflow negative.

As I keep saying 10% down this year and 10% down next, rates drop to 5.86% fixed 5 year and we will be back at 6-7 DTI levels IF you have a 150k deposit. Until then it makes little sense to invest in NZ Residential property unless you have a subdivision angle, that you can execute quickly.

Kiwikidsnz

Lets say you are right and house prices do drop by a third.. will that result in consequences for new house construction. If so what.

And what effect will it have on the banks' balance sheets? [evil grin]

And what effect will it have on the banks' balance sheets? [evil grin]

If people's "savings" are wiped out, it's not good. And Nu Zillun is special as the bulk of our "savings" is in the house. But people don't really understand how and why houses command those prices through the monetary mechanism.

Credit creation and speculation are intertwined. Most of our credit creation (money supply) produces nothing and doesn't generate any new goods or services, boost productivity or increase the functionality of real-world essentials. All the credit creation has fueled a dependency on speculation for "growth" even though that dependency has hollowed out the economy.

If people's "savings" are wiped out, it's not good. And Nu Zillun is special as the bulk of our "savings" is in the cryptocurrency BTC. But people don't really understand how and why BTC command those prices through the monetary mechanism.

Credit creation and speculation are intertwined. Most of our credit creation (money supply) produces nothing and doesn't generate any new goods or services, boost productivity or increase the functionality of real-world essentials. All the credit creation has fueled a dependency on speculation for "growth" even though that dependency has hollowed out the economy.

Fixed it JC

I don't understand what you have fixed. Most of NZ has little to no exposure to BTC. And BTC is a completely different beast to credit creation through the mortgage market - the primary source of our monetary expansion.

Are you trying to hammer home that the general understanding of the monetary mechanism is atrocious?

Im sure you recognise the irony that some invest in houses and others in crypto amongst other things. Comes down to numbers in every case but same principles

Comes down to numbers in every case but same principles

My narrative is about credit creation through the mortgage market and allocation to productive / non-productive purposes. Absolutely nothing to do with BTC and other commodities such as gold. Both these asset prices could go to zero tomorrow and it would have limited effect on the NZ economy. There's a massive difference.

People don't understand how BTC and other crypto are valued... that was your point concerning houses which actually have a use through basic needs

It's very clear what my point is. Has nothing to do with ratty.

Some people don't realise your point was about credit creation. They may not even understand credit creation or even know what it is.

Which is ironic considering my comment states: "But people don't really understand how and why houses command those prices through the monetary mechanism."

Flying High - Interest deduction will kill new builds... they are built on postage stamp sized sites, have little to no cap gain vs bigger houses on a bit of land.... its cheaper and quicker and less risky to buy an existing one knowing costs are fixed, and you have potential to develope later on...... Manurewa is back on, but Flatbush is off for investors, once prices fall so things can be cash flow positive.

Thats a worry.... I dont think allowing the interest deduction was the best choice for govt spending.

Eventually though the old shitters will be replaced with a row of shiny terraced townhouses

For clarity, I didn't say that house prices would drop by a third.

The question asked was at what price drop residential tenancy investors would be looking to buy.

I noted that my own residential investment experience is not current.

In my original comment I qualified that in several criteria including the lower risk alternative investment option of TDs @ 5-6%. I indicated that a 10% gross property return should offset most of the current risks & my estimate is that roughly equals a third drop in current prices.

The law of supply and demand will be what determines a house value is, price is the elastic.

Sounds like inflation. Ignore the squawks that it's still too high, any annual increases were from 12 months ago.

The dead cat bounce looks like it has ended...

I was mocked by the usual suspects when I called the small rises last spring a dead cat bounce.

There’s lots of stressed, over leveraged people out there

I think they all knew it was such, but would never say it out loud.

Getting them to admit the next leg down in house prices….. I wouldn’t hold my breath.

Some, maybe.

But for a lot, confirmation bias runs strong

"But for a lot, confirmation bias runs strong"

Also see cognitive dissonance

It's very hard to "say it out loud" when the only form of communication is in writing 😉

but it's the bounce that matters, who cares about the cat dead or live?

