The shortened week after Easter witnessed a sharp drop in auction activity, with the number of properties going under the hammer declining by more than a third compared to the previous week, which was also short due to Good Friday.

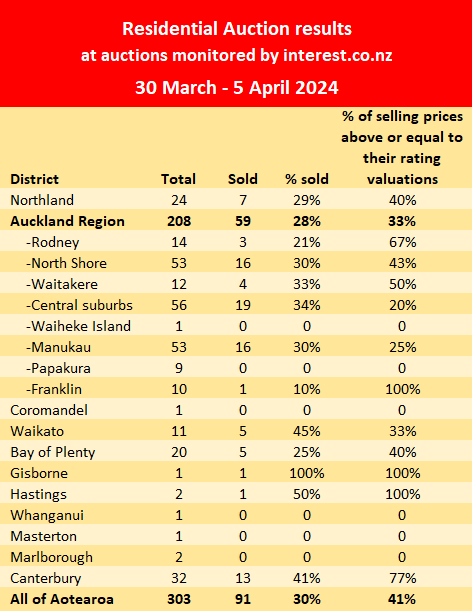

There were 303 residential properties on offer at the auctions monitored by interest.co.nz in week of March 30 to April 5, down from 527 in the week before Easter.

That was the lowest number of properties offered at the auctions monitored by interest.co.nz since the first week of February.

However the sales rate stayed about the same, with 91 properties selling under the hammer at the latest auctions, giving an overall sales rate of 30%, up just slightly from 28% the previous week.

The latest results suggest auction activity is starting fall as we head out of the peak summer selling season and into the quieter months of autumn and winter.

The table below gives the results from each district covered at the latest auctions, and details of the individual properties offered at each auction, including the selling prices of those that sold, are available on our Residential Auction Results page.

The comment stream on this story is now closed.

•You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

111 Comments

Such a low rate of success. I am assuming that these figures don't include successful deals by negotiation immediately after an auction? Can't quite understand why anyone would try to sell their house by auction and cut out 90% of prospective buyers who can only make conditional offers.

True, it works in the buyers' favour for those who are pre-qualified

1 in 3 are selling their home after a 3 week campaign,

Despite the stats being terrible, this still seems to be a better result than other marketing methods right now.

If it doesn't get any interest at auction you move on to selling by negotiation. I have been following a lot of properties that got reasonable bids that were passed in and the great majority eventually sell later for more than the passed in bid. It's very rare to see one sell for less. Going to auction adds a grand or so to the marketing equation.

I believe if the property sells on the day or day after the auction it is considered as sold by auction unconditionally. Although i wonder why buyers agree to this.

I've been watching a few auctions and it amuses me by the way the auctioneer talks about "pesky conditional offers" if the property doesn't sell at auction. They always throw it in like it's a horrible thing to happen and the people wanting to bid should never let it happen. I just can't understand why anyone would buy a house without being able to put in conditions. Especially when there are things like un-consented additions or similar.

It isn't school hols yet, what would explain the big 42 percent drop in numbers between two shortened weeks.

Perhaps the data set is just too small to draw any meaningful conclusions from?

Your right the numbers are dismal

Still a week of school to go for most.

Still a week when lot's of people go away. Are not around. So you don't put it to auction then.

In the east Auckland suburb I live in the last few months auction results show most houses passed in. Of those that sold a lot are several 100k under CV.

The fact you think CV is anywhere near market value or indeed any valuation is what is hilarious here. They do not even look at the properties or the land in question (a high slope with leaky rambshackle & slippage next to a flat slope with a mansion can get quite similar CVs if they were positioned close to each other and often have). No CV in history has EVER been a property valuation but a standardized measure for rates payments done with a cheap computer algorithm for councils differentiated by the suburb and number of properties within it, with some cheap sales data thrown in so it does not seem completely bonkers inequities between suburbs and services (but it always is). Geez soon you will be thinking that the CV is an accurate market valuation for leasehold properties and apartments. Completely clueless. Most CVs are way out by hundreds of thousands.

