House price gains are continuing to grind to a halt in the Auckland area but things remain buoyant in some other parts of the country.

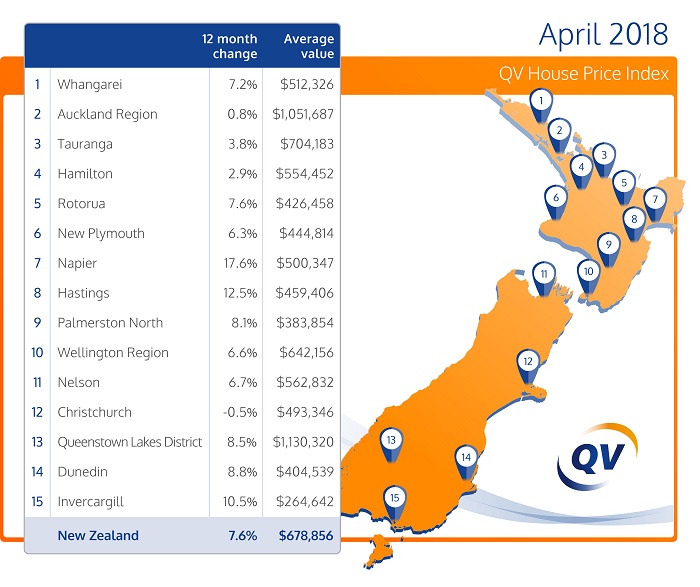

According to Quotable Value, the average value of nationwide residential property values for April increased by 7.6% over the past year (up from 7.3% as of March). The nationwide average value is now $678,856. When adjusted for inflation the nationwide annual increase drops slightly to 6.4%.

Meanwhile, residential property value growth across the Auckland Region increased by just 0.8% year on year (down from 1% as of March). A year ago the Auckland region was experiencing annual house price growth of 10.7% - and that was then the slowest rate since 2014.

The average value for the Auckland Region is now $1,051,687. When adjusted for inflation values actually dropped 0.3% over the past year.

QV general manager David Nagel said many regional centres were continuing to see steady increases in price, "while the rate of growth continues to slow, plateau or even drop slightly in the main centres".

He thought this was partly due to a continued trend of people seeking a lifestyle change away from the cities and purchasing better-valued properties in the regions, particularly those regions that are within commutable distances of major centres.

Nagel said annual value growth also remained flat in Christchurch, while the Hamilton, Tauranga and Dunedin markets continued to rise moderately.

"The slowdown in value growth can be partly attributed to the usual seasonal slowdown in activity as we approach the winter months and also the fact that many people, particularly investors, are not expecting significant capital growth in the coming months so are less active in the market.

“Despite the fact that home values remain high, first home buyer activity is increasing particularly in Wellington and Dunedin – as people take advantage of their KiwiSaver funds as deposits.

"The higher proportion of first home buyer actively is largely due to rising rents which mean it can often be as affordable to purchase an entry level home and pay a mortgage, as it is to rent a home.

"However, for many, raising a deposit is still a bridge too far to cross to be able to gain entry into the housing market."

QV says that values across the Auckland market are varying, although not significantly. North Shore values rose 3.2% in the year to April, with an average value there now $1,233, 394. The former Auckland City Council central suburbs rose 0.6% year on year and the average value there is now $1,086,879. Waitakere values dropped 0.2% year on year. Manukau dropped by 0.3% year on year; Papakura values rose 1.1% year on year a and the average value there is now $701,123; Franklin values also rose 0.2% year on year and Rodney values were also up 0.1% year on year.

QV Auckland senior consultant, James Steele said there is still a good amount of activity taking place across Auckland, however, values remain flat. "We are seeing strong interest from first home buyers, who are making the most of a drop in investor activity, and a slight easing of lending criteria and relatively low interest rates.

"A number of first home buyers are targeting the sub-$600k price bracket in order to obtain the KiwiSaver HomeStart grant but those unwilling to compromise on size or locations are finding these criteria difficult to meet.

"Listings are staying on the market for a longer period of time and fewer properties are going at auction, providing more opportunity to negotiate and place conditional offers which is benefiting buyers."

Hamilton City home values increased 2.9% in the year to April. The average value in Hamilton is now $554,452 and QV Hamilton property consultant Andrew Jaques said, overall, "it’s a steady market".