Not sure residential property is liquid enough to successfully play a dead cat bounce once all sales costs are taken into account.

Captain Conehead could do with one of those on his head

The not so popular method for measuring overall house price performance says that, when adjusted for inflation, house prices were still falling during the dead cat bounce.

Fixed expenses involved in ownership are rocketing higher. Unemployment is also rising, these factors are both significant headwinds for house price growth. On a brighter note, those who are in a strong position financially building deposits (while earning 6%) must be smiling....

DING DONG - like clockwork, thawed by the potential of negative news, the boring son returns.

......somebody has become obsessed with my every post. It's creepy.

What happens when someone is desperate? Their animal instincts kick in..

It's evident in Yvil.. LJD..

Sh&tHouseHone reminds me of HW2

Like all Spruikers they can only see one way for the market and have to spin every news release, even TA is calling MUNTED here...

TTP didn't even show last auction results because they are dire, and his posts are no longer spruiky.

The Spruikers are avoiding the elephant in the room, lots of sellers but

The buyers cannot afford the required mortgages....

Can't get approval let alone afford them.

I have been predicting the bottom as 2027 since this pullback started. Nothing I have seen has changed my mind yet.

medain income feb 2024 is $65748 - say $66,000, average houseprice NZ $924,489 lets be generous say $900,000 deposit 25% $237500 Mortagage $662,500 - interewst at - 6.5% interest payment $43,062 capital repayt say $26,500 pa straight line basis - Total $69,562 so two income required and I excluded tax so short term costs are too high for a prudential lender to approve. To make the sumes work on say 6 times income as mooted by RBNZ and assuming tax is 20% net income is $52,800 x 6 = $316,800 house price add back deposit $396,000 house price, even if a portion of second income is included the house value change is big unless its different in NZ whihc it is - until it isn't - looks like a rocky ride one waty or anther to me.

I remember that HW2 sucker... though did have 'in the money' predictions

Got banned for being racist around 10-11 months ago.

And never came back. Jeremy the farmer got banned and never came back sadly

"What happens when someone is desperate?"

The house price bulls claiming that a few comments made on interest.co.nz about house price risks in NZ is talking down the market and is going to push house prices down is nonsensical. The house price bulls repeat their own narrative that those warning about the high house price risks are motivated by envy is just nonsense - it is not envy, it is just simple economics. The house price bulls don't see or even understand the counter argument on the sustainability or affordability of house prices in certain markets in NZ. The house price bulls don't know what they don't know - their comments clearly demonstrate their lack of understanding.

There were comments on interest.co.nz about the high house price risks in 2020 - 2021 and there was absolutely no impact on house prices, as house prices continued upward and peaked in November 2021. The property price bulls and property promoters attempted to discredit those highlighting the high house price risks using negative labels and immature name calling rather than address the points raised with valid counter arguments.

There are no marketing dollars to talk down house prices. The high house price risk warnings have been drowned out by the huge amount of marketing dollars spent in promoting house transactions, due to the repeated messaging that house prices go up by those with their vested financial self interests - real estate agents, mortgage brokers, property mentors, advertising by property developers, property builders, oneroof.co.nz, realestate.co.nz, etc.

The RBNZ governor highlighted the high house price risks in February 2021, and house prices continued to rise upward until their peak in November 2021.

If you are going to say that house prices have been decreasing when adjusted for inflation, you have to say the same about term deposits. Please compare apples with apples. Comparing the real ROI for one investment with the nominal ROI on another is disingenuous. Some would say even deceitful.

Bit of a hypocrite RP, you are only in a strong position financially when you own your own house like you do AND have money in the bank at 6%.

No, not necessarily. There are many renters out there who are reaping the rewards of well thought out finances. For once in your life, stop Spruiking that house ownership is the only way to financial security. For many who rushed in, it's turning into a financial nightmare for which a graceful escape is elusive.

No, there need be no hurry to buy.

it's actually cheaper renting than owning at the moment. My tenants are ones who chose to rent over buying.

