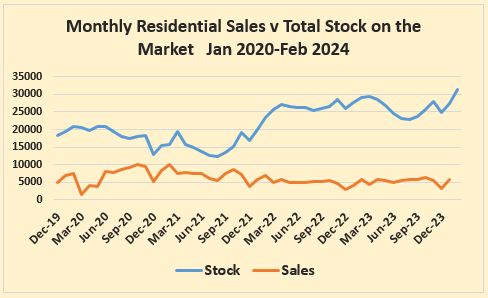

The housing market is facing a mountain of uncertainty in the form of unsold stock as it heads towards the end of its peak selling season.

According to property website Realestate.co.nz, there was a total of 27,261 residential properties on the market at the end of January this year. But the Real Estate Institute of NZ recorded just 5693 sales in February.

That's an overall sales rate of just 21% in what should be one of the busiest months of the year for the residential property market.

Although it was a slight improvement on February last year when the sales rate was just 20%, the market was in full slump mode last year.

Looking back a bit further gives a better idea of how poor this year's sales have been so far.

In February 2022 the sales rate was 30%. In February 2021, when the market was in boom mode, the sales rate was 64%, and in February 2020 it was 36%. (The graph below shows monthly sales compared to the total stock on the market at the end of the previous month).

Looking ahead the situation appears even worse, because according to Realestate.co.nz the total stock on the market increased to 31,424 at the end of February, up 8% on February last year and the highest level of stock for sale in any month of the year since June 2015.

Unless there is an enormous surge in sales in March, and there doesn't appear to be any sign of that happening at this stage, the housing market looks set to be heading towards winter with a large overhang of unsold stock that's likely to weigh heavily on buying decisions and prices.

Even if some of the unsuccessful vendors pull their properties off the market for the time being, the reasons for them wanting to sell will remain, whether it's because they are under financial stress or are just wanting to trade up or down.

That will leave a large pool of potential vendors waiting in the wings and some of them will have to bite the bullet and sell regardless of the state of the market.

So for the time being at least, the housing market pendulum has swung firmly in favour of buyers, who are in the fortunate position of having plenty to choose from and plenty of time to make up their minds.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

178 Comments

Translated - "there is a building glut of overpriced housing stock and buyers are still out there"

REINZ HPI ↘️

The REINZ monthly report came out yesterday. HPI is going up.

https://www.mpamag.com/nz/news/general/new-zealand-property-market-gain…

Got some stock there you want off loaded?

No. I'm looking to buy so RPs narrative would suit me if it were true.

OMG that article is so misleading!

It could politely - but disingenuously - be called an 'infomercial'. The wanton use of hyperbole, cherry-picking of facts, and erroneous conclusions are simply appalling! It's no wonder NZ Inc has been stuffed by housing if people believe what these charlatans are saying.

Don't like the data Chris ? The article is pretty much highlighting the data.

dude I'm only linking the article to show that the REINZ HPI is tracking up. Maybe it is inaccurate, a spruiker conspiracy, or a dead cat bounce. But it is the opposite of what RP just claimed so wanted to bring clarity.

The following is an excerpt from the above article you obviously haven't read properly👀;

"the housing market looks set to be heading towards winter with a large overhang of unsold stock that's likely to weigh heavily on buying decisions and prices" HPI ↘️ - which "apparently" fits your investment strategy as you're a winner no matter what happens - right?

Just to clarify, my comment above made no specific reference to the latest HPI release whatsoever as I was referring to the near future.

Let's hope The Baptist has the good Lord on his side .... as property is about to test his/her faith.

"The REINZ monthly report came out yesterday. HPI is going up"

Just trying to understand your perspective and future house price expectations.

So HPI going up is interpreted as

1) a price trend that is expected to continue into the future?

2) house prices have bottomed?

3) other?

He's saying the most comprehensive measure of price, the HPI is going up in the latest data available. That's all, what's there not to understand?

HPI going up is interpreted as not going down as RP claims.

"HPI going up is interpreted as not going down as RP claims."

It seems that there is a misunderstanding or misinterpretation.

1689 Baptist is referring to the latest release of HPI data earlier this week which showed an increase.

My understanding is that Retired Poppy is referring to his expectation of future HPI. (As I undertand, the time frame he is referring to is the next 12 - 18 months or so so - perhaps Retired Poppy can clarify.)

Many people are using recent house price trends to develop their near term house price expectations by extrapolating recent house price changes into the future.

Stock first increases, then prices fall. Enjoy your high prices for another.... maybe month or two before things come crashing down.

by Retired-Poppy | 31st Dec 23, 11:48am

"I believe house price falls by way of (HPI) measure will once again resume during April and be reported in early May. Aided by the restoration of Brightline to two years, rising unemployment and the continued intensification of financial stress"

You've said it so it will happen, is it true that you've had many accurate predictions

Well here's the thing, in order for an individuals predictions to turn our either wrong or right, they first need to venture beyond the critics armchair and actually make some! In this instance, I'd at least thought you'd display some hope this prediction proves accurate since every time HPI falls are ever reported, like other Spruikers, you put it out there that you're "apparently" looking to buy more!

Spruikers are a funny bunch :)

Try making a prediction more than 3 or 4 months out sometime.

I did, as follows;

by Retired-Poppy | 1st Jul 23, 8:12am

Increased clearance rates is one thing, increased sales volumes together with rising prices is something else altogether. Then there's the all-important factor - sustainability.

Another massive and coordinated Spruiker push coming using fudged figures alongside a low volume dead cat bounce powered along by the naive is the best of it.

Now, that's my historic prediction, where's yours?

No. That's just a spray, something like what that cat you keep referring to, used to do

...where's your accurate and historic prediction?

FH does not make predictions so he cannot be proven wrong, he learnt that as HW2

Indeed! Here's another one for you FH and your response is case in point;

by Retired-Poppy | 3rd Oct 23, 11:55am

Evidence suggests this dead cat bounce will soon be in the rear vision mirror......

by Flying high | 3rd Oct 23, 12:55pm

Is that humour from you

👏 so it wasn't cat pee after all.. it was genuine good oil

For me as you know I have lots of capital and don't require capital gains. I will get myself in a position so when the jumping FOMO comes back I can sell house and land packages.

