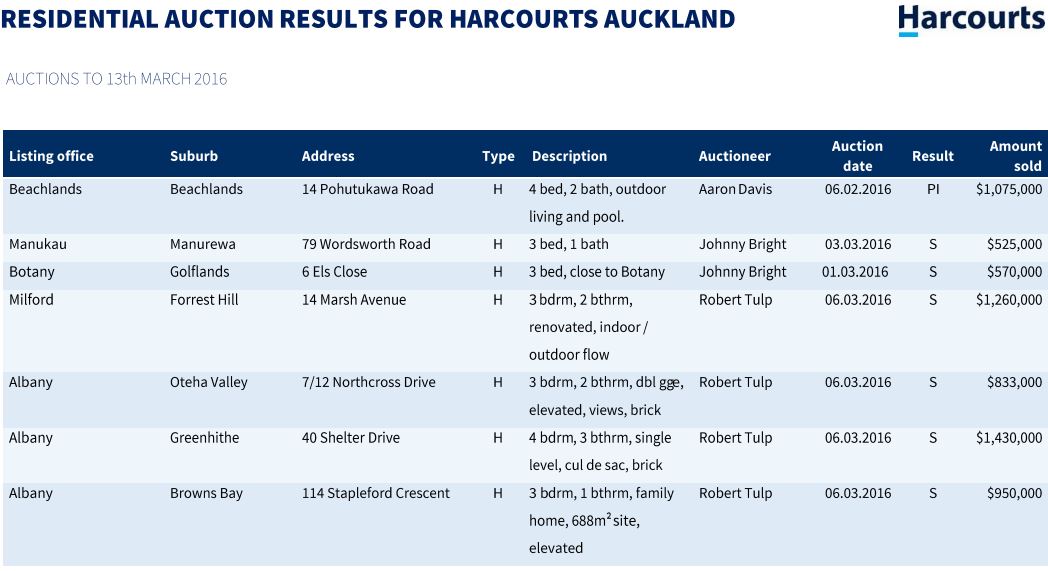

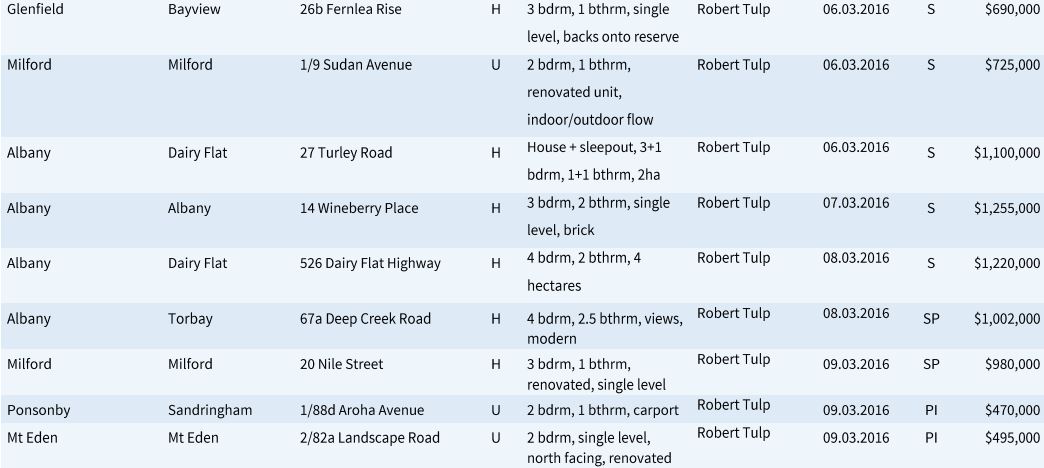

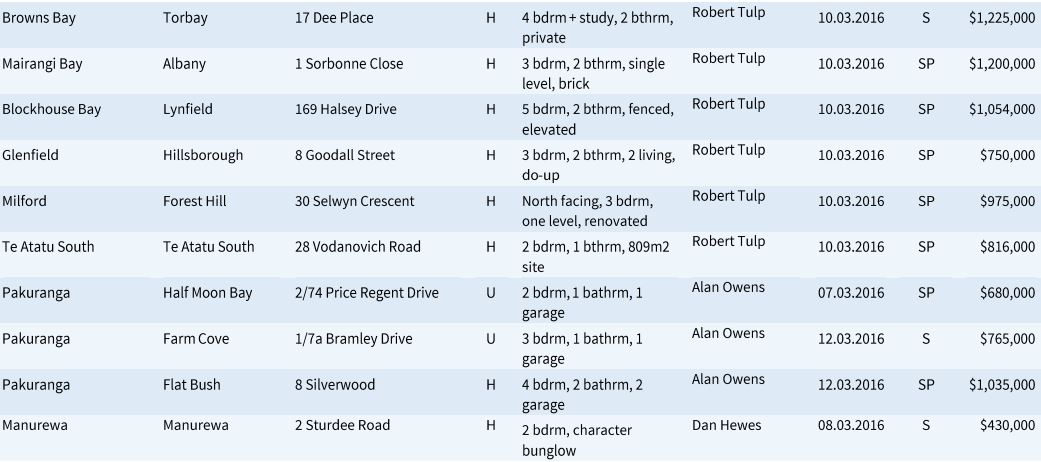

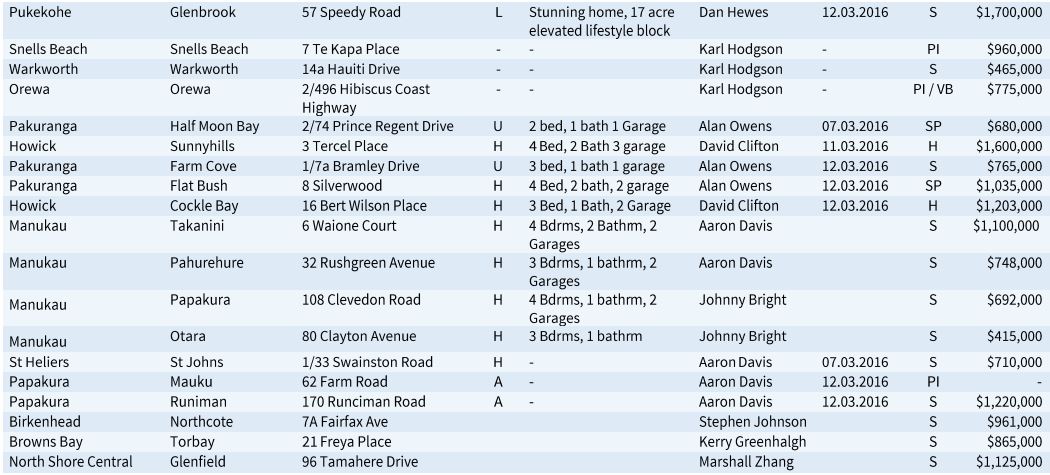