Tauranga home values rose 3.8% year on year and the average value in the city is $704,183. The Western Bay of Plenty market rose 6.8% year on year and 2.2% over the past three months. The average value in the district is now $630,703.

QV Tauranga property consultant, Steven Dunn said Tauranga continues to see good interest especially for those looking to purchase in the higher price bracket as well as from first home buyers.

"However, across the board values appear to have stabilised and we continue to see buyers are taking longer to complete due diligence before purchasing."

Wellington had an annual rate of growth of 6.6%. The average value is now $642,156.

QV Wellington senior consultant, David Cornford said market conditions in Wellington are pretty stable with modest value growth.

“The number of days to sell has increased slightly but is still significantly lower than the long term average and overall the market is robust.”

Christchurch City values continue recent trends, either remaining flat or seeing slight increases or decreases in value. Values dropped slightly by 0.5% year on year with the average value in the city now $493,346.

QV Christchurch property consultant Hamish Collins said the market remains steady in terms of value growth.

"Well-maintained property continues to sell well although this is often dependent on the seller being willing to negotiate on price. We are observing that discounts are being offered on a good portion of properties that are sold although these discounts are not overly substantial."

Values in Dunedin continue their upward trend having increased 8.8% in the year to April, with the average value in the city at $404,539.

QV Dunedin property consultant, Aidan Young said the market has slowed but values remain stable overall and there appears to be a bit of a mixed sentiment.

"Dunedin continues to provide a lower entry point when compared to many other parts of New Zealand."

See below for the average dwelling prices in all parts of the country and their movements over the 12 months to April.