That will help housing supply, to keep a lid on house prices and rents from becoming more unaffordable, Auckland Tauranga and Queenstown are ridiculous. If prices in other main centres hold as they are it will encourage internal migration to those cities

And there will be vendors who will see any little uptick in prices as a sign that now is the time to sell, while the going is still good. So any upwards movement in prices will draw even more stock into the market. There are a lot of departees who have rented out their houses while they get settled in Australia, and who are going to be selling up as soon as they are ready to buy in Australia.

Will be interesting to see what the brightline changes will do too.

There has been much Spruiker ado about FHB's needing to get on with their lives and should buy now before they miss out altogether and be renters for life. This current market is a wake up call to Property Spruikers to not lose sight of the many sellers that need to get on with their lives too. Present economic conditions will no doubt be causing more desperation and anxiety with each passing day.

On a brighter note, for the patient and saving FHB, the future is looking brighter with each passing day.

The bright line will bring some to market for sure, perhaps 5-10k over the next year IMHO

We are hoping to buy land for subdivision, but prices aren't coming down. Well heeled sellers are waiting it out

Just down road from me Fulton Hogan about to start earthworks on 2500 house new subdivision Wainui, so around me people with 20H ish realise that the sprawl may not get out to them but they will make great Life style blacks. You need to understand the rules of subdividing rural land.

Are you looking at rural or city sub division?

IMHO its the only way you are going to make a gain out of land in NZ for the next 5 plus years.

The RBNZ will be hell bent on decreasing the 70% property lending of our NZ banks, the asset concentration IMHO does not match up with their financial stability mandate.

hence DTIs as well

Yep let me get my detailed plans out so I can post them on a public forum for yourself and others.. am I stupid? Don't answer that! Lol

Thats so funny, like I am going to subdivide 800 sq m to 4 townhouses but i will not tell you where.......

Rural vs City is hardly doxing yourself, I have friends about to sub city stuff, its looking like now may be a gd time to start planning so you can borrow in 18 months to build....

Yes blatantly doxxing yourself over different forums is your specialty... I love reading it, I suppose according to you I dont know what I'm talking about

Hi Retired-Poppy,

You made the same comments (as above) 7-8 years ago, insisting that FHBs should deposit their money in bank term deposits and not purchase a house...... Since then house prices have risen by around 60-70percent........ Much better to have reaped that capital appreciation AND avoided paying rent.

Important message to all FHBs: If you follow the advice of the DGM, you will never own your own home. For the DGM, the time is never right to purchase property. Be warned about their comments/advice.

TTP

Thats funny as I own 15H, how did I do this TTP?

Must be one of the bigger DGMs here... but also a trader and not scared of risk.

Why did the market go down... More Sellers than Buyers.

You old spooky spruiker

If I was a young FHBer I would move to Aussie, where you can buy a house AND your employer pays 10% into super for you!

I spent 8 years in London making pounds, its a great way to get ahead.

Why did the market go down... More Sellers than Buyers.

And the economy shat the bed. You always omit broader economic problems with house price declines.

Where in Aussie? Brisbane has just surpassed Melbourne in price.

Adelaide or Perth (Perth also has FIFO work which will suit NZ Tradies)

Well the top was marked by an economy that was TOO HOT, record borrow and spend loose fiscal conditions and low rates...... so NEVER just buy at the top of a rockstar economy!

When RBNZ first put OCR rate up Oct 2021, it was like watching a shark siren go off, all the buyers ran away....

You have to understand economy to trade well.

Or you can just watch top economists, when they buy a new house its normally the top.....

(Perth also has FIFO work which will suit NZ Tradies)

Just from anecdote, most of these guys will spend all their money on new wagons, or get super sick of FIFO before they can save the money.

Just be a decent tradie, literally anywhere in the practical skills bereft western world, and you should be able to afford a house (and have the skills to do up a knackered one).

Most of these guys.....

better to stay here and become infertile then?

Age doesn't impact a males ability to reproduce in the same way it does for females.

Adelaide or Perth (Perth also has FIFO work which will suit NZ Tradies)

FIFO is great if you are good at squirrelling away your money instead of pissing it against the wall, and realistically is only beneficial to stockpile cash for bigger plans. Makes for a hard time making long-term friends and finding a partner if you're only around 1 week every month.

"And the economy shat the bed."

An unintended consequence of housing price bubbles.

The bigger the party, the bigger the hangover.

Australian super is currently 11%, going to 11.5% in July, and then 12% in July next year. NZ just gets further and further behind.

Big discounts coming in mid 2023

No, wait, Jan 2024

Actually, low-ball in Autumn 2024

FHBs have more desire to buy, than many of the current sellers, who are attempting to trade up, sideways, or down. Desperation will be there for some, divorces that need to finalize, inherited properties the kids want to liquidate, that sort of thing, but many of these listings will either just sit there and languish, or the sellers will just pull the listing.

Poppy's target audience of wealthy plastic surgeons who've saved a million bucks or more in the 8 years of his advice, but haven't bought their first house, will do well. Although they'll probably now be infertile, so no kids for them.

you will easy get 10% off this year for these reasons

Spruiker alert level : desperation and panic

BUY NOW GODDAMIT OR YOU WILL BECOME INFERTILE

it was a long bow

I don't know how many times I could reiterate how I couldn't give two shits whether people join the ponzi or not. FWIW, I see a future of declining home ownership by the younger generations. Whether that'll be better or worse for them financially, I can't really say, as the market and society adjusts.

It's just inescapable fact that females have a limited window to have children, delaying it for the next market cycle to try and get a house cheaper is more than halving it this time round. FHBs motivations to buy, are usually stronger than those needing to sell.

Oh, that and every time people think houses are too expensive, they're usually very wrong.

"It's just inescapable fact that females have a limited window to have children, delaying it for the next market cycle to try and get a house cheaper is more than halving it this time round. FHBs motivations to buy, are usually stronger than those needing to sell."

How many FHB couples in NZ are even considering starting a family with the cost of living in NZ and specifically the greedy shitshow of our housing market? Of my children's large group of friends (early 20's through early 30's) possibly 2 have kids - the rest are either not interested or can't afford it. In recent history parents with the ability stumped up with a chunky deposit for them but even that has all but disappeared in their social network. What happens next?

We mass import more workers.

Delaying having kids because you don't own your house? Is that real? Or used as an excuse not to have kids?