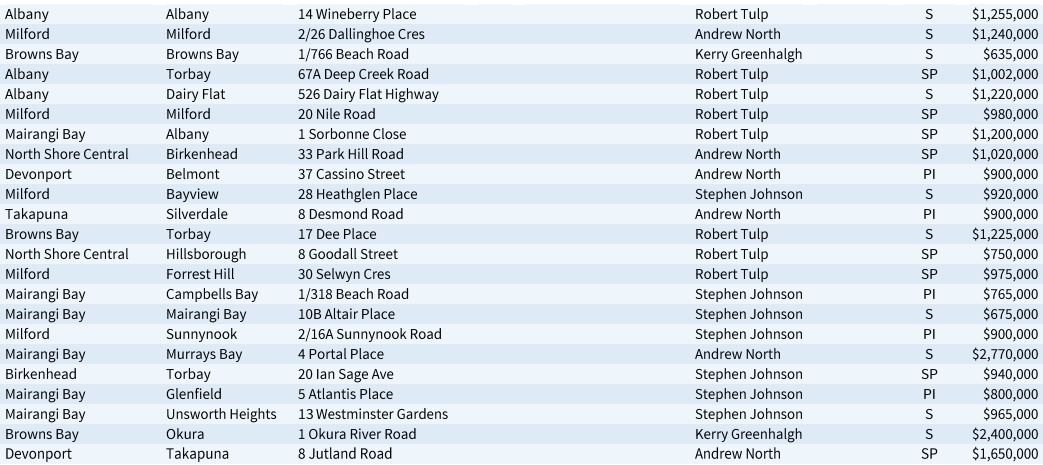

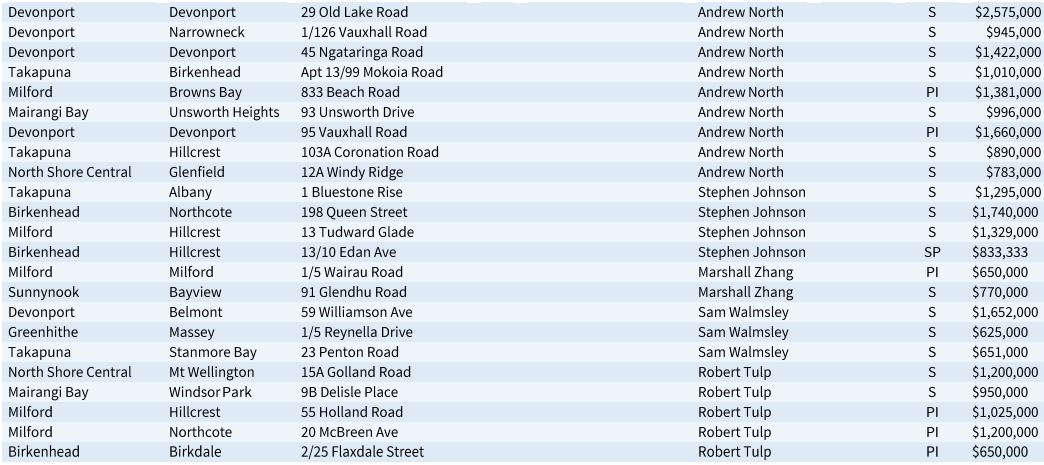

Harcourts sold 72 of 93 auction properties in Auckland last week, giving a clearance rate of 78%.