But I guess it is the misperception of fluffy wealth goodness that you get from your CV that keeps you warm. Next time actually understand what a CV is and understand it relates to your rates payments not a market valuation. It is easy to get your CV reduced and you should because it helps reduce the general increasing of rates to account for the sprawl. You CV is a point in comparison to others stating that you either pay more or less rates in comparison to them. Hence suburb by suburb those that cost the most to councils and drain the most in services usually pay much more. Added targeted rates are usually added on top for specific infrastructure items that are new.

Gosh you are in a grumpy mood today Pacifica. I agree that the actual purpose of a CV is not to set a price for the house, but to strike rates. But I think in recent times the proliferation of valuation websites along with the very unstable market has meant that many are looking to CV as an indication. In our area there are very low sales volumes meaning getting a list of recent sales as comparisons is very difficult (here a sale of a similar property from 12 months ago gives no indication of the value of a property today). So what appears to be happening is vendors and agents are using the estimates on these websites in a lot of instances - these all appear to be a function of CV …………. rightly or wrongly.

While we all know that CV's are only used for rating purposes (and I refer to them as RV's for that reason), when I got my updated RV a few years ago I objected and had the property revalued by a Council valuer. At the time we were thinking of selling, hence the reason for the objection. Two months after the revaluation, I had a RE agent contact me with an unsolicited offer - we were not on the market at that point. The purchaser said they would not pay a dollar above the (revised) RV, and that was what we accepted. The revaluation was an increase of $355k above the updated RV (it went from $1.2m to $1,555m). We were surprised, in a good way, and wondered at the time what we might have been offered if we had not had the revaluation. Anyway, the lesson is that while it may cause hilarity, it is nevertheless true that some purchasers fail to recognise the purpose of a RV and our instincts that we should accept a small increase in rates for that reason turned out to be beneficial for us. It also pays to remember, in this context, that the major components in rate calculations are services, and that the valuation only forms a part of the calculation.

The property besotted are struggling to reconcile the poor throughput rate and coming up with some humorous uninformed explanations and theories supporting sustainable price increases while fixated on past performance. They cannot explain why unsold inventory keeps piling on and refuse to acknowledge the building case for a resumption of the downward trend that began in Feb 22. With local job losses only beginning alongside mounting global risks of all sorts, I believe we haven't even seen the worst of the economic downturn yet.

Does a sustainable recovery in house prices lie in the future? Of course it does. In the meantime and for the sake of ones financial wellbeing, best try keep it real....

And when the doom merchants' steadfast predictions are wrong, wrong, and wrong again, and they see that the crash they bay for accompanies a wave of greater human misery than just the over leveraged.....

They eventually adopt a moderate, less eager stance.

Remember back half a dozen years or so when ol’ Poppy used to encourage a purchase due to the clearly positive conditions sitting just on the horizon?

Only been on the forum for 6 months or so, but RP has held strong to his conviction of an ongoing downturn in the face of modest climbs. Time will tell I guess.

Just curious, did RP or anyone on here correctly call the peak and encouraged selling in late 2021?

1689 Baptist, perhaps you're not asking the right question. Did anyone predict a global pandemic and the extraordinary efforts that would be taken in order to protect the financial system from complete meltdown? This is what added even more froth....

I cannot imagine how anyone sane could honestly believe the market could keep rising post Nov-21. It was not a hard prediction to make.

you called the peak at Nov 2021 did you?

