Barfoot and Thompson, Auckland's largest residential realtor with 40% of the market, reported its strongest January month in four years and said it expected gradual and modest increases in house prices over the first quarter of 2012.

“The average sales price [in January 2012] at NZ$529,768 was up 2.7 percent [from January 2011], sales numbers at 683 were up 21.3 percent and new listings at 1031 were up 15.1 percent," managing director Peter Thompson said.

The average sales price was down by NZ$43,303 from December (see chart below).

Thompson said the month was "an extremely positive start to the year".

“In January we sold more properties in the month than we have since 2007, prices reached their highest average ever for the month, new listings were up 15.1 percent and we sold double the number of million dollar homes than we did last January,” Thompson said.

“The seasonal dip in activity that occurs each year as a result of the Christmas, New Year and annual holiday breaks was present in the trading figures, but on every key measure this January was significantly ahead of that for January last year," he said.

Million dollar sales

Barfoots sold 40 homes in excess of NZ$1 million during the month. Thompson said homes at the top end of the market tend to be quieter than in other months with many buyers and sellers being away on holiday.

"We have not sold that many homes in that price category in a January since the peak year of 2007," he said.

“Homes valued at a million dollars and above are subject to different market drivers than the rest of the market, and we anticipate demand for high end homes to remain strong."

At the end of January Barfoots had 4766 properties listed, Thompson said.

"While 4 percent higher than the number at the end of December, it was the lowest number we have had at this time of the year for four years. Limited choice has been a feature of the market now for the past 7 months,” he said.

The outlook for housing in the first quarter of 2012 was for a continuation of the trading pattern for the last half of 2011, which saw gradual and modest increases in prices with the number of homes sold monthly remaining in a band of between 700 and 900 properties, Thompson said.

“From now until late autumn new listings and sales numbers will build before starting to ease with the approach of winter. Buyers and sellers are taking a measured approach and it will result in the market remaining stable and positive,” he said.

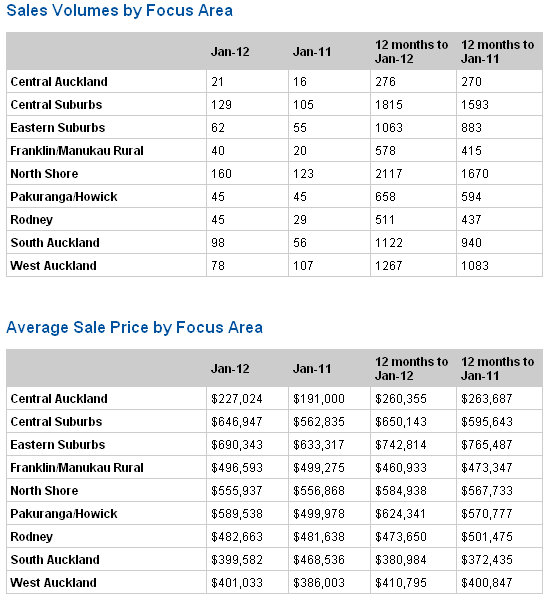

Central Auckland, North Shore lead the way

Figures on the Barfoot and Thompson website show subburbs in Central Auckland and the North Shore led the way in terms of sales in January:

(Updates with comments from Peter Thompson, chart)

Barfoot Auckland

Select chart tabs

28 Comments

Just look at this "Buyer Briefs"

http://www.remuerarealestateregister.co.nz/buyer-briefs

Looks like $1M is the lowest people are willing to spend...

Auck Central has put on 15% in the last year.

Perhaps 15% price inflation in a year implies boom conditions and I should revise my previous prediction of only 8% increase for Central Auck in 2012.

A quiet day on this thread.

Lonely at the top etc.

Your LIM report arrive yet?

Too wet to go the letter box...

Boring... can we talk about Kate and Mike wedding?

yeah,I'm over RE agent reports too

it is in real estates interest to blow their horn regarding rising house prices.

higher the price the more commision we can suck out of a sale.

i want to see a headline that reads 'house prices drop realestate agents not making any money''

Another bunch of parasites on a feeding frenzy.

The ones that didnt make money have all departed.

According to sources who would know (my mother)

"Kate looked like a tranny hooker in that dress."

Which is a bit of an insult to tranny hookers.

..........and Mike's suit looked too big... (or perhaps it was meant to match his head)

No No No! It's not him , it's HER. Check out this photo from the herald.

http://www.nzherald.co.nz/relationships/news/article.cfm?c_id=41&object…

No wonder they kept it a secret, I would be ashamed too. There is something very scary about her overdone clown face. Watched a movie about a demented clown once, but that has nothing on Ms Hawkesby. And people are going to pay to look at MORE photos in a magazine?

It's a sad, sad world we live in!

I spotted her a number of times at New World, Victoria Park.. now you said it, it's not too far from the famous "Picton' street and k Road !!!!

Hey Matt in Auck, have you thought about getting PR?

I had a brief look at the policy and it's not easy as I thought, and the fee is almost 7K for a family application + they will hold some bond money!