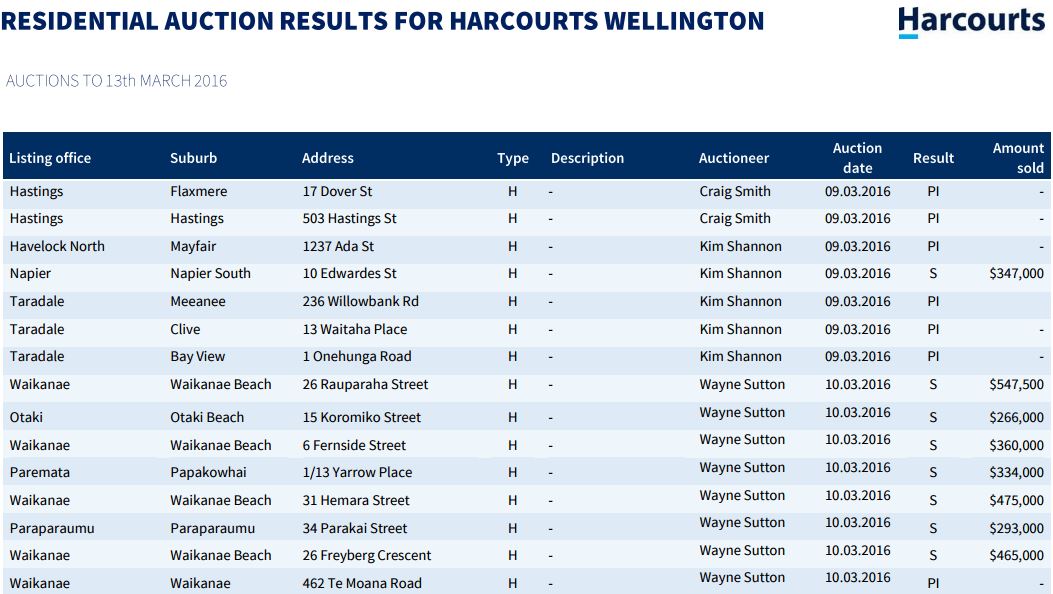

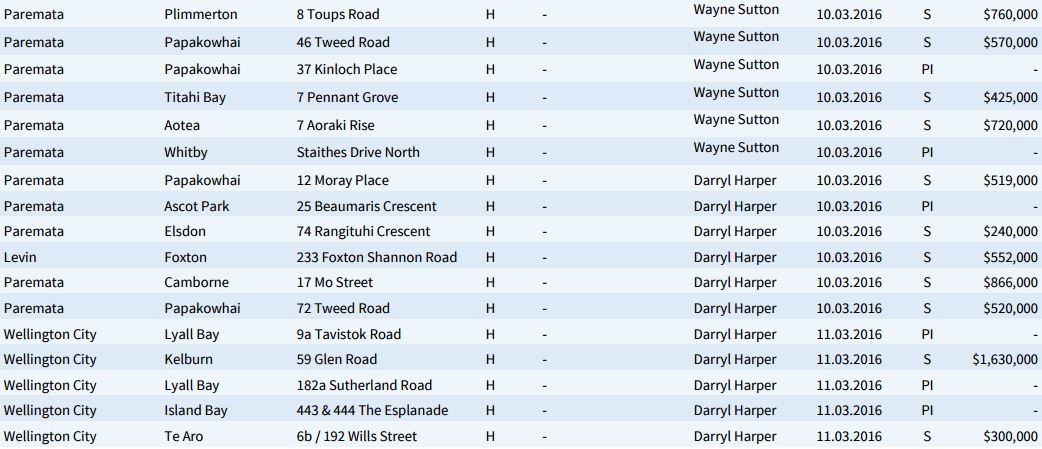

In Hamilton 11 of the 18 auction properties were sold giving a clearance rate of 61% and in Wellington Harcourts sold 19 of 32 auction properties, giving a clearance rate of 60%.