David Chaston called it here

Considering the pandemic hit NZ start of 2020 and the government at the time spurred on a massive increase in property values yeah that was pretty bad time to sell when the pandemic hit, or when productive jobs got paused and massive credit was released to the banks for property speculation. But yeah more than 2 years after covid 2019 when the easy credit was drying up (spurred on by govt lending condition policies). Yep completely unpredictable (except all those months of select committee hearings and press releases on the difficulty of lending capital and the conditions making it more limiting to buy). Ironically property values have still not decreased back to where they were at 2019. If you brought before and sold now you would still be making bank far more then if you had a working income at the time (note: you would get less profit then if you sold at the peak but it would still be significantly profitable, only those wildly overvalued of which there were shtboxes dropped near the peak which sold for massive speculative gains then would be closer to their value at 2018-2019). Much of NZ housing is far removed from actual building value and it has been a speculative market for some time.

Few called a peak, even less identified low interest rates were going away, and why.

The future is fairly hard to predict with any degree of accuracy. Some things take longer to play out, and some things happen that aren't factors of consideration.

But a bunch of other stuff, fairly predictable.

Planter

"Few called a peak, even less identified low interest rates were going away, and why."

I am going to put my hand up.

“by printer8 | 18th Dec 20, 9:19am

Clearly the current rate of housing inflation is unsustainable . . . “

I repeated the same comment on numerous times such as on 27 April 21 and 31 May 21.

Also, over the same period in 2021, I was also calling BNZ 2.99% five-year mortgage as attractive and wouldn't last and would give some assurance.

"by printer8 | 5th May 21, 2:52pm

Indications are for upward pressure on longer term rates.

I’m not surprised by this: over the past few weeks I have been posting that the BNZ 5 year rate of 2.99% was competitive and wouldn’t last."

I do not claim to be clever or a clairvoyant; it’s just that unlike many on this site outright rubbishing RBNZ, a range of both bank other economists and other commentators, I take note of their differing comments to come to a conclusion.

Those who who outright rubbish RBNZ, bank and other economists and commentators have over-inflated egos and sadly simply undermine the validity of the whole comments section.

Very well done P8 !

Great job! And very well said at the end.

The fact you think calling a mortgage rate as good denotes you have any special inherent skill is pretty sad. The way you attack any valid criticism & critique of inequitable policies as "undermining the validity" of discourse is pretty shameful in a democracy. I would expect that sort of attitude in a authoritarian or totalitarian state but not in a democracy of diverse viewpoints with diverse experiences.

A stopped clock is right twice a day. Any clueless sap could see a 5 year rate at 2.99% would have been good, especially with the conditions in front of them that were well signaled at the time (I.E. the RBNZ & govt acting against the economic interests of NZ and the people esp to increase cost of living inflation in big ways). I did not comment on it as I own outright without mortgage and since we were starting a multi property charitable development we did not need to get bank funding (in fact neither would the benefactors of the properties either). Our interest has always been in maintaining the investment capital and resourcing products from outside of NZ. Investment & shipping rates & consent time frames had more influence to us, with 3 years waiting on the generational council plan from 2018 to come in and 2 years for consents to be processed.

But I guess charitable endeavours for the benefit of fellow humans is a far remote activity to those on most of this forum and those in the RBNZ. Consideration on beneficial productivity, economic and living conditions for those in NZ is in short supply with RBNZ employees. Who would eat their own grandmothers pension and steal her home from underneath her.

Hard to pick a peak ahead of it happening. But easy to see it in the past.

I would say it peaked near a couple of years ago. Some here can't see that.

I wasn't here late 2021 but sold my house in Feb 2022 (with the clear intention of waiting for the crash and buy again later). I got the intel from the finance guys of my company (people should always listen to those guys, they don't work for the bank, they don't have anything to sell). Been renting since then. Could buy back my former house for 20/25% less and while I've spent around 100k in rent over the past 2 years I'm still several 100k positive.

That's putting your money where your mouth is!

"Could buy back my former house for 20/25% less and while I've spent around 100k in rent over the past 2 years I'm still several 100k positive."