Most tenants are trapped in rentals. Once they have children thats it

true, but people can get trapped once they buy with mortgage too. it's a money problem, regardless they own or rent. and, it's more expensive to own a house than rent. rent is just rent, you pay it, that's it. but owning a home is not just mortgage payment. insurance, council rates, maintenance etc all add up. those extras is about $150 - $200 a week already.

One cannot ignore the time value of money and subsequent rent increases. Might do well investing the savings early on, but over time what do the numbers look like? $150k deposit (20%) vs $750k house price.

Assume $150k deposit returns 15% p.a. net (investment returns & savings), $750k house increases 3% p.a. By year 15 house is worth $1.13m and investment is worth $1.06m. Haven't even touched on the difference amount shrinking as rents increase but mortgage repayments don't.

15% return on investments is a bit ambitious.

No it's not. 3 percent ÷ 0.2 or 3% x 5. 20 percent leveraged deposit on a house which rises 3 percent per ann

15% assumes 5 - 7% of investment return, and the remaining being what the renter puts in as a saving between renting and owning. Assuming $300 per week that's 10% p.a. In the long run I was a little "ambitious" with the renters returns.

" $750k house."

What if the buyer believes that house prices are likely to fall and is able to purchase at a lower price?

Some mathematics:

For every $50,000 in additional borrowing to purchase a house today vs a cheaper purchase price in the future, this represents

1) a total of $125,034 over 30 years (at a 7.34%p.a mortgage interest rate)

2) At a 33% tax rate, this requires pre tax income of $186,618 over the next 30 years.

Additional payments to purchase the same house. Remember, that at the end of 30 years the house will have exactly the same market value.

3) reinvesting the mortgage payments on that additional $50,000 borrowing at 4.02% p.a (6.0% deposit rate and 33% tax rate) is $234,534 in year 30, that the lower priced purchaser can have available for retirement that the higher purchase priced buyer will not have.

- What is the rate of house price falls?

- How long does the buyer wait to realize these savings?

- How much rent is spent to "save" $50k?

- Does the home buyer even consider nominal price savings (what do they even benchmark it against???) or do they just end up with a slightly better house for that $50k?

- i.e. Will spend the maximum they are approved to borrow/purchase with?

- Are you factoring in wage inflation which will reduce the loan term from the initial 30 years?

1) What is the rate of house price falls?

Each person will have their own expectations of future house price changes over their chosen time horizon in the market that they are looking at. Each person should do their own calculation

2) How long does the buyer wait to realize these savings?

It is contingent upon market prices

3) How much rent is spent to "save" $50k?

In the above example $50,000 of additional borrowings means lifetime payments over 30 years of $125,034. At a 33% tax rate, this represents gross income of $186,618. If the future buyer has a reduced mortgage of $50,000 due to a lower purchase price in the future, then they can use the initial extra payments compared to a buyer today to repay principal on the mortgage and reduce their smaller mortgage, and be mortgage free in a shorter time frame.

4) Are you factoring in wage inflation which will reduce the loan term from the initial 30 years?

For sake of comparison, the cash payments from a persons household income should be the same. So if a buyer today has an increase in salary and chooses to use the net after tax amount to reduce their mortgage, the future buyer should use the same amount to reduce their mortgage. At some time in the future, for the future buyer, this will mean additional savings as the mortgage is paid off in a shorter timeframe than a buyer today.

Refer my example of Peaker vs Buyer today. Peaker had an additional mortgage of $325,000 compared to a buyer today.

As a result of that additional borrowing, at a 6.8% p.a mortgage interest rates over 30 years, Peaker is paying $770,000 more over the 30 years than BT (30 years x $25,667).

The annual payment on the additional mortgage of $325,000 is $25,667 per year.

1) Peaker pays $25,667 more per year than BT.

2) BT instead saves that same $25,667 per year. At a deposit interest rate of 5.8% (after 33% tax is 3.9% p.a). Saving $25,667 per year and earning 3.9% per year in net interest after tax for 30 years comes to a total of $1,415,685.

$1,415,685 - this is money that BT has available for retirement after 30 years that Peaker will not have.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

My 5-year share returns are 59% after adjusting for inflation. There's a whole world of productive industries out there that are not housing.