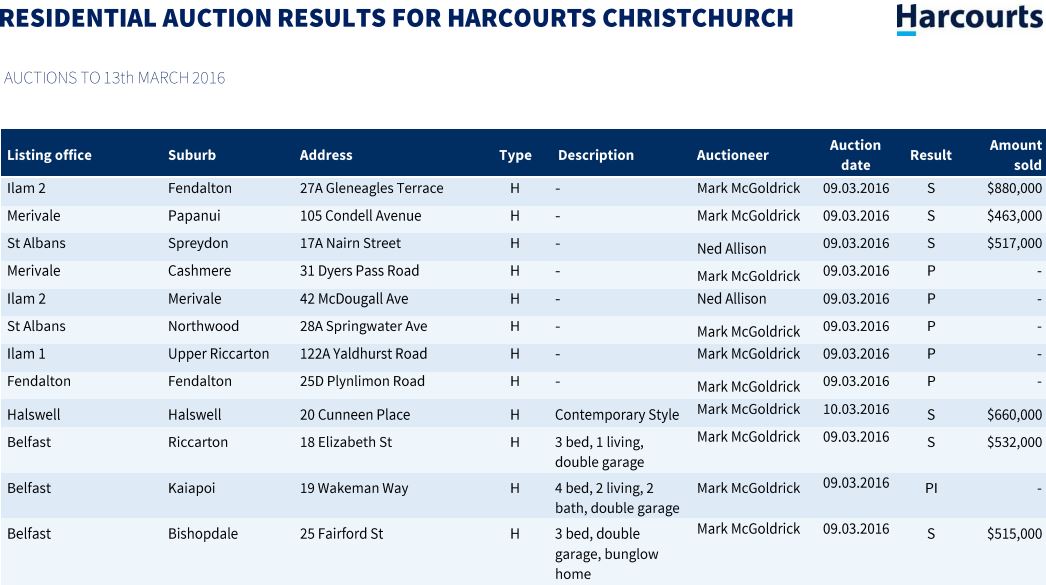

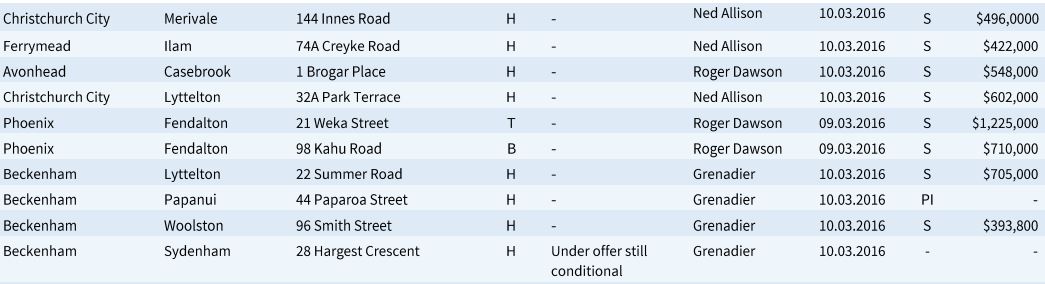

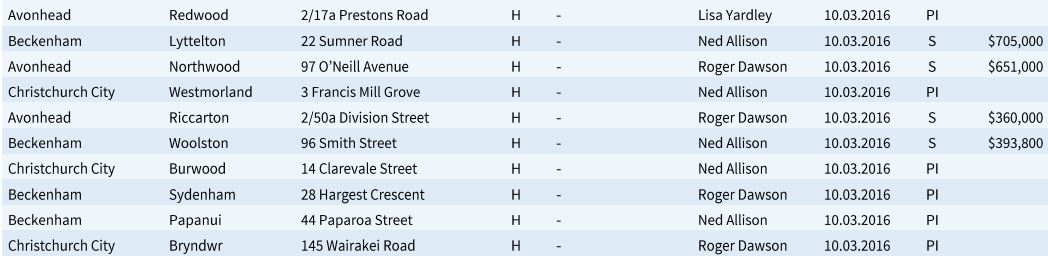

In Christchurch two thirds of the auction properties were sold, with sales achieved on 10 properties and five either passed in, postponed or withdrawn.

See below for the full results of Harcourts auctions in Auckland, Hamilton, Taupo, Wellington and Christchurch last week:

|

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

59 Comments

Hi Greg, are the above Harcourts sales results calculated from 'success under the hammer' at auction, or do they include after auction sales?

The reason I ask is these results seem completely at odds with B&T auction results from last week where for the Bays and Manukau the success rates (under the hammer) ranged between 35% to 39%.

It's all sales, not just under the hammer.

Top price Hamilton lifestyle .

To everyone who has been banging on about the big crash that you believe started during the (usual) Christmas period slowdown. Is this the nightmare scenario playing out?

No it's more like when you go outside and throw a ball in the air. At the top, the ball kinds of looks like its floating there. You admire its ability to hang there. You think, may this time it will stay there or keep going up. But no, sure enough, gravity always wins and it comes crashing back down to earth.

To the best of my knowledge that reasoning, like that metaphor only applies when the scale is very small. For example the moon is a somewhat larger ball that was "thrown" in space and now has a common center of gravity with the earth that is inside the earth nevertheless it doesn't fall to the earth because the earth's gravity isn't the only force acting on it. Similarly there are innumerable forces acting on the residential property market.

Are you saying the Auckland property market is not of this world?

Does this mean one should now invest based on the Lunar Cycle?

Your reasoning is akin to saying that the moon orbits the earth. A much better metaphor would be the Voyager space craft which we threw and periodically we get marginally closer to it because of the elliptical nature of the earth's orbit, but generally it just keeps going further ("up") over the long term.

