Augusta Funds Management is syndicating an industrial property in Queensland, allowing New Zealand investors to invest into the Australian industrial property market with a minimum investment of A$50,000.

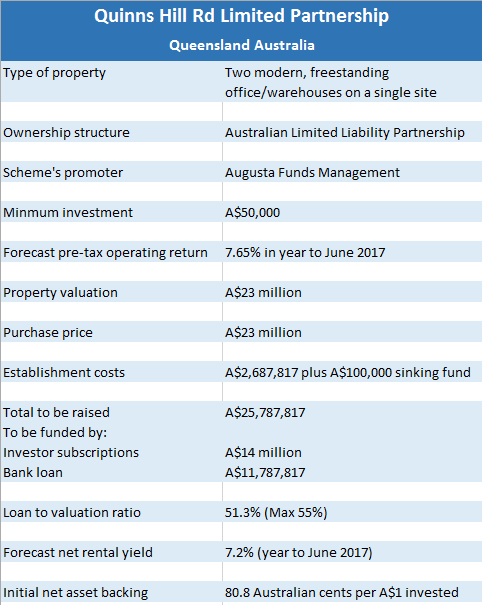

The syndicate, which is being structured as an Australian Limited Liability Partnership will acquire a property at Stapylton in the north west of the City of Gold Coast for A$23 million.

The property contains two large, modern warehouse/office complexes, each with its own tenant on a long term lease (further details are in the attached Product Disclosure Statement).

The syndicate, to be known as the Quinns Hill Road Partnership, is seeking to raise A$14 million from investors (the offer is only open to New Zealand investors) with the balance of the purchase price and the scheme's set up costs to be funded by an A$11,787,817 bank loan.

Syndicates are generally set up to provide their investors with a long term income stream and Quinns Road is forecast to provide a pre-tax operating return of 7.65% in the year to June 2017, with cash distributions to be paid monthly.

It will not have a termination date and will be wound up and surplus capital (after expenses and the repayment of debt) will be distributed to the investors when 75% of the partnership interests vote to do so.

The scheme is broadly similar in structure to most New Zealand-based syndicates and investors will need to consider all of the usual factors that could affect its long term performance, such as the quality of the tenants, movements in Australian mortgage interest rates, general market conditions and the potential to improve the property and add value over time.

But there are also particular implications of investing in an Australian-based scheme, which investors need to consider carefully.

The obvious one is that the cash distributions paid to investors each month, and the amount of capital they receive when the scheme is eventually wound up, will go up or down depending on movements in the prevailing exchange rate when these amounts are converted from Australian to New Zealand dollars.

Another important factor is the effect that Australian stamp duty and capital gains tax will have on the capital return investors receive when the scheme is eventually wound up and the building is sold.

The scheme will pay stamp duty of A$1,376,363 on its purchase of the property and that will come straight out of the investors' equity.

Property syndicates tend to be fairly expensive beasts to set up for the amount of money they raise and stamp duty adds significantly to those costs.

The scheme has set up costs of A$1,311,454 and the biggest component of that is the offeror's fee of A$600,000 which is to be paid to Augusta.

When stamp duty is added it takes the total establishment costs to A$2,687,817, which comes straight out of the investors' equity, reducing their net asset backing at the commencement of the scheme to A$0.808 for every A$1 they invest.

Then at the other end of the scheme's life when it is wound up and the property is sold, capital gains tax will be payable in Australia.

Although the scheme's investors and its managers will be hoping to grow the value of the property over time, the combined effects of stamp duty and capital gains tax will reduce the amount of any capital gain that will be available to be paid out to investors when the scheme is wound up.

Augusta general manager Phil Hinton said it had taken about 2-3 years for the valuations on other properties the company had syndicated and continued to manage in Queensland, to rise to the point where they fully covered the initial set up costs as well as the purchase price.

At that point any further rises in the valuations should start providing investors with an increase in their equity.

See below for the Quinns Hill Road scheme's key financial facts and a link to its Product Disclosure Statement.

Click on the following link to download the scheme's Product Disclosure Statement:

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter"and enter your email address.

2 Comments

I suggest taking a quick look at the breakdown of fees as your starting point on this one. Already a few questions I would have.

These syndicated properties are meeting a need. I attended a presentation on the scheme today. At no point did they actually say what the net rate of return on the investment was so one could compare their property with a local investment. They just talked about the yield or internal rate of return. My back of an envelope calculation is it makes 6.3% net before management costs. But then a fully managed syndicate gets a small investor into the business without all the issues investors face dealing with tenants, banks, accountants, and maintenance issues.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.