I have never understood the concept of "getting on with your life". Renting doesn't stop you from doing anything. If you believe so you're the kind of person who will never do much in life, waiting for all the planets to align before comitting to a decision.

You don't have to buy a house to have kids (there's probably a better argument that renters have higher birth rates), but it is part of the psyche for people that they shouldn't have kids until they have their affairs in order, which often includes home ownership.

You could say that, someone with excessive debt who is struggling to pay their mortgage due to higher interest rates, does not have THEIR affairs in order!

And a couple who wants to take out a mortgage on a house will find their borrowing power drops considerably as soon as they have dependents.

You don't have to buy a house to have kids

No, you simply need to procreate, however the looming thought of losing one income and having the added costs of a child, coupled with the increases in core costs of living such as food, shelter, transport, all weight on the plans for those wishing to have children. Add in the very real concern that the cost of a mortgage may be possible to sustain on two incomes, but not in any way after losing one income to have said child, and risk losing all of their savings they worked so hard for to get their deposit, and it is easy to see there are very real and high risks to having children currently. Naturally this can vary depending where you are in the country, however anecdotally I have known several parents with young kids who rental locally to me, and they have been going from rental to rental each year or so as the landlords always say they're selling up, which seems to have been legitimate with them all going on the market not long after they leave. This is another unintended consequence of the housing ponzi we have, destabilising families.

Yes it's definitely real. It could also be the belief that they will be able to buy a house in the future, if that belief is low then so are your expectations of a stable family environment with our investor friendly rental laws. This isn't Germany where renters are better protected.

If you pump out half a dozen kids, Kainga Ora will give you a free brand new million dollar house. How's that for an incentive?

Better get cracking then!

Currently seeing a few places on a family members rural street selling up as the oldies downsize form their rural sections and lovely large houses. Nobody is buying and with many selling at the same time people are asking questions. All are asking over what they are currently worth, time will tell until one of them cracks and takes a lower price and the cascade will continue.

Even with record levels of high migration the NZ economy is struggling and housing market still sluggish. The alarm bells are ringing.

Good time to be a buyer. Don't pay asking.

Tell him he's dreamin

Exactly am out looking noe for next project

How are the prices of building materials tracking from the ground Colin?

Had an interesting conversation with someone involved in processing large development applications on the weekend. She told me that material costs were well down from where they were a year ago.

Most interestingly, when I asked how busy they were, she said that they had a lot of work - doing 'section 127s'. Apparently these are amendments to existing applications that have consent. The amendments were really being submitted to reset the 5 year consent time as delaying work seems preferable (I imagine due to financing issues possibly due to lack of presales).

I'm curious, has anyone ever.paid asking?

I've been prepared to pay over asking price on a few occasions. Never needed to though.

Few people investigate the critical value factors that I do so their understanding of value is not very well informed. I have come up against other parties that look at what I look at and these people will sometimes pay more than I'm prepared to. Win some, lose some. There's plenty to go around at present.

"has anyone ever.paid asking?"

Many buyers have paid well over asking price by the seller vendor. Where?

Look at auctions /("buying competitions" under conditions of FOMO) where buyers pay well over the vendor's reserve price.

This weeks auctions were lackluster...

Rates still holding higher.. prices going 👇

Can you remind us what the HPI showed over the last year... don't get fooled by the short term fluctuations.

DGM, would you say yesterday's REINZ monthly report that shows HPI is rising to be an inaccuracy, a spruiker conspiracy, or a dead cat bounce?

I'm also curious as to your hypothesis on rates. If rates are holding (although they're actually coming down) wont prices also hold if all other factors remain the same?

Is it seller desperation or seller confidence of an underlying change thats encouraging so many to come to market.

Just wondering

I think many people put their plans on hold over covid, then the market fell. OneWoof have told everyone its BOOMING last few months , so they all need more rooms , less rooms, different city, or smaller mortgage... No one wanted to sell into the 2022 falling market...

There is not enough borrowing power to settle all these sales at 7.25% mortgage rates, people cannot afford it now so people will have to meet the market or withdraw properties.

I still see -10% by xmas

They were waiting for NACT to save the housing market so held on.

Will get a lot worse.

New bright test triggers on 1 July - allowing those who bought within last 5 years to sell with no tax.

Rental market will lose a significant percent of its stock - markets will be flooded, new rental crisis like never before.

Those who bought within last 5 years should be underwater not worrying how much tax they're gonna pay

Ayup. And if you're financially distressed enough to sell your rental, you're not worrying about tax implications and it's highly likely on the market already.

and not selling

If someone's distressed, it probably will be priced accordingly.

$1 reserve seems popular....

What are all the $1 reserve listings selling for

"What are all the $1 reserve listings selling for"

For those properties in Auckland and Wellington, they are selling at prices that are lower than their independent valuation, homes,co.nz valuation in November 2021.

Remember what some commentators on interest.co.nz were saying at the peak? They may or may not have vested interests. The point is that these commenters are unable to see the impact of their advice at that time on those highly leveraged buyers in late 2021 - 2022.

Imagine an owner occupier taking their advice at the time, using ALL their life savings (incl Kiwisaver) and taking on large amounts of mortgage debt to purchase an owner occupier residential dwelling, who is now in cashflow stress, mental stress and could lose their owner occupied home in a mortgagee sale, and now face life changing financial circumstances which result in a deterioration of lifestyle at retirement. Many have experienced a significant loss in their equity deposit (some may even be in negative equity) and facing cashflow stress.

Names omitted intentionally (but these commenters are still active on interest.co.nz)

a) 9th Nov 21, 2:38pm

"I have always looked at this from the opposing direction - the risk in not owning a property? If you do not own a property you are short, not even square, but short"

b) 9th Nov 21, 5:52pm

"Or maybe right the opposite, don't hesitate, be brave and go for it, you'll be fine"

c) 23rd Nov 21, 8:52am

"It makes absolutely no sense for a couple like this to bank a capital gain now rather than wait two years and avoid 90k in taxes. The market is not going to crash 10% in the next two years."

d) 9th Nov 21, 2:38pm

"locally, I can not see anything in the near future that would decrease these current values."

e) 14th Oct 21, 11:25am

"Shrewd investors will capitalise on perceived price weakness - cementing their position for the next market upswing.

Well located property remains a prime investment for the long term. (But you already know that.)"

f) 9th Nov 21, 6:50pm

"Odds on anyone still able to buy a house and make the mortgage repayments and has the right attitude will come out the the other side."