Lets not forget the failed launches where it blew up killing all on board.

No. I know the ball will come down every time. If I know all the conditions that led to it's upward propulsion I could tell you exactly when it will come down also. Unlike property...

What have you been drinking to to think if you throw a ball in the air it might actually stay there floating?

I haven't been drinking anything, although I think most landlords and speculators have got drunk on debt.

When they wake from their hangovers, they might be able to see clearly.

To use your ball analogy, surely then you're waiting for the ball to drop down and prices to go back to...... when? Should prices go back to 1980s levels where a family home in St Heliers cost you maybe $200k max?. What about 1960s levels where that same home cost $25k? Or perhaps you're waiting for it to go back to the 1930s where you could purchase the equivalent for £1100?

@espirit - back to fundamentals will be fine

What fundamentals?

And why do the chicken lickens not know of these "fundamentals", they must be tired of screaming the sky is falling and looking silly a few months later.

Esprit - Back to when there was some correlation between the average salary and the average house price.

Fine, but what is "some connection"? (I'm not being facetious, I genuinely don't know). I remember back in the '90s, my parents bought a nice home in a nice Hawke's Bay neighbourhood for $137k. Back then as a craftsman plumber, my father was earning about $45,000. Same profession today only probably earns $60,000, which would mean that same house should only be worth $183k. It probably has a market value of three to four times that.

This isn't something that's just happened in the last 3-4 years, this is something that's been going on for the past 30+ years. Despite the peaks and troughs there's been a gentle widening of the gap.

For there to be a correction that you speak of, the Auckland average would need to fall to somewhere like $280k, and short of a financial holocaust affecting the entire world (which would probably see lots of money trying to flow into our little safe haven anyway), I just don't see that happening.

