‘Since 1999, house prices have risen over 400 percent, more than twice as fast as average incomes.’

So spoke the Australian Treasurer Jim Chalmers in his recent budget speech. He might have added that the figure is closer to 500% in some capital cities.

Chalmers was spruiking major tax changes in his budget to address housing unaffordability which his government identifies as a cause of serious intergenerational inequity.

The thrust of his strategy is to remove two tax concessions that he believes favour investor landlords to the detriment of first home buyers. The first is negative gearing – the ability to offset property losses against other income – and the second is the 50% discount on gains currently allowed when calculating capital gains tax.

For good measure the Treasurer also wants to introduce a minimum 30% tax rate on capital gains.

The proposed reforms are subject to certain exceptions for residential property already owned and future acquisitions of new housing. Nevertheless, if enacted, the reforms will represent a dramatic change to the economics of investing in the housing sector.

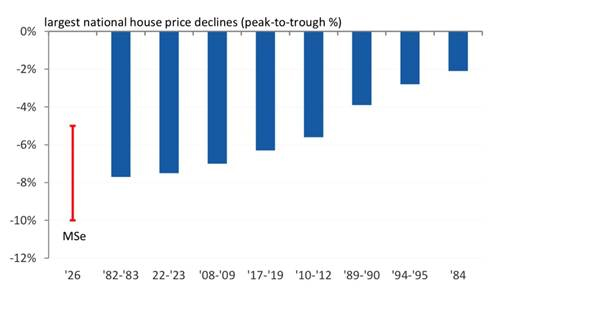

Just how dramatic is highlighted in a comprehensive analysis by the research team at Morgan Stanley Australia. It expects house prices to fall between 5 and 10%. That would constitute ‘one of the largest price corrections over the past 40 years’.

Source: Morgan Stanley Australia

SQM Research is forecasting falls of up to 9% in Sydney and 7% in Melbourne because those are the markets most exposed to investors.

But not all commentators are that pessimistic.

Westpac expects investor activity in the residential market to fall by 34% in the near-term and for total housing market turnover to decline 20% – not a great outcome for real estate agents and lenders to investors.

However, the bank forecasts house price growth ‘to stall flat on average across the major capital cities’ rather than turn negative. Different markets will have different outcomes with Westpac seeing falls of 3 to 4% in Sydney and Melbourne in 2026 but rises in Perth and Brisbane.

Significantly, Morgan Stanley estimates that ‘a 15-20% decline would be required to fully restore investor economics’ to the position pre-Budget i.e. to make investing in residential rental property as attractive as it was previously.

No leading market commentator is predicting house price falls of that severity. Therefore, if Morgan Stanley is correct, the golden days of investing in rental housing in Australia are over.

It’s the end of what Morgan Stanley calls a 30-year housing ‘super cycle’.

This is momentous given that for decades residential rental property has been a long-term source of wealth creation for many Australians. According to 2025 figures from Property Update, more than 2.2 million homes, roughly 22%, are owned by investors.

And it’s not just the budget changes that are weighing on Australian house prices. A challenging environment had emerged before the budget thanks to rising interest rates, rising inflation, and economic uncertainty attributable to the Iran crisis.

The Reserve Bank of Australia has increased the cash rate by 0.25% on three occasions in 2026, most recently the week before the budget. That has quickly flowed through to higher bank lending rates which in turn has reduced the borrowing capacity of most borrowers.

Until recently at least one further RBA rate hike was anticipated in the short term. However, that risk has lessened over the last fortnight due to a drop in the Consumer Price Index from 4.6% to 4.2% and a rise in the unemployment rate from 4.3% to 4.5%.

But that interest rate reprieve is only expected to be temporary, and it will do little to assuage the general sense of gloom permeating the housing market and the wider economy.

According to some commentary in the Australian press, the latest budget may have implications for New Zealand. Faced with higher taxes on residential property investment at home, the suggestion is that some Aussie investors might look offshore to jurisdictions with less onerous tax rules.

Jurisdictions like New Zealand – a capital gains tax-free zone.