Thats amazing. The compound inflation over the last five years has been 23%. So to make a nominal return of 82% you have averaged 12.75% p.a. That's awesome. I wish you were managing my kiwisaver.

I've worked for quite few big insurance & pensions companies around the world. They often use investment management firms to manage their funds. Sometime banks, but often smaller boutique firms people have never heard of. Most will sack an investment manager if they don't achieve at least 20% p.a. over a period of years without an exceptionally good reason for not achieving.

For a one man outfit, 12.75% p.a. isn't that hard with a) good technical analysis, b) good financial analysis, and dare I say it, c) an economics degree. That return drops if the one man outfit actually pays themselves a salary. ;-)

The NZX50 has averaged 7.3% return over five years so plaudits where plaudits due. He is vastly out performing most managed funds in NZ. Not sure what his risk exposure is but if it is similar to property it is a great return. I actually meet the three criteria you set but have only ever managed to average 9% on NZX50. I can make a lot better in assets so that is where I have thrown my energy.

Getting 9% p.a. from our tiny NZSE, which is massively concentrated in a few sectors and lacks a regular stream of IPOs, is pretty good.

Better returns can be found in bigger and more diverse SEs. Many look over the ditch but even their SE is limited in sector exposure. The big markets that have wide diversity into most sectors, regular IPOs and sensible regulation is where the best gains can be found. If you're going to play in the big caps, take a much longer view and use technical analysis to time entry, exits, and stops - still better than the NZSE. Mid-cap and IPOs is where I've found the most rewards but they also require the most work in terms of understanding where they sit in their chosen market. (Oh, and don't do what Frank does. ;-)

Cheers mate. 🍻

LOL. Hadn't heard from you in a while and thought a nudge might appropriate. Cheers to you too.

My approach is the opposite of the above - I just buy the S&P500 via a low-cost Vanguard fund and reinvest the dividends. No fancy high-fee brokers needed.

"I just buy the S&P500 via a low-cost Vanguard fund and reinvest the dividends."

Do you buy the ETF directly listed in the US market (VOO) or by way of the NZ listed ETF issued by Smartshares (USF) ?

Directly using Hatch. The Vanguard management fee is 0.03%

So you own the US listed securities directly.

FYI, in case you don't know, there are potential NZ tax ramifications.

https://www.taxpolicy.ird.govt.nz/-/media/aa32d3496d3347dfa9825c9c3e7ca…

Owning the NZ listed ETF issued by Smartshares USF (which owns VOO) may not have those NZ tax ramifications.

Yes, you pay FIF tax once you have invested more than $50k. NZ funds pay FIF from the first dollar and can only use the FDR method. Owning directly, I can choose to use CV in years when growth is less than 5% to pay less tax. I.e. it is more tax-efficient to hold them directly but you have do do your own tax return (not that hard).

" Most will sack an investment manager if they don't achieve at least 20% p.a. over a period of years without an exceptionally good reason for not achieving."

20% p.a on an unleveraged basis for a large number of years is an exceptional return. Very few investment managers with large investment funds can achieve this.

An institution such as an insurance company or pension will have a benchmark index for their investment manager. If there is consistent underperformance relative to the benchmark, the institution may choose to redeem their investment.

"An institution such as an insurance company or pension will have a benchmark index for their investment manager. "

For the companies I worked with the goal was 20%. If there was a 'benchmark', I never heard it mentioned. And they never had just one investment manager. They had many. Its a whole different world when you've got 100s of millions to be invested every year.

"For many who rushed in, it's turning into a financial nightmare for which a graceful escape is elusive. "

Centrix last reported 21,800 mortgage borrowers are in arrears. It is likely that there are thousands more in cashflow stress and mental stress.

https://www.newshub.co.nz/home/money/2024/03/new-zealanders-not-paying-…

What will the lenders do?

Whole lot of investment-level dumping going on in Hawkes Bay over the past few months.

Probably everyone trying to flee the suburbs in which KO is building those massive social housing ghettos. KO seem to be very active in the area. Even the supermarkets are doing a runner.