Esprit - There's a huge imbalance and imbalances tend to correct themselves, eventually.

Agree there's an imbalance. What sort of correction will we see? Price consolidation for a number of years while wages start to catch up? (Stagflation), or will it be a slow, gradual decline over 5 years or so. I doubt it'll be the immediate ~60% drop in prices half the people on here seem just dying to see.

Esprit - I don't think there will be a massive drop in prices. I certainly hope there won't be - it could wreck the economy. As I have said previously, I feel sorry for 1st time buyers who felt pressured into buying property in the last few years. A lot of people seem to believe that prices will only go up.

It all comes down to interest rates and the next government.

Shortly before the 1929 crash, economist Irving Fisher famously proclaimed, "Stock prices have reached what looks like a permanently high plateau."

If the ball stays in the air for 6 years can we assume it will stay there for another 6?

Well if it stays in the air for 6 years it must be floating and immune to gravity. It would therefore appear we've mistaken our metaphorical ball for a BUBBLE!

And as we know, BUBBLES always POP. Unless you landlords know of something I don't?

Landlords know that "they" stopped making land a long time ago. Everyone wanting for the "bubble" to pop think land is going to fall out of the sky and make an Auckland 2.0 so they can finally buy something in Remurewa for $100k... Keep thinking that.

So to be clear, you think the property bubbles of Spain, Ireland, Japan and the US all popped because land fell from the sky? Yes, yes, that's right. In all of these countries they extended their borders, added millions of square kilometres to their land masses and as a result their property bubbles burst!! What a joke! Who are you trying to kid?

I ask you this: I assume you're older - you have that I can't be told anything because I'm a baby boomer feel about you. Did you wear bell bottom pants in the 1970's? Did your wife used to have a perm?

Why now do you not wear bell bottom pants, and why doesn't your wife still have a perm?

Why? People went mad for bell bottom pants for a period. They went mad for perms for a period. Right now, Kiwis have gone mad for property. But like our pants and our haircuts, the property fad won't last forever. In 10-20 years time we'll look back and think about property like we do about bell bottom pants and perms and say, 'what the hell was I thinking?' Right now, by the tone of your comments, I can see that you're part of the madness so have limited perspective - you can't see the forest for the trees. More kiwis need to step back, get some perspective on this issue. But they're so involved in it, so wrapped up in the euphoria (which has moved to delusion) that they've lost their common sense. What we're going through isn't normal - but I fear only a bursting of the bubble will wake most kiwis up from their current delusion.

The stuff of nightmares - the future of the property market I mean, not bell bottoms and perms, although they were bad enough.

If AKL property values are the same in 10 years time as they are today I will be happy. They are just too high on any yield/earnings basis. So many times I have heard people say "but it's different this time" but what goes up comes down at some time and the indicators are all on red. What did happen to the commodity supercycle?

I saw people buy property in London in the late 80's with massive mortgages and for many the downturn completely screwed their personal finances for the next 15 years. A lot of people haven't experienced a proper property downturn. Unfortunately it tends to be the young who have taken the excessive risk to get onto the ladder. I feel genuinely sorry for them.

What we're going through isn't normal - but I fear only a bursting of the bubble will wake most kiwis up from their current delusion.

Have u considered that ..."what is not normal"... is an ocean of very cheap Fiat Money... in a Global world.... In the name of "fighting deflation", Central Banks and Govts have abandoned the price stability aspect of Fiat Money... ( AND...this is reflected in , what is, a Global Asset Boom ).

You use terms like ..Bubble...Euphoria.... delusion.... madness..

Do u have any tangible evidence to suggest that this is the Sate of the Property mkt...???

eg... One of my metrics for a "bubble"... is excessive credit growth .. ( In the Mid 2000s' Housing credit was growing at 16% / yr.... In the current cycle its' about 7% ).

What the previous commentaor said about land is true.... Land prices respond differently to the forces of supply/demand ...than most other things..... Thats' what makes locational value such a powerful thing..

Ask a fool whether he's a fool, he'll say he's not. Ask a wise man whether he's wise, he'll also say he's not.

Who's the fool and who is wise?

Do u have any tangible evidence..??? What are u basing your assertions on.??

OR...is this just an .."intuition"...on your part..