What the property promoters don't want people to know

Here are the respective cashflows for Feb 2022 buyer and a buyer in Feb 2024 (BT)

1) Feb 2022

a) Feb 2022 buyer (Peaker):

REINZ median house price for Auckland: $1,190,000

i)

Equity of 20%: $238,000

Mortgage: $952,000 (80% LVR)

1 year mortgage interest rate: 3.61% p.a

Mortgage payment: P&I 30 years: $52,477

ii) Rates, insurance: say $4,760

iii) Total payment $57,237

b) Buyer in Feb 2024 rents until Feb 2024:

i) Rental per year $32,084 (2.7% gross rental yield on Peaker's purchase price of $1,190,000)

ii) Saves: $25,153 (this can be added to their deposit)

iii) Total payment: $57,237 (same cashflow as Feb 2022 buyer )

2) At Feb 2024

a) Feb 2022 buyer

i) Mortgage: $922,072 (reduced due to principal payments)

1 year mortgage interest rate: 7.29% p.a

Mortgage payment: P&I 28 years: $78,139 (increase of 49% from 2022 payments)

ii) Rates insurance: say $5,050 (due to inflation)

iii) Total payment: $83,189 (this assumes that the Feb 2022 buyer can continue to hold on - in many cases the increase in payment may be too much of a burden on household cashflows and need to sell (and realise their loss of savings used as an equity deposit)

b) Buyer today

i)

House price 20% lower as stated above: $952,000

Equity: $304,500 (made up of $238,000 above plus savings of $25,153 above for 12 months to Feb 2023, and savings of $41,437 for 12 months to Feb 2024)

Mortgage: $647,500

1 year mortgage interest rate: 7.34% p.a

Mortgage payment: P&I 30 years: $54,511

ii) Rates insurance: say $5,050 (same as for Peaker)

Total payment for housing: $59,560

iii) Additional amount to reduce mortgage principal: $23,629

iv) Total payment: $83,189 (same cashflow as Feb 2022 buyer)

Also the equity position of

1) the Feb 2022 buyer today:

House price: $952,000

Original Mortgage: $952,000 (assumed to be interest only for sake of comparison)

Equity: ZERO - that is effectively 100% loss on their original equity.

2) the Buyer today

Equity: $304,500 (made up of $238,000 above plus savings of $25,153 above for 12 months to Feb 2023, and savings of $41,437 for 12 months to Feb 2024)

This is the reason that SND is several hundreds of thousand dollars positive relative to the Feb 2022 buyer.

Due to the large mortgage and interest on that mortgage, Peaker will pay more for the same house.

The buyer of Feb 2022, could have $1,055,000 in savings to be used in retirement in 2052 (30 years after 2022), that Peaker will not have (they used this money to pay for the higher mortgage and interest on that.

To all owner occupier buyers:

Property promoters will always tell you to act today due to their vested financial selfish interest

When house price risks are high in the market, that is the equivalent of walking in front of a fast moving car. It is better to wait until the life threatening danger has passed before moving.

The property promoter doesn't see or care about the approaching fast moving car (and potentially life threatening danger to owner occupier buyers). The property promoter is primarily focused and concerned with receiving their toll which owner occupier buyers only pay if they choose to cross the road. Many property promoters will tell you that there is no danger in crossing the road. Owner occupier buyer's safety is the last thing on their mind. If you're an owner occupier buyer, your safety should be the first thing on your mind.

CAVEAT EMPTOR

HUH? 😕Pa1nter, your post is confusing.......

If you're confused, maybe.

The people hyping up a property crash for years on here (and also trying to predict when it's going to occur).

Have only just started identifying what else will likely need occur at the same time.

It's now fairly evident, that the common person unfortunately takes a beating first.

The "common person" has been taking a beating for years by forever chasing the home ownership dream only to be scuttled at every turn by self serving speculators supported by government policy that thinks forever rising house prices equals a healthy, happy population. Reality is the wealthy get wealthier and the "common" folk miss out and move to Australia. As for the "common" folk still here, if by some miracle house prices fell enough for them to buy a home to secure their future, I don't think they would give a s#@t what comes with that.