If these commenters did not have any vested financial self interest, then they didn't know what they didn't know. They didn't know about the extremely elevated house price risks.

Remember what were property commentators saying at or just after November 2021?

1) Tony Alexander - 19 reasons why there's no crash - December 2021

https://ndhadeliver.natlib.govt.nz/.../DeliveryManagerSer...…

2) Catherine Masters - July 2022

Why the New Zealand housing market is nowhere near crash point

https://www.oneroof.co.nz/.../why-the-new-zealand-housing...…

3) Ashley Church - April 2022

Four reasons the housing market won't crash

https://www.oneroof.co.nz/.../ashley-church-four-reasons...…

4) Kelvin Davidson - Dec 2021

“But will prices actually fall? I’m not convinced because in the past a serious housing downturn has come with a recession, but no one is suggesting that and unemployment is low at 3.4 per cent.”

https://www.stuff.co.nz/.../real-estate/127305870/what-lie…

5) Nov 2021 - Here's why it might be fruitless to pin your hopes on a house price crash

Rental market will lose a significant percent of its stock - markets will be flooded, new rental crisis like never before.

It's a real shame houses vapourise into nothing once an investor sells, they should do something about that.

They don't vapourise, they just leave the rental pool.

As the get bought by renters who then don't need to rent. Exactly what we want to be happening.

And the modern first home buyer is far more likely to be letting a room or two than traditionaly might have been the case.

I did a trial pre approval and this topic was brought up and recommended by the advisor over 1yr ago outside of my preexisting intention to do the same.

My closest confidante also had the discussions with a different advisor at another time prior. Where the suggestions or discussions were had.

Another friend has just moved in to board with some first home buyers they previously rented with. That in another NZ city.

Do not fear that commercial business oriented landlords exiting will mean so many more empty homes and rooms whilst those people previously homed become not so.

Ironically, some houses leaving the rental pool do get 'vapourised'.

Not to worry though. They typically get reincarnated as 3+ new houses on smaller sections and sometimes we can even save the existing house from vapourisation by transplanting it elsewhere. ;-)

Reincarnation is a thang for houses. lol.

I had to feel for the family that bought my childhood home and had it cut up and trucked to a rural section. Builders took 5-6months to come and get the roof on it, meanwhile half the houses carpet got waterlogged and other bits and pieces. They got a lovely old 1800's hardwood home for peanuts and now have to fork out to get major repairs done.

Where I live ( a North Island provincial capital) anything north of close to $1m is dead in the water. Buyers simply cannot get the finance or don’t want the level of finance needed to upgrade. Prices will have to be lowered if people need to sell. Tougher times are coming. We have been greedy. Now we have to face reality.

I am hearing from agents that regional NZ, buyers failing finance on the new interest rate test rates. Re ofer lower and get told no from greedy sellers, not sure where all the new rich buyers going to come from, maybe migrants...

5700 buyers last month, not all failing their finance applns, most being approved

Is there some evidence of approval, or just a feeling?

Plain logic. High sales would be 10k per month and the level of demand is just not there now. If all borrowers were approved that might make 8 to 9000 sales per month. Its clearly more than half are accepted

Thats my observation as well. A larger proportion of 'lower quartile' houses are selling than before. FHBs are making up a bigger proportion.

Median prices are flat but HPI is steadily increasing.

All this tells me that buyers are lowering their house expectations more so than sellers lowering their price expectations.

The price of lower quartile housing is still linked to the cost of building, the remaining life of the house and the likely maintenance costs. The costs are linked to inflation, and inflation isn't going away. Most sellers are sitting on significant equity, and the frothy top of the market in 2021 was marked by a very small slice of buyers at the time. If you don't have to, most will just wait. If unemployment ramps up, there may be a few more motivated sellers. Most of the interest.co.nz articles focus on the Auckland market, the rest of the country is more affordable, and plenty of people are spending up on upgrading their homes.

The price of lower quartile housing is still linked to the cost of building, the remaining life of the house and the likely maintenance costs. The costs are linked to inflation, and inflation isn't going away. Most sellers are sitting on significant equity, and the frothy top of the market in 2021 was marked by a very small slice of buyers at the time. If you don't have to, most will just wait. If unemployment ramps up, there may be a few more motivated sellers. Most of the interest.co.nz articles focus on the Auckland market, the rest of the country is more affordable, and plenty of people are spending up on upgrading their homes.

Thank you Einstein

The housing market pendulum swings in extremes. Remember how hot it was 3 years ago? We are currently experiencing the inverse of that. The valleys are as deep as the mountains are high.

That said, prices will recover, and when the upturn arrives, it’ll quickly wipe away any losses, and the cycle continues

"when the upturn arrives" will be some considerable time away..............

"prices will recover, and when the upturn arrives, it’ll quickly wipe away any losses, and the cycle continues "

Or it may not ... LVRs and now DTIs + more supply.

I doubt we'll see anything like the extreme peak we saw in 2022. No RBNZ MPC/Gov will make that mistake again. "Below normal i-rates" will be much more carefully managed in the future with small rises triggering LVR and/or DTI ratio contractions. The boom/bust cycle in NZ's building sector is causing heaps of damage.

In the nearly 10 years of Ireland implementing DTIs:

- wages up 25%

- house prices up 80%

- rents up 90%

- 25 to 34 year olds still living at home up 50%

It would appear DTIs aren't an effective tool at improving affordability. Potentially the inverse.

House prices in Dublin fell 70% at the GFC. They introduced DTIs in 2015 which were 4 for FHB and 3.5 for others. In 2022 the house price to income ratio in Dublin was 5.7. In Wellington we're staring at 9's and in Auckland 10 - 12.

What would our house price to income ratios look like if we had Ireland's DTI's?

Lets not let the facts get in the way of a good spruik

Ireland's a great example why not every bubble burst is the same.

Super cool how most discussion on here wants to play pointy finger and labelling others, instead of a robust, reasoned discourse.

Agree, would be nice if we could have a debate without the lazy ad hominem.

It's often code for "I lack any cogent response to what's been said, so let's play in the gutter"

Few of the answers to much of our issues is as simple or clear cut as people like to think. Life can be full of taking the least bad option.

Likely still pretty high. Put it this way, if we follow Ireland's path, 70% price falls, DTI, the whole sheebang..... Houses won't be any more affordable.