OR... Is your metric, simply, home affordability..?? ( eg. house price to income )

Come on... Don't spout riddles about fools and wise men...

Give us something to sink our teeth into...

If you were so sure of your position you wouldn't need my evidence.

Your responses are all the evidence we need.

I suggest you watch "The Big Short" to see why many of those property markets were always going to crash. They bear no resemblance to what is happening in the Auckland market.

You have no evidence for your belief that the Auckland property market is a bubble waiting to burst. Your best reasoning is "what goes up must come down"' something I would expect from a school child.

As to your rant on perms and bell bottoms and trying to draw some analogy to property. I can't even respond to that drivel.

FYI I am not a baby boomer, just a hard working Gen X.

HeavyG - I sincerely hope you have not invested your hard earned money in the Auckland property market in the last few years. If you have, then I am very sorry.

Denial is one of the key distinctions of a society experiencing a bubble. Happens every time. They don't want to face the facts of what could happen next because of greedy behavior in the past.

'They bear no resemblance to what is happening in the Auckland market.' You confuse what has happened with what is going to happen. Very different things.

I can suggest some books if you're interested in reading anything other than the property press?

I don't think anyone can honestly expect 2016 to continue on like 2015 with all this global uncertainty and the effects of dairy starting to pervade into the wider economy (which will eventually be felt by everyone).

Hey we all know that Asia is tightening up on it's capital flight, so property prices here are bound to slow down in the next few months.

Though if there's another OCR cut that will allow FTB's and NZ residents get more of a foot hold on to the property market and it's high time that happened, so we may not have to go through a crash but a slow down. And another reason why it is far better for NZ residents to own property here rather than Over Seas Investors, is that this affects our much larger economy.

When people own their own property rather than just renting, They tend to spend a lot more on maintaining and extending their homes and invest in better quality goods such as; furniture, soft furnishings, electrical goods and general home ware.

They also invest a lot more in their community, setting up businesses etc.. and are less transient then those who just rent.

But unfortunately now that prices are so high, NZ buyers will need to commit most of their spending power paying foreign banks back the debt and won't have much/any money left over to spend in the domestic economy.

There is no silver lining to this story..

The funny thing is - in my circle of friends they are all "arming" themselves with "pre approved mortage certificates" in expectation of the great crash ....... for mainly apartment type investments so i suspect we still have sometime to go until the music stops. so i think "greater sucker theory" still applies.

Arming themselves! Do they treally think they are gonna have to move that fast? I'd suggest this is going to be a long drawn out downward spiral...as the NZ economy adjusts to a new normal. The bounce is a lifetime away.

Hooray! We seem to have reached the "Back to normal" stage of the property bubble.

https://upload.wikimedia.org/wikipedia/commons/4/4b/Stages_of_a_bubble…

{kind=link}

But happy to see more speculators putting the money where their mouth is. Invest, invest in property and become rich. The new paradigm! Property never goes down. Productive economy going down? Interest rates at historically lowest levels? Nah, that means nothing. We should all close down our low returns businesses and borrow more to buy houses.

It's amusing that the only people who say "property never goes down" are the ones predicting (hoping for) an imminent crash. Any experienced investor will tell you property goes in cycles - up and down.

Thanks for the wiki link. Truly academic!

Would you like a hand down from up there Machiaveli or should I send up some more Oxygen?

Nitrous oxide please.

Yes truly academic. Maybe a photo of some tulip bulbs would be easier to read?

As things deteriorate abroad I believe NZ will still be a very desirable place for foreigners with cash to invest in property and housing in the present and future. Currently as that door is left open they will keep coming. The likes of Trump etc only add to that flow. My point is I don't see a huge drop anytime soon when you look at our tiny population vs land mass and the perception foreigners have of NZ. Many see NZ as a life boat when the northern hemisphere falls apart. Are they wrong?

Yes.

Lol, nice, straight to the point. I like that. Make no mistake, I too want the door shut

No your right, NZ is a sanctuary in the south pacific and we have plenty of water round us to keep away the undesirables and those looking to get here illegally. Pretty simple really you pour your money into real estate here and when your country goes down the gurgler you hop on the first plane here and leave the trouble behind you. People with plenty of money have time and means to plan their exit strategy.

Carlos67 - I consider the offshore property speculators to be fairly undesirable. It hasn't stopped them getting in.