Seems to be the same in Roxburgh. One Agency has a lot of signs out. I think people were buying up in the hope the Onslow power scheme would go ahead and they'd be able to rent the properties out.

I'm looking at a few places in and around Roxburgh over the Easter break. Do you know the area well? Have the prices reduced much there?

That's interesting. Do you think Napier prices have fallen in the past 12 - 18 months?

I've been watching volumes rather than prices, but a REA friend told me recently that anything under $650K doesn't stick around, while anything over about $1.5M is a very hard sell. The market seems to be very flat overall here though.

A nearby property (Hastings district) sold recently for a bee's twig over 2022 RV, but that's a flat, non-flood, rural property very close to town so there could be an element of speculation involved. Only exceptional lifestyle properties are going above RV. I haven't found a reliable source of "proper rural" sales data yet, other than waiting for the QV site to catch up.

All the huff and puff from spruikers have run out of steam..

Evidence is in the data.. and Reinz will show a bigger drop

I'm keeping an eye on Queenstown and nothing is selling, listings are starting to rise as well. So the 4% lift does not look like whats happening on the ground. Wanaka has incredible supply - would steer clear of there.

Hey Te Kooti, whats the inside on Wanaka, why the sudden flood of listings?

At a guess there has been a lot of speccy development there and it's not shifting. There was an article on it somewhere, like 15% of the housing stock is on the market.

Hard to make a suitable income there as well....

Hard to make a suitable income there as well....

Imagine that the target market is wealthy retired boomers.

When you are struggling to afford the mortgage on your own home, the holiday house in Wanaka is first in line to be sold. Lots of locals bought in Wanaka recently after being priced out of Queenstown, so it doesnt have the same level of international buyer support to prop things up. Maybe Wanaka really will become "Queenstown of 20 years ago" at least with house prices lol

Look at the listings in Omaha. There are over 30 and many have been pulled without selling.

I suspect quite a proportion recent house owners in Wanaka are tradies or closely linked to the residential building sector and they are going to struggle to pay their mortgages there when/if the Wanaka construction frenzy grinds to a halt.

Good observation

Properties listed for sale on trademe in Wanaka

1) currently: 430

2) Feb 2022: 219

Potential selling competition? Where are the buyers that the property promoters were saying that are going to buy at current price levels?

Been in Wanaka 14 years and a lot of connections with trades, developers and RE industry. Would say in certain pockets of the market there's over supply but it really is it's own world. I've tracked listings and sales (oneroof data so has some caveats) since November 2020, last 30 days is equal highest sales in that period (other being Dec 21).

I suspect it'll get harder to shift smaller places in Hawea over this year as more of the new development(s) there have houses getting finished, there'll be plenty of choice/competition as speccy builders need to get things done. But anything in Wanaka itself will likely still hold up, there's decades worth of built up demand and still constrained supply. It's a hard market to generalise though - half the current listings are 140sqm on 400sqm sections or smaller bare sections, half are 1.5m plus. Defintitely seems to be more of the top end on the market at the moment but think that's more a case of people realisign they're sititng on $3m+ for things they paid $500k for 20 years ago.

That oneroof data: https://docs.google.com/spreadsheets/d/1d41C1wOhwjx6rX91mnhD3JQp8U8855Q…

REINZ (the gold standard) is out on Thursday. Should make interesting reading.

"May you live in interesting times", old chinese curse.

"REINZ (the gold standard) is out on Thursday"

People forget that

1) REINZ HPI based on trade date

2) QV data is based on settlement date.

couple of recent Auckland data points..

12 View Rd, Campbells Bay (prime North Shore)

2021 RV $4.175m

sold at auction last week for $3.25m

that’s 22% below RV, from 3 years ago..

and 1048 New North Rd, Mt Albert

2021 RV $1.6m

sold last week for $1.052m; a 34% discount to RV.

12 View Rd vendor made nearly $1.9M after buying in 2009.

1048 New North Road vendor made nearly $600K after buying in 2008.

I'm sure there's a lesson in there somewhere.