This is because DTIs don't actually address affordability, they just limit borrowing. The flawed assumption is reduced borrowing automatically makes prices lower.

New house building in Ireland has been in the doldrums, because the market can't meet the DTI limits, so everyone ends up scrapping over whatever houses exist (either to buy or rent).

The discussion regarding affordability on this site sits disproportionally in concepts that won't provide it.

Yet they're still building 30k homes a year? A similar number to what we're doing, except they have DTI's "hamstringing" them. In fact technically they're building slightly more than us.....

- Ireland completions increases 10% to 31.5k in 2023.

- NZ gains 27k houses in 2022.

Look back 10 years, and also compare the same years - we were over 50,000 in 2023, 2022 was an extreme low due to COVID complications getting construction done.

Both countries are under building though.

Are you sure you're not referring to consents? There were 16k homes completed in Auckland 2023. So 34k in the rest of the country??

https://www.interest.co.nz/property/125203/record-1927-new-homes-were-c…

Also, here's a chart showing the number of home completions in Ireland from 2011 to 2023 by quarter. Notice how this starts to increase in 2015, coincidentally when they introduced DTI's?

https://www.statista.com/statistics/1417855/ireland-number-of-homes-com…

Why do you think this happened?

Mortgage interest rates could have helped? Average mortgage rates in Ireland:

- 5.86% in 2008,

- 4.05% in 2015,

- 2.8% in 2022.

Interest rates indeed but without the prospect of capital gain due to said DTI introduction then the focus for profit would be around subdividing and building in volume.

"Put it this way, if we follow Ireland's path, 70% price falls, DTI, the whole sheebang..... Houses won't be any more affordable."

Can you expand / clarify on your perspective how after a 70% price fall in house prices, house prices won't be any more affordable?

Why would you hold up Ireland as a good example? They have one of the worst housing crisis in the world. Ireland is what happens when Govts decide to force housing investors out of the market.

https://www.stuff.co.nz/business/property/129646516/heres-what-we-can-l…

https://www.nytimes.com/2024/01/15/world/europe/ireland-housing-crisis…

Fairly typical response from you there, Pa1nter. I.e. grab some random facts - while presenting no context - and concluding what you want to conclude.

For some context, you could read this from the Eire central bank (no less) ... https://www.centralbank.ie/docs/default-source/publications/research-te…

(And no. I won't be replying to your attempts at misdirection. It just a waste of time as you are always right.)

Don't worry, National will do what they can to keep the market alive... Reversal of the interest tax rules is just the start.

$20 per week tax cuts will save the market /sarc

I just got some local (auckland) data on recent commercial industrial sales and leases, Im really not sure what is going on, recent sales make no sense to me, gross returns mostly around the 4 - 5% mark, some even lower. Im picking some pain in this arena over the next couple of years.

Singapore selling Westfield holdings in NZ, about 1.4bil I think.

They will be selling because relatively speaking our commercial property looks expensive to other countries. Read “ we haven’t adjusted enough yet as we are deluded” Commercial property was being valued off a retail model during the C0%ratesVID era and now money is more scarce real valuations need to take hold again. Think there’s pain in residential??……

I've made a 24% gain on my Scentre Group shares since 1 January, plus am getting a 6.2% dividend. More to come once interest rates start dropping.

LOL. Be careful.

If you are a potential FHB and can keep your job while the money supply carries on contracting then things will look better and better as time goes on.

Personally, I don't think a small decrease in interest rates is going to lead to enough new borrowing to turn things around. Nor will new immigrants (too many planning on leaving for greener pastures are potential FHBs so will balance that out). Nor will a reduction in new builds (supply is not the issue - demand is and it is being decimated by the cost of money). Demand will eventually return/be acted on once prices make sense and this will be reflected in an increase in the money supply via new borrowing.

Long story short, look at what happens with lending. Rising prices are a reflection of new money entering the system.

If you don't believe that supply has a less significant part to play in this consider the fact that from London to Vancouver to Sydney to Auckland to just about any other major anglo city (and beyond) everyone will blame some particular local planning issue for the cost of housing. They're (mostly) wrong. This is a global asset price issue and it has everything to to with the simple fact that there has been more money sloshing about. Until new money is pumped in at sufficient quantities (via lending) the downward trend won't reverse. Sure, there'll be bumps along the way in this market or that, but the ultimate cause and trend is clear.

If you start seeing signs of anything that looks like QE, pay attention!

"If you don't believe that supply has a less significant part to play in this consider the fact that from London to Vancouver to Sydney to Auckland to just about any other major anglo city (and beyond) everyone will blame some particular local planning issue for the cost of housing. They're (mostly) wrong."

Could elaborate on why you believe they're most wrong? It differs from the impartial views I've read that conclude supply is a factor and local planning rules have played a significant part in limiting supply.

Yeah, sure.

I've got a lot to say about the whole supply vs demand issue. I'll try to summarise some of it here - starting with that comment about planning.

Obviously I'm not trying to argue that more supply is not a good thing insofar as you consider lower prices to be a good thing.

The comment above is basically an application of Ockham's razor. Is it likely that all of those cities suffer from their own particular brand of bad planning or even the exact same form of bad planning resulting in the same issues with housing affordability, or is it more likely that there is some other common cause? I am suggesting that there is a more likely common cause - cheap credit / an inflated money supply. This is clearly the case with other asset classes. Why should it not be the case with housing (especially since this coincides with the 'financialisation' of housing - particularly in anglo culture)?

Another thing that makes me question the common wisdom of high prices being due to a shortage of homes (as opposed to investments) is that there are two good examples of instances where high prices don't correlate with low vacancy rates.

In Melbourne, Prosper Australia (a very old Georgist organisation) have shown with their 'Speculative Vacancies Report' that areas of the city with the highest vacancy rates are the same areas that have experienced the most capital gains in the past year (think inner city areas like Fitzroy, Docklands, etc). Notably they don't use real estate agency data to identify vacant properties - they rely on water usage - so much more reliable in my opinion.

In the UK (actually just England from memory), a study was done using council data (they have good usage statistics due to the 'bedroom tax'). They determined that the proportion of what they term Low Use Properties or LUPs (which include holiday homes for example) is highest in areas with high property values. The study was prompted by all the anecdotal evidence of the widely held belief that wealthy foreigners were buying up houses in the most desirable areas and leaving them empty.