I hope the Aus govt is serious about recent announcement.. might also be one of those 'yeah yeah we'll think about it" comment and our govt interpreted as 'yeah yeah they'll do it!"

hey Moa - yeah I think I'll hold out for now, we'll wait and see.

SK you must have a thick skin to be able to enjoy talking about capital gains in housing and putting up your rents as it only adds misery to people who are less fortunate than yourself. How are your children (if you have any) and their friends going to be able to get on the property ladder? No wonder so many are off to Perth to work in the mines ( some to just pay off their student debt ) as incomes are pathetic in New Zealand for the majority. Something will have to give at some stage. If property prices and rents do not adjust to levels where the average New Zealand working family can afford them and also be in a position to meet their daily living expenses more and more people will move to Australia. Of course not all will make it but there are a lot of New Zealanders doing very well over there.

I wonder whether you are a typical New Zealander who puts all their eggs in one basket. Look at the US sharemarket which is back to its highs in the last twelve months. Buying Apple at US$331 last year and building up numbers on dips has been a very good investment. If and when the NZ dollar drops will only add to the gains.Makes your 15% look light especially when one looks at your expenses including depreciation. No tenants to consider. They just want to look after your property just like it is their own as they really appreciate what you do for them. They really love getting your annual increases as it means you are thinking about them and everyone loves that.

You must not let SK get beneath the skin exA...SK is only doing what National English and Key want done....we are entering the era of the tenant serf..the landlord and the bank Kings....

A system structured around cheap credit available to landlords to chase renter property and raise values beyond the saving ceilings of the serfs...with rent supplements (subsidies) paid over to landlords by a compliant govt..which are funded by borrowing and go to boost the landlords drive to buy yet more rental property.....

It will fall flat on its face the day Shearer escapes from his useless political advisors and recognises the need to bugger the landlords and the banks with promised laws aimed at an end to the rort. Termination of supplements with legal protection for tenants who cannot be evicted and need only pay the rent they were paying...minus the supplement!....at a stroke of the pen, Shearer would slash the staff in winz who work hard to keep the supplement system going...but he would also smash the property values of the rentals...driving them down to the level where income poor kiwi families( that's most of them) could afford to buy. He would also reduce his fiscal hole by the billion plus a year currently handed over to the landlords.

WAKE UP SHEARER!

The signs are all there- first the "average" folks find it harder and harder to pay their bills and keep the dream alive of homeownership, and they lose to the bank. They are like the bottom of the bucket. As the bottom falls out of the bucket, it pulls down the higher priced markets with it, the ones that depend on the floor of the market, like Auckland.

Case in point- indicators I see- "average" lower middle income properties have higher percentage of mortgagee sales (wage earner lost his job or had hours cut back), same for land sales (who wants to build in an uncertain job market?). As this stock builds up (this stuff doesn't sell quickly- I watch the days on market for "average" properties- and can tell you that the "official" numbers are a pack of lies- "average" houses are sitting longer on the market, because speculators have left the market. Real landlords are paying cash for bargain properties, whereas "average" homes sit, unsold, building inventory on the bank balance sheets. Now there's a statistic you will never see. These are homes families can afford- but they aren't buying because the job market is uncertain.

Why would a real landlord (looking for a high return) buy an "average" property for $400K, to get $400 a week rent, when he can buy for less than $200K and get $350 a week from someone on a rent supplement? The answer is "he wouldn't." So who buys the $400K home, the one without a view, on the wrong side of the street, that needs to be fully updated and insulated, to get near its 2007 value when it was bought? The answer is "the bank," who is forced to take the write down on their balance sheet, and add it to unsold inventory. The same thing happened/continues in the US- why buy a house at 2006 prices when I can buy the one down the street for $50K less? Or rent it for half? "Since my wife just had her hours cut back, I think I'll rent." The overpriced house doesn't sell, and sits on the bank balance sheet, killing the bank slowly. This is what they don't want you to know. Instead you'll hear unicorns and rainbows from the likes of Barfoot's until it becomes obvious to everybody that it's all a lie.

If this country could take the pain and re-direct it's energy into real productivity and exports, then we could have some kind of footing, with an eye to the future. This game playing with property has made all of our collective energy misplaced, and investments unsafe.

Thank you for making my day!! It's just like Downton Abbey aye~ How dramatic :P

As the report above clearly shows- the outcome is always the same. A 10% drop will take a 20% rise to come back to the previous high- what is the foundation of that happening in this country? It only takes a 10% drop to wipe out 20% in gains. That 20% could represent your planned retirement.

Sorry, SK, you don't have a damned thing until you have cash in the bank, after finding a greater fool to buy your property, an even greater fool to approve the loan, pay all fees, and collect your check. A break in any of those steps and you have no money. The buyers can disappear, the bank can stop lending, or you can't sell for enough to cover your fees.

"Equity" is a flightly idea that can get wiped out in a liquidity crisis, that is as plain as day to everyone but you, apparently. Others believe this is exactly what we are in right now. It's called "counter-party risk." Your whole investment strategy lies in your faith of the banking system always being there, and a steady stream of greater fools to pay for your overpriced property. Take away any of those loops in the chain, and now you're BROKE. You can't buy groceries with equity, I'm afraid.