See for example the article in the Australian Financial Review entitled ‘Property investors may be tempted by UAE, New Zealand’.

And the issue goes beyond residential property. The budget’s proposed removal of the 50% discount for calculating capital gains will apply to all assets including shares and unit trusts. This has led to widespread criticism and claims that the change will drive some Australian entrepreneurs offshore to friendlier tax climes.

The Australian ran a piece headed ‘Australia risks business exodus to New Zealand’.

An exodus seems unlikely but even before the latest budget there were stories of investors in high growth Australian startups moving to Queenstown before new funding rounds produced massive capital appreciation.

There are clearly significant potential tax benefits if you can satisfy the relevant tax residence rules.

And you want to live in New Zealand.

*Ross Stitt is a freelance writer with a PhD in political science. He is a New Zealander based in Sydney. His articles are part of our 'Understanding Australia' series.

14 Comments

As we know only too well in NZ, with our insanity laced, overbidding of property upto 2021.....

This is the charting future, for our Cobbers over the ditch:

https://fred.stlouisfed.org/series/QNZR628BIS

"Fair go mate", they will cry, as their market implodes.....and goes the way of all Property Ponzis, Downburgers.

The future is important to consider and prepare for, as best we can, and should be understood - as will we all see 2005 prices again soon? - as our big export partner, China, now stare gauntly into, as their reality:

https://fred.stlouisfed.org/series/QCNR628BIS

Likely much.

This is the charting future, for our Cobbers over the ditch:

https://fred.stlouisfed.org/series/QNZR628BIS

Here's a better chart for you Gecks. Aussie broad money supply growth has been off the hook. Where does that money supply come from? Issuance of mortgage debt by commercial banks,

https://fred.stlouisfed.org/series/BRDMNYAUM189N

The RBA admits that household credit (dominated by housing/mortgage lending) is the largest segment of total credit, and its growth has historically tracked broad money growth reasonably closely. In practice, periods of strong mortgage lending (e.g., housing booms) tend to line up with stronger growth in broad money.

Pray tell what occurs, in the Aussie Fair Go Diggers and Gamblers housing market, when the supply of forevermore Broad Money Mortgage flow, even slows or holds steady, for a few years?

Look out below, for a few years????

Now you looking to me for answers. And I cannot tell you. I do know that But Team Albo has been throwing out trinkets in the form of gov guarantees for young people with 5% deposits.

APRA have previously said that loans with a 95% value ratio are high-risk. The govt scheme encourages this behaviour. APRA admitted that high-ratio lending is "more risky" and they are watching it closely. What if property prices drop by 10 or 20%? If people fall into negative equity, the taxpayer is underwriting a huge chunk of those losses.

APRA says they have confirmed that they’ll expect banks to hold the same amount of capital against these loans as any other high-risk product.

Seems to me that the Aussie ruling elite are all over the shop when it comes to their Ponzi.

AFR

Hayson, says a gulf has opened up between buyers and sellers, with vendors still wedded to the expectations they had for prices before the budget tax proposals changed everything.

“Sentiment controls the market. There’s no question, we are now in a cycle that is a buyer’s market,” Hayson says. “We’ve got a massive disconnect right now. You’ve got sellers that are holding onto prices that [they] might have [achieved] only six weeks ago.

“They can’t get their head around that the market has dropped. That’s how quickly it happens.”

As NZ sellers can attest to, change of expectations in the face of raw data and sentiment, can take a long time to eventuate. Nobody wants to accept lower prices and the feedback loop of massive capital gain is a hard expectation to shake.

https://www.afr.com/property/residential/weekly-auction-clearance-rates…

More capital city homes failed at auction than sold in the week to Saturday, dragging the clearance rate below 50 per cent for the first time in six years, upcoming Cotality data is expected to show.

While preliminary data published on Sunday showed a 54.5 per cent clearance rate, Cotality’s research director Tim Lawless said the final figure due to be published later this week would likely be revised down. With more results included it is expected to drop to its lowest point since May 2020.