Both of these studies demonstrate that what you might intuitively think to be the case - i.e. that vacancy rates would be lowest in areas with the highest demand - isn't actually the case in those places at least (England and Melbourne).

In a past life as a postie in Wellington I saw this firsthand. As an example, there is a very desirable street in Mt Vic - McFarlane Street. I delivered to that street for years. At any one time about one third of the homes were empty (on the market, being renovated, owners away, even looking mothballed in some cases).

StatsNZ keep statistics on the number of households and the number of what they call 'private dwellings' going back to about the mid 90s. When I looked into them years ago it was clear that the proportion had not changed significantly and that when it did change there was no correlation with prices (i.e. as households:dwellings decreased, prices often went up and often vice-versa).

All of this of course comes down to what we mean by demand. My argument is that since residential property has been financialised to an ever greater extent, a certain amount of what I would call 'artificial' demand is created. A boom will attract speculators. Cultural and technological shifts can cause the short term rental market to explode in size. This is not demand for homes, it is demand for investments.

We should be looking closely at the things that boost demand for property investments. That is the easy but unpalatable (for many) solution to our accommodation (and by extension, social) crisis.

For an example of how the waxing and waning of investment demand can have an impact on availability of homes, just look at Ireland. Pre-GFC, the common wisdom was that there was a shortage. Within a short period of economic downturn, suddenly there was an oversupply. And now with the recovery a shortage of homes (but plenty of AirBnBs!).

I won't get into this now, but if you want to argue about why people would 'leave money on the table' by underutilising property I could give you a host of reasons, but it's better left for another time ;)

I might just add that I've held this view for a long time and saw it as some confirmation when a downturn in prices here in NZ saw a corresponding increase in rentals on the market. I am fairly certain that much of that was due to the surfacing of underutilised properties. How else could it be that there was a period - as far as I recall - where the number of both properties for sale and properties for rent both increased?

Reasonable to assume given the increase in ease to rent out a batch or the family home via the likes of booking.com and AirBnB.

AirBnB and the like are having a much bigger effect on the long term rental market than many people give them credit for in my opinion.

I remember looking at available 'entire residence' numbers on AirBnB for Mt Vic sometime ago and counting about 50.

Assume Mt Vic has around 2000 dwellings, that's about 2.5% now on AirBnB. Even assuming that half of those on AirBnB are actually primary residences being made available for a time, that would make 1.25% of dwellings removed from the long term housing stock.

Now consider that a typical number of available rental properties that are vacant is about 3% (i.e. not including other vacant or underutilised properties - only those listed for rent or currently rented). If those 1.25% of properties in Mt Vic all shifted from the short term to the long term rental market it would be very significant.

Demand for money. As is obvious by the surge in listings, the promise of money tomorrow is uncertain. So long as that promise remains via incentives, subsidies and allowed speculation, there is incentive to withdraw a house from the pool and leave it idle. Would people land bank a property if it was certain it would halve in value in 10 years?

Would be interested to know a % of renters who think the status quo is working, remove all the crocodile tears.

Would people land bank a property if it was certain it would halve in value in 10 years?

Exactly. Further to that, would people pay current prices if capital gains were off the table (I'm not even talking about further falls)? Unless the money printing machine (i.e. cheap credit) starts up again this is the foreseeable future. Cheap credit is not 0.25 or 0.5 less than the current rate. All of the talk of planning, construction, red tape, etc is secondary to that fundamental.

I should add that I do actually believe that we are in for more QE in the future, sadly. Until that happens though, as I said, the foreseeable future...

Some great points there. There’s a minority movement called ‘supply skepticism’ that questions the whole assumption that lack of supply is the major issue in terms of housing affordability.

I don’t subscribe to it, but they have a point. I personally think the truth sits somewhere between their view and the conventional viewpoint.

Never heard of 'supply skepticism'. Thanks, I'll take a look sometime.

I should make it clear that I am not arguing that supply constraints don't play their part - that would be silly. I'm just of the opinion that the more significant part of the supply and demand equation as it applies to the housing market has been on the demand side for a long time (not necessarily always and everywhere of course).

Supply side issues do also need addressing and always will as communities naturally grow and change, but it can never be a sufficient solution to our current problem. It's just easy for politicians to argue about while ensuring everyone can stay on the gravy train. It's politically 'safe'. Let the councils deal with that one or better yet use it to your advantage and come up with some boondoggle.

You could, in theory, cause an accommodation crisis in a growing community with supply constraints alone, but that is definitely not what is going on here (or in Sydney, Vancouver, etc) in my opinion.

As an aside, I was living in Australia when John Howard was elected. I remember he repeated the mantra for years that "interest rates will not go up under my government". I was young at the time and wondered how and why he would put so much emphasis on this claim. Turns out you can pretty much tie it in directly to the start of the mainstream property investment madness. The terms 'negative gearing' and 'equity mate!' appeared in the mainstream around the same time.

I did just look into 'supply skepticism' and although interesting, doesn't really seem concerned with the issues I raise.

To sum up my view (as I did in a recent comment below):

The property boom of the past few decades has caused an increase in real vacancy rates (or underutilised properties if you prefer).

Didn't know there was a movement as such but where do I join...

Number of NZ private households (2022) - 1,943,000 - https://www.stats.govt.nz/information-releases/dwelling-and-household-e….

Poulation (2022) - 5,127,400 - https://www.stats.govt.nz/information-releases/national-population-esti…

Working Poulation >20yo (2022) - 3,802,000 -https://www.stats.govt.nz/information-releases/household-labour-force-s…

On above numbers there's enough houses for one house per 2 working age people i.e. per couple.

Or 2.6 people per household allowing children.

Obviously houses aren't always where people want to live, but many sit vacant in some of the most desirable places in NZ as baches, which links to earnedincomes point.

Obviously houses aren't always where people want to live

Now consider that two of the studies I mentioned above (concerned with the markets in Melbourne and England) indicate that the proportion of vacant/underutilised properties is highest in expensive areas. That means cities for the most part.

In the case of the Melbourne market, obviously they were only looking at a city, but it was clear that inner suburbs such as Fitzroy had a much larger proportion of underutilised properties than a place like Werribee (a far-flung suburb full of new build McMansions).

Just look at Queenstown as the example

Thanks for the reply. You don't mention the population growth of our cities.