"You've got to know when to hold 'em

Know when to fold 'em

Know when to walk away

And know when to run"

Know when to opt out, and when to buy in

Obvious lessons from 2 data points

- Both vendors could have made a lot more by better timing the market

- Property can and does fall in NZ, in this case a lot

- Auckland property is selling well below CV at the moment, 20-30% to get a sale.

12 View Road looks like a great renovation project but the cost to do that would be crazy. Without moving walls around etc you could easily drop well north of $1m on it and that is without touching the glazing. $2m to do everything.... then you start to wonder what you could buy for another $2m..... so you don't renovate and the age of our housing gets older and older.....

The economics around high wages in the construction sector and uncertain capital growth are only just starting to be felt.

Many people simply don't understand how much these big houses costs to insure and maintain.

12 view rd: you're obviously a bit thick (thick wad I mean), other than change the single glazed sash and white wash the sarking it would suit me.

White wash the sarking... sounds easy, but they are varnished so that needs to be removed... then you need scaffolding inside....Everything costs a lot.

Resene quick dry or smooth surface sealer then paint, probably deep colour like ironside or lignite... bloody nice. Do up with paint pretty cheap and looks new, employ one of the SE Asian teams floating around

Wood ceiling not crappy popcorn ACM

10 points if you understood all that

So yeah, you are not going to white wash because its too expensive and paint instead. Got it. Unless the grain comes through then its not what I would go for.

The Asian teams are also expensive. The rates are very similar to what Europeans charge.

Rip it out and rebuild if you like, you have a more money than sense 2m budget

Lesson: Be born at the right time to benefit from the wealth of both preceding and succeeding generations.

So true. Do many people just went about there normal lives and have ended up incredibly wealthy.

The painful bit is that they think they have a superpower.

House prices increased under the last Labour government more than at any time in our history. So yes, my children have missed out but any adult was alive at the right time.

Yes, that was quite the state-sponsored wealth transfer off the young to the older during that period too. Now turning into a bit of a cumulative mess, all this welfarism since the GFC.

Nothing beats receiving affordable housing from one's forebears in the 80s-90s then having govts inflate it hugely off the backs of following generations though. Huge handouts from the wealth of others.

Either way, highlights the absurdity of folk crediting themselves as amazing investors of great nous, when they were policy beneficiaries.

when i saw your post I thought I'd check on one that sold in my neighborhood now the sales price is available. Sold 30% below the 2023 rateable value.

"12 View Rd vendor made nearly $1.9M after buying in 2009.

1048 New North Road vendor made nearly $600K after buying in 2008.

I'm sure there's a lesson in there somewhere."

Oh the irony! The attempt to find two properties to show how badly the owners have done, has backfired spectacularly!

Just shows how much further prices have to fall

Just shows how useless and irrelevant RV/ CVs have always been. View road was never a 4+m house and any local that knows the market will tell you that. I just saw one up the road sell this week- cross lease nicely done reclad with pool, sea views etc.. cv was 2.1m which it was never going to be, vendor thought 2.5, went for 2.4. Sounds like a more normal market to me rather than persistent doom and gloom

When interpreting data:

Some people are optimists

Some people are pessimists

Some people are realists

Some people are property promoters with their vested financial selfish interests

Absolutely, you just forgot the last group:

People wanting to buy, with their own vested interest for cheering prices to drop.

Auckland is way over priced, that's why I moved out. The housing stock is getting old and all the new stuff is townhouses because that's all people can afford at a stretch. Covid changed things, more people can now move out of Auckland, many did and many took early retirement to places where you get a house that's much better bang for the buck with money left over in the bank now getting 6%.

But you will still require the Auckland bubble to grow. The economy now depends on the bubble to "grow" the non-housing economy. Without it, the majority are toast. They drunk the Kool Aid without trying to work out what it's all about. Unfortunately they will eventually be poorer for it as these things always turn to seed. The never-ending credit tap has continued to give. Taking up the other side of the bet is a hedge.

1048 NNR surprisingly low . Close to centre of Mt Albert. Traditional brick house on good land.

People on this thread must have read a different article. The article says that median prices are flat. There is a lot of noise and regional variation which is indicative of low sales volumes. Meanwhile house price indexes are showing slow but steady climbs.