QV House Price Index - April 2018

| Territorial authority | Average current value | 12 month change% |

| Auckland Region | 1,051,687 | 0.8% |

| Wellington Region | 642,156 | 6.6% |

| Main Urban Areas | 794,929 | 6.5% |

| Total New Zealand Nationwide | 678,856 | 7.6% |

| Far North | 429,640 | 6.9% |

| Whangarei | 512,326 | 7.2% |

| Kaipara | 524,681 | 6.4% |

| Auckland - Rodney | 958,130 | 0.1% |

| Rodney - Hibiscus Coast | 939,821 | 1.0% |

| Rodney - North | 977,649 | -0.9% |

| Auckland - North Shore | 1,233,394 | 3.2% |

| North Shore - Coastal | 1,418,758 | 3.6% |

| North Shore - Onewa | 971,425 | 2.4% |

| North Shore - North Harbour | 1,214,201 | 3.0% |

| Auckland - Waitakere | 824,631 | -0.2% |

| Auckland - City | 1,232,850 | 0.8% |

| Auckland City - Central | 1,086,879 | 0.6% |

| Auckland_City - East | 1,550,784 | 1.8% |

| Auckland City - South | 1,090,785 | -0.7% |

| Auckland City - Islands | 1,142,511 | 7.6% |

| Auckland - Manukau | 900,095 | -0.3% |

| Manukau - East | 1,152,825 | -1.7% |

| Manukau - Central | 697,708 | 2.4% |

| Manukau - North West | 778,373 | 0.3% |

| Auckland - Papakura | 701,123 | 1.1% |

| Auckland - Franklin | 670,785 | 0.2% |

| Thames Coromandel | 727,825 | 5.4% |

| Hauraki | 390,049 | 10.7% |

| Waikato | 478,199 | 6.3% |

| Matamata Piako | 434,872 | 6.1% |

| Hamilton | 554,452 | 2.9% |

| Hamilton - North East | 700,007 | 2.5% |

| Hamilton - Central & North West | 513,328 | 2.1% |

| Hamilton - South East | 503,222 | 2.8% |

| Hamilton - South West | 492,644 | 3.7% |

| Waipa | 536,369 | 7.1% |

| Otorohanga | 310,287 | 21.0% |

| South Waikato | 227,230 | 14.6% |

| Waitomo | 189,539 | 12.1% |

| Taupo | 469,232 | 7.1% |

| Western BOP | 630,703 | 6.8% |

| Tauranga | 704,183 | 3.8% |

| Rotorua | 426,458 | 7.6% |

| Whakatane | 427,494 | 9.0% |

| Kawerau | 193,629 | 8.8% |

| Opotiki | 316,431 | 10.9% |

| Gisborne | 310,283 | 10.9% |

| Wairoa | 168,881 | 1.5% |

| Hastings | 459,406 | 12.5% |

| Napier | 500,347 | 17.6% |

| Central Hawkes Bay | 315,767 | 19.8% |

| New Plymouth | 444,814 | 6.3% |

| Stratford | 261,449 | 11.8% |

| South Taranaki | 220,658 | 10.3% |

| Ruapehu | 185,261 | 11.5% |

| Whanganui | 244,293 | 10.9% |

| Rangitikei | 201,728 | 9.0% |

| Manawatu | 335,839 | 11.2% |

| Palmerston North | 383,854 | 8.1% |

| Tararua | 192,245 | 8.5% |

| Horowhenua | 308,273 | 15.6% |

| Kapiti Coast | 556,894 | 13.4% |

| Porirua | 548,008 | 7.3% |

| Upper Hutt | 486,862 | 9.3% |

| Hutt | 537,556 | 6.8% |

| Wellington | 761,400 | 5.1% |

| Wellington - Central & South | 755,217 | 4.7% |

| Wellington - East | 813,497 | 3.6% |

| Wellington - North | 687,873 | 6.3% |

| Wellington - West | 882,892 | 5.2% |

| Masterton | 338,665 | 16.4% |

| Carterton | 387,727 | 17.6% |

| South Wairarapa | 477,960 | 23.0% |

| Tasman | 565,906 | 8.5% |

| Nelson | 562,832 | 6.7% |

| Marlborough | 457,935 | 6.9% |

| Kaikoura | N/A | N/A |

| Buller | 179,227 | -4.8% |

| Grey | 212,262 | 0.6% |

| Westland | 246,411 | 3.5% |

| Hurunui | 389,074 | 5.1% |

| Waimakariri | 441,774 | 0.0% |

| Christchurch | 493,346 | -0.5% |

| Christchurch - East | 369,448 | -0.4% |

| Christchurch - Hills | 662,855 | -1.4% |

| Christchurch - Central & North | 580,031 | -0.9% |

| Christchurch - Southwest | 475,337 | 0.0% |

| Christchurch - Banks Peninsula | 513,244 | 2.5% |

| Selwyn | 550,036 | 0.9% |

| Ashburton | 352,568 | 1.4% |

| Timaru | 355,389 | 6.0% |

| MacKenzie | 510,957 | 12.1% |

| Waimate | 236,036 | 7.3% |

| Waitaki | 304,665 | 13.8% |

| Central Otago | 488,488 | 12.4% |

| Queenstown Lakes | 1,130,320 | 8.5% |

| Dunedin | 404,539 | 8.8% |

| Dunedin - Central & North | 418,991 | 8.8% |

| Dunedin - Peninsular & Coastal | 368,480 | 6.4% |

| Dunedin - South | 386,807 | 9.8% |

| Dunedin - Taieri | 419,638 | 8.8% |

| Clutha | 213,369 | 12.5% |

| Southland | 273,561 | 10.3% |

| Gore | 228,934 | 9.1% |

| Invercargill | 264,642 | 10.5% |

No chart with that title exists.

65 Comments

The housing market is slow - but prices are holding.

Nothing new.

TTP

Incorrect, when adjusting for inflation, prices in Auckland and Christchurch are now falling. FHB are gaining ground by earning interest on their term deposits, no rates, maintenance or insurance. This is great news, but it is very much early days of what could be a long term period stagnation of say ten years. If so, for FHB, there is no hurry. I think it's worth noting that this "toppy" housing market is marking time as a sitting duck to an undesirable offshore sourced event. It would easily collapse "Ireland" style.

Hi R-P,

Sorry - but you're mistaken.

When you factor in the (rental) return, then the house owner is still comfortably ahead.

And, notably, rents have been rising quite rapidly. (Population pressures make this inevitable.)

TTP

Disagree, rental yields are sub 3%. Yields when compared to relative risk free term deposits are abysmal. Doesn't add up. Minus the capital gains, its a lousy investment for the novice Landlord/speculator, poor timing for the first home buyer. Remember, Ireland had population pressures too, then the work ran out.

Hi R-P,

You should note that inflation (measured by the CPI) is much lower than the typical rental yield.

Further, the average house price in NZ has increased by 7.6 percent over the last year, according to the latest data. (Even Auckland is still ahead on the numbers.)

So housing still shapes up pretty well as an investment. Certainly better than bank deposits.