More people need more houses. If the houses don't exist, those than can afford to bid up the price. Had Councils not restrained supply - more dwellings of the right kind and at varying price points would have been built - and we'd not have had decades of above inflation house price rises.

Greenies like Murray Grimwood aka PDK and Gaudy Garry Taylor got elected on councils so they could change the land supply rules. Fuk em

I didn't mention population growth directly, but did refer to the StatsNZ household and private dwelling numbers and how they have changed over time (apologies for not looking them up again but it was some time since I looked and the site is not making it easy to find them again). Taken together, they don't indicate a steady decline in dwellings relative to households over the past few decades (as you would expect if supply was the cause of price rises). It's also worth noting that household size hasn't been increasing, so we can rule out explaining the dwelling to household ratio not decreasing by reference to that.

I agree that supply is important and that planning changes are needed to accommodate growth, but my argument is that this is secondary to availability of credit and demand side issues in general when it comes to price rises. I didn't mention tax incentives, but obviously they also play a part and are worthy of attention when looking at the demand side especially.

more dwellings of the right kind and at varying price points would have been built - and we'd not have had decades of above inflation house price rises.

While I agree with the first part of that statement, I am a long way from having faith that the second part would follow. In my opinion we won't solve this problem without addressing the demand issues.

Just for good measure, here's another argument for demand side causes. In the past, owning a second home (such as a holiday home or pied a terre) was generally an expense. Fewer people subsidised them by renting them out on the short term rental market and capital gains weren't sufficient to justify a complete lack of income generation.

Once prices started to rise at a sufficient pace, capital gains made all the difference and simply owning a second home was no longer an expense but a lucrative investment. Also consider others that were incentivised to purchase second homes due to the burgeoning short term rental market. It's not unreasonable to assume that the proportion of people that own second homes (I am not talking about long term rentals) has increased for this reason.

Now, consider that by definition a primary residence cannot be vacant, only other dwellings. If the proportion of primary residences to other dwellings has decreased (for reasons such as given above) then it is not unreasonable to assume that the proportion of vacant dwellings will have also increased.

Here is an anecdotal example of the above from a conversation I had with a relative just last week. They are by no means rich, but are looking to purchase a small apartment in Wellington to make it more convenient to visit their grandchildren when it suits. They will be relying on some existing funds, probably equity, and the possibility of AirBnB to subsidise this purchase. This would have been unthinkable for people in their situation thirty years ago, but essentially they are talking about taking an existing property and precluding it from becoming a primary residence. I don't think their case is all that unique.

Ultimately, I believe - against what seems intuitive - that the property boom of the past few decades has caused an increase in real vacancy rates (or underutilised properties if you prefer).

Been house hunting since May 2023. This article reads like my experience. Lots of houses staying on the market or pulled because boomers want 2021 prices for the homes they haven't maintained for 30 years.

The stalemate continues...looks like vendors aren't too stressed to sell. How many more weekends will you go to open homes & waste time on due diligence - would you be prepared to pay a slightly higher price to be able to move on with life?

Yea why not take on $800k debt for your first home then just get on with living?

This stalemate is often broken by the 3 D's

Here is one group - distressed developers

https://www.oneroof.co.nz/news/cruel-reality-developers-offering-huge-d…

Could these developers not have made sufficient pre sales? Or is this the remaining inventory that was unsold? Or perhaps previous off the plan buyers have chosen not to settle at settlement date?

For a typical person, that slightly higher (or lower) price can be translated into a year of work or even significantly more. It's a high stakes game.

I encouraged a family member to hold off in 2022. They're a good earner and the saving they made by buying 18 months later translates into over 2 years of work (or more than 4 years when interest is considered).

Not sure I'd be so confident to advise them to hold off now though. Things are not as certain as they were then. Happy to take my own advice though :)

"It's a high stakes game."

This is something most people do not realise. The property promoters with their vested financial self interests won't tell you this.

Peaker vs Buyer Today

How does this compare with a Peaker and a Buyer Today (BT) in NZ?

1) Peaker

a) Nov 2021

The median house price at the peak for Auckland was $1,300,000

With an 80% LVR, this is a mortgage of $1,040,000

The 20% equity is $260,000

b) Feb 2024

REINZ median House price for Auckland: $975,000 (-25.0%)

Mortgage: $1,040,000 (assumed to be interest only for comparison purposes)

Equity: NEGATIVE $65,000 (-125%) (i.e negative equity)

2) Buyer Today ("BT")

The current REINZ median house price for Auckland is $975,000

For a buyer who waited, and used the same $260,000 equity used above, the mortgage at this price would be $715,000 (an LVR of 73%)

The Peaker has a mortgage which is higher by $325,000 (mortgage of $1,040,000 for Peaker vs $715,000 for BT)

As a result of that additional borrowing, at a 6.8% mortgage interest rates over 30 years, Peaker is paying $770,000 more over the 30 years than BT (30 years x $25,667).

Assuming same incomes, and same living costs (food, travel, etc except mortgage), BT can save the $770,000 in payments that Peaker is paying.

The annual payment on the additional mortgage of $325,000 is $25,667 per year.

1) Peaker pays $25,667 more per year than BT.

2) BT instead saves that same $25,667 per year. At a deposit interest rate of 5.8% (after 33% tax is 3.9% p.a). Saving $25,667 per year and earning 3.9% per year in net interest after tax for 30 years comes to a total of $1,415,685.

$1,415,685 - this is money that BT has available for retirement after 30 years that Peaker will not have.

Remember that at the end of 30 years, the house price will be exactly the same for Peaker and BT.

BT will have more money available for retirement than Peaker.