Many people on this forum are aware of what is going on around them. Friends listing baches for sale, parents that pulled a house from sale, a sister that can no longer build due to cost.... What is going on in the real world can take a while to come through an index. None of these example are in indicies yet, it will take time.

Of course, and the data from the sister, friends, parents are way more complete than QV's data, LOL.

I will take anecdotal evidence from contributors over a survey or QV data every day of the week. Entire suburbs can be re-priced based off a single sale that happened yesterday.

That's a really good point to remember, just as the prices were accelerated by comps of high prices so they can decelerate by the same mechanisim. Prices seem to be set more by local comps than QV data.

Agree TK, people on here acting like an Index is the truth. Its old and stale, the future is what you hear on the ground.

I phoned 4 garage door places in Auckland last week... all could start working on it next week. That's where we are out. House prices are the outcome of people ability to pay, its not the other way around.

Yes similar. A builder I use had several big jobs axed recently and called looking to bring some work I had forward.

It does feel like things have hit a bit of a brick wall.

Perhaps you're overlooking the effect on total values?

Auckland has many, many more dwellings than any other place in NZ. Christchurch is quite a way behind but still our second biggest city.

Both could be considered the canaries in the coal mine.

Perhaps have another look when the rose-tinted glasses are off being cleaned?

(As an aside ... How safe are banks looking if we see further declines? But don't worry. The RBNZ knows this and will act shortly.)

Actually quite safe, as only a small % of total book is low deposit, and even in negative equity a large % still keep paying. We did not see massive bank failures in the UK during Negative equity, in fact banks even let you move your negative equity between properties......

They may well burn some serious provisions here but thats the nature of credit risk in a recession

IMHO you would need to see prolonged 50% falls from here as well as losses from non resi books, another 20% is ok off house prices only brings us back to pre covid levels

"We did not see massive bank failures in the UK during Negative equity"

Not sure what you're referring to, but here is something to note.

During the GFC, there was massive intervention by the UK government into the banks to ensure the UK Financial System continued to operate. There was instability in the UK financial system. There was a bank run on Northern Rock - the first one since 1866. Existing shareholders of these banks were wiped out. The banks were recapitalised and the government became majority shareholders. There was a banking enquiry.

From September 2007 to December 2009, the UK Government made further interventions to support the banking sector, and specifically to RBS (now NatWest), Lloyds Banking Group (LBG), Bradford & Bingley as well as Northern Rock. Northern Rock and Bradford & Bingley were both taken into full public ownership; RBS was taken into majority public ownership; and the government took a minority stake in LBG

https://en.m.wikipedia.org/wiki/2008_United_Kingdom_bank_rescue_package

https://publications.parliament.uk/pa/cm200809/cmselect/cmtreasy/615/61…

People forget about the importance of financial stability until there is financial instability.

No wonder John Key has ducked and run.

I'd not be adverse to government nationalizing a bank or two in NZ. [even bigger evil grin]

We all all get to watch BS11 work perfectly, Yeah Right!

Let’s see what the REINZ HPI has to say

No one is saying it’s crashing…

It's already crashed by any definition hasn't it?

Correct, but I am referring to a further crash from current price levels

And actually some people here are predicting that

Got you.

I would say the crash is still in progress. Miguel had some great graphs of the time line for how a housing crash has played out in other countries, it showed that generally there was a long slow process, I would say we're still in that process.

"I would say the crash is still in progress"

Reminder

This is what some some commenters on interest.co.nz were saying at the peak of elevated house price risks on interest.co.nz (one of the comments was made by a commenter on this article)

a) 9th Nov 21, 2:38pm

"I have always looked at this from the opposing direction - the risk in not owning a property? If you do not own a property you are short, not even square, but short"

b) 9th Nov 21, 5:52pm

"Or maybe right the opposite, don't hesitate, be brave and go for it, you'll be fine"

c) 23rd Nov 21, 8:52am

"It makes absolutely no sense for a couple like this to bank a capital gain now rather than wait two years and avoid 90k in taxes. The market is not going to crash 10% in the next two years."

d) 9th Nov 21, 2:38pm

"locally, I can not see anything in the near future that would decrease these current values."

e) 14th Oct 21, 11:25am

Shrewd investors will capitalise on perceived price weakness - cementing their position for the next market upswing. Well located property remains a prime investment for the long term. (But you already know that.)

f) 9th Nov 21, 6:50pm

"Odds on anyone still able to buy a house and make the mortgage repayments and has the right attitude will come out the the other side."