We're seeing a fairly typical squeeze of those closer to the margins, while those with assets will likely further consolidate their position.

So like, I get that the system sucks, and have done for a fairly long time. But the system currently is as such, that the sort of down market that allows the common person to pick up discounted assets, is going to have most common folk in less of a position to, than in more regular times.

Hence, despite plateaued pricing, actual affordability worsens, not improves.

So assuming no one's putting their hand up to change anything, understanding how this system works, is infinitely more prudent than lamenting it.

Or, just move to Australia and live in the same system, in a different geographic location.

Ultimately, turning housing into a welfare scheme for older folk who received affordable housing is expensive and causes a lot of misery, yes.

No inheritance or death taxes in N'Zee. Does well for the children too.

Well, that is if, you think we need a new aristocracy.

The envy is strong with this one.

Shrieks of "envy!" are always ironic

I come from a family where my parents would be in the top 5%.

Envy? Nope.

But I do have a keen sense of what is fair.

Socialist quite right you are

Rates staying high is slowly compressing the housing market.

Vendors are slow to react and will feel the pinch with every day that passes

Stock levels are increasing going into winter, when it's usually the other way around

Rates staying high is slowly compressing the housing market.

Vendors are slow to react and will feel the pinch with every day that passes

Stock levels are increasing going into winter, when it's usually the other way around

That double post got me going but then I realise its just your wicked sense of humour Yvil

WOW - a Realist and Spruiker agree? Incredible!

Perhaps we could have peace return to the world and endless wars, end??

No - walking on water is more likely that wars stopping.......

Oil and Gold spiking again. All harbingers for instability and a continuation of the NZ Housing Ponzie/REA Scamsters circling the drain.

Would be buyers - walk away unless you are getting a 25 to 40% discount on the asking price and CV

Housing Market confidence is shattered and hanging by a thread!

Don't be the Real Estate Agents Useful (Buying) idiot!

I would rate this as your most intellectual post

Yvil feeling deep down his upvote wasn't enough,

Thanks D.

I do realise it's a fine line between Intellectual/Genius and a complete Nutbag:)

- I navigate this line with difficulty and Yet ......occasional finesse.

Anyhooooo.........as the old saying goes "may we live in interesting times"

- We are currently at so many positive and potentially life/planet threatening intersections, with so many Nation States with their existential backs against the wall or last defending bulwark......

Expect the unexpected and fireworks in the next 8 months of 2024!

Inflation to Roar Back is a dead cert now!

The world is at an inflection point, when a speculator joins forces with a realist

I thought he was just remotely accessing your clipboard.

Dumb thought

I just wanted to have a bit of fun with the children… They didn't disappoint !

Whatever you say grandpa, even though you were the one that acted like a child reposting my post

See... my point exactly. No creativity or intellect in the reply, just proof of being basic and childish.

Isn't it past your bedtime grandpa

Since you edited your last post, possibly realising it was childish, I will copy and paste your latest one here.

"Isn't it past your bedtime grandpa"

So that is your best attempt at showing that you're not childish, but creative and smart ?

Grandpa do you need medical attention? You seem very perturbed

Love the flirting. What did you get each other for Valentines Day?

You seem to be jealous.. You can have Yvil to yourself..

Well spotted Hugh, we got each other nappies, because DGM can't yet make it through the night without them, and I'm so old that I need them again !

GM grandpa, reminder to take your pills

Maybe you need your Ritalin

Ah, explains your eccentric behavior.. share some with Yvil

Wikipedia: What Are the Signs of childishness and Emotional Immaturity?

Blaming others when things go wrong.

Lying to get out of uncomfortable situations or conversations.

Name-calling during conflicts.

Inability to control one's impulses, such as engaging in reckless behaviors.