Here are the respective cashflows for Peaker and a Buyer Today (in Feb 2024)

1) At Nov 2021

a) Peaker:

i) Mortgage: $1,040,000

1 year mortgage interest rate: 3.47% p.a

Mortgage payment: P&I 30 years: $56,348

ii) Rates, insurance: say $6,500

iii) Total payment $62,848

b) Buyer in Jan 2024 rents until Jan 2024:

i) Rental per year $33,800 (2.6% gross rental yield on Peaker's purchase price of $1,300,000)

ii) Saves: $29,048 (this can be added to their deposit and can reduce their mortgage even more than $715,000 mortgage used in these calculations)

iii) Total payment: $62,848 (same cashflow as Peaker)

2) At Feb 2024

a) Peaker

i) Mortgage: $1,005,618 (reduced due to principal payments)

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 28 years: $85,421 (increase of 51% from 2021 payments)

ii) Rates insurance: say $7,166 (due to inflation)

iii) Total payment: $92,588 (this assumes that the Peaker can continue to hold on - in many cases the increase in payment may be too much of a burden on household cashflows and need to sell (and realise their loss of savings as noted above)

b) Buyer today

i) Mortgage: $715,000

1 year mortgage interest rate: 7.32% p.a

Mortgage payment: P&I 30 years: $59,482

ii) Rates insurance: say $7,167 (same as for Peaker)

Total payment for housing: $66,649

iii) Additional amount to reduce mortgage principal: $25,939

iv) Total payment: $92,588 (same cashflow as Peaker)

Some mathematics:

For every $50,000 in additional borrowing to purchase a house today vs a cheaper purchase price in the future, this represents

1) a total of $125,034 over 30 years (at a 7.34%p.a mortgage interest rate)

2) At a 33% tax rate, this requires pre tax income of $186,618 over the next 30 years.

Additional payments to purchase the SAME house. Remember, that at the end of 30 years the house will have exactly the same market value.

3) reinvesting the mortgage payments on that additional $50,000 borrowing at 4.02% p.a (6.0% deposit rate and 33% tax rate) is $234,534 in year 30, that the lower priced purchaser can have available for retirement that the higher purchase priced buyer will not have.

Thanks for these comments. It's really quite stark when looked at closely. The (dark) magic of compound interest!

In general I think that a big part of the problem is that people basically give advice to others along the lines of "this is what I did, it worked for me, it'll work for you" with no consideration of different circumstances.

People like TTP who do not own a house you mean?

People like TTP who do not own a house you mean?

Learn from my mistakes.

TTP

not sure why anyone should take your advice TTP?

why with all your wisdom do you not own a house?

waste time on due diligence

Since when is doing ones due diligence "wasting time"? Especially when it comes to the largest purchase most people will make in their lifetime?

Go along to open homes now vs 1 month ago.... tumbleweed

be Slow

I'm in a similar position to Mikey and the answer for me is no.

Ultimately this is the first time in more than a dacade that prices aren't skyrocketing. Even if they aren't dropping, every passing week of more saving buys me more equity and financial security when the right opportunity comes up.

Hang in there Mikey. I’m pretty confident you are doing the right thing. Much better to buy late than to buy early and lose you equity.

Although it’s stressful, it would be far more stressful had you bought 12 months ago.

Why would it be more stressful if you bought 12 months ago? You'd be living in your home, value the same or higher according to HPI, potentially paying lower rates than offered now, not wasting time with open homes stressing about what to buy, not dealing with a landlord...

Looks like real estate commission is drastically changing in USA, because current model has been deemed to be causing inflated house prices. Off to find some written material on it. Hopefully we will follow suit here, real estate agents need to be balanced and fair with both sellers and buyers.

Always been a mystery to me why agent commissions should increase along with house prices. Were agents in the 90s really worth so much less than agents today? Or maybe it has nothing to do with 'worth'?

I suppose you could make the argument that there are more agents to share the pie around now, but that is a shitty outcome for buyers and sellers. Imagine if more dairys meant higher prices because 'they all have to make a living'.

I'm obviously missing something...

Agents are vastly overpaid. Generally no post school qualifications or failed at an earlier endeavour and they are paid more than a specialist who is making your life easier or even trying to save your life.

Not 100% correct. Specialists can easily earn millions by dumping public work, or relocating to Aussie. Neither a good outcome for kiwis without medical insurance.

Last chance to offload before the bright line tax avoiders charge the exit mid year. Many will sell at what ever they can get ratcheting ever downwards the estimate algorithms tracking lower and lower. Margin call anyone.

This will pour petrol on the fires of speuvestor fear...

they have to find buyers, who seem suddenly not so interested.....

Then from midyear all the much, much lower CVs get released locking in the 3 year print listed reality of much lower values.........

This will have the 2021 to 2022 values seen as a Tsunami flood tide values that will take 10 to 20 years to surpass..........HIGH interest rates will guarantee it.

While I like your pitch, councils are generally so in debt and behind on infrastructure investment I'm not sure CVs can ever be lowered accross the board. It's a tax after all.

That said, houses can, and are, selling for less the council could not care less.

While I fully expect my CV to drop 200K .......I expect I will still face 10 to 20% rate increases p.a over the next few years.

The coming 25.8% increase in water charges for Auckland properties in 4 months, will be a big whack around the ears for the poorer households......plus the big Council rates hike coming to everyone.

The coming much lower CVs, won't mean any lower rates for anyone, quite the opposite given the creaking infrastructure, upgrades, as we all know.

It just may slightly alter how the increased councils spending costs will be spread and apportioned to the already beleaguered ratepayers based on where your value matches the average value movements "down and downer".

It's truly HERFL, Higher every rate for longer.

The price of the cv has no relevance to the overall rates take. It's just a way of deciding who pays how much.

Average CVs could drop 100% or increase 100% and the total rates take would not change and if your CV dropped or rose by the average amount you would pay the same rates as if it had stayed the same.

When asking if prices are rising take a look at average size of section house sits on for new builds and it’s price per square metre

Lo you will see land is now 450m per section at Warkworth for example. 5-7 years ago in Orewa it was 600m. And standard prior to 2000 was about 800m

in short you pay more for less

What is land price inflation??

Carry costs for residential property (outside of mortgages) are to double in the next 5 to 7 years.......how you like them multiple mortgages on rental properties now......?

No, you cannot 1.5 to double the rents.....

Piles of houses that can't be sold. How do you reconcile this with the housing shortage narrative?

A1 is coming for the new real estate agent. They will have more empathy than current agents 😊

By A1 I presume you mean AI?

Yea, I wonder, if AI will replace RE agents, which should be pretty simple on the 'transaction' side (not sure about the 'bargaining/promotion' side), what will that do to house prices? I guess they will come down a bit?

that RE 60k+ commission on a 2 mil property will likely only cost a couple of k if AI does it. So that 2 mil house can effectively be sold for just over 1940k and the vendor will still walk away with a similar return. Will be interesting to watch that space.

Or sell yourself. Save it all.

My neighbour has just sold for $2m......CV $1.7m.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.