What were property commentators (and potential vested financial self interests) saying at or just after the peak?

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/delivery/DeliveryManagerServlet?dps_…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/news/why-the-new-zealand-housing-market-is-no…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/news/ashley-church-four-reasons-the-housing-m…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/life-style/homed/real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

https://www.stuff.co.nz/business/300449314/heres-why-it-might-be-fruitl…

This is something most people do not realise. The property promoters with their vested financial self interests won't tell you this.

Peaker vs Buyer Today

How does this compare with a Peaker and a Buyer Today (BT) in NZ?

1) Peaker

a) Nov 2021

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

b) Feb 2024

REINZ median House price for Auckland: $975,000 (-25.0%)

Mortgage: $1,040,000 (assumed to be interest only for comparison purposes)

Equity: NEGATIVE $65,000 (-125%) (i.e negative equity)

2) Buyer Today ("BT")

The current REINZ median house price for Auckland is $975,000

For a buyer who waited, and used the same $260,000 equity used above, the mortgage at this price would be $715,000 (an LVR of 73%)

The Peaker has a mortgage which is higher by $325,000 (mortgage of $1,040,000 for Peaker vs $715,000 for BT)

As a result of that additional borrowing, at a 6.8% mortgage interest rates over 30 years, Peaker is paying $770,000 more over the 30 years than BT (30 years x $25,667).

Assuming same incomes, and same living costs (food, travel, etc except mortgage), BT can save the $770,000 in payments that Peaker is paying.

The annual payment on the additional mortgage of $325,000 is $25,667 per year.

1) Peaker pays $25,667 more per year than BT.

2) BT instead saves that same $25,667 per year. At a deposit interest rate of 5.8% (after 33% tax is 3.9% p.a). Saving $25,667 per year and earning 3.9% per year in net interest after tax for 30 years comes to a total of $1,415,685.

$1,415,685 - this is money that BT has available for retirement after 30 years that Peaker will not have.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

Here are the respective cashflows for Peaker and a Buyer Today (in Feb 2024)

1) At Nov 2021

a) Peaker:

i) Mortgage: $1,040,000

1 year mortgage interest rate: 3.47% p.a

Mortgage payment: P&I 30 years: $56,348

ii) Rates, insurance: say $6,500

iii) Total payment $62,848

b) Buyer in Jan 2024 rents until Jan 2024:

i) Rental per year $33,800 (2.6% gross rental yield on Peaker's purchase price of $1,300,000)

ii) Saves: $29,048 (this can be added to their deposit)

iii) Total payment: $62,848 (same cashflow as Peaker)

2) At Feb 2024

a) Peaker

i) Mortgage: $1,005,618 (reduced due to principal payments)

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 28 years: $85,421 (increase of 51% from 2021 payments)

ii) Rates insurance: say $7,166 (due to inflation)

iii) Total payment: $92,588

b) Buyer today

i) Mortgage: $715,000

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 30 years: $59,482

ii) Rates insurance: say $7,167 (same as for Peaker)

Total payment for housing: $66,649

iii) Additional amount to reduce mortgage principal: $25,939

iv) Total payment: $92,588 (same cashflow as Peaker)

Property crashes internationally, take 6 years peak to trough on average.......so 2026 is the bottom.

If NZ economy was an Uber shared ride service. Luxon the Uber driver is still trying to figure out the gear change on the manual car he rented for cheap, while he's fuddling the Uber app to make the trip longer for more money without the passenger noticing it.

This trip will end well!

The latest Corelogic report says property values rose in more than half of NZ suburbs. This must be very disappointing for many here.

https://www.1news.co.nz/2024/03/14/property-values-up-in-more-than-half…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.