Needing to be the center of attention at all times.

Wow.. for once you are honest and listed all of your characteristics..

Good on you grandpa

Sorry I'm going to have to leave you, I'm going out on the boat shortly. Have fun DGM, and enjoy your day !

Good on you Yvil, very succinct.

Most OO do not list a house to test the market, they want a sale. the stock building up will need to lower price to acheive that sale, there is no way buyers are going to chase this market. Sales will clear about 10% lower.

Ask a few REs they all say bid is 10% lower

In recent months I have sold one house for 4% lower than asking price, and I sold another for 1% more than asking price.

It would be interesting to hear from other commenters who have bought or sold in recent months as to what % up or down they settled on.

"In recent months I have sold one house for 4% lower than asking price, and I sold another for 1% more than asking price"

Trying to understand your decision making framework. What was the reasoning behind selling the properties?

With so much uncertainty in the housing market, and many predicting further drops in prices, plus wanting to reduce debt, it was the most pragmatic choice to make at the time.

I sold a house in West Harbour in August last year for $1.3m, CV $1.46m, but needed a lot of TLC.

A house over the road from where I currently live just sold for $300k more than CV.

Prices have come back, but those that waffle on about a crash are dreaming. I'm building out near Riverhead, new subdivisions have all sold. Currently one section available in the area.

I remember when they were starting the massive developments in Riverhead and we came right as a couple tourist buses were being shown through the showroom properties with 5 very chuffed translator realestate agents (we were inspecting more recent building materials and practices that would have been used for those properties). In discussion we found out they had sold most the properties off the plans without a peg in the ground yet.

People say you cannot buy from overseas but that is very untrue and it is easy to set up a company with local agents. It is also why much of NZs property market can be influenced by overseas investment markets as well. However there is a significant local investment market as well.

Another development on the way in Riverhead in addition to the ones I've previously mentioned. In the local rag, 51 units have been approved in central Riverhead.

I agree the market is not crashing. It is just drifting back as annual inflation bites into values. This will continue until inflation drops and interest rates start to gradually pull back. That will be late this year at the earliest as inflation is still too high. Rates , insurance , fuel and food costs are currently scary and some will get scarier. I look forward to seeing those entering the market for the first time getting a break.

Good quality properties and land are still selling for a premium. They always will, it's the rubbish that will suffer.

Not where I live which is a North Island provincial capital. Premium is especially not selling as people cannot afford or get the finance needed. Anything above $1.5 not selling. Some have been on the market for two years or more. Some have dropped their prices but still not selling. Vendors will need to reduce to levels that would give them nightmares. This will get worse during winter as they don’t look so premium then. You would have to think there are some very frustrated and frightened vendors out there currently and not just where I live.

Yes buyers should only offer 25 to 50% below CVs.......otherwise they will be holding the bag as values sag and inflation stays high!

Auckland property prices rose 3.72% in the year to Feb. So much for the great crash predicted here hundreds of times.

So a loss against inflation then!

It ain't a crash is it? And I've had 2 neighbours sell recently. One $300k above CV.

Crash...what a load of codswallop.

Who is using the word crash?

The general definition of 'crash' is a plunge of 20% or more. There's plenty of posters here who think the market will plunge more than that.

Dreamers......it ain't plunging around here.

Obviously the thought that your property is increasing in value is your blanky. Personally I could not give a toss whether my home is increasing in value or not. What makes me very happy is spending lots of time with my children and grandchildren. Also that they and their friends and relations can get on the ladder without any stupid ten times loans. Personally I have made sure my children have very little or no house debt at all. Like you buying a home was not a struggle compared to today.

IMO the best time to buy a house was 1993, ... the 87 crash had finally ended, was before big price appreciation, mortgage interest rates had fallen from high double figures to mid single figures

Bought the house I am in still in 1996 for $490k. Agents say it is worth $3m today. That’s nuts. That’s not fair. Those getting on the ladder today will not have the same luck as myself. Us boomers have been lucky and some of us have been very greedy and bought more rentals than we will ever need. Just because we could does not mean we should have.