TTP

You are correct TTP, it is a steady ship at present. I'd like to see Auckland Central East rise further than the current $1,550,784. Should be around the $2m mark.

Yawn......

I have learnt so much from the optimists on this website - particularly about the ability to take past trends and extrapolate them

For instance - my daughter has grown six inches in the past five years. On this basis I know for a fact that she will be 8ft 9 by the time she is thirty and that I should ignore anyone else's experience with daughters (here or overseas) and just understand that her eventually being 10 foot tall is inevitable.

You failed to factor in the inevitable height bubble burst (HBB) factor. Following 10 years of growth a HBB correction is required which will result in your daughter devaluing from 5 feet to 2 feet. This will be due to ring fenced growth hormones and a reduction in calcium immigration. Combined with the increase in the supply of children through Government programmes she will ultimately be 8 inches tall...

Works both ways.... Pessimist.

Clearly, ex socialist has reached a new intellectual peak.......

But let’s hope his daughter is even smarter.

TTP

Ex socialist is mentoring a daughter who will represent the smarter generation of FHB. She will stand financially tall remembering how she followed the sound advice of her father and steered clear of village idiots.

The smarter generation of FHB will recognise that the most important decision that they will make is not when they buy, but who they buy it with (assuming that two incomes are the norm rather than the exception these days).

10 ft financially tall.

You're assuming no mortgage - if the house is leveraged then that multiplies the losses. A larger mortgage also reduces the rental return as mortgage rates are higher than typical Auckland yields.

Chch is different, here we have falling house prices and falling rents.

You're assuming the depositer has not borrowed the funds. Someone may borrow a personal loan at 18% and place the funds in a term depsoit at 3.5% (if they are nuts).

Buying a house with the borrowed finds is looking better with mortage at 4.5% even if the rental yield barely pays the mortgage a homeowner may still come out on top with the capital gain.

Your scenario of a cashed up depositer versus a borrowing house buyer is apples and oranges.

I wasn't talking about depositors. Yes leverage works out well when there is a capital gain, but the other edge of the sword is it magnifies losses which is what Auckland and Christchurch are currently experiencing (admittedly only to a very small degree). In Auckland, rental yield is very unlikely to cover interest if bought recently with a chunky mortgage.

Edit: actually I'm wrong to use the real price fall in Auckland in this case, I should be using the nominal raise which is magnified, then degraded by inflation after that. My apologies. My original point still applies to chch.

The OP and responder were (TTP and Retired Poppy). You might want to stay on point next time instead of straw-manning the conversation.

OK then, sure. How many term deposit owners do you think borrow money to invest? How many property investors do you think borrow money to invest? I think it's very reasonable to assume leverage in one case and not the other as that is how it's done in the vast majority of cases.

I will happily agree that to properly compare, the total value of the term deposit should = the size of the deposit rather than the value of the property. I don't think this changes the out come of the maths, as at present in Auckland the mortgage interest rate is larger than the typical rental yield, and capital gains are essentially non-existent.

If I were to do a more complete comparison, I would not have compared property to term deposits, I'd probably compare to share market investments, which in NZ often have a higher yield than property and a similarly impressive record of capital gains over the last few years. Or perhaps peer to peer lending, which sees returns of ~8-10% at a minimum (admittedly with a different risk profile).

No they're not TTP, if you look at the QV figures today, Wellington, Auckland and Tauranga all had 0.4% declines last month and Christchurch and Hamilton also saw big falls in April too. Having seen 12 months of low volumes and pressure building on sellers, the market is now in an early phase of a collapse. Hi I'm Nic Johnson and I'll be here all week.

Hey Nic, hang around, it may be funny.

I'm hoping its at the top of a peak, and its like a Dam which is starting to get a few cracks in it, slowly weakening with each new measure the government implements. Plus with outside forces coming to bare like credit tightening, the eventual increase in rates.

Planes still glide for a while on low power to. Would suggest there has been a decline in the outer Awkland specuvestor box land. Hasent reached central yet but for every central sale theres plenty being passed in.

Hi Averageman,

You write, "Planes still glide for a while on low power to."

But the "property plane" is gliding with quite reasonable power - especially with the added thrust from strong first home buyer activity. (See, for example, the headline in today's Dominion Post: buying a [first] home makes more sense than renting.)

TTP

Can we get this right.

There is no "strong thrust" from FHB.