Burn. Their ponzi is even stupider than ours. Thats saying something.

This is Fine!

Add to any CBA shorts

See for example the article in the Australian Financial Review entitled ‘Property investors may be tempted by UAE, New Zealand’.

👉https://archive.is/NtVaM

The past few months should have made it clear that anyone who 'invests' in property in the UAE is bonkers.

Ai overview:

UAE citizens with full political and social rights make up roughly 11% to 15% of the total population (approx. 1.3 to 1.4 million people). The remaining 85% to 89% are expatriates. Exact figures for the socioeconomic sub-groups are not officially published, but demographic and labor data reveals the following breakdown:

*The Precariat (Low-wage laborers): An estimated 50% to 60% of the total population—representing millions of workers, primarily from South and Southeast Asia. They generally face insecurity of tenure, are tied to specific employers under the kafala system, and are employed in construction, domestic work, and low-tier services. There is no universal minimum wage in the UAE.

*Entrepreneurial & Professional Expatriates: Roughly 25% to 30% of the total population. This diverse tier comprises highly skilled corporate workers, business owners, and investors from around the globe, including a prominent but small minority of Western and affluent expatriates.

Does New Zealand really aspire to be the Dubai of the South Pacific?

Why on Earth would Aussie property gamblers, be tempted to buy into NZs 5 year property crash?

Catching a falling knife in NZs market, gets you very bloody, financially cut hands!

Many property pumpers are saying the "market has bottomed" "about to turn" "best time to buy was yesterday"

- This is unbelievable, given it's been the mantra for the last 3 years, (including many transient property gamblers/pumpers/hoarders here) while values have sunk further into the mire.

Study this beauty with "Triple Garaging Home On 1,194m² of Pure Potential" - in Auckland's suburban heartland:

1. The buyer from 2016, would be very lucky to turn a nominal profit dollar, selling in today's crashing market. If an owner/investor, add on holding and mortgage costs, they make a VERY BAD LOSS.

2. They been trying to sell the tired lot for the last 4 years, to no avail.

3. They are now "willing" to now readily accept just -$450,000 below the recent 2024 CV. Shows the 2024 CVs have all crashed in real value since and some, by large amounts. Those paying near current CVs, will take major, future haircuts!

4. However, buyers appear to get a free washing line thrown in, with major side dish of deferred maintenance, dilapidation and significant rates bill.

5. IMHO this beauty would be a buy currently, around 2014 values of around 550k. Paying above, risks a big future of negative equity and bills piling up!

Pure Potential ??? Really??? How can the Land Agent sleep at night?

Yet Rush in Punters!!! Just wear your thick chainmail gloves, to protect from the falling knife cuts!!!

https://www.oneroof.co.nz/property/auckland/massey/21-mcclintock-road/o…

The credit expansion has to come from somewhere...at least Australia typically run a trade surplus.

If we study the massive credit expansion within the less wealthy NZ, it has come from the want of the commercial Banks, Central Bankers and Politicians, to believe it is fine to allow loans to be extended to people, at lunacy levels, of 5x DTIs and higher.

Then to turn another blind eye, to property values rising at rates past 2 or 3%. Which gains past 3%, outpace average wage inflation.

The only destination, with repeated +3% gains, is on course to BUBBLE LAND, then leads to a BUST.

Dont disagree...the point is if you (investors) require/demand a return then the credit expansion is required to be secured against something...if not land/property, what?

We delude ourselves that 'money' represents real resources...the reality is they are not connected other than in our minds.

https://www.afr.com/property/residential/sydney-now-leads-melbourne-in-…

Sydney’s housing values fell faster than those in Melbourne last month, as declines in the NSW capital sped up to 0.9 per cent on the back of higher borrowing costs and weaker consumer confidence and investor activity following last month’s federal budget.

Sydney’s decline in May only just eclipsed Melbourne’s 0.8 per cent fall, but with sales volumes dropping faster and a higher exposure to investor buyers, the NSW capital was set to lead the country’s housing markets down, data provider Cotality said.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.