How many rentals are you the landlord for. I know my LL owns a few

I would rather watch trains.

And in recent years the taxpayer has supported property to a huge degree to protect and enlarge that wealth. We're pouring welfare into property while folk rant about the poor.

That doesn't mean much without context though does it...what did you set your asking price based on?

It was an auction, it was my late mother's house which was required to be sold under the conditions of her will. I built it for her many years ago, the original cost was $140k, including land. We advertised it as... 'deceased estate, must sell'. The interest was massive.

The house was packed with people and there was lots of bidding.

@DMC45 listing prices based on sale prices of similar properties in the same area.

What has your experience been of selling in recent months?

As I mentioned, one neighbour sold for $300k over CV, another neighbour has just sold, it hasn't reached settlement date, so I don't know, and he's not saying, but I'm certain it will be well above CV.

I bought by tender in May. At the time, very few of the houses I was looking at had an asking price. It was bloody annoying.

Sold one new build at 3.8% below my advertised price; second new build at almost exactly the same % above my advertised price

I believe the market still has a fair way to fall, maybe 10%+. But sometimes circumstances are more important than trying to time the market, which is why I bought a place in Ak last week after a couple of months of looking. For a good price, half way between 2014 and 2017 CV, or 21% below 2021 CV. My experience was that many vendors, primed by agents, are being completely unrealistic and thus not selling. But there are some who are more realistic, and an increasing number who need urgent sales

I sold 800 sq m in Nov 21 and then purchased 157,000 sq m for same money...... deal of the century as can subdivide.... the purchaser is living in that house now, which must be hard as it was rotting with a shower curtain..... anyway their problem that they cannot finance a development now. Making it worse they bought it sight unseen just photos..... so some of us saw things happening back then........

Are you drunk ?

Takes one to know one

IT Guy is just saying he sold a full sized section in a city and then bought a 40 acre block in the countryside somewhere for the same money. It's not really comparing like for like though.

If it takes 45 mins on a good day to get home, never mind

IT Guy WFH 3 days a week and in Takapuna 2 days......

Remember the old saying that house prices double every 10 years?

Well, at this time, it is utter rubbish.

To double in 10 years requires a gross per annum rate of return of roughly 7.2%. (Rule of 72.)

Of all the auctions I'm monitoring, the vast majority are getting a gross per annum rate of return of between 5% and 2%. (I'm looking at the recent auction price and going back to the previous sale, and from the difference calculating the gross p.a. r.o.r.) Even some with complete makeovers and significant selling costs like staging are only getting returns in this range. (Usually down to the 3 rules of property.)

Anyway - those getting the upper gross p.a. r.o.r. percentages - of about 5.5% - bought around 2010/2011.

CN can tell you why. ;-)

Also, incomes don't double every 10 years, so while it did happen it was just the balloon getting bigger and bigger.

Google NZ property "double every 10 years" and behold the rogues' gallery

Your right Chris. With affordability as it is, I doubt I'm going to average 3% c.g. let alone 7.2% in the next five years with my portfolio. On the counter, rents are rising fast.

Anyone making a certain statement in an investment market built on top of earthquake fault lines is clearly selling something. But it is those who take their statements seriously which are equally as bad.

It does not need to be refuted at all because no one should believe in certainty in investment. Esp with housing being more susceptible to weather & natural events then many other investments that housing has an entire insurance market solely dedicated to it.

The new 2024 RV's are out down here and they are down across the board so expect to see the number selling above RV to increase significantly. One area took a dive by 11%.

Agents will hail more selling above CV as a sign the market is starting to boom again….

So much the for the great kiwi housing crash...

https://www.stuff.co.nz/money/350234789/barfoot-log-jam-breached-auckla…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.