Have a look at the lies promulgated in Canada- now they are creating whole new indexes to justify overpriced property- all lies, as we look back 5 years from now http://worldhousingbubble.blogspot.co.nz/

Here's one better, again I recommend greaterfool.ca as well, this guy is seeing the same, ominous signs in Vancouver I am seeing- commercial vacancies- lots and lots of space for lease to start your new business. What better time to start a business and hire come employees, right? Why are so few starting businesses? These are the people who pay your paychecks so you can pay your mortgage http://vreaa.wordpress.com/category/19-blastradiuspostcards/

Without good paying jobs, your rents, and property investment is levitating on air, waiting for the inevitable.

As the inventory builds for the lower end of the market (lower middle class, bare land), it drags on the upper end (Barfoot's rubbish reports of everlasting prosperity- all lies). We've seen this all before. It ends badly for average, undiversified "homeowners." The outcome is always the same- a reversion to the mean, just like the above report.

WE should take Texas example and raise property taxes. They have no state income tax in Texas? Hugh?

TAXES ON $100,000 APPRAISED VALUE

$1,855.10 Houston

http://www.westurealestate.com/taxes.htm

More

I’m not arguing that Houston collects disproportionately more taxes than other cities do, because I don’t know whether or not they do. I’m not trying to say that Houston is ruthlessly pummeling its citizens with taxes. My point in this post is not that Houstonians are over-taxed in total, merely to examine the significant impact that our property taxes have on the market value of our homes.

This is clearly a major contributor to the list-prices for homes in Texas being lower than in many other states. The ways in which we choose to collect taxes distorts the market, and I find this particular impact to be interesting because I think people are overlooking it when they talk about the “low price” of housing. There are a lot of factors that contribute to the low market price of housing in Houston, and this is a big one.

That’s my one and only point in this article.

http://www.neohouston.com/2009/06/property-taxes-and-home-prices/

As far as I know, Texas has no 'rates' just a State Tax, like GST, on all purchases.

For all you property bubble deniers, this should provide some good thinking material

Debunking the myths of the Australian real estate bubble.

As the Aussie market goes, it drags ours down as well- because most of our lending is dependant on the strength of Aussie banks, whose credit rating were all just downgraded. Or did you not know that? That means higher mortgage payments, in the end.

How does it feel, when buying a "home," to also be paying for another person's retirement fund?..because that's what you are doing. Is it a good idea?... to know that you are buying more than just a house and land? All that Antipodean's know is to pour their money in to "safe as houses" investments, and go neck deep into debt doing it. There it is, plain as day, completely exposed- when you are buying a house you are also funding a person's retirement, knowingly. Does that make sense? Or is it crazy? It's a known fact, as the highest percentage of wealth is in property for Kiwi's and Aussies- absolutely no investment diversification.

t's a good contrarian indicator, as well, when everybody knows something to be absolute fact, it's time to start betting against it, and waiting for the illusion to pass.

When "everybody knows" something to be true, you have what's called a "mania" (as in "maniac") and it's best to run the other way, to beat others to the soon-to-be-crowded exit...and it's better to be a day, month, or year early, than a day late.

I don't buy any of your so-called money making in property right now...it's all based on a pack of lies.

If you have your life savings tied up in property, I think you are crazy, in light of counter arty risk. SK- good luck. Hope you have all of your properties well leveraged as part of your plan, and you learn your lesson, for what is about to happen. If you are fully leveraged, you won't be "owning" your properties much longer, as the bottom falls out of the market, starting with the lower-middle class property, where inventory builds.

When things start getting really bad, that's when the so-called experts blatantly lie. "When things get weird, the weird turn pro." Unbelievable stories become the Lord's word. I think that is what we are seeing now. Outright lies, covered in lipstick, and a nice bow. Good luck with that plan, if you believe it. Olly, too, if you believing putting your investment in his plan. I hope you have years of faith left in you, because you are going to need it, as you babysit property for the bank, until they take it from you. This is one effect of low interest rates- they stay low- until they aren't any more, and the bank then takes back your property. You have no control over it, because you can't control interest rates. So many right now have their whole life tied-up in the FAITH that rates won't rise. If you invest now, you must BELIEVE that they won't go up. That makes you a fool. Faith? Belief? What do these not have in common with religion? Because it certainly has nothing to do with investing wisely, or for the best of all. It places your entire future on something over which you have no control, until the reversion to the mean wipes out your equity.

Have a look in America, where the real estate agents now admit that they fudged their numbers. That's the problem when you have wolves guarding the sheep.

Why don’t you go and do something productive instead of dribbling this unintelligible nonsense all over your keyboard.

We know something good must be happening in the property markets if HAPPY RENTER spends so much time banging on about property.

Perhaps if you did some work Happy Renter rather than typing crud on here - you could change your name to Happy Owner rather than obviously UN-Happy Renter

and I thought the number one rule of buying property was that it shouldn't be an emotional decision :-)

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.