It is true that the share of FHB mortgages hit the $900m in March as reported by interest.co the other day. However, NZRB figures show that the NUMBER of FHB mortgages were 2,044 in March 2016 and in March 2018 they were 2295. A 11% increase is not a strong thrust; it simply reflects improved affordability (read as falling prices relative to income) with prices at best plateauing.

If you are relying on your so called "strong (11%) thrust" from FHB, then consider the RBNZ figures that for investors, the number of mortgages in March 2016 was 6,426 and in March 2018 only 4,004 a drop of 38% - which I do call strong.

In terms of the state of the market; FHB are buying for intrinsic reasons based on affordability, investors are buying for economic reasons and the biggie is their thoughts are as to where the market is going in the near future.

So forget the "strong trust" from first FHB - its just a desperate comment.

The growth in FHB will also be partly attributable to population growth

You've replied to him with actual numbers, zero chance that you'll get a response.

TTP.. That was a sponsored article trying to talk buyers into the market given how low volumes are now nationwide - in the absence of investors, they need FHB's more than ever to stop the collapse. What wasn't reported was the 5 of 6 main centres saw prices fall between 0.2 and 0.4%. (QV figures not mine) only Dunedin was spared. Big falls for one month wouldn't you say but the sign of things to come. I think the second engine on the debt Ponzi plane may also be running out of gas now! I'm Nic Johnson and it's been nice to meet.

As I said before, while banks are willing to lend, FHB's will keep over extending themselves. Unfortunately this pool is a lot smaller than say China. Hence the "gliding" analogy.

Meanwhile across the ditch the plane have started to nosedive:http://www.abc.net.au/news/2018-05-01/sydney-melbourne-housing-property…

Oh my.. maybe the likes of ttp, dgz,yvil, Eco bird, ex expat.. can go over the ditch to try rescue the drowning ship.. just as they do here

I appreciate the mention with this group, but I’m not worthy. I just occasionally mention sales in 1071, have no investment property and no intention of selling my family home. Btw I’ve never even considered buying in Australia as their stamp duty is ridiculously expensive.

Fair enough

Why should stamp duty matter when housing is such a foolproof investment.

Does Interest.co.nz have access to numbers on what proportion of FHBs are dipping into their kiwisaver?

I would suspect close to 100% but it would be good to have hard data

.

Excellent sleuthing, thanks Pragmatist!

If the kiwisaver withdrawal scheme was stopped, what value would first homes fall to?

EDIT: I'll have a go:

House values: $911M / 0.8 = $1139M

Deposits: $1139M * 0.2 = $227.8M

Deposits less kiwisaver: $227.8M - $80M = $147.8M

Values of houses able to be bought without kiwisaver: $147.8M / 0.2 = $739M

First homes drop in value to: 739/1139 * 100% = 64.9%

Hmm... The economy is a very complex system, so I don't dare to draw the conclusion that house prices could fall by this much, but it's clear that kiwisaver withdrawals likely have a significant effect on house prices in NZ

.

If Kiwisaver withdrawals are such an important source of FHB deposits, then why limit them to the savings at the time of purchase? If you allowed say the next two years of contributions to be routed to debt repayment then it would enhance the FHB buying power against the Investors.

.

And even if thats not the case, allowing them to capitiise future earnings and push prices and therefore debt to even more stupid levels seems like a really daft idea.

I hear you. Great contributions too. You're on a roll.

Good luck with your strategy. So that leaves you with hoping that buying a house in future is like waiting for a bus where it will be good if everyone waits nicely in line based on their arrival at the stop until the scheduled bus arrives, then everyone pays the same fare and everyone gets their desired seat. That works nicely until the bus doesn't arrive, someone jumps the queue and/or there aren't enough seats.

.

And even if thats not the case, allowing them to capitiise future earnings and push prices and therefore debt to even more stupid levels seems like a really daft idea.

Excellent comment. It's a shame there are so few forms of immunisation to this lunacy you have just described.

.

That's a lot of retirements ruined. All the lost compounding gains and starting retirement savings from scratch. Then factor in the lost cash flow to either the economy or retirement savings which the median mortgage payment being around 50% more than the cost of renting.

These statistics look bad from a personal finance perspective.

.

A couple saving for a house can easily take 10 or so years from when they start working which puts them in their 30s. We have a heap of problems on the horizon.

Also probably have to pay off their student loans in that time too.