...youre talking a two tier economy/society. The haves being largely foreign and the locals being the have nots .. Didn't our forefathers come here to escape such inequality...perhaps thats why the current flag needs to go?

lost for words... keep the flag, throw away the Key

Agreed.

Written bold on my voting form...Waste of time, effort and money.

Also on my previous waste of my time, effort and money, for the Choice Form.

A factor I could not resist....Free post...Yeah right....TUI...Get the picture.

(though it may pay to advertise...my dissent).

Cannot fund Cancer treatment..and many other essentials.but then we have all lost the plot, the the tablets and our minds...

A flag....someones priorities must be sorely lacking in integrity...

Smile and Wave...Tui...everlasting groan.

Tui should have been my choice for the flag...then I could have given it the...BIRD....as well.

Those who want more money spent on medicine are not prohibited from buying medical insurance. I for one prefer choice. The flag symbolizes our national identity and as such is worth making distinctive.

Abolish the dole & minimum wage replacing them with guaranteed jobs cleaning the city / maintaining infrastructure paid at 50% below market rate to encourage people to find jobs themselves before falling back on the guarantee. That will free up more tax dollars for people to spend on their choice of health insurance. Side effects would include currently un-subsidized drugs being made available (based on your insurance) and lower need for public healthcare spending which would free up more tax dollars for individuals to buy better health insurance...

Is there a voice of reason who can cut through all of the spin, bluster, press releases, asking prices, medians and means to give an informed view of Auckland?

The facts as I see it:

Asking prices up - so what. My neighbour was asking for 1.7M for a clapped out state house and has been waiting 4 months to sell. She refuses to think it is worth less. Asking prices are a measure of what?

REINZ stratified index shows falling prices in Auckland since October. No longer publicly available so quite hard to get figures. Anyone have data for February?

Open homes were dead but they've picked up a bit in the last month (Eastern Suburbs).

Clearance rate up for Auctions at least - has the fear set in and people are willing to drop asking price in order to sell?

The Chinese are not back, back , back! There is no reason to expect a change. Offshore Chinese money is staying away for now. All indicators say it is getting harder but IRD registration is a blocker, the money will go to Oz instead.

Barfoots time to sell is high. Listings highest ever.

Sales volumes collapsing. Within the Auckland region, the biggest drop in sales numbers occurred in Manukau where sales were down 31.5% compared to February last year, followed by the central isthmus (within the boundaries of the former Auckland City Council) -22%, Waitakere -15.5%, Rodney -13.8% and North shore -5.1%.

Cowpat made most insightful comment last week: "By the way when I reread Barfoots latest report (for which I am only interested in its churn rate ), I found it revealing that the number of sales lowest since 2011, what was not stated ( and given that they always quote new highs et al ) was that the number of new February listings was the highest for a February month since ever. " Put those two things together and you get a lot of unsold stock.

So I am a bit bearish because when you look at the raw data you just see a peak in October and lots of negative signals for the next few months. And it's shaping up that way in those global cities that have become investment classes in themselves. The top end of London is falling. Sydney clearance rates are falling.

Everyone needs a home, but as an investor you'd surely want to be a grade A nut job to be buying property now and expect capital gains? Even if the echo chamber that is the NZ property media tell you Tauranga is the new Manhattan, the numbers just don't back up the spin. And I haven't even mentioned the collapse of dairy etc.

I can't see anything but a slow deflation in Auckland which might accelerate to more significant falls if the economy continues to go downhill.

More than happy to be convinced otherwise! Just show me some data or local insight...

The Brightline test request foreign tax identification, from what I know the government didn’t follow the rule and skip through this requirement on those Chinese applications – only require the national identification number rather than the tax number (Think about the difference on provide your driver licence number instead of IRD number). That was why Chinese investors were panic when the Brightline test introduced in late last year, and then they see the loop hole require national identification number only as they never paid any tax for the fund for buying house in NZ

Do you think the Chinese authorities would connect the national identification number to a person's tax number? Doesn't sound too difficult...?

if they don't use a fraudulent one I'm sure they could

That is the whole point of the legislation. If a Chinese National now buys a property then it gets reported back to Beijing. The Chinese Government can then ascertain whether the funds were illegally moved out the Country or not.

Big brother is watching you across all borders these days.

The U.K. have clamped down and now there are hardly any foreign buyers in London.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.