And that's the bigger problem. Just look at contributions for the month of March 2018: http://www.kiwisaver.govt.nz/statistics/monthly/contributions/

Withdrawals are 20% of contributions.

I hear the Sex Pistols, God Save the Queen: "Noooooooo future! Noooooooo future for yooouuuu!"

.

Yeah I edited my comment when I took another squiz at the charts. At least some people will retire.

I wonder if the government has done any due diligence on the financial advisory front? Encouraging FHBs to dip into their kiwisaver is a form of financial advice, right?

I don't think any Government is seriously looking ahead. They are probably putting in as much effort as they did in managing the Government employee pension which is so underfunded and poorly invested that 75% of the pension payouts are bailed out by current tax payers (even though the scheme was scrapped).

And that's the bigger problem. Just look at contributions for the month of March 2018: http://www.kiwisaver.govt.nz/statistics/monthly/contributions/

Withdrawals are 20% of contributions.

And the highest monthly withdrawal on record since the first month of introduction. 19% higher than the monthly average since introduction.

A Mexican stand-off brewing between buyers and sellers.

In this stand-off, RE agents would be an unhappy lot. No sale, no commission.

Buyers of course have the option of renting.Never mind if rentals have increased. The reduction in house prices over the waiting period may still outstrip the rent.

So in this stand-off, who would blink first?

MFD, Chch rents are not falling at all for the above average investor.

Our rents overall are up on previous years.

House prices are flat but certainly not dropping from what I am seeing, and why would investors worry about prices anyway if they are getting goods returns?

The reality is that so many new houses and repaired houses are around so it is amazing that prices haven’t dropped substantially, but people still want to buy and the homes are very good value for money.

The thing is that Chch is a very desirable place and will continue to be so in the future!

MFD, Chch rents are not falling at all for the above average investor.

...So rents are falling for at least 50% of investors?

.

His comments are so full of desperation to justify his position and anger since Labour won the election. The fact that Auckland has a population about five times the size of poor old Christchurch says it all. Auckland is the place to live and accordingly large capital gains have been made. Christchurch is out on a limb, is freezing cold in the winter and it has been devastated by the recent earthquakes. Hence rents and house values surely but steadily dropping.

Gordon, Gordon, Gordon, no desperation at all but I can tell that there is so much jealousy going on from your side for property investors!

You stick to Auckland Gordon Where returns are not positively geared and air will stick to cold Chch where I can make a great living from providing a social service by providing accommodation for people who want to rent!

Our rents are not decreasing and values are increasing steadily!

Offer still there Gordon, go on take it up!

I have no need to resort to residential property investment The Boy as I have my commercial properties, equities and residential subdivisions. If I was desperate enough to go residential property investment I would still chose Auckland first as people actually want to live there as proved by the population difference between Auckland and poor old Christchurch. The Boy one of my commercials would dwarf your as is where is rubbish in Christchurch.

I prefer data to anecdote where possible, so I feel comfortable saying rents and prices are falling. Not dramatically, and I don't expect either to fall dramatically here. I'm certainly not feeling any pressure to buy any time soon. Agree the city is desirable and the stable property market is just another attractive feature.

Planes actually glide on no power but still descend at a rate dependent on the attitude and airspeed but eventually they end up on the ground

Mum and Dad investors won't be worried about inflation or falling house prices.They know that at the end of the day when they sell their property ,the payoff will come.

And therein lies the problem.

The reliance on thinking the value of your property is always going to go up.

And also knowing that Mum and and Dad investors are also voters. So Govt is not going to ignore them.

It is a vicious cycle.

The brand-new FHBs are getting advice that interest rate & inflation are NOT going to increase in near future. And no-one knows when interest rate gonna go up

Meanwhile I'll still wait as I missed the bus 4 years ago and will sit on my savings @3% interest ( minus tax). Definitely not a winner; but don't want to take this huge mortgage of many times of my annual salary.

Just wondering is there any bond/ fund where I can invest , so that I can look at buying a house some 6 years down the line ? Expect advices from u-can't-lose-on-house and so called 'DGM' merchants . thanks

No point asking for advice on here, its all one side of the fence or the other. What you have to realize is that everyone cannot be on one side of the fence so there is no right or wrong. The simple answer is if you can afford a mortgage, have a good job then buy a house. It worked for me. Now I'm investing money and its 3.50% currently for